When Big Risks Meet Limited Time

Protecting your nest egg becomes more important as you age.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I'm 63 and still investing like I'm 35. I have to make myself change. My main goal now should be not to lose what I have. It's been more difficult to change than I thought.

-Comment from a Filthy Rich Animal reader

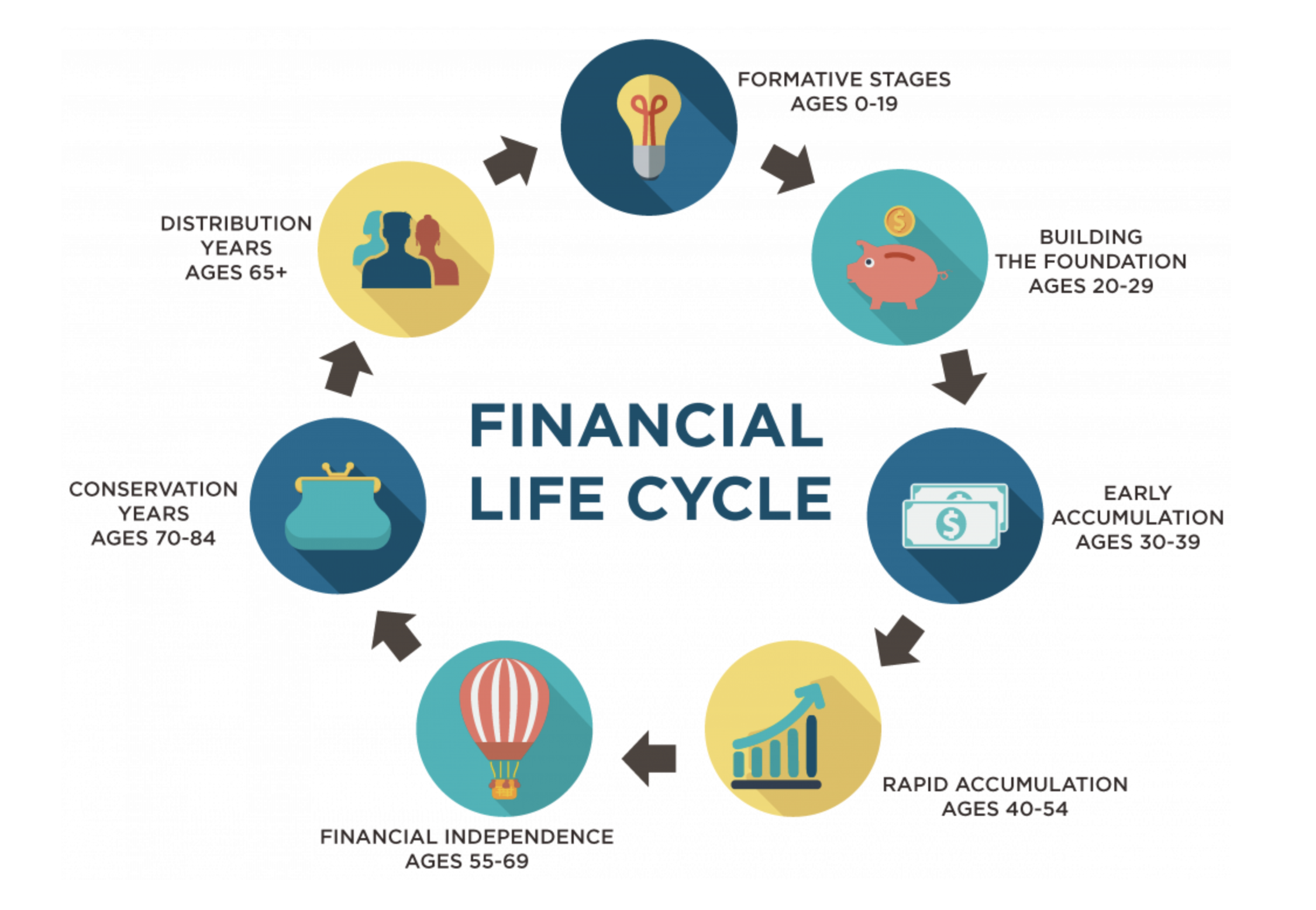

In the curriculum for the Certified Financial Planner credential, which I’m currently studying, there’s a section on life cycle planning. It includes financial planning for young adults, those forming and raising a family, those in the empty-nest stage, and finally, people in retirement.

The retirement age these days can vary, even though the official Social Security full retirement age for today’s 63-year-olds is 67. Some people retire sooner, some later. Also, some people start families later in life, or change careers, which can set them back a few years on savings. So take all those age ranges with a slight grain of salt.

However, the main point remains: The purpose of lifecycle planning is to help investors (and their financial planners) better anticipate and plan financial concerns they may face this year, or five years from now.

I’ve shown you plenty of pie charts to illustrate the industry-wide recommendations for a glide path that gradually reduces portfolio risk as you age.

Here are some of the reasons why investing science has determined that a lower risk profile benefits the vast majority of investors.

Why A More Conservative Glide Path?

Investing aggressively can be more fun and exciting, particularly if you enjoy stock picking. But we all know chowing down on pizza is more fun than eating vegetables and lean proteins. (Yeah, I know, you can put veggies on pizza. You know what I’m talking about, though!)

We also know which one is more likely to put on the pounds and send you into high blood sugar and the risk of heart problems.

Your future self will thank you for swapping out the junk food once in a while (more often, really, but I don’t want to be a total buzzkill right now). The same goes for stock picking and active trading versus mindful retirement investing.

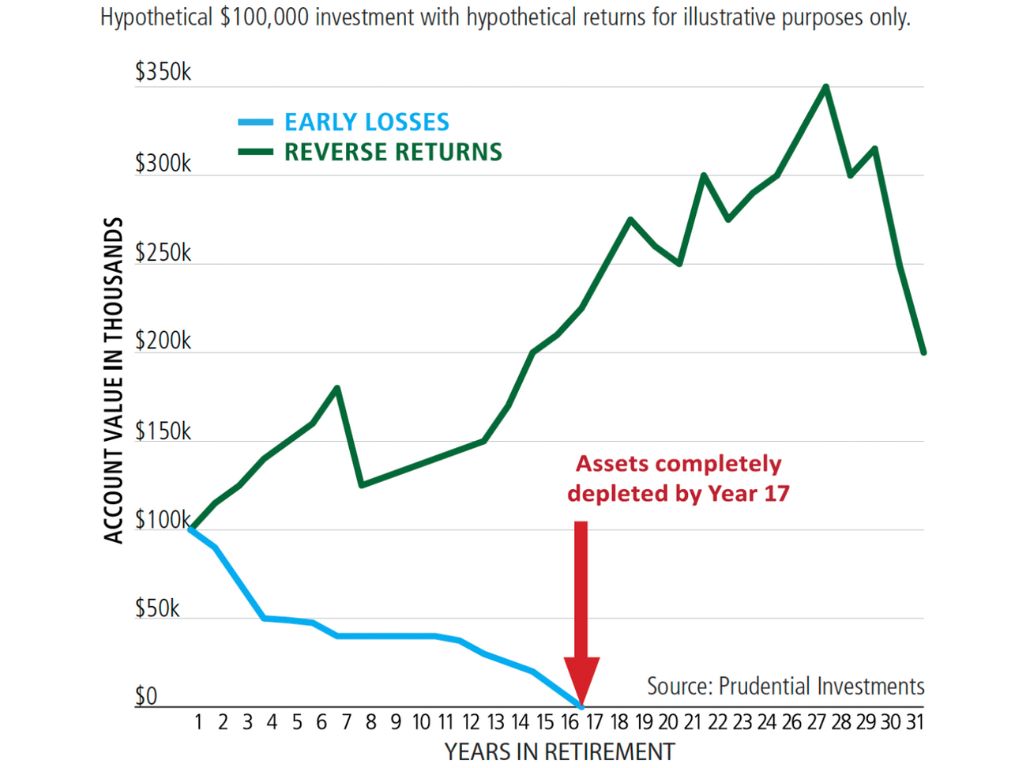

This image shows you what can happen to an investor who takes too much risk in the years just before retirement. If you’re unlucky enough to be retiring right around the time the markt tanks, you may be unprepared for what can happen next.

Here’s why a more conservative glide path makes sense.

1. Greater Risk of Running Out of Money Early

If your portfolio takes a big hit just as you're starting to withdraw money (like if you’re 63 and might be thinking about retirement), that loss can wreak havoc on your financial security.

At that stage, a less aggressive allocation, meaning using fewer single stocks and fewer risky assets like small-cap stocks, fast-growth techs or high-yield bonds, can significantly extend the lifetime of your savings when market drops inevitably come along.

2. Lifestyle Shift Demands Stability

As retirement nears, your focus naturally shifts (or should shift) from growing your investments to using them to support daily living. Even if you’re not retired, start adopting that mindset.

Think of what you would live on if you no longer had a paycheck from work.

Target-date fund managers widely vary in how aggressively they reduce equity exposure by retirement time. That’s not necessarily bad; it’s a sign they’re balancing the need to protect savings with enough growth and income to maintain purchasing power.

3. Protects Against Big Losses That Hurt in the Short-Term

This is a place where our overly aggressive 63-year-old investor could run into trouble. While stocks do offer higher returns, a big drop in value, especially early in retirement or just before retirement, can be devastating.

A conservative mix helps cushion that downside, reducing the chance of your money kicking the bucket before you do.

You Won’t Want to Hear This, But….

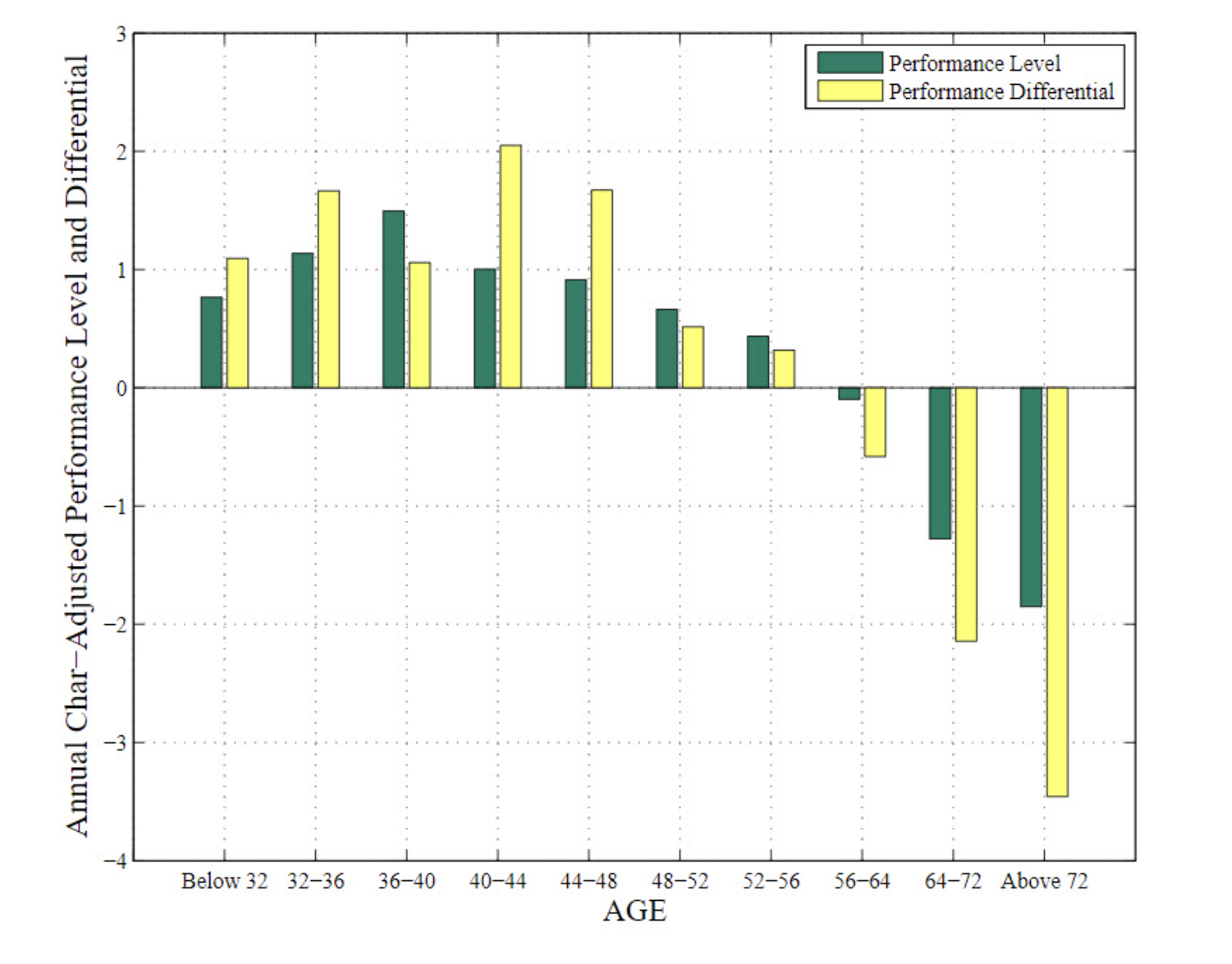

Here’s a particularly unpleasant truth: Data show that stock-picking becomes riskier as you get older.

A 2009 research study by George Korniotis and Alok Kumar at the University of Miami revealed that older investors often underperform younger ones by about 2% a year, for a few reasons.

- Stock choices aren’t as strong: Picking winning stocks becomes harder, and older investors tend to hold on to losers longer. (I’d add: More current research shows that with the domination of a few huge techs and a handful of other mega-caps, market-beating stock-picking is even more difficult today than in 2009.)

- Portfolios are less diversified: Too much money ends up in just a few stocks.

- Confidence stays high even when skills fade: Financial literacy tends to drop about 3% to 5% lower returns annually on a risk-adjusted basis

Sure, those findings don’t apply to everyone. For example, you can hold up Warren Buffett and the late Charlie Munger as exhibits A and B to argue against this research.

(Don’t forget: In addition to Buffett and Munger’s genius, they had research teams and veered toward prudent investing, rather than risk-taking.)

The bottom line: In retirement, you don’t have decades to recover from big losses. A few bad picks can do serious damage when you’re already withdrawing money from savings.

A smarter move: Shift from risky individual stocks or even ETFs holding risky asset classes, to diversified funds (like index funds or ETFs) as you get older. This helps protect your money and reduce the chance of a devastating loss at the wrong time.

A Little Play Money Is OK

One last thing: Of course you can still scratch the itch to pick stocks or take a flier now and then. I've had plenty of clients do just this, and I want them to, if they’re interested in “playing the market.” (I loathe that term; you shouldn’t be playing with the money you’ll need to last three decades when you’re not working. It also suggests the goal is to outsmart the market, when it should be to generate the income you’ll need, not have bragging rights … or something.)

Sure, you can have a little stash of “play money.” Just be sure it isn’t something you’ll need to keep the lights on when you’re 86. You can use your winnings for a pizza party :)