What Happens When Wall Street Locks the Exit?

Private investments aren’t built for daily liquidity.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

When you invest in a retirement or brokerage account, you expect you can exit a given investment if you want to, whether or not it creates a taxable event.

You don’t want a fund company telling you, “Nope. You can’t get your money right now.”

But that’s what’s happening.

After a flood of redemptions, asset management giant BlackRock (BLK) recently said it would limit withdrawals from a private credit fund.

According to a Reuters report, “Sentiment has soured around private credit in recent months, and retail investors are increasingly asking for their money back from funds like BlackRock's $26 billion HPS Corporate Lending Fund (HLEND), which were designed to be open to wealthy individuals.”

Wasn't it just last week that Washington regulators proposed letting private-market investments into 401(k) accounts?

Exit Denied

But now we know what happens when these funds get stressed: The doors lock.

Canva license

For a wealthy investor with access to funding elsewhere, a gated fund may be just an inconvenience. But for someone depending on that money to retire, it's a different conversation entirely.

The HLEND fund lockdown applies to accredited or high-net-worth investors, not to everyday 401(k) savers. Not yet, anyway,

The proposed Department of Labor rule wouldn't immediately flood 401(k) menus with standalone private credit funds. Most analysts expect these investments to arrive slowly, embedded inside target-date funds that millions of Americans hold without really understanding the innards.

And that's precisely the problem.

What’s Inside These Funds?

When the gates came down on BlackRock's fund, at least the accredited investors knew what they owned.

But the average 401(k) saver picking a retirement date fund may have no idea that a portion of their nest egg is sitting in illiquid private credit loans. That is, until the day they need the money and find out the hard way.

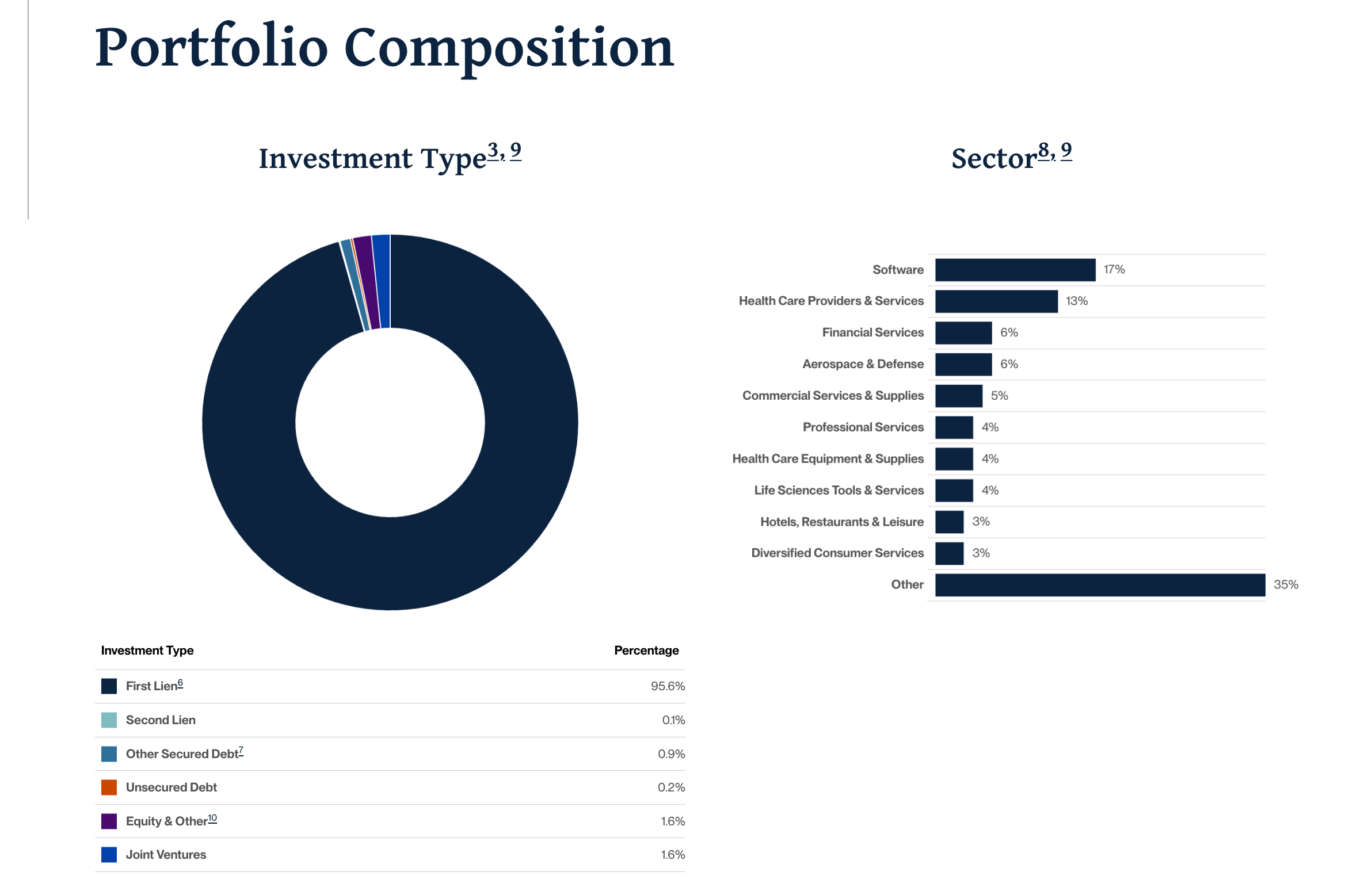

These images from BlackRock show HLEND’s investment categories, and the names of top components. Seasoned market participants, or people who worked in the financial industry, may have a glimmer of recognition.

The average retirement investor probably doesn’t have a clue.

BlackRock

BlackRock

A caveat: The private credit gating doesn’t indicate a systemic collapse, so that particular scary thought is not something to panic about.

However, there is a liquidity mismatch finally becoming visible under stress.

The result is that investors are seeing that their money may not be as accessible as they thought. That realization will push them toward products with daily liquidity and transparent pricing, at least until everybody forgets and the cycle repeats itself.

What Is Private Credit?

These are illiquid loans to mid-sized companies, packaged into funds now being marketed to accredited retail investors and, increasingly, retirement accounts.

The assets can't be sold quickly. That was always in the fine print, but in the giddiness over this newly prominent and accessible asset class, it got overlooked.

Who the Structural Mismatch Hurts

These funds were designed for patient institutional money with long time horizons. Retail investors have different needs and different expectations.

When sentiment sours and retail investors want out, the math doesn’t math anymore. That’s when the gates come down and the guy holding the key walks away.

The gates, it turns out, are a feature not a bug.

The Liquidity Question

Private equity and private credit returns have deteriorated from the peak years of 2022 through 2025. Every asset class has ebbs and flows, so that in and of itself shouldn’t be surprising, but many investors believe the latest thing (whatever it is) is that magical unicorn that will always go up. And up.

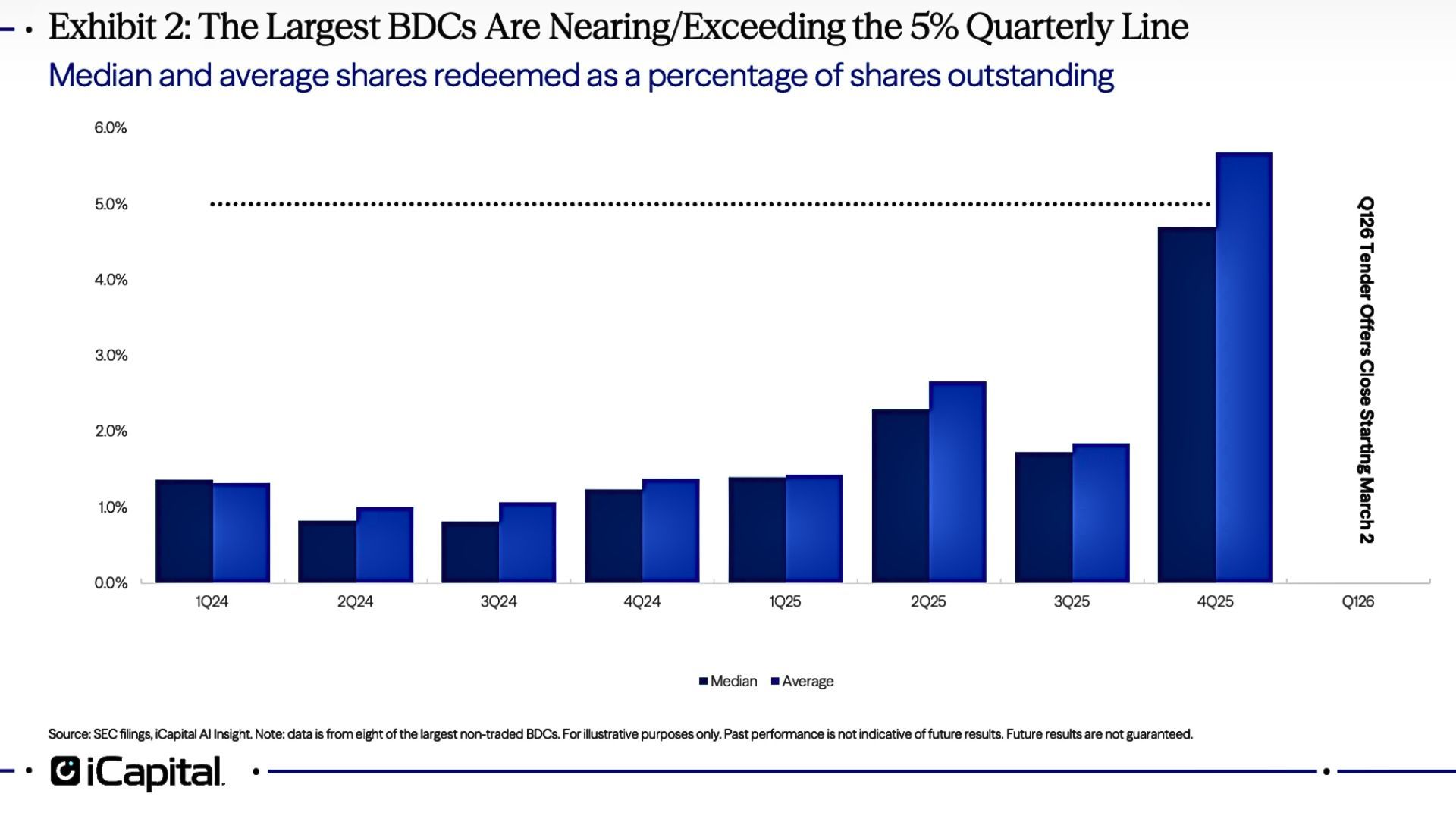

Redemption requests at the largest private credit funds surged in late 2025, crossing the 5% threshold that triggers withdrawal restrictions. More investors wanted their money back than the funds were designed to handle. Oops.

This image from iCapital shows that redemption requests at the largest business development companies, which invest in private credit and sometimes private equity, surged in late 2025. Those redemptions crossed the 5% threshold that triggers withdrawal restrictions.

iCapital

In other words, more investors wanted their money back than the funds were designed to handle.

With private-market investments, the big institutions that got in early are sitting on aging positions they need to exit. The aggressive push to open these products to retail investors arrived at a convenient moment, right when institutional demand was softening and sponsors needed new buyers.

The Real Stakes for Retirees

Washington and Wall Street have been pushing the use of private credit in 401(k)s and individual retirement accounts.

BlackRock bills its LifePath target date funds as offering a "paycheck for life." That narrative has been used to justify the inclusion of these risky and potentially illiquid assets.

That’s nice for BlackRock, but a 60-year-old whose retirement account sees the redemption gate close at the wrong moment has a pretty short recovery runway.

The machinery to sell these assets to retail investors already has significant momentum. But anyone thinking about dipping their toes into these waters should ask: Is anyone in Washington or on Wall Street asking whose liquidity problem this actually solves?

I think we all know the answer to that.

Related: The Great Diversification Illusion: Why Your Funds May Be Moving in Lockstep