The Portfolio Strategy Everyone Buried Is Quietly Ready for a Comeback

Bonds are back and it's time to rebalance.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

2-27-26-portfolio-shutterstock_2684318391

2-27-26-portfolio-shutterstock_2684318391

We’ve all heard it: “The 60/40 portfolio is dead."

The idea of regularly rebalancing a portfolio of index funds was considered a sickly remnant of a bygone era, something today’s smart investors would mock.

And yes, there were even memes.

YouTube

The sentiment hasn’t been entirely wrong (especially the thumbnail proclaiming "Bonds Are Dead"), but there’s more to the story.

When stocks and bonds both fell in 2022, it became fashionable to say diversification had failed. Balanced portfolios were “broken.” Bonds weren’t an effective equity hedge. The classic allocation was dead and buried.

But now, something is starting to become clear: The problem wasn’t diversification.

It was starting yields, or the yields on bonds at the time you buy them.

That’s not just some academic talking point. It's absolutely the most important driver of future bond returns.

It Wasn’t Diversification. It Was Math.

When high-quality bonds yield 1% to 2%, you can pretty easily model out expectations for their future returns. Even if they provide portfolio ballast, you know they probably won’t contribute much to long-term growth.

During the zero-rate era, bonds did their job defensively by mitigating stocks’ volatility, but they weren’t positioned to drive meaningful portfolio returns.

But, as it turns out, it wasn’t exactly a “This time it’s different” moment for the ages.

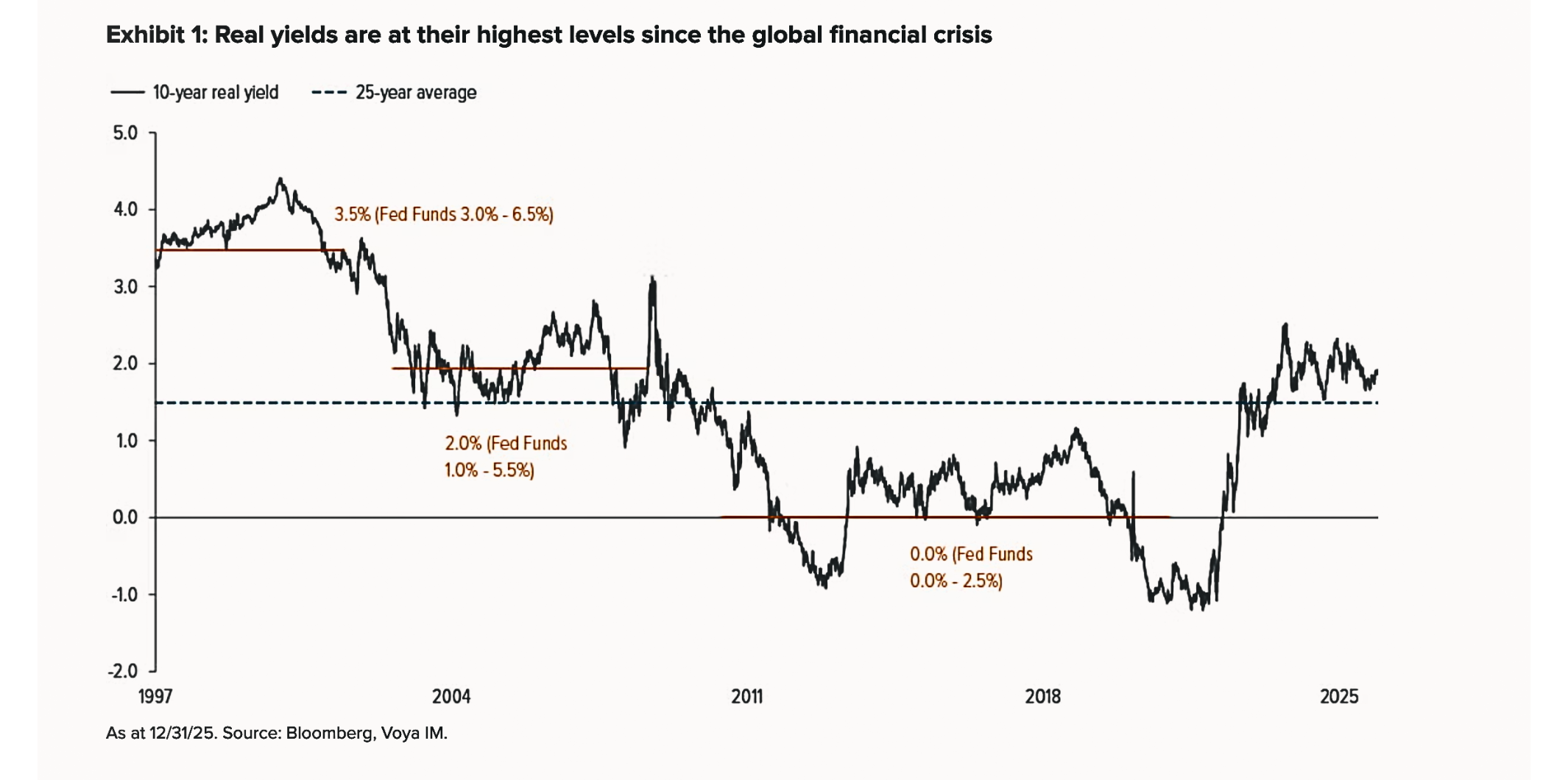

In a January note, “3 Risks, 3 Opportunities in Fixed Income for 2026,” Jeffrey Hobbs, CFA, Voya’s chief investment officer for fixed income, wrote that elevated real yields are reshaping portfolio construction.

At the moment, corporate bonds don’t offer much extra yield and stocks are priced to perfection, leaving little room for error if earnings disappoint or economic growth slows.

As Voya’s Hobbs noted, “With real yields at generational highs, fixed income is a very attractive place to be right now.” In other words, investors may now want to start looking at income, rather than price appreciation, to drive results.

Among Voya’s findings:

- Real, inflation-adjusted yields are higher than they've been in years.

- Investors are finally earning a meaningful real return again.

- Bond income hasn't looked this attractive since the post-financial crisis era.

This chart from Voya shows you how 10-year yields are at their best levels in more than 15 years.

Voya

But Wait: If Yields Are Higher, Don’t Stocks Suffer?

Yes and no.

Rising yields can certainly pressure equity valuations, especially when it comes to high-growth stocks.

Think of techs. Higher interest rates make next year’s profits less valuable in today’s dollars. That can shrink the price investors are willing to pay for each dollar of earnings.

That’s part of what happened in 2022.

But here’s how that balances out:

- Higher yields today mean better bond returns from here on out.

- Cheaper stocks now set the stage for stronger equity gains ahead. That’s the whole premise of value stocks.

Starting conditions matter more than all the scary headlines. Right now, bonds are offering real competition to stocks for the first time in years. That shifts the way you’d construct a portfolio.

Back to Our Friend, the 60/40

Higher bond yields mean:

- More income from the defensive side of the portfolio.

- Better downside cushion. (Which is what you want bonds to do all the time.)

- Stronger rebalancing opportunities in times of stock-market volatility.

Balanced portfolios become less dependent on those eye-popping stock returns.

Proceed With Caution

Now, this doesn’t mean that everybody should just default to the 60/40. If you’re younger, you can probably take more risk.

If you’re older, you’ve been very fortunate in the past 15 years, in that you’ve been able to load up your portfolio with techs and faced minimal downside risk.

If that sounds like you, you may want to rethink things.

For all investors, it’s time to consider that the conditions that made a 60/40 portfolio look weak — ultra-low yields and sky-high stock valuations — are no longer as extreme.

So to paraphrase Mark Twain, reports of the 60/40’s death were premature. Diversification hasn’t stopped working, but it works better when both sides of the portfolio actually pay you.

Related: Cracks Appear in Credit Markets Amid Echoes of Great Recession