The Retirement Planning Hack Wall Street Doesn’t Talk About

Why smart investors focus on buckets, not just stocks.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Nearly two in three Americans (64%) worry more about running out of money than death.

Allianz Center for the Future of Retirement, 2025 Annual Retirement Study

This might surprise you, especially if you’re someone who’s an avid stock market follower or trader: How you plan and organize your money in retirement is often more important than the actual investments you hold.

Don’t misunderstand: The investments are absolutely important, and it’s possible to own a pile of stuff without any cohesive plan to generate the retirement income you need.

But here’s what the stock jocks get wrong: The process of decumulation requires an entirely different mindset from looking at the hot new IPOs. (You can keep doing that for fun, outside of your retirement plan.)

Retirement Planning

In or near retirement, you have several other considerations to juggle, including:

- Withdrawal rates

- Location of assets

- Tax strategy

- Social Security and Medicare

- Other income sources, such as pensions or annuities

In the past few issues of Filthy Rich Animal, we’ve given you the rationale for investing your retirement money in a balanced mix of stocks, bonds, and alternative assets. The idea is to construct your portfolio so it can weather market cycles and support sustainable withdrawals.

We also gave you some sample portfolios for an idea of the types of ETFs you can use. In every case where you’re looking at an investment in a broad asset class, or sometimes even a narrow sliver, you’ll find more than one fund that does the job.

Why Your Investment Strategy Must Change

Can’t you just keep your current portfolio and pull income as needed in retirement? Well, it depends.

- Withdrawing during a downturn can shrink your savings much faster.

- The same average return can have very different retirement outcomes.

- Early losses plus withdrawals can cause lasting damage.

- Later market gains can’t always undo early losses.

- You can separate spending and growth money to reduce damage.

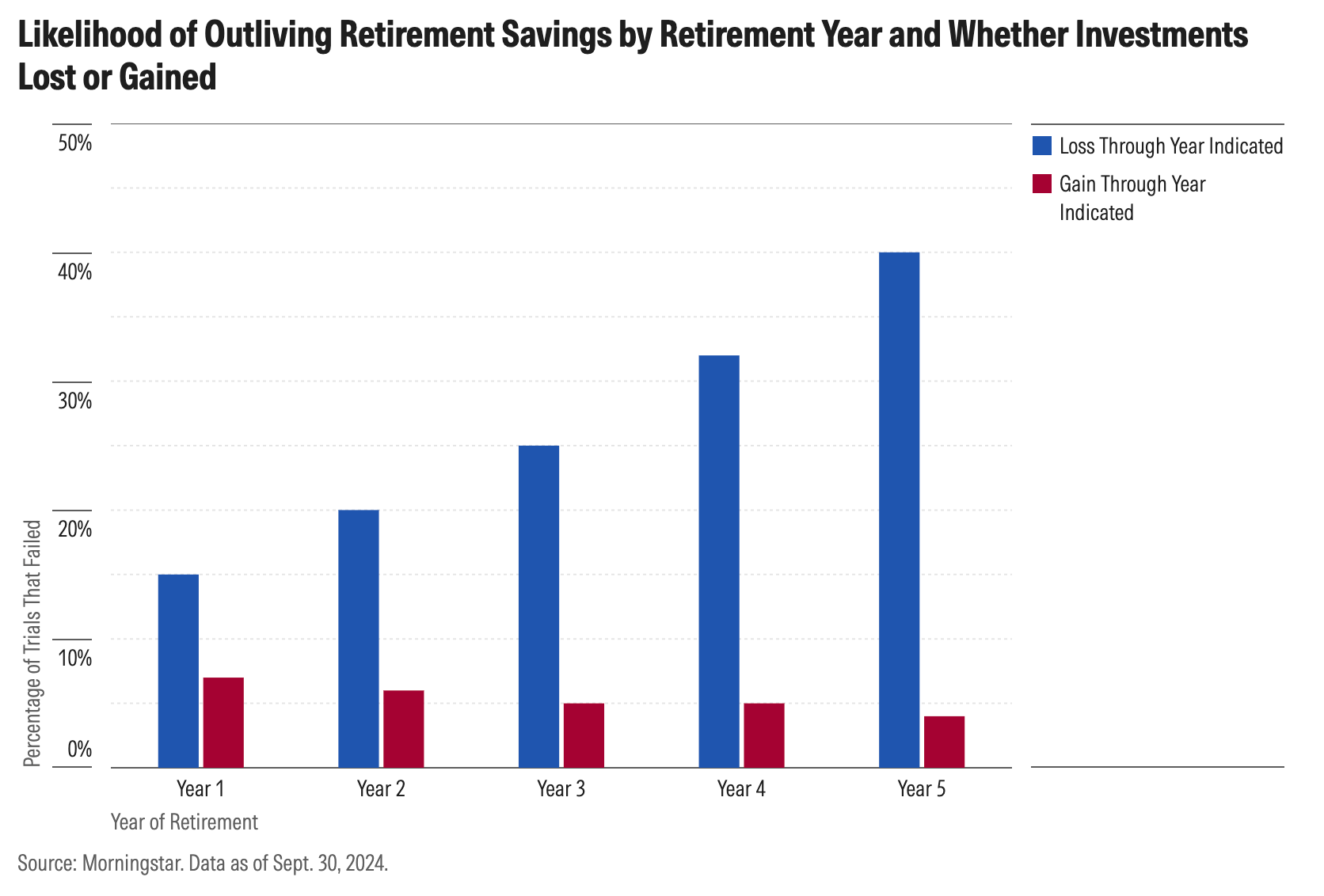

We reviewed the concept of “sequence of returns” risk in an earlier email. As a refresher, here’s a chart from Morningstar that illustrates the damage that can occur when the market turns south soon after a person retires and begins making withdrawals.

Introducing the Bucket Strategy

You can segment or "bucket" money based on the timeframe of income needs. Here’s how that might look.

Bucket 1: Years 0–5

This is the money you’ll need in the first five years of retirement.

Its goal is to protect principal and meet income needs not covered by other sources like Social Security.

These assets should be ultra-conservative: high-yield savings accounts, Treasury bills, CDs, fixed annuities, and bonds.

The silver lining of today’s higher interest rates is that these vehicles now yield 4% to 6%, much more than just a few years ago.

Bucket 2: Years 5–15

This money is for medium-term needs.

It should be invested in a balanced mix: longer-term CDs, fixed annuities, individual bonds, dividend-paying stocks, and index funds.

The goal here is steady growth and moderate income.

Bucket 3: Years 15+

This is your long-term growth bucket. It can be invested more aggressively in stocks, real estate, and potentially alternative assets.

Why 15 years? Because the S&P 500, historically, has never lost money over any 15-year period.

This bucket has the highest growth potential and is designed to ride out volatility.

Maintaining the Buckets Over Time

As you draw down Bucket 1, the income and dividends from Bucket 2 automatically replenish it.

If that’s not enough, you can tap into principal from the fixed income side of Bucket 2, keeping your stock positions intact to allow for more growth.

It’s good practice to trim profits from your long-term assets (Bucket 3) every 10 years to support income needs.

Over time, you may gradually shift some money from stocks to more stable assets, but as a rule of thumb, most people should keep 30% to 40% of their portfolio in stocks at any age for long-term growth.

Playing the Long Game

This strategy can help you enjoy your retirement without the stress of market volatility impacting your lifestyle.

By aligning your portfolio with real-world income needs and timeframes, you can protect your spending in the short term, and give your investments the runway they need to grow for the long haul.