The Temptation That Almost Took Me Out of the Investment Business

The most embarrassing moment of my career taught me lessons that kept me in the business. These lessons can help you in times like now.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Every investment professional has a moment they’d prefer to forget. Mine happened early in my career — just before the dot-com bubble burst — when I was managing private client portfolios and running model strategies for other RIAs. The markets were roaring higher, quarter after quarter. Clients were happy. AUM was growing. And I felt pressure — pressure to keep up, pressure to beat the indexes, pressure not to look out of touch.

Back then, I approached investing the same way I often discuss today: bottom-up, quality-first, valuation-aware, with a focus on durable cash flows. Think of it as a business owner lens applied to public equities. It worked. Until it suddenly didn’t.

As the markets pushed relentlessly upward, I found it harder and harder to beat the benchmarks. And that’s when the temptation crept in.

How I Got Sucked In

I wish I could say I resisted. I didn’t.

Like many young investment managers today, I drifted toward the belief that to survive, I had to follow the crowd. I convinced myself that owning more of the largest market-cap names was “prudent.” After all, those names were driving the index. Those names were in the headlines every day. And those names were what investors kept asking me about.

So I made a critical mistake: I adjusted my models so that market cap — not fundamentals — became the primary driver of my portfolio weights.

In plain English, the bigger the stock, the more I owned. I drifted away from my discipline. I let the crowd pull me in.

And then the bubble burst.

The Email I’ll Never Forget

During that chaotic period, I was pursuing new business. I met with a highly respected investment management firm — one with an exceptional long-term track record. Their portfolio manager asked for my holdings and weights, which I sent over confidently enough.

The email he sent back was short. Very short.

“Thanks for sending your holdings. I’m not interested. Your holdings were very telling.”

That was it.

No explanation. No lecture.

But I knew exactly what he meant.

He could see that I had abandoned my fundamentals. He could see that I let market cap dictate my decision-making. He could see that I had been sucked in.

It was one of the most embarrassing moments of my entire career. But it was also one of the most valuable, because it forced me back to first principles. It forced me to remember who I was as an investor.

The Same Temptation Is Back — and Stronger

Fast-forward to today.

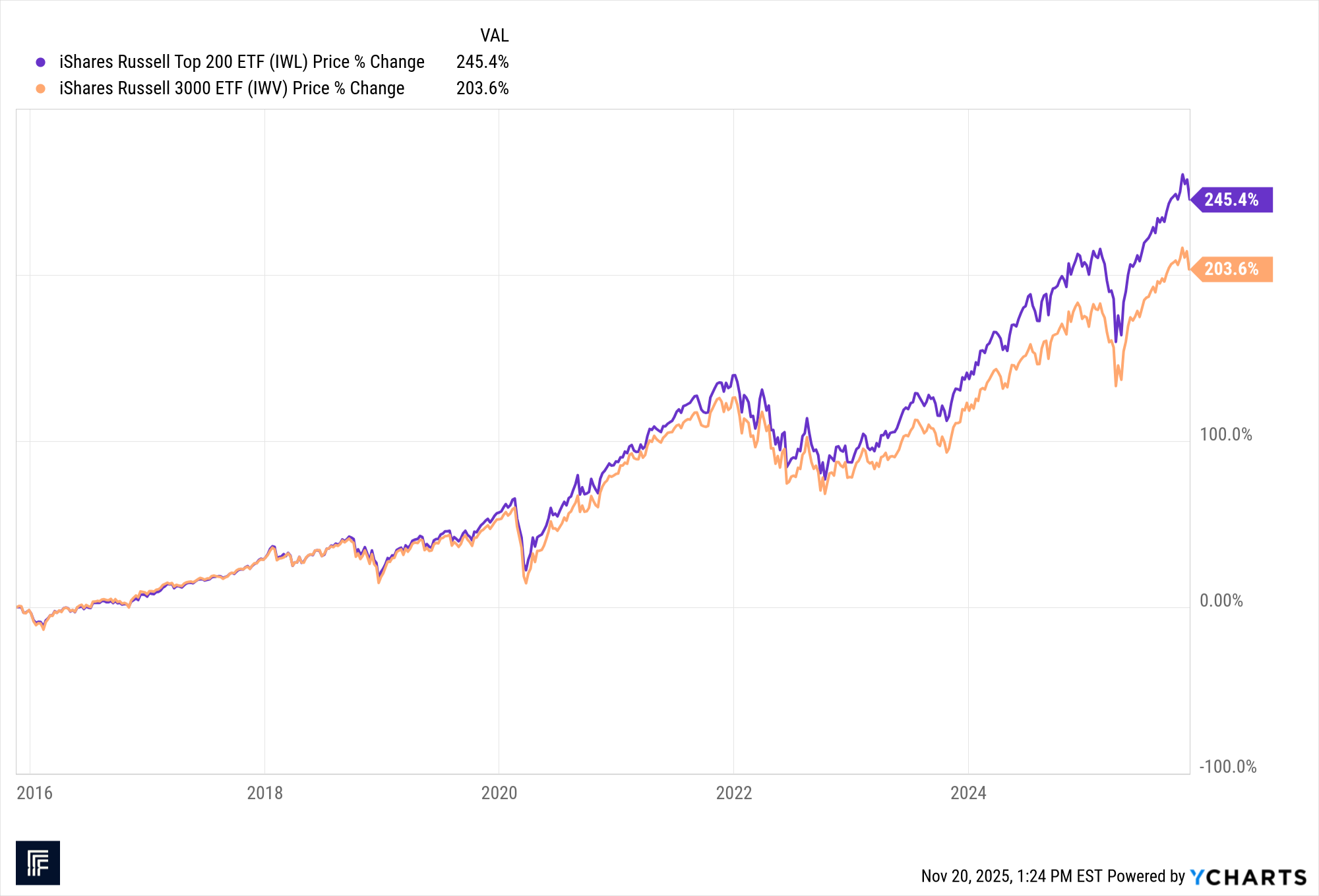

The same pressure that I felt then, you may be feeling now. The top 200 Russell names are crushing the broader index. The mega-caps dominate every headline. These companies seem invincible. Their fundamentals are incredible. And the narrative is intoxicating:

“How can you go wrong owning these?”

But you can go wrong.

You can go very wrong.

I’m not saying the top will happen this month. I’m not saying it will happen this year. Fundamentals still look strong. AI is a real economic force — much like the early Internet — with legitimate second- and third-order opportunities. The private equity investor I sat next to on a recent Austin-to-Dallas flight told me the same thing: power infrastructure, data centers, AI-enabled services — the real spend is still accelerating.

This is not fake. It’s not illusory. The long-term innovation is real.

But bubbles are always built on real innovation. The excess comes from behavior.

The Discipline That Saved Me

After that embarrassing wake-up call, I corrected course quickly. I returned to fundamentals, returned to discipline, returned to the blocking and tackling that actually compounds capital over time.

Today, I use the same lens I should have stuck to then.

Ask simple questions:

1. Profitability: Are they earning real economic profits?

2. Balance Sheet Strength: Can they withstand shocks?

3. Product & Competition: Are they selling something valuable, differentiated, and durable?

4. Valuation: Am I being compensated for the risk I’m taking?

In other words: Quality. Valuation. Fundamentals.

Yes, I’m a quant. I run quantitative models all day. But even the best factor strategies with value components have lagged against cap-weighted indexes. “Value” isn’t fashionable right now. It wasn’t fashionable in 1999 either.

That’s precisely the danger.

What I’m Doing Now

I’m leaning into the things that compound capital — not the things that make headlines.

Dividend Growth Strategy:

Companies with consistent dividend increases, strong profitability, and discipline. If they cut the dividend, they’re out. It’s simple, powerful, and grounded in real economics.

Select Equity Strategy:

A bottom-up strategy that blends fundamentals, growth, and intelligent momentum — without chasing hype or market-cap distortions.

Diversification:

I’m not ignoring fixed income. If a security cannot compensate me above the risk-free rate with a meaningful spread, I’m not allocating to it. Simple as that.

Avoiding the Hype:

I’m not paying 100x sales for anything. Not earnings — sales.

A Final Warning (and an Encouragement)

If you’re a long-term investor, your goal should be simple:

Compound capital.

Avoid permanent loss.

Let volatility work for you, not against you.

If you want to trade, that’s fine — just do it separately. But for wealth that needs to last, stick to the basics. The boring stuff. The repeatable stuff. Quality, valuation, technical confirmation — QVT.

And remember this: One of the easiest ways to avoid blowups is to eliminate the worst technical performers from your investable universe. Don’t try to catch falling knives. Don’t own the bottom quartile of momentum unless you have a very specific reason.

The lessons that embarrassed me early in my career kept me in the business. Maybe sharing them now will keep someone else out of trouble too.

Happy investing!