Why One Stock Won’t Rescue Your Retirement

Even so-called safe stocks can be risky

You've reached your free article limit

You've read 0 of 1 free Pro articles.

“Danger Will Robinson!”

In the 1960s show “Lost in Space” a robot would warn humans of imminent danger, accompanied by a flashing red light and a, well, robotic voice.

I thought of that when I recently saw an article on a different financial-media site urging people to augment their retirement savings by investing in a single stock.

You won’t put your retirement savings at any risk with that, no sirree. (And in case that wasn’t clear, here’s the /sarc tag.)

On top of that, the headline writer termed the recommended stock “extremely safe.”

For the record, there’s no such thing as an “extremely safe” stock, although a stock with a long track record of paying dividends is likely to continue that streak, which is what I think the writers were getting at. Still, “extremely safe” is potentially dangerous hyperbole.

Some Dividends Can Be Considered Safe

Be wary of retirement advice that centers on a single stock.

Now, before we drill down to that topic a little more, I need to say: Some stocks do have long histories of paying and increasing their dividends.

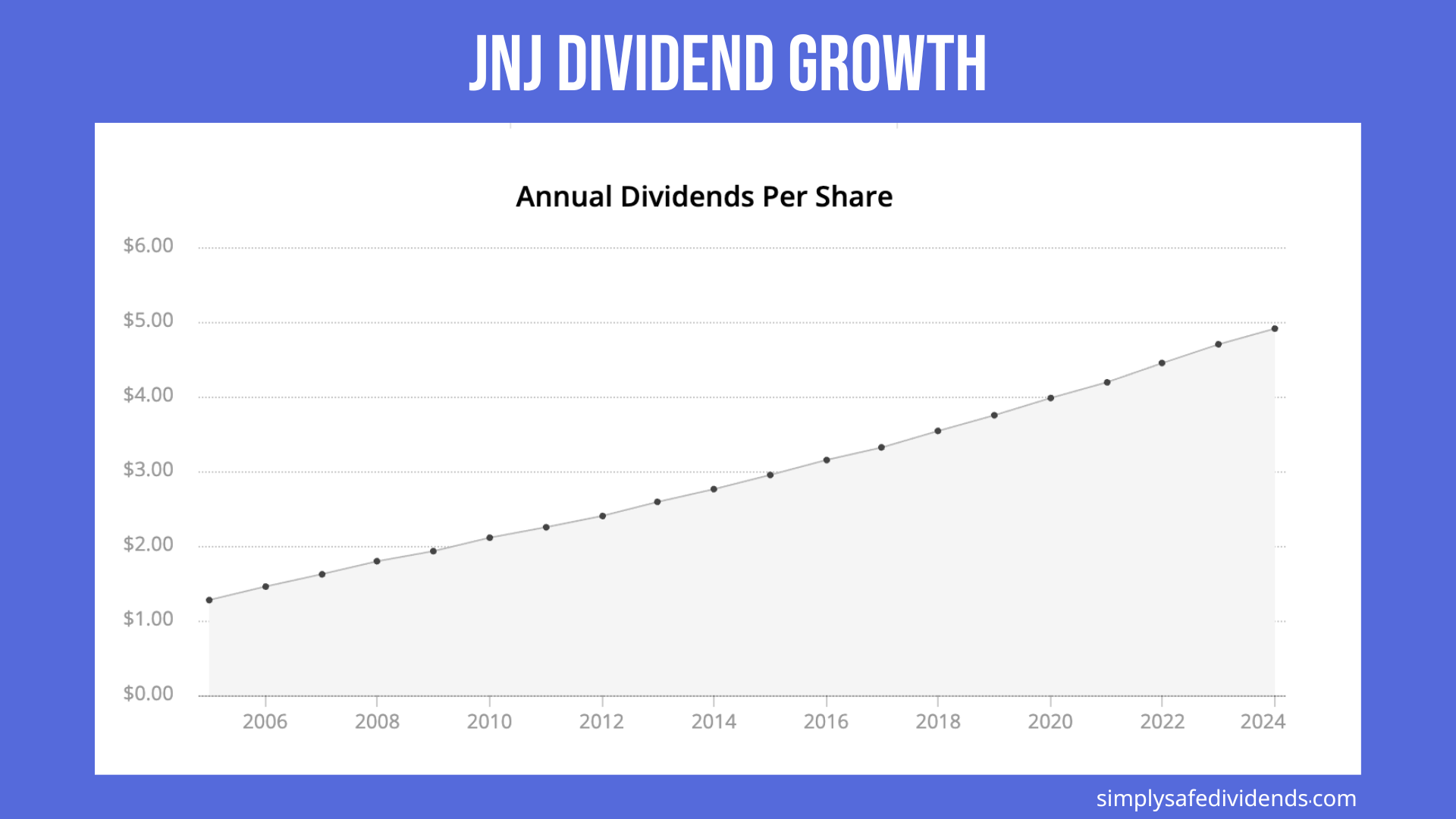

For example, health-care stalwart Johnson & Johnson JNJ has paid a dividend for 109 years, and it’s increased its payout for 62 consecutive years, putting it in the ranks of Dividend Kings.

Dividend-data aggregator Simply Safe Dividends calls Dividend Kings a “rare breed of companies that have raised their dividend for 50 or more consecutive years. These are outstanding businesses that have survived everything from economic recessions to major technological advancements.”

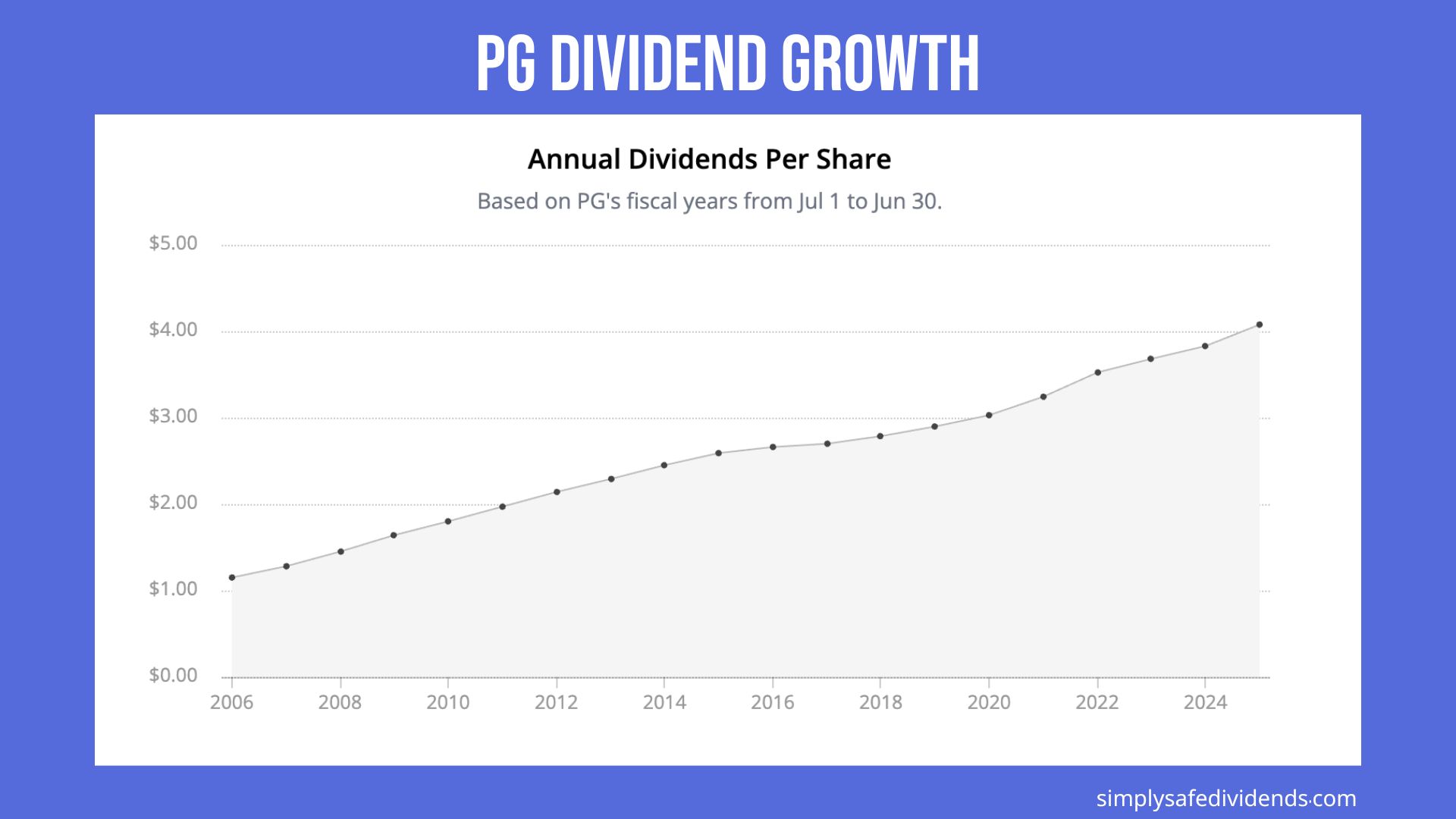

Procter & Gamble PG is another member of the dividend royal family, boasting an uninterrupted dividend streak of 135 years and a dividend-growth streak of 69 years.

It’s perfectly fine to say those companies have safe and reliable dividend payouts. In both cases, earnings payout and free cash flow ratios support continued returns of capital to shareholders through dividends.

Why You Can’t Call Any Stock 'Extremely Safe'

Yet even the most stable-seeming stock carries risk. It actually makes intuitive sense: The traditional retirement portfolio, with 60% in equities and 40% in bonds and cash, is riskier than a 50%-50% portfolio.

You can extrapolate from that why basing too much of your retirement savings on a single company, even a large-cap blue chip, isn’t wise. Some stocks might appear safer because they have betas lower than 1, meaning their price typically moves less than the broader market does.

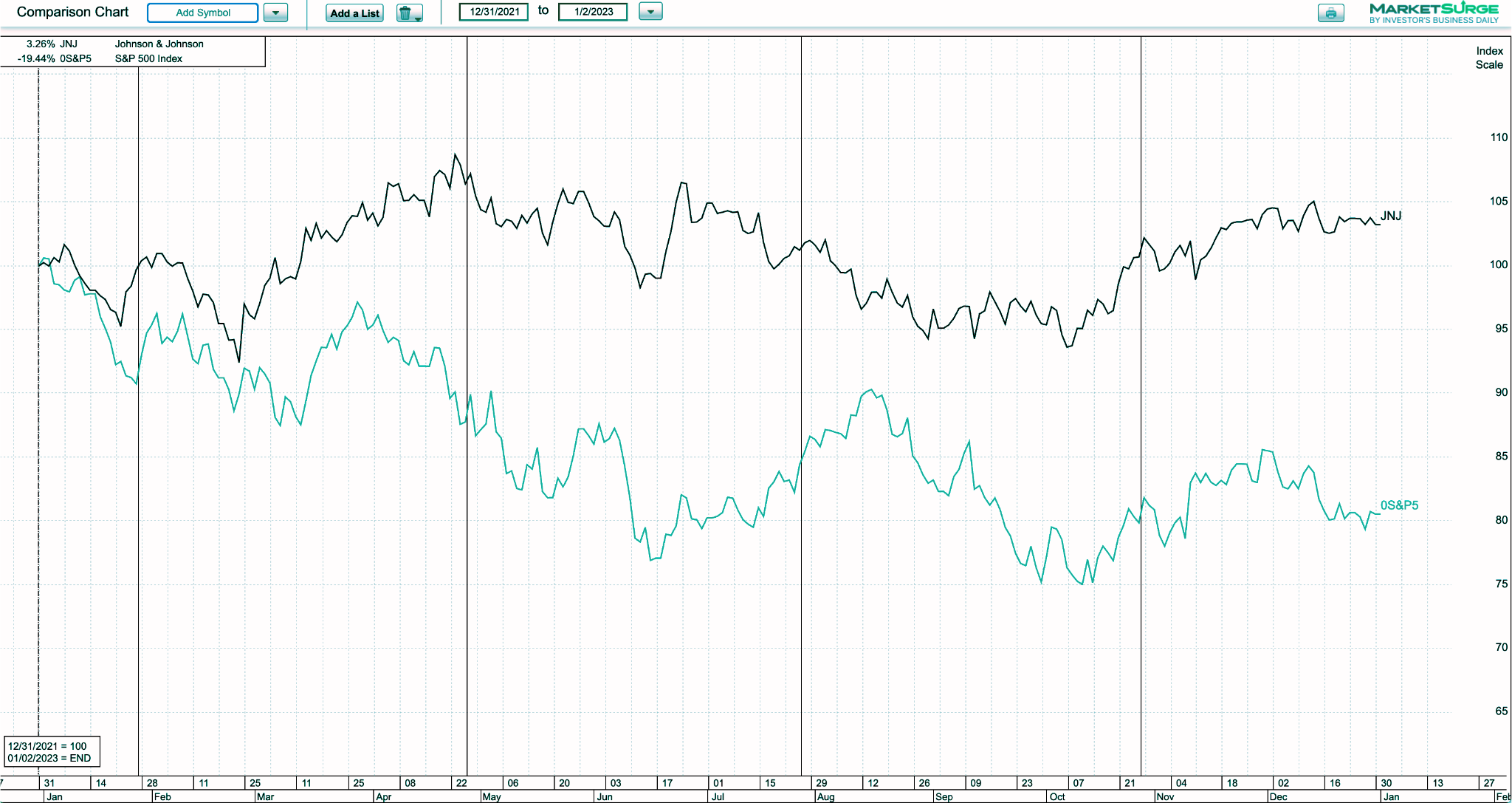

For example, J&J has a beta of .05, meaning it tends to move only 5% as much as the overall market’s swings.

While that indicates smaller day-to-day price moves, it doesn’t eliminate the dangers of single-stock concentration. Company-specific risks, such as, oh, a lingering lawsuit over talcum powder — a real problem JNJ has grappled with for years — regulatory changes, management missteps, technological disruption or shifts in consumer behavior can cause even low-beta stocks to underperform or fall sharply.

This chart isn’t directly showing the effects of beta, but it can be a proxy for the performance of Johnson & Johnson versus the S&P 500 in 2022, when higher beta techs were far more volatile.

Diversifying your investments reduces exposure to these idiosyncratic risks, ensuring that one company’s challenges don’t derail your entire portfolio.

A Single-Stock Recommendation Is Bad Retirement Advice

In the article I referred to above, the stock mentioned is a real estate investment trust with a dividend yield of 5.43%. That’s high, and I understand the visceral appeal.

It’s also the case that this particular company has grown its dividend for 30 years and paid a dividend for 56 years. That’s pretty impressive and is a good indicator that the payouts are likely to continue. After all, the dividends continued through all manner of market cycles and news events.

But to latch onto the dividend alone doesn’t explain how REIT dividends are vulnerable to rising borrowing costs, inflation and real-estate-market downturns. Retirees could wrongly assume that the payout is guaranteed like a pension.

To suggest that one stock can fill a retirement-income gap is naive.

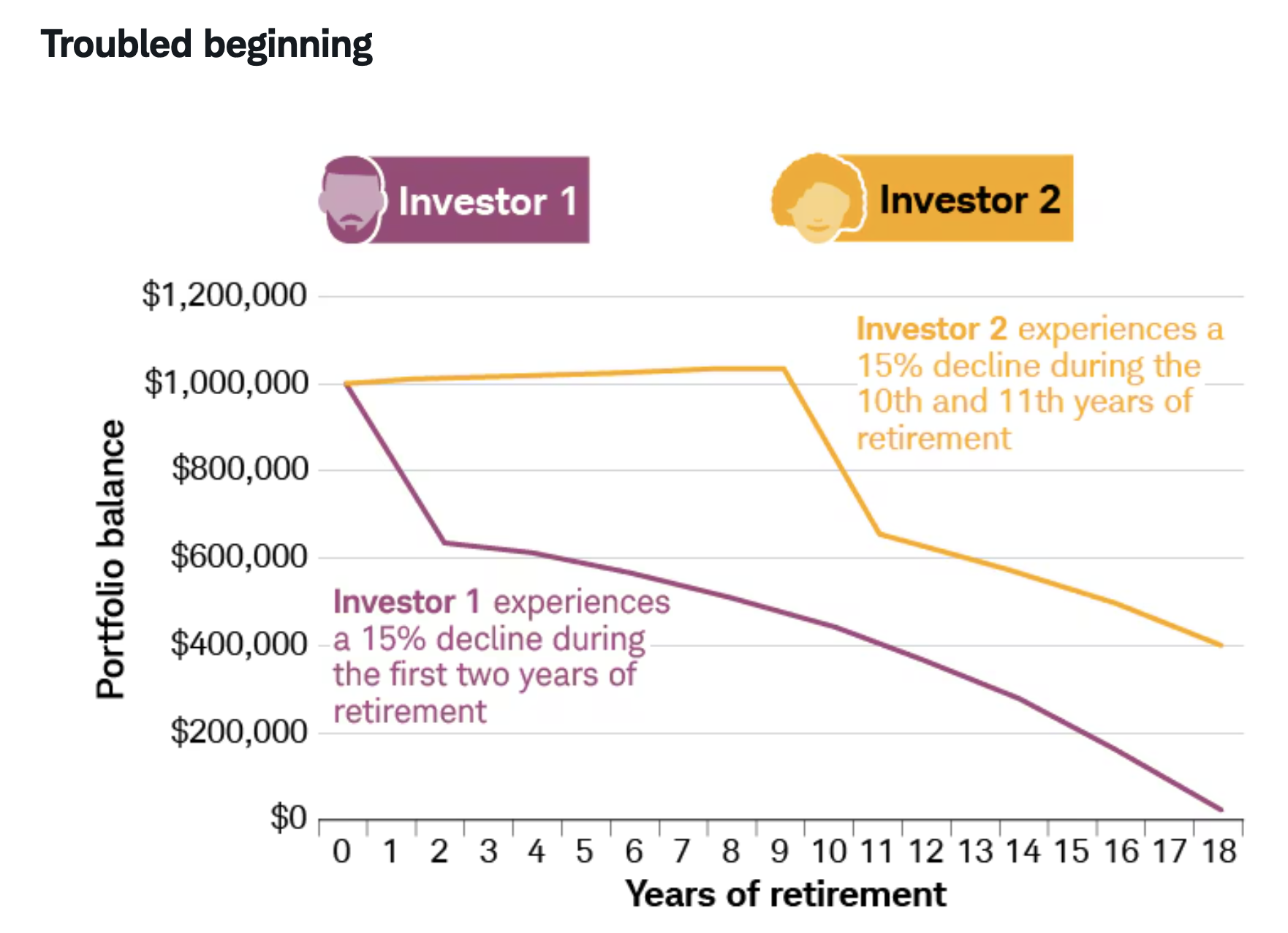

Sequence-of-Returns Risk

One big problem: Stock-price volatility could hurt retirees who are withdrawing funds during down markets. A falling share price erodes the sustainability of income even if dividends continue to be paid.

That’s particularly true in the early years of retirement, when a large portfolio decline can wreak havoc that lasts for years.

I’ve shown you examples like this before, but this is worth repeating: The illustration below, from brokerage Charles Schwab, shows what happens to two investors who each start with $1 million portfolios, who take initial withdrawals of $50,000 (with 2% inflation adjustments each year after — work with that number; it’s just for illustration purposes) — but who then see a 15% drop in portfolio value.

The investor who faces such a decline early in retirement runs out of money far sooner than an investor who does so later.

Ensure your investments are suited to your situation

Here’s a real danger, and a pattern I’ve seen too often:

Say you feel as if you’re behind on your retirement savings, and you decide that one particular stock, or maybe even a handful, is the ticket to catching up.

(I’ve also seen people who think options trading is the way to make up for a lack of savings. Nothing wrong with using options, but they’re not a get-rich-quick scheme.)

On the whole, be careful when it comes to one-size-fits-all advice.

High-yielding REITs may be appropriate for some retirees with higher risk tolerance, but always keep in mind your individual factors like age, portfolio mix and withdrawal needs when deciding whether any given investment is a good fit.

And don’t look to any single stock to be a hero to save your retirement. I’ve worked with enough clients and seen enough risky portfolios: The heroics eventually backfire.