When the Paychecks Stop: How to Invest for the Next 30 Years

Make Your Nest Egg Last Decades

You've reached your free article limit

You've read 0 of 1 free Pro articles.

You’ve spent years building your nest egg, so in some ways, you’ve already done the heavy lifting. but now comes the real challenge: turning those savings into sustainable income that can last 30 years or more.

“It’s not just how much you have saved that matters—it’s how you spend it down. A thoughtful drawdown strategy can extend the life of your portfolio by years, especially when facing uncertain markets.”

JPMorgan Guide to Retirement

The unfortunate truth is, most retirees don’t have a clear plan for how their investments should evolve after they stop working.

I’ve met countless people who know how to save, but not how to strategically withdraw and spend without draining their accounts too fast. Some retirees are too conservative and miss out on the necessary growth. Others take too much risk and put their savings in jeopardy every time the market heads lower.

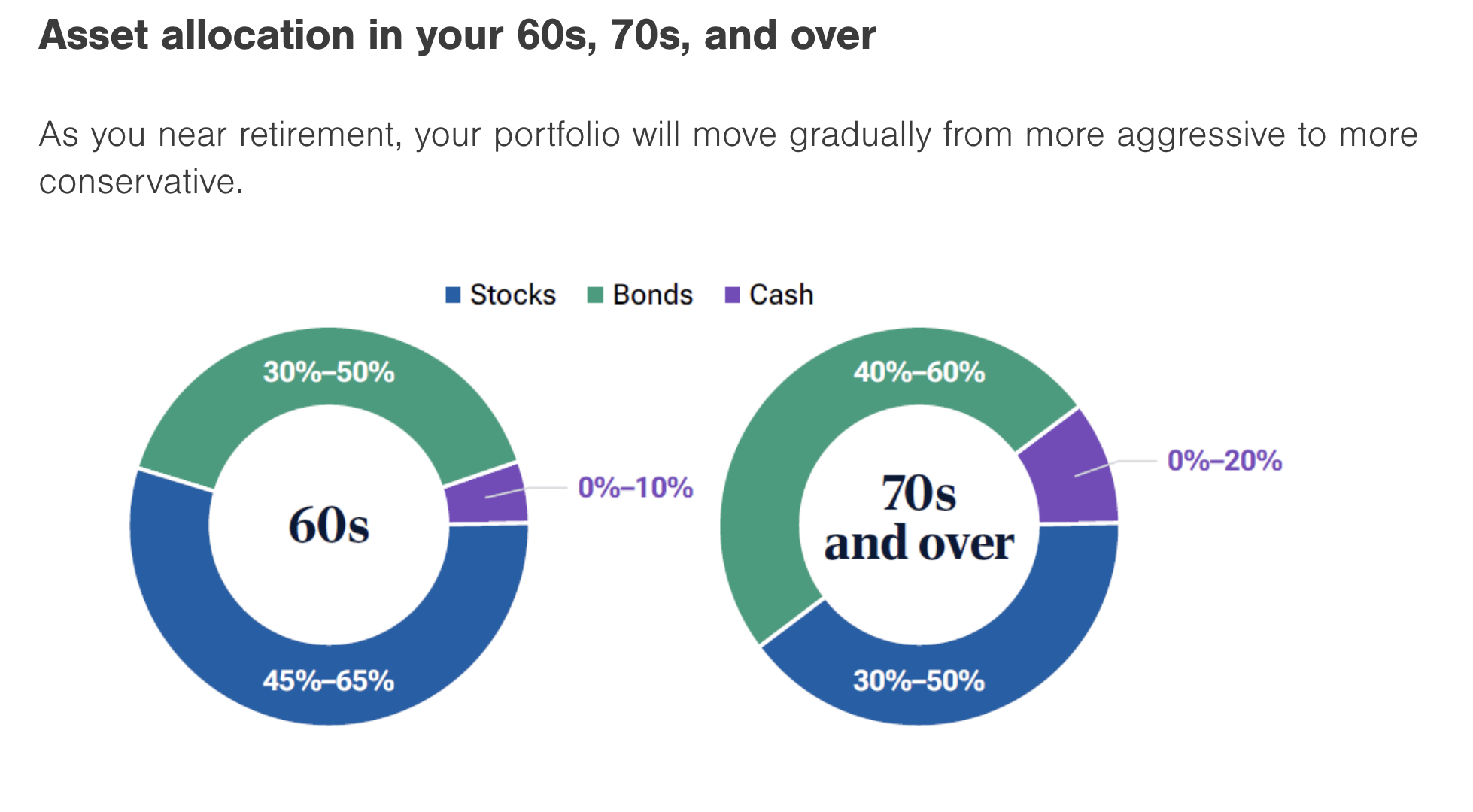

These pie charts from T. Rowe Price give you a good baseline for broad asset class allocation.

Sample Portfolio

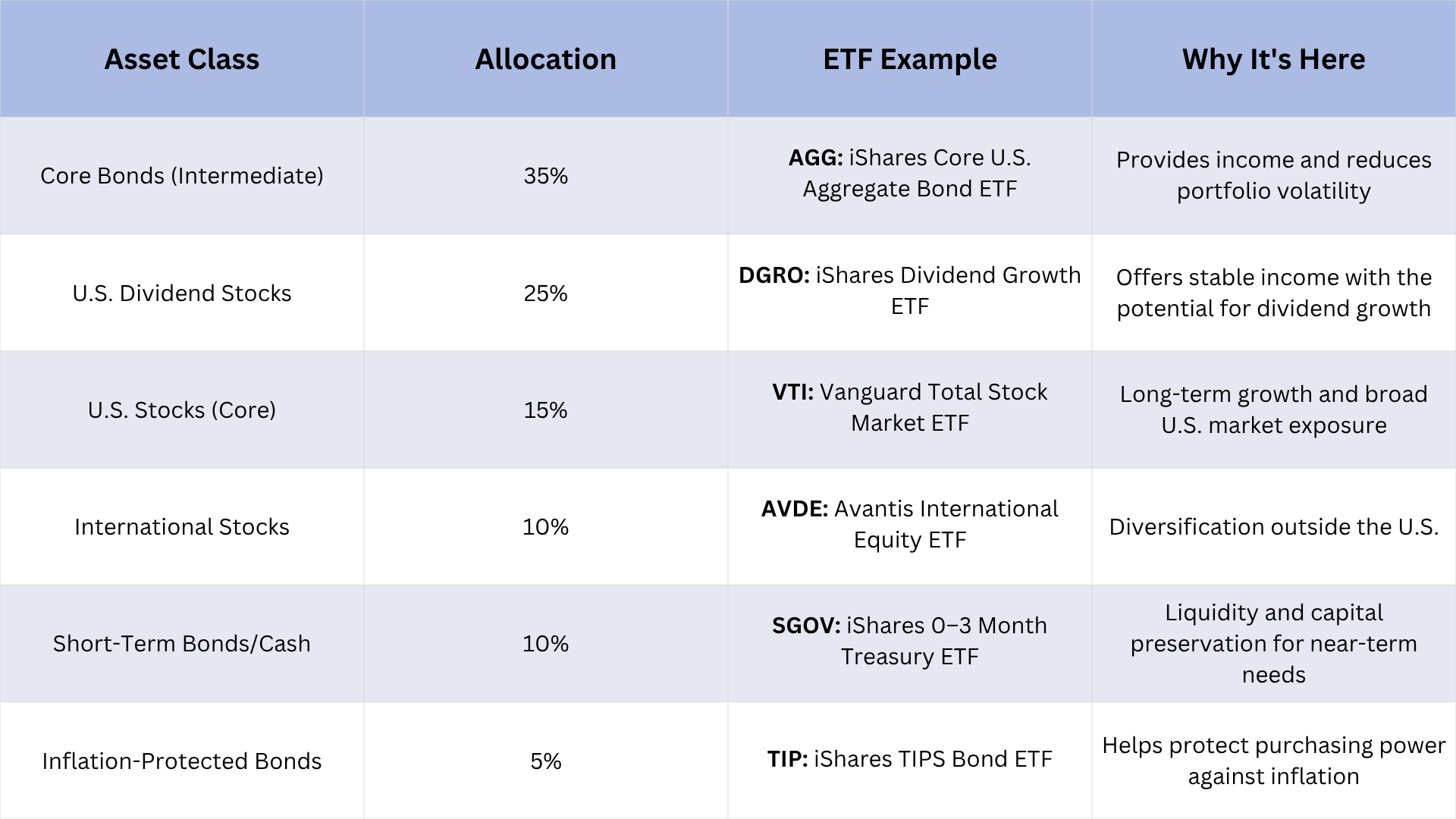

Try not to over complicate your situation by loading up with a dozen or more funds. Some investors, and even some financial advisors, think “more is better,” but too many funds means it’s more difficult to get traction in any area.

Here’s a sample (and it’s exactly that, not a recommendation) for funds that could constitute a retirement portfolio that balances growth and income while mitigating risk. The account holder in this scenario is a recently retired 67-year-old.

Strategy & Sequence of Returns Risk

You probably already know that you should dial down your risk exposure (aka stocks) in retirement, since it’s now more difficult to recover from market downturns with reduced opportunity to earn income.

Sticking with your pre-retirement portfolio and simply withdrawing money as needed could expose you to sequence of returns risk, one of the most dangerous pitfalls for retirees.

Sequence of returns risk occurs when the market drops early in your retirement, right as you begin drawing down your portfolio.

The combination of losses and withdrawals at the same time can cripple a portfolio’s long-term sustainability

“When you’re drawing from a portfolio, your withdrawal essentially locks in any losses that occurred before the portfolio had a chance to recover. That can have long-term consequences, even if returns normalize later.”

Christine Benz, Morningstar

What That Looks Like

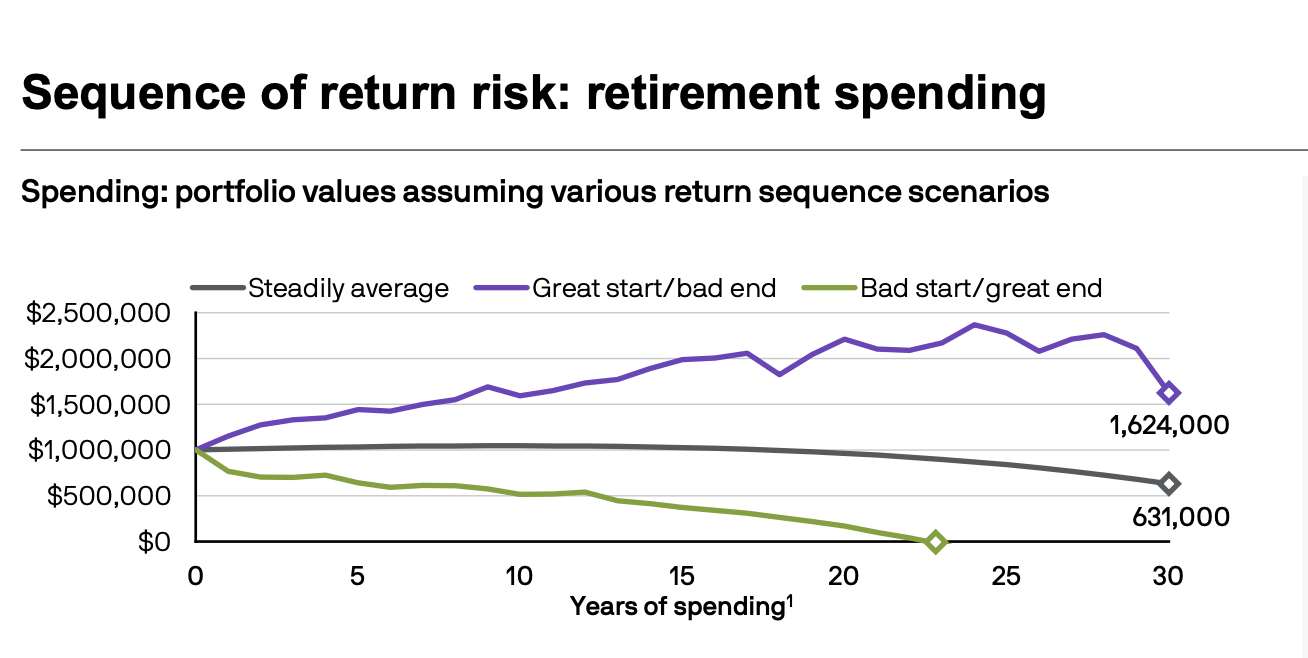

This chart from JP Morgan does a great job illustrating how the order of investment returns (not just the average) affects long-term retirement outcomes when you’re making withdrawals.

Each line assumes the same starting portfolio value and the same average return over 30 years, with annual withdrawals to fund retirement. But what’s different is the order in which the returns occur. That timing alone leads to dramatically different outcomes.

Great Start, Bad End (Purple Line)

- Strong early market returns give the portfolio a boost.

- Ends with the highest value: $1,624,000.

- Early growth provides a cushion against later losses.

Steadily Average Returns (Gray Line)

- Consistent returns over time.

- Portfolio remains relatively stable, ending around $631,000

- Demonstrates a "neutral" baseline with no return timing extremes.

Bad Start, Great End (Green Line)

- Losses occur early in retirement, before later growth kicks in.

- Portfolio is tapped out after about 22 years.

- Early poor performance while withdrawing money accelerates depletion.

Addressing Sequence of Returns Risk

Planning for retirement withdrawals requires more than just average return assumptions. you need a strategy to protect against early-downside risk.

But fortunately, it’s not just luck of the draw; there are ways to protect your portfolio against the inevitable market downturns.

What if you could structure your retirement portfolio so that part of it focused on stability, part on income, and part on growth? Each segment has a clear job to do and a timeline for when you’d need the money.

This approach doesn’t rely on trying to time the markets (a fool’s errand), but on aligning your money with your real-life spending needs over time.

In next week’s email, I’ll show you how that can work.