Think Like Investing Icon Jack Bogle … Or a Black Lab

Investors of all ages benefit from maintaining a recommended asset allocation in turbulent markets

You've reached your free article limit

You've read 0 of 1 free Pro articles.

There’s an endless parade of wildlife meandering through my yard.

A creek runs behind my house, and it’s a daily occurrence to see ducks, geese, woodchucks, rabbits, and, in the warmer weather, a blue heron. Once in a while, I’ll spot a fox.

But the most frequent visitors are the deer.

A few months ago, I looked out my front window and saw a fawn helping itself to the rosebushes, thorns and all.

While this happened, my black lab, Annie, stared out the window, mesmerized. She couldn’t look away, but she wasn’t freaking out and barking or growling, either.

Annie reminds me a famous investor. Can you guess who?

Jack Bogle, that’s who. Well, in one sense, anyway.

Build Wealth With Disciplined Investing

Bogle, the famed founder of Vanguard Group, was among the pioneers of index fund investing.

He advocated using a sensible, long-term asset allocation strategy, rather than constantly shuffling portfolio holdings to chase returns or avoid downturns.

A quote widely attributed to Bogle is “Don’t just do something, stand there!”

Whether or not he actually said that doesn’t matter; it’s an accurate reference to his investment philosophy. In fact, Bogle’s 2018 book was titled “Stay the Course.”

Investors who closely watch the major indexes or their own portfolios are conditioned to react to every market move, but that’s not how wealth is built.

When markets become volatile, when prices plunge or soar, it’s understandable to be captivated by the action, just like my dog staring down that deer.

But that doesn’t mean you should leap into action.

Bull and Bear Cycles are Normal

That’s where asset allocation comes in.

Let’s come back to that deer for a minute. Around here, it’s not at all surprising to see deer wandering around, but it can still be exciting to see one at my front window.

Bullish (upwards) and bearish (downwards) cycles in the market are also completely normal, no matter the cause.

Rather than reactively making portfolio changes, a better approach is to carefully consider whether your investment mix is designed to weather any market condition.

Here’s a quick glance at how this might look for three groups of investors: Young savers in the accumulation phase, mid-career investors who know when they plan to retire, and finally, retirees (including those who are about to retire).

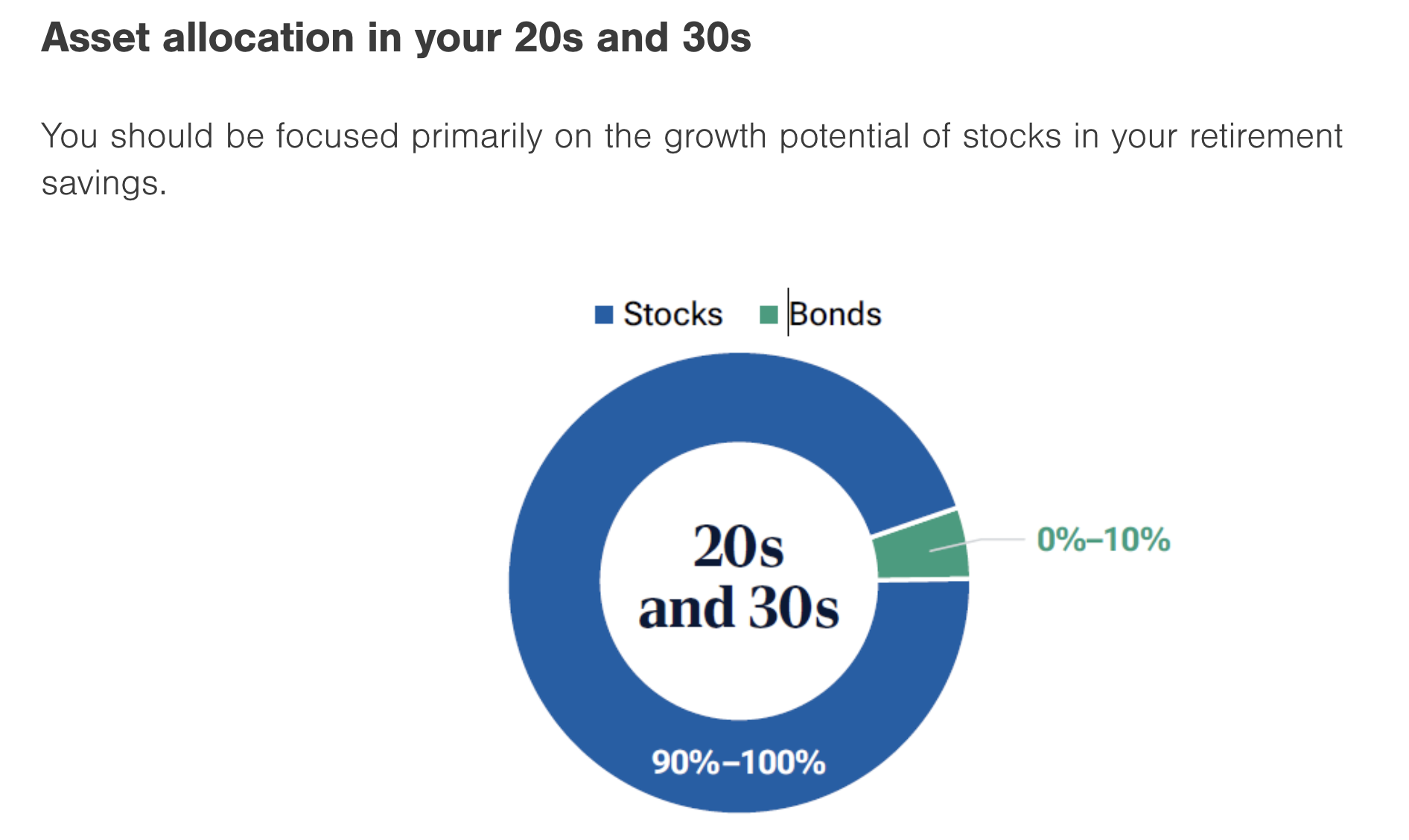

Asset Allocation for Young Investors

Investors in their 20s and 30s and even early 40s have the runway ahead of them to take more risk.

For the youngest savers, those in their early 20s just beginning their careers and investing with small amounts of money, over-diversifying is a risk that may dilute returns.

For someone in this category, there’s nothing wrong with just investing in a single U.S. index tied to something like the S&P 500 Index. But for those who are contributing regularly to a 401(k) and are in the process of accumulating assets, a small allocation to fixed income can help mitigate stocks’ volatility.

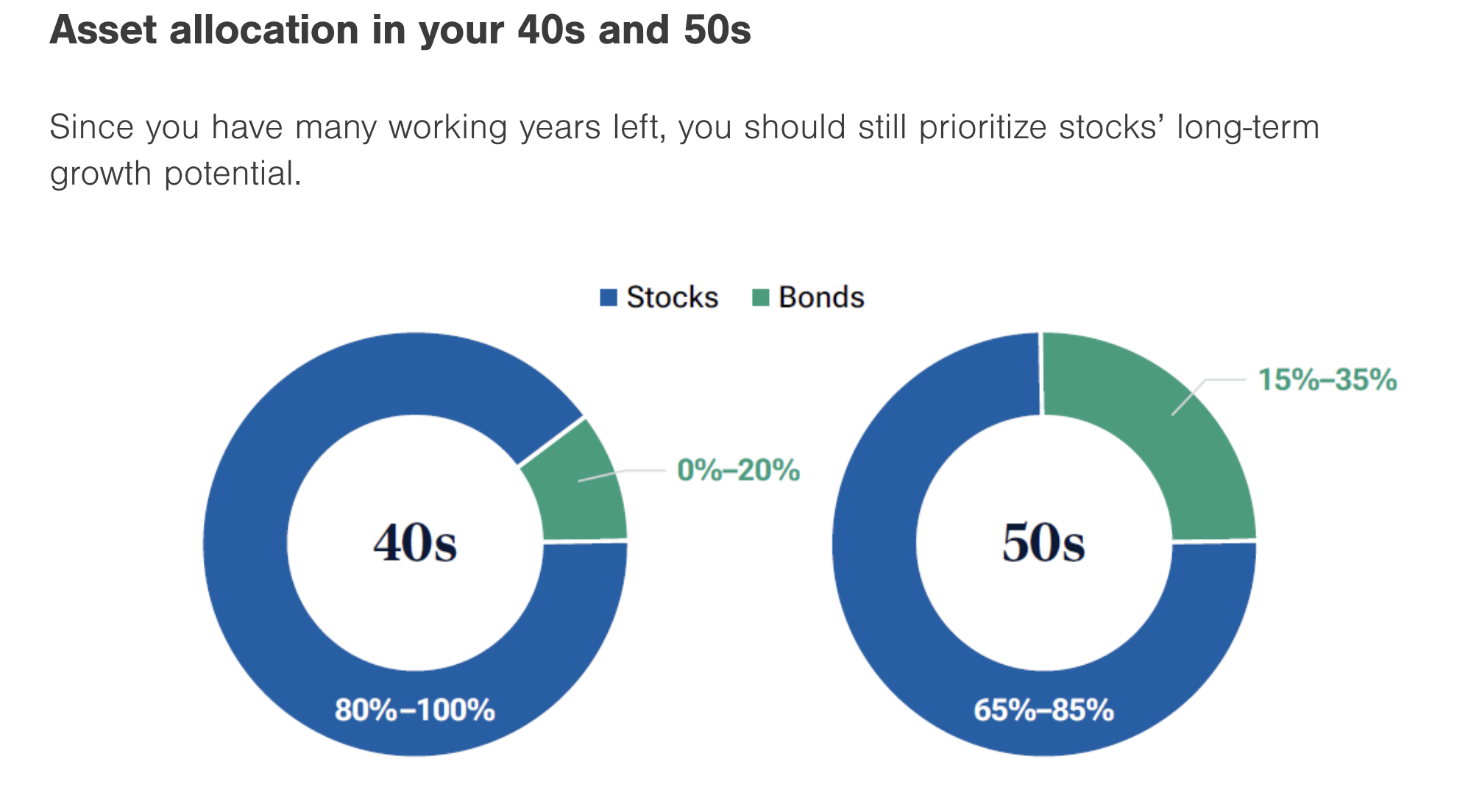

Asset Allocation for Mid-Career Investors

In your peak earning years, you’ll probably find yourself balancing several financial objectives.

But try to avoid the mistake many people make at this age, of sacrificing their own retirement funds while simultaneously saving for kids’ college.

T. Rowe Price recommends that you aim to have three times your income saved by age 45, five times by 50, and seven times by age 55. Even small increases in contributions now can make a big difference later, and once you turn 50, catch-up contributions allow you to boost savings even more.

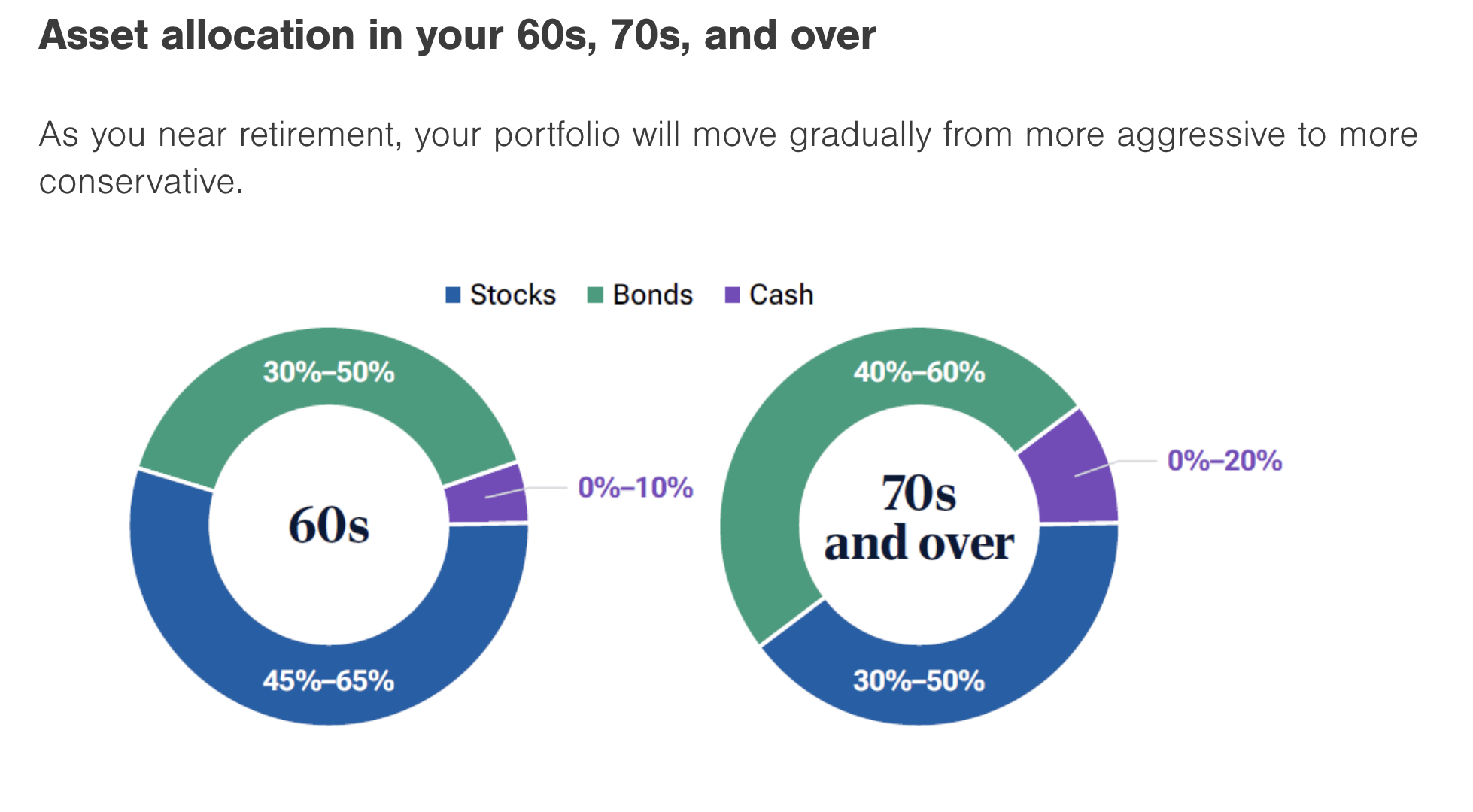

Asset Allocation for Investors in or Near Retirement

Longer life expectancies means retirement can last 30 years or even longer. That's good news, right? But living longer has one downside.

Your parents or grandparents could get by holding mostly bonds for income, along with some blue chip dividend stocks, because the money didn't need to last as long.

But, a longer life means you need the growth from stocks to stay ahead of inflation as well as holding bonds and cash pay for your lifestyle and manage short-term risk.

In the next few emails, I’ll dig deeper into investment strategies for retirement savers at different phases of life. Sometimes the conventional wisdom is absolutely correct, but other times there’s either new research that’s applicable, or an approach that takes your unique situation into account.

But whatever your stage of life, it’s better to be Annie the black lab, calmly watching the deer instead of barking up a storm. Even better, you can be like Jack Bogle, and rather than “doing something” by madly trading in an effort to stem losses or build gains, consider just standing there.