You Might Live Longer Than You Think. Here's How to Invest for It.

By the time you retire, the odds are great that you'll live to be 85 or older. And that means your risk and spending needs won't be static.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Imagine being told that the way you invest at 62 is how you should invest at 82. Same risk profile. Same rules. Same assumptions.

That's crazy. Right?

Yet, that’s how a lot of traditional retirement planning still works, and it’s exactly why so many plans feel overly cautious early on and strangely disconnected later in life.

I want to look at why that static assumption is outdated, and what the research really says about dynamic portfolios, dynamic spending, and how your risk could shift over time.

The Assumptions Are Simplistic

Traditional retirement rules, like fixed withdrawal percentages that never change, are built around simplicity, not reality.

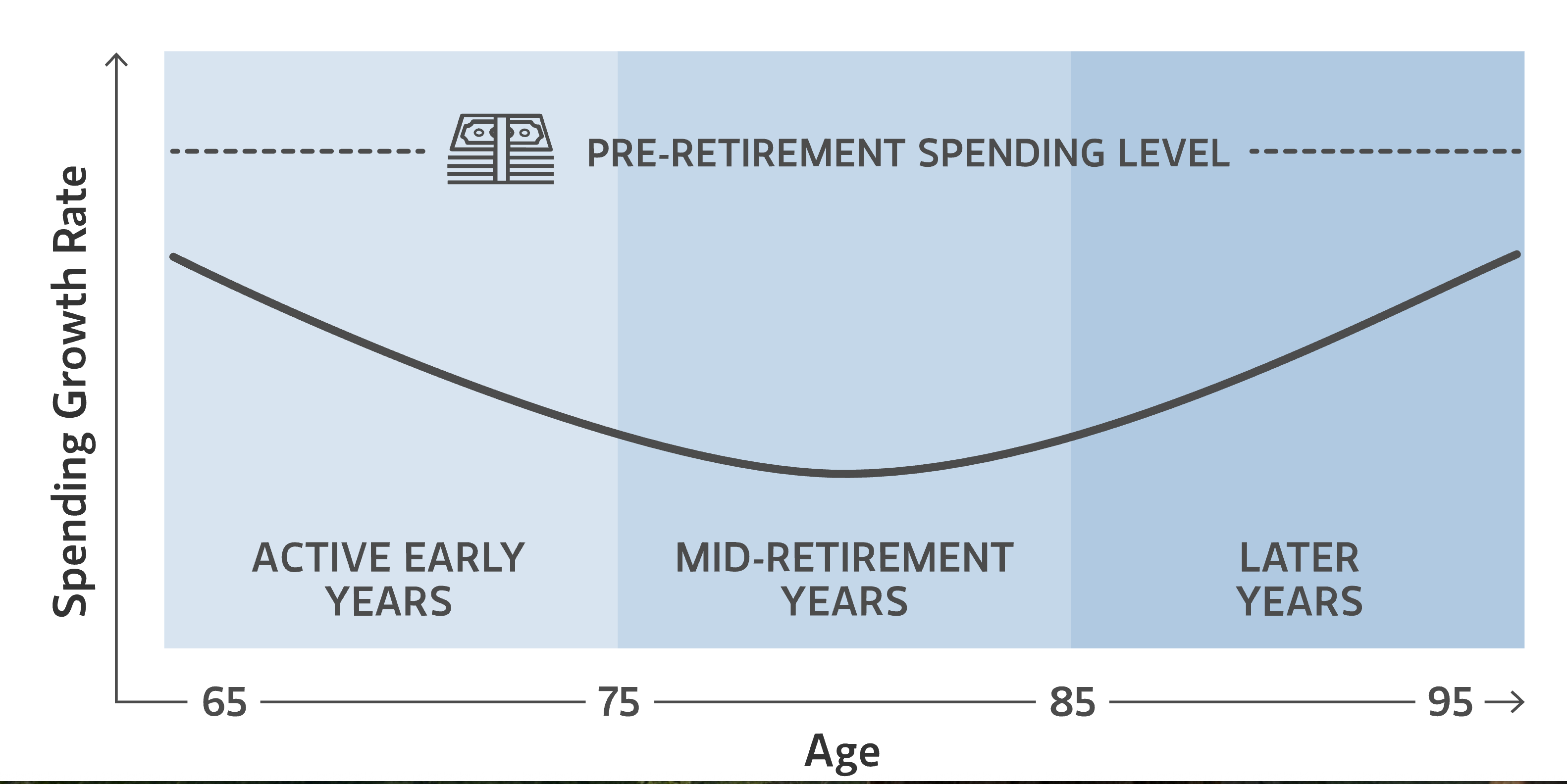

This image from Morgan Stanley illustrates how spending tends to evolve over the course of a retirement that can last 30 years or more.

Over time, not only do markets fluctuate, but your spending needs change, and your income sources evolve. What starts as a portfolio-heavy income stream is gradually layered with Social Security, Medicare, and other forms of payment, potentially reducing how much heavy lifting your investments need to do.

In a November column for Kiplinger, Mike Palmer, CFP, a managing principal at Ark Royal Wealth Management in Raleigh, North Carolina, wrote, “When it comes to retirement planning, a ‘set-it-and-forget-it’ strategy is unlikely to work.”

The 4% “Rule” is Really a Guideline

Last year, I interviewed William Bengen, the retired financial planner who first popularized the 4% rule. He told me that this guideline was never meant to be a static prescription.

In his 2025 book, “A Richer Retirement: Supercharging the 4% Rule to Spend More and Enjoy More,” Bengen wrote that there’s more to the familiar rule than meets the eye.

Here’s what he told me in the interview, published in U.S. News & World Report:

"The 4% rule isn’t really a rule; it’s a process. My new research looks at 10 variables that affect retirement income, and eight of them you have control over. This book builds on everything I’ve learned over the past 30 years and shows how retirees can safely increase their withdrawal rate without taking on more risk."

What does that mean in practice?

- Bengen is now comfortable suggesting 4.7% and even slightly higher starting withdrawal rates than 4% in many scenarios.

- Those more flexible rates assume intentional design, not blind repetition.

Risk is Dynamic, Not Static

For example, early in retirement, a balanced portfolio may include ETFs like these (not necessarily all - these are examples of what you might own).

- iShares 0-3 Month Treasury Bond ETF (SGOV)

- iShares 1-3 Year Treasury Bond ETF (SHY)

- Vanguard Total Stock Market Index Fund ETF (VTI)

- SPDR S&P 500 ETF (SPY)

Later, once Social Security is firmly in place, the portfolio can rely more on differing core funds. Those might include:

- Vanguard Total Bond Market Index ETF (BND)

- iShares Core US Aggregate Bond ETF (AGG)

- Schwab US Dividend Equity ETF (SCHD)

Now, don’t go creating a portfolio using those funds. These are just examples of how your allocations may change over the course of retirement.

Not the Same as Reckless Risk

One fear people sometimes have is: “If I stop being static, aren’t I just taking on more risk?”

Not necessarily.

Dynamic planning is pretty simple, in theory. It just means taking risk where it makes sense, and reducing it where it doesn’t.

Research and practice show that:

- In early retirement, when spending is front-loaded and sequence risk is high, you can benefit from reserves and flexible strategies.

- Later, after guaranteed income streams like Social Security are in place, your portfolio’s time horizon shortens, and a moderate amount of additional risk can actually support sustainability.

- So rather than being “all stocks” or “all bonds,” a dynamic portfolio adjusts its role according to what a retiree actually needs when they need it.

Rising Glidepath to Improve Outcomes

This isn’t a new idea.

As long ago as 2013, financial author and planner Michael Kitces wrote:

“Recent research shows that despite the contrary nature of the strategy - allowing equity exposure to increase during retirement when conventional wisdom suggests it should decline as clients age - it turns out that a ‘rising equity glidepath’ actually does improve retirement outcomes! If market returns are bad in the early years, a rising equity glidepath ensures that clients will dollar cost average into markets at cheaper and cheaper valuations.”

What This Doesn’t Mean

Adding equities to a portfolio sounds exciting, and it’s certainly been a great strategy for the past 17 years (mostly).

But figuring out the correct glidepath is not the same as ditching the more conservative investments and owning just high-beta stocks like Micron (MU) .

Most retirement planning still assumes that the way you invest at 62 should look the same at 82, and that’s a big mistake.

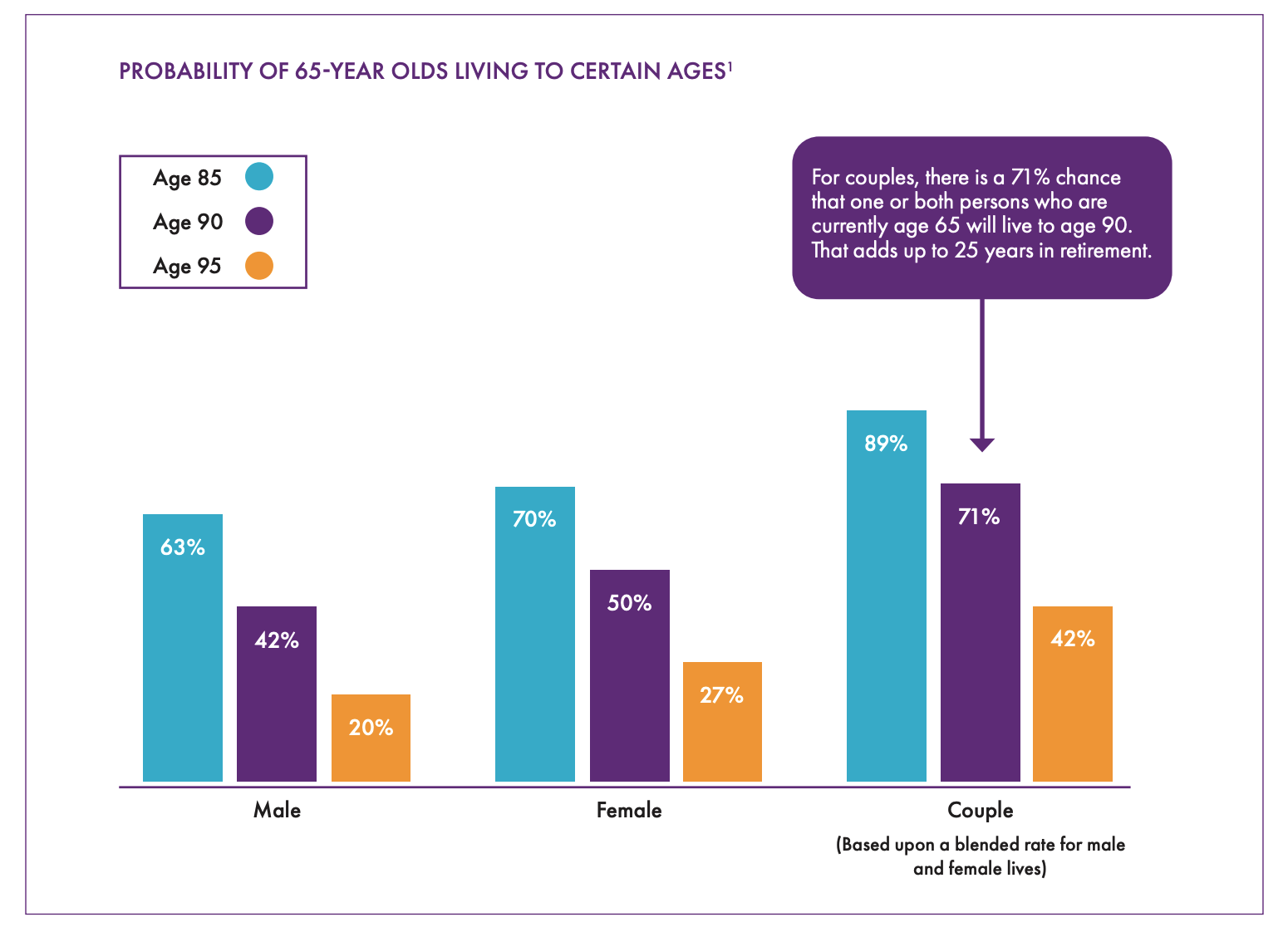

Most people don’t realize this, but if you live to 65, you’ve already “cleared” a bunch of earlier mortality risk, so the odds of reaching 85 are conditional on having already survived to 65. In other words, at 65, you may have a better chance of living to 85 than you did at 30.

This image from Lenox Advisors shows the probability of a 65-year-old living to 85, 90, or 95. The odds of living to 85 are pretty good!

So those tables that say the average life expectancy is 76? For the most part, they can be ignored, as they include data pertinent to people who died young.

So this likelihood of living a long time in retirement means you’ll need more income. The old-fashioned conservative approach of investing in bonds may not cut it; the recommendation of fine-tuning your risk assets may be a better approach.