Three 401(k) Mistakes You Can Easily Avoid

Three errors could shrink your retirement

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Three 401(k) Mistakes You Can Easily Avoid

So you’re a good retirement saver? Salting away money in tax-advantaged accounts on a regular basis?

There may still be room for improvement. Here are three ways you can fine-tune your process.

Mistake 1: Not Automating Contributions

Most advisors and plan sponsors recommend automating both enrollment and contributions.

For example, maybe you’re already enrolled in your employer’s plan, but you left your contribution level at “set and forget.” Over time you may be cheating yourself out of money your future self will need.

But say you automate an annual increase in your contribution. (Hopefully that coincides with annual raises; the raises may not be that reliable at many employers, unfortunately.)

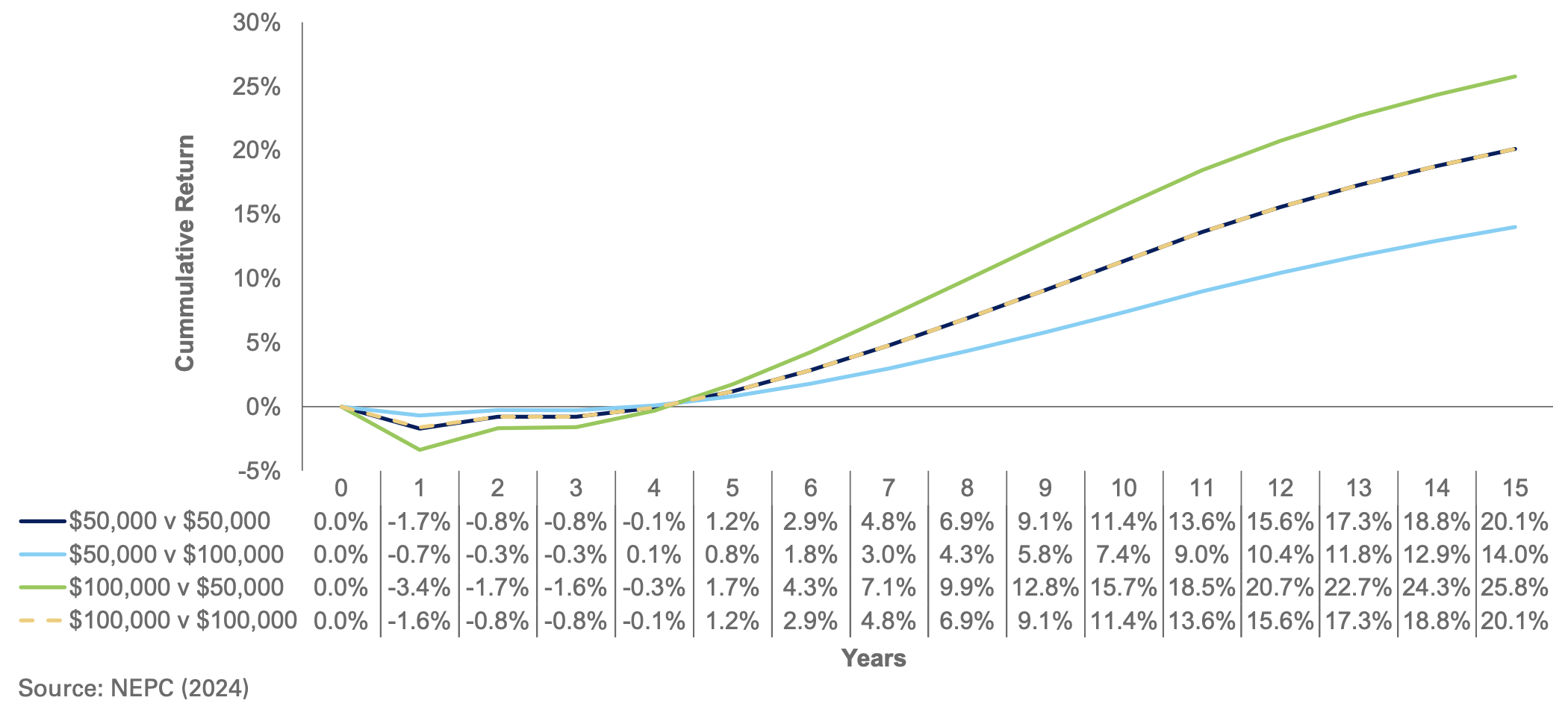

This chart from institutional investment consulting firm NEPC shows that retirement plan participants who are automatically enrolled in auto-escalation programs, gradually increasing their contribution rates, accumulate significantly more wealth over time than those who are not.

The numbers on the lower left show how an employee’s salary path can affect savings growth.

For example, if you start your career earning $50,000 and you work your way up to $100,000, you can make larger contributions, in dollar terms, and maybe also in percentage terms.

If those raises are combined with just a 1% annual increase in your 401(k) contribution rate, it can lead to much faster account growth. Of course, if you increase the contribution by a higher amount, like 2% or 5%, you’ll probably see growth at an even more rapid clip.

Worth noting: That early dip into negative territory happens because the chart includes market ups and downs, which investors should expect. In the first few years, investment returns may be negative, even though you’re adding to your contributions. Over time, as balances and contributions grow, the positive compounding kicks in and the account climbs steadily. (In the meantime, during the down years, you’re dollar cost averaging, so don’t get discouraged!)

Over 15 years, the compounding effect of steady contributions results in a 14% higher account balance, even after netting out investment fees.

Of course, if you don’t sign up at all for your 401(k) plan, or manually enroll or change settings instead of putting it on cruise control, you may still fall short of your savings goals.

Mistake 2: Ignoring Fees and Poor Asset Allocation

Research from brokerage Charles Schwab shows that lower-cost funds deliver better investment outcomes. That makes intuitive sense; if a fund manager takes a bigger fee, that’s less money going into your pocket when compared to a similar fund with a lower fee.

Here are some examples of how that might work, using specific investments.

S&P index funds*:

- Vanguard Institutional Index Fund (VIIIX)

- Fidelity 500 Index Fund (FXAIX)

- T. Rowe Price Equity Index 500 (PREIX)

*There’s often a mistaken assumption that S&P funds are only available in an ETF wrapper; in fact, there are some low-cost mutual funds that also track the index.

Mistake 3: Missing The Employer Match

If your employer offers a 401(k) match, it may be one of the most powerful ways to boost your retirement savings—essentially free money added to your account. This money is intended to help encourage you to keep saving, but it’s really also part of your compensation.

Fidelity report, “7 Types of ‘Free Money’ You Don’t Want to Miss," August 5, 2025.

That employer match is yours for the taking, so why lose out on that money?

For example, say your salary is $100,000. Your employer offers a 50% match on your 401(k) contributions, up to 6% of your salary.

In other words, for every dollar you contribute, your employer will contribute 50 cents, but only on the first 6% of your salary. So:

- You contribute 6% of $100,000 = $6,000

- Your employer matches 50% of that = $3,000

- Total going into your 401(k) = $9,000

This chart from Empower shows how contributing to your 401(k), especially enough to receive your full employer match over time, can substantially boost your retirement savings.

In this example, an employee earning $65,000 who contributes 5%, meeting the employer match, can retire with more than $1 million. In contrast, a saver who contributes just 2% ends up with just $433,000.

The chart is a good illustration of how your employer match, along with the magic of compounding, can help maximize your retirement account value over 40 years.

Maximize Every Retirement Dollar

Don’t overlook small tweaks that can eventually lead to bigger balances. These aren’t dramatic changes, but they can add up.

- Automate contributions and yearly increases to build momentum.

- Watch the fees: Low-cost funds often perform just as well, or even better, than higher-cost investments. Higher fees cut into your return.

- Always grab the full employer match. That’s part of your compensation, not a bonus.