What's Mental Accounting? It Could Wreck Your Retirement

Even cautious investors face surprising retirement risks.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

A few years ago, I had a client in his 60s who was nearing retirement. Before he began working with me, David had some random “stuff” in various taxable and tax-advantaged accounts.

He was ready to get his investments streamlined, but still wanted the latitude to do some trading outside of his retirement accounts.

But David was doing what’s called “mental accounting.” He was looking at each various account type as a separate entity, depending on the source.

But this is classic mental accounting, and it’s one of the most dangerous mistakes retirees make.

In David’s case, he viewed some accounts as places to take outsized risk, and others were earmarked as more conservative. We worked it all out to invest in a way that was suitable for his time horizon, while still allowing him some latitude for trading in a small account.

Retirement Income at Risk?

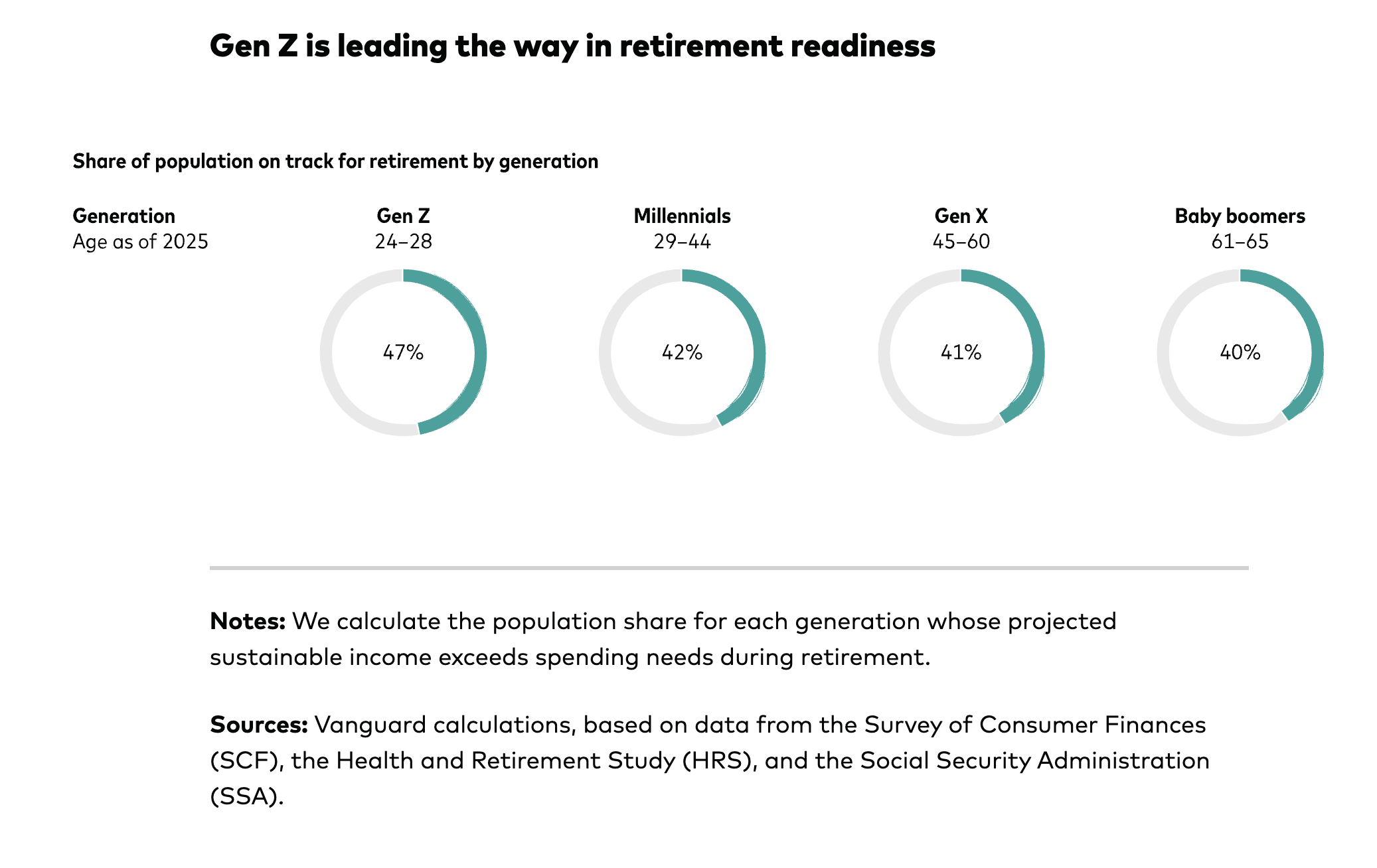

In an October 2025 report, Vanguard estimates that only about 40% of the youngest Baby Boomers, those age 61 through 65, are on track for sustainable retirement income under current saving and allocation patterns.

Younger generations are further ahead, but it's more concerning that people in their 60s are lagging when it comes to savings.

It’s not necessarily a bad thing to split money into different categories, such as these.

- My “safe” money (certificates of deposit, cash)

- My retirement money (401k)

- My fun investing” (a few favorite stocks)

- My spending money (dividends)

As with my former client David, a version of that system ultimately worked out well for him.

However, the potential pitfall means investors may overprotect the “safe” bucket and underfund the long-term growth bucket.

And while I’ve advocated for the “bucket system” as a way of simultaneously growing and protecting assets for a potentially long retirement, that’s not the same as separating money based on its source or its intended use.

You Can Be Too Safe

Here’s a sad, cautionary tale.

Years ago, I worked with an advisor who started in the business in the 1970s. She told a story about a long-ago client who was terminally ill, and bought long-term government bonds for his wife. He was convinced he was buying financial protection for the years after he was gone.

He called the bonds her “forever safe” money: They offered steady income and no volatility.

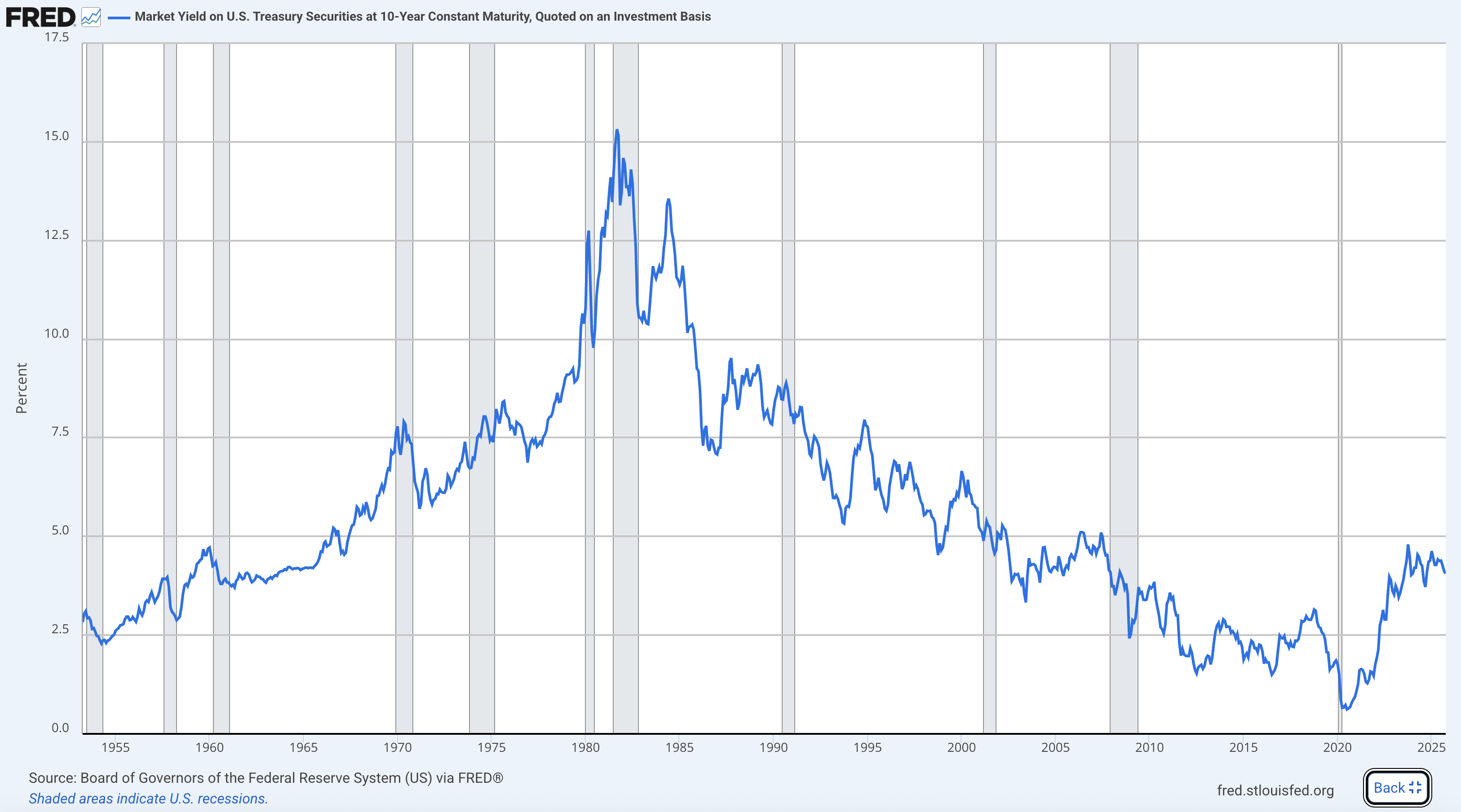

After he died in the early 1980s, interest rates spiked higher.

The value of his widow’s bonds plunged as new bonds paid far more, and inflation simultaneously eroded her real income. She couldn’t sell the bonds without taking a substantial hit, but holding them meant falling further behind each year.

What my former colleague’s client meant as a secure investment became a trap, and eventually, she had to return to work in her 60s.

Not because she’d taken too much risk, but because her portfolio had been too conservative for too long.

This chart from the St. Louis Federal Reserve clearly shows that rapid rise in bond prices that eventually abated and remained low until rising in 2020. (And they’re still low, relative to some historical rates.)

That’s all to say: A portfolio that feels “safe” in the short term can become much more risky than investors anticipate.

Investing Is Often Counterintuitive

In an April 2025 article, “How to safeguard your retirement,” brokerage Fidelity warns that to maintain purchasing power, inflationary periods often require increasing rather than decreasing equity exposure.

Understandably, high inflation can have the opposite emotional effect. During times of economic stress or uncertainty, people often stash away their financial acorns for safekeeping, just like Filthy Rich Animal mascot Earny the squirrel hides seeds and nuts for winter sustenance.

The tricky part is that inflation, recession, and falling markets can each have a different impact on your portfolio. As a consequence, the strategies for dealing with them can differ, and may sometimes seem to work in opposition to each other.

"For example, during inflationary times, you might consider boosting the growth part of your portfolio by investing in stocks, which historically have outpaced inflation.

But during recessionary times, stocks tend to lose value. Since people nearing and in retirement may now be facing all those challenges, it's important to build a portfolio that attempts to manage both risks in tandem."

-Fidelity Viewpoints

This quote from Fidelity illustrates how mental accounting can quietly work against you.

By separating your assets according to source or emotional attachment, you may find yourself making decisions that feel safe in the moment yet undermine long-term purchasing power.

Risk Capacity, Not Risk Tolerance

In a May 2025 research report, Vanguard noted that its Life-Cycle Investing Model stresses that retirement portfolios should reflect risk capacity, or what returns are needed to meet goals, not simply their comfort levels.

According to Vanguard:

- Save more to avoid reacting to markets: Increased savings rates have the biggest effect on long-term success. This means you have a cushion to ride out the inevitable market volatility.

- Use reliable income like Social Security: This can support maintaining enough growth assets to outpace inflation, and allow you to treat your investments as part of a unified strategy.

- Personalized portfolios outperform rules of thumb: Don’t fall into the trap of thinking your portfolio should be either more aggressive or more conservative simply because that’s the right mix for someone else.

Practical Next Steps

Audit your own mental accounting. Are you separating money into artificial buckets, which may result in taking too much or too little risk?

- Stress-test your plan for 25 to 30 years of inflation. This is something that do-it-yourself investors often neglect.

- If you aren’t yet taking Social Security, review your expected benefit at different claiming ages.

- Evaluate stock concentration. For example, outsized holdings in Apple (AAPL), Tesla (TSLA), and Nvidia (NVDA) are common these days.

- Use a total-return plan rather than relying solely on either growth or dividends.

- Align your portfolio with long-term needs, not short-term feelings. (This is by far the most difficult of these steps.)

Aligning Dollars With Future Needs

The examples of my client David and his scattered accounts and the widow’s so-called “safe” bonds illustrate how easy it is for mental accounting to put a dent in long-term outcomes.

As Fidelity noted in its report I referred to above, safeguarding retirement often requires leaning more into growth when inflation rises, which may feel counterintuitive.

Also, Vanguard’s research emphasizes that your portfolio should reflect risk capacity, which means what returns you need to meet your goals, rather than short-term comfort.

The goal isn’t to abandon structure or to ignore emotions; it’s to ensure that every dollar, in every account, is working toward the unique mix of assets you need for a sustainable retirement.