What’s Lurking Inside Your 401(k)?

Better fund choices may boost returns by lowering your costs.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

401k With Bull and Chart

401k With Bull and Chart

When was the last time you looked at what's actually inside your 401(k)?

Readers of this column are typically more attuned to their investments than the general population, but for some Americans, the number of times they look at their 401(k) in a given year is zero.

If you're not a member of TheStreet Pro yet, please join us. It's a great time to Go Pro!

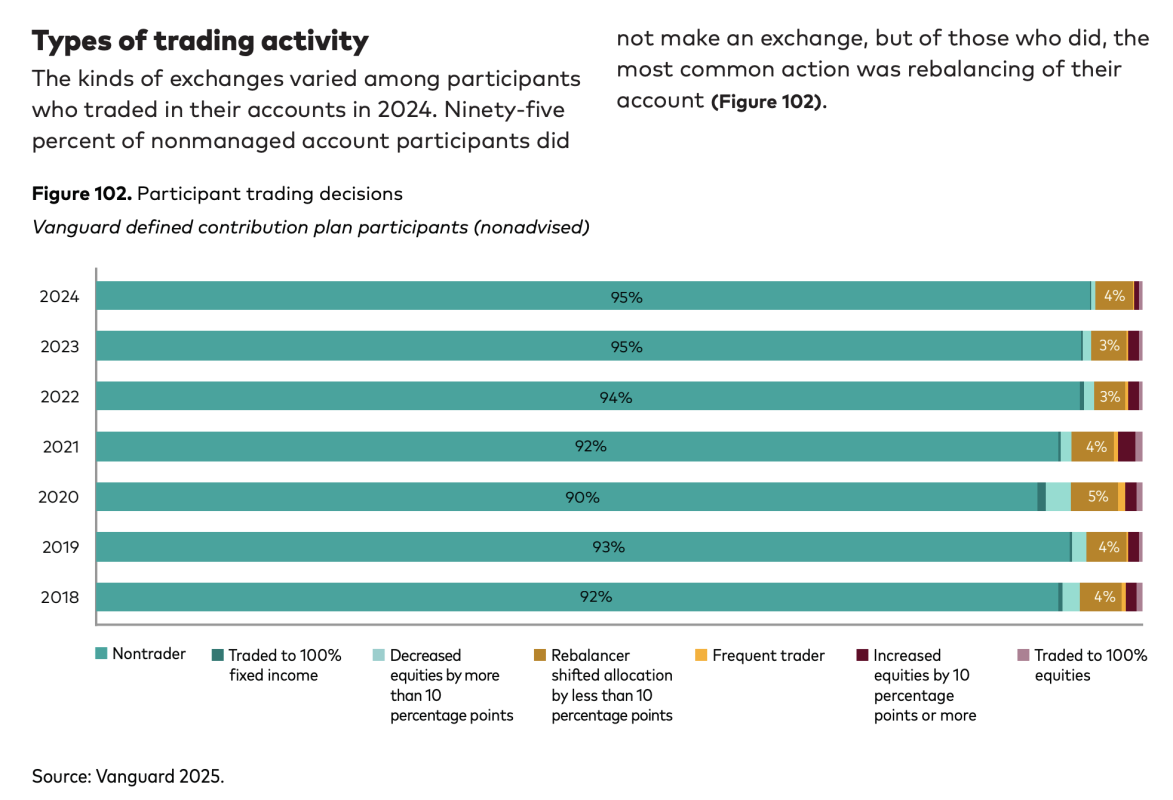

According to Vanguard's How America Saves 2025, which tracks the retirement saving behavior of nearly 5 million plan participants, “During 2024, 5% of nonadvised participants traded within their accounts, while 95% did not initiate any exchanges.”

Vanguard

This image shows that the number of investors not messing with their 401(k) holdings has held above 90% for several years.

A couple of points:

1. Actively trading your 401(k) is a terrible idea. Even without tax consequences, trading your 401(k) means making active bets on market timing.

Most investors, acting on instinct rather than discipline, will buy after markets rise and sell after they fall. This locks in losses and misses recoveries at precisely the wrong moments. It also results in a willy nilly collection of stuff in the account with no serious allocation.

2. A good part of the inertia Vanguard identified is due to the increased adoption of target date funds, which require no rebalancing on the part of 401(k) account owners.

However, for those holding funds with no built-in glidepath, that indifference usually has a price tag.

A startling number of workplace retirement plans have high-expense-ratio funds hiding in plain sight. Here are some less-than-optimal funds to avoid (if you can) and some better alternatives.

High-Priced Funds

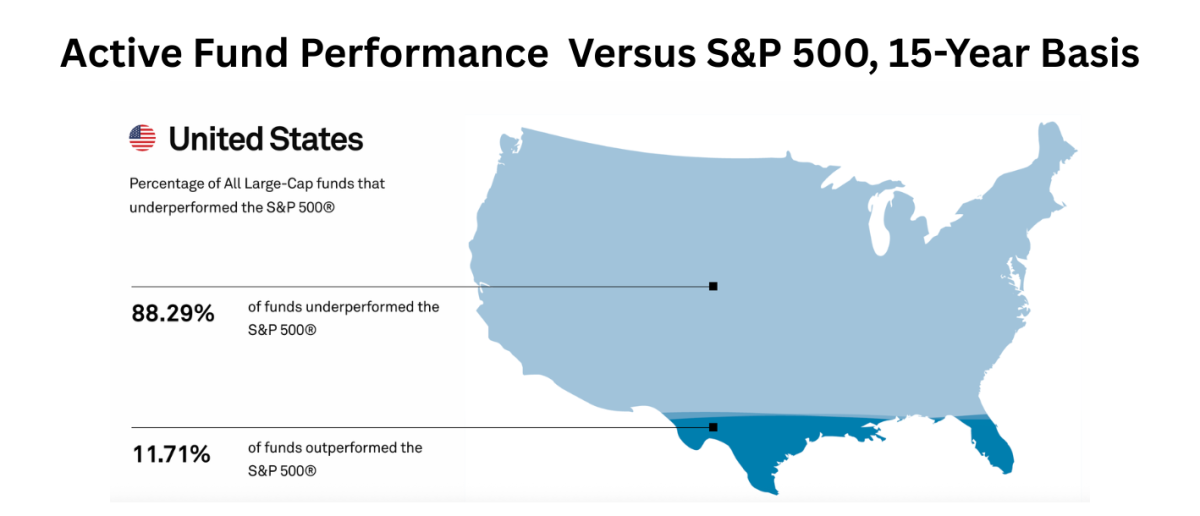

- American Funds Growth Fund of America (AGTHX): This large-cap growth fund is among the most widely held in 401(k) plans. It has a solid long-term track record, but that has more to do with outperformance of domestic large-cap stocks than managers’ magical stock-picking. Costs can vary dramatically depending on which share class your plan offers. Institutional R6 shares, available in some larger 401(k) plans, have an expense ratio of about 0.29%. You should ask yourself whether an actively managed fund, in a category where only 14% of active managers have beaten the S&P 500 over the past decade, is worth the premium over an index fund.

S&P Global SPIVA Scorecard

- PIMCO Total Return (PTTAX): This actively managed intermediate bond fund holds mostly investment-grade debt. It’s a staple of many 401(k) plans, possibly because it’s just been there for so long that plan administrators haven’t swapped it out, despite outperformance by index fixed-income funds. Many 401(k) plans use the institutional share class, which carries an expense ratio of around 0.46% to 0.49%, substantially higher than an index alternative. In lean interest rate environments, that extra fee can consume a sizable chunk of what the fund actually earns.

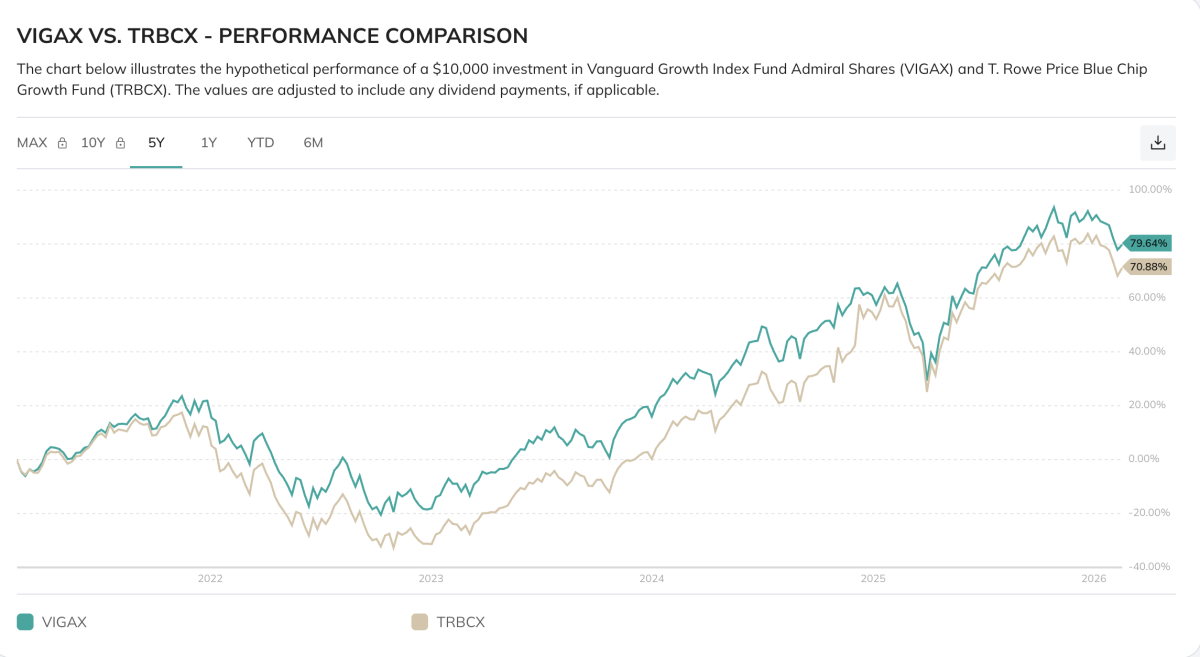

T. Rowe Price Blue Chip Growth (TRBCX): This active fund is another recognizable name on 401(k) menus. It holds well-established companies with strong earnings potential, so there’s nothing speculative here. Like AGTHX, this fund has benefited from the dominance of large-cap U.S. asset class performance. The catch is the fee. Owners of the institutional I Class shares pay 0.57%, well above index fund ratios.

Lower-Fee Choices

- Fidelity 500 Index Fund (FXAIX): This fund stands out because it’s even less expensive than some S&P index funds in an ETF wrapper. The expense ratio is just 0.015% annually, meaning an investor with $100,000 in the fund pays $15 a year in fees. It’s pretty darn precise when it comes to tracking its benchmark, returning 25% in 2024, a tracking gap of just two basis points. As SPIVA research shows, with so few managed large-cap funds beating the S&P 500, FXAIX offers a cheap and consistent alternative.

- Vanguard Total Bond Market Index (VBTLX): This fund delivers wide exposure to the U.S. investment-grade bond market, which includes corporate, government and mortgage-backed securities, all for a low fee of just 0.05%. However, there’s a twist: The institutional class of the PIMCO bond fund, above, has edged out VBTLX over the past decade, net of fees. But for 401(k) participants not in the institutional share class, the higher fees of the PIMCO fund mean a bond fund needs to outperform by nearly a full percentage point to match what the index delivers. Most participants have no idea which share class they hold. VBTLX removes that uncertainty entirely.

PortfoliosLab

- Vanguard Growth Index Fund (VIGAX): Here, you’ll get exposure to the usual gang of large-cap names: Microsoft (MSFT), Nvidia (NVDA), Apple (AAPL), Amazon (AMZN), Meta (META), at just 0.05%. It tracks the CRSP U.S. Large Cap Growth Index. The actively managed TRBCX's retail shares run at 0.69%, and as noted above, even the institutional class comes in at 0.57%. The image above shows the outperformance of VIGAX over the past five years.

Your task for today is to open up that 401 (k) and see what you're holding. If you're paying too much for the funds you own, or haven't thought about rebalancing, it's a great time to dig in and see how you can optimize your portfolio. Future you will thank you for it.

Related: 2026 Isn’t 2000—or 1929: What Bears Are Missing About Today's Market