Where Are Stocks as We Begin 2025? What Should Be Expected Going Forward?

The current concentrated nature of the S&P 500 is without precendent. Let's look at how we arrived here and what that means for the market. Plus, an update of my current top-10 holdings.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Understanding future market action requires knowing market history.

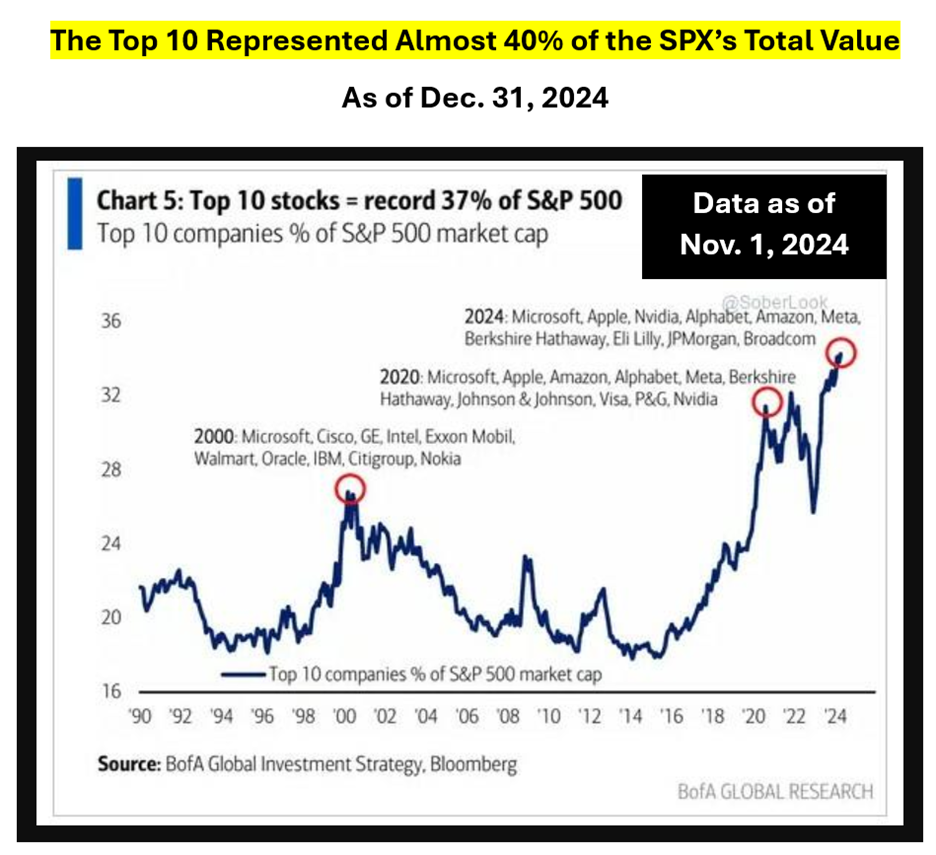

2024 concluded with the highest concentration ever seen in terms of the largest 10 holdings in the S&P 500 Index (SPX) and their make-up of the index’s market value.

Near the end of the technology/internet bubble in March of 2000 the 10 largest components of the SPX accounted for not quite 28% of its assets. At its peak reading in 2020 the top-10 holdings were near 32% of index assets.

By year-end 2024, that weighting had surged to nearly 40% of the total index market cap, from under 36% as of November 1, 2024. That is historically without precedent.

Momentum like that is always unsustainable over the long-term.

The changes to the 10 largest S&P 500 holdings over the years are worth noting.

In 2000 Cisco Systems CSCO, IBM IBM and Intel INTC were still highly coveted tech stocks. General Electric GE, Citigroup C and Nokia NOK were also wildly popular non-tech names. How times have changed. Half the top-10 largest holdings in the S&P 500 were technology firms.

During 2020 nine of 2000’s largest names (all but Microsoft MSFT) were gone from their perch. The biggest five holdings were all tech companies. Berkshire Hathaway (BRK.A, BRK.B) Visa V, Procter & Gamble PG and Johnson & Johnson JNJ moved into the top 10.

Nvidia NVDA, a newcomer, made its first appearance at #10.

At year-end 2024 the top-six largest names were all tech firms. Berkshire held firm while Eli Lilly LLY climbed in on the strength of weight-reduction drug profits. JPMorgan Chase JPM and Broadcom AVGO rounded out the big 10, which now sports seven technology members for the very first time.

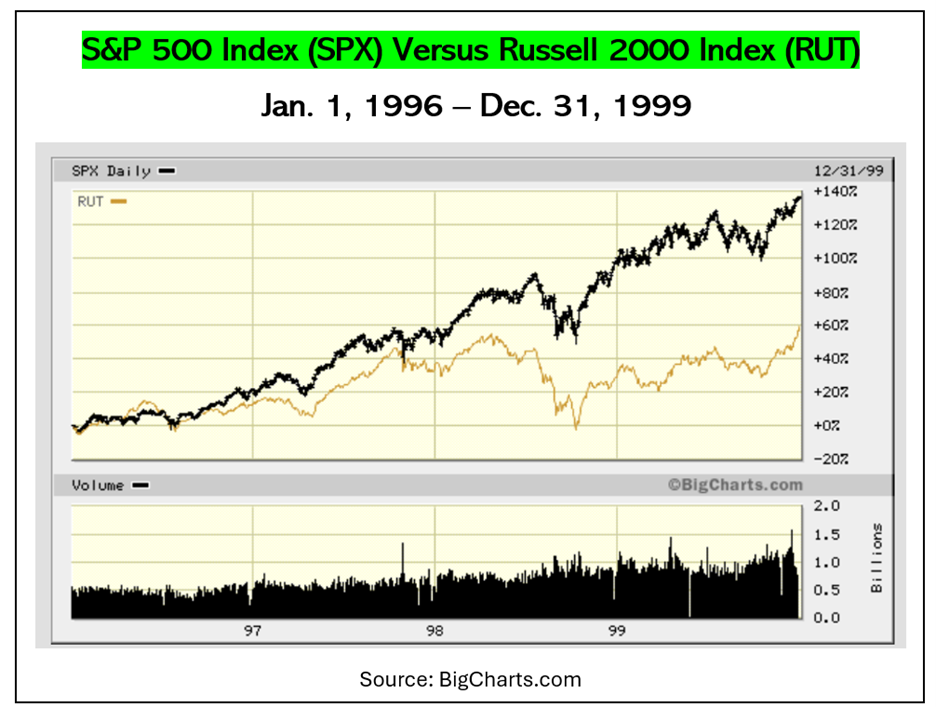

The four-year chart of the SPX versus the Russell 2000 from 1996 through 1999 was the most recent period like today’s situation. The more the mega-cap stocks outperformed, the more “hot money” chased it by sending cash into index funds and ETFs.

Managers of those portfolios were forced to buy more of the largest names regardless of how highly inflated their valuations had become. From January 1996 through December 1999 the SPX’s relative performance more than tripled the gains on the Russell 2000.

Traders late to the party were paying outrageous prices to own stocks which had already run up to unsustainable valuations.

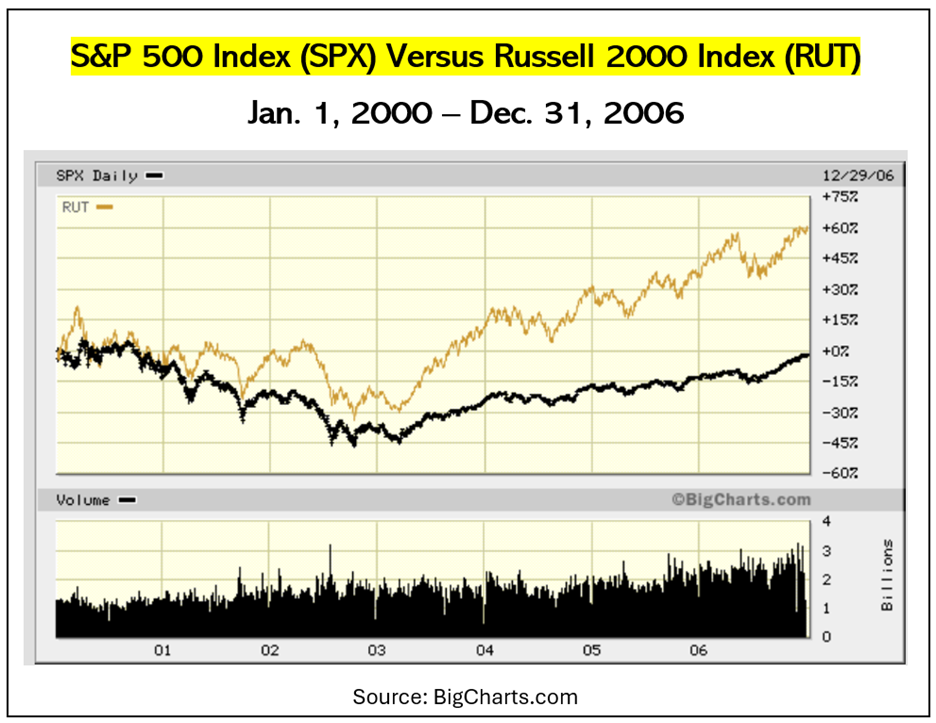

In the following seven years, from Jan. 1, 2000 through Dec. 31, 2006, the Russell 2000 ran up a 60% cumulative outperformance as the S&P 500 went nowhere.

Small-caps, which almost nobody was interested in during the tech/internet bubble, were clearly the place to be over the next full seven years.

Value stocks in general followed suit, even if not as dramatically as truly small-caps did.

The chart below details how the S&P 500 Value ETF SPYV did versus the more wildly held S&P 500 ETF SPY.

As happened in early 2000, the large-cap index is now quite pricey. The all-tech QQQ ETF looks even more expensively valued.

If you hold positions in those sectors it is a great time to be locking in gains rather than wading into what is likely to be a sideways (at best) or an outright downturn (at worst) that could last quite a while.

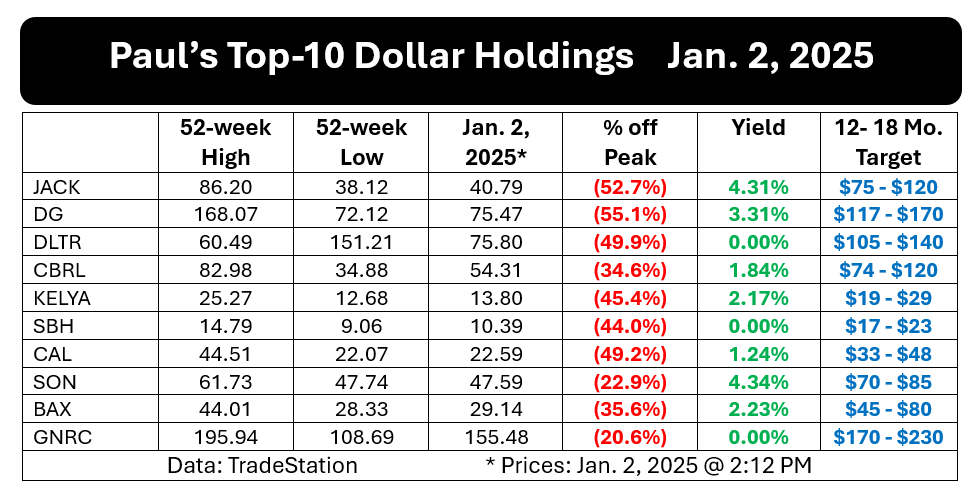

Here is an updated version of my current top-10 holdings ranked in order by dollar value.

2024 was not a good year for me. Value remained out of favor. I expect to see huge rebounds in every one of the listed names. I reaped huge capital gains on stocks bought much earlier, which were sold after 1–3-year holding periods.

All but three of my stocks pay cash dividends. Each sells for a fraction of what I see as their true value. Six of the 10 names could about double simply by returning to their trailing 52-week highs.

The only stock on my list which I am not currently adding to is Cracker Barrel CBRL. It is already up about 60% from its recent low point, set in early September of 2024.

Most of my 12-to 18-month goal prices could well be exceeded if things go better than my somewhat conservative estimates.

My Roth and Traditional IRA accounts are primed for major rebounds if my expected scenario plays out. In the meantime I am pocketing dividend income and covered call premiums collected via sales during trading rallies of my holdings.

After 46 years of investing I have learned that the price of success often requires living through frustrating periods when my picks are in contrast to the majority of investors.

I expect to be writing more frequently again. Thanks go out to all who reached out to me to let me know my absence was noticed.

At the time of publication, Price had positions in JACK, DG, DLTR, CBRL, KELYA, SBH, CAL, SON, BAX and GNRC.