The Not-So-Hidden Costs of Forgetting Your 401(k)

Flexibility beats neglect in retirement planning

You've reached your free article limit

You've read 0 of 1 free Pro articles.

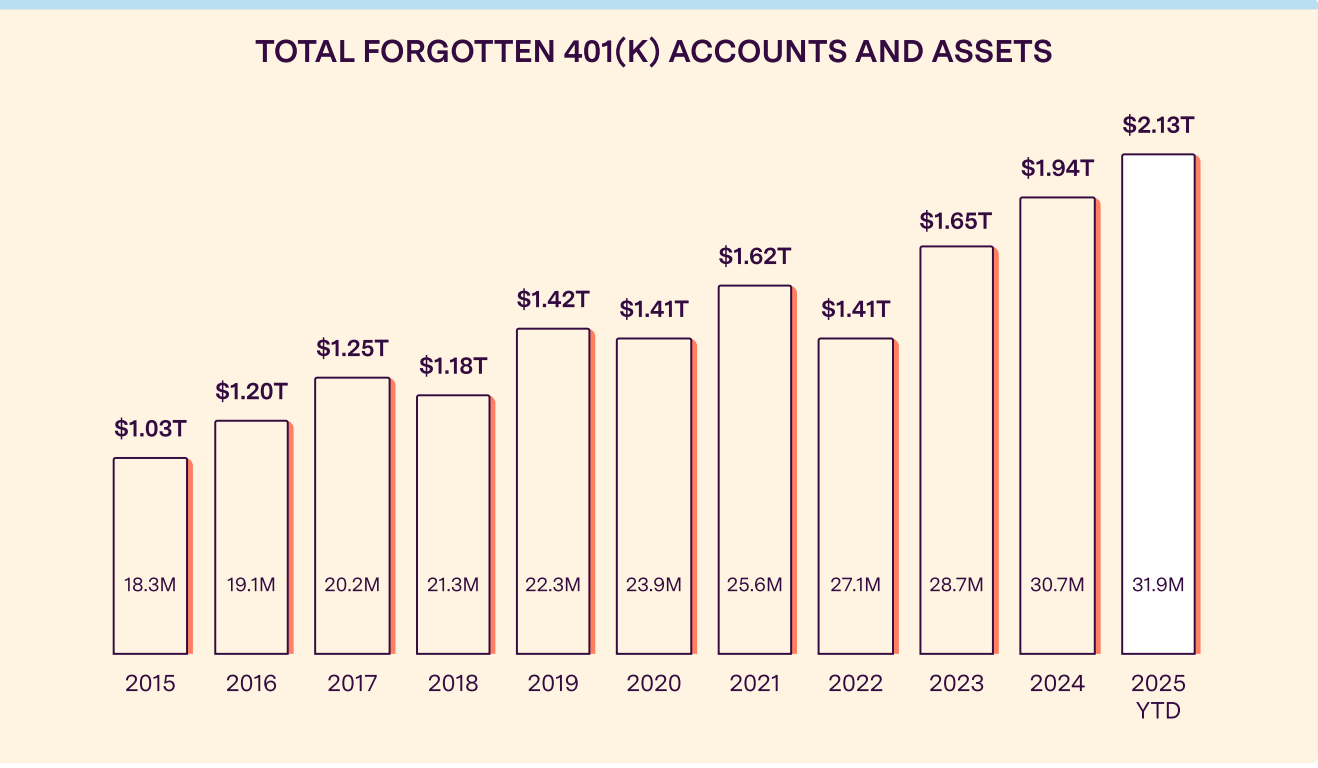

$2.1 trillion, with a “t.”

That’s how much has been left in 401(k) accounts after employees change jobs, get laid off or retire, according to a new report from Capitalize, a company that helps facilitate 401(k) rollovers. That’s a 30% increase over 2023, the last time Capitalize issued its forgotten 401(k) report.

When you leave a job, you might think moving your 401(k) to an IRA is something to do later (whenever that is). What often happens, though, is weeks turn into months, which turn into years.

Life happens, and you’ve moved on to other adventures and that 401(k) isn’t anywhere near top of mind. You might even have another account, with a new employer, that you’re more interested in.

Rolling Into More Flexibility

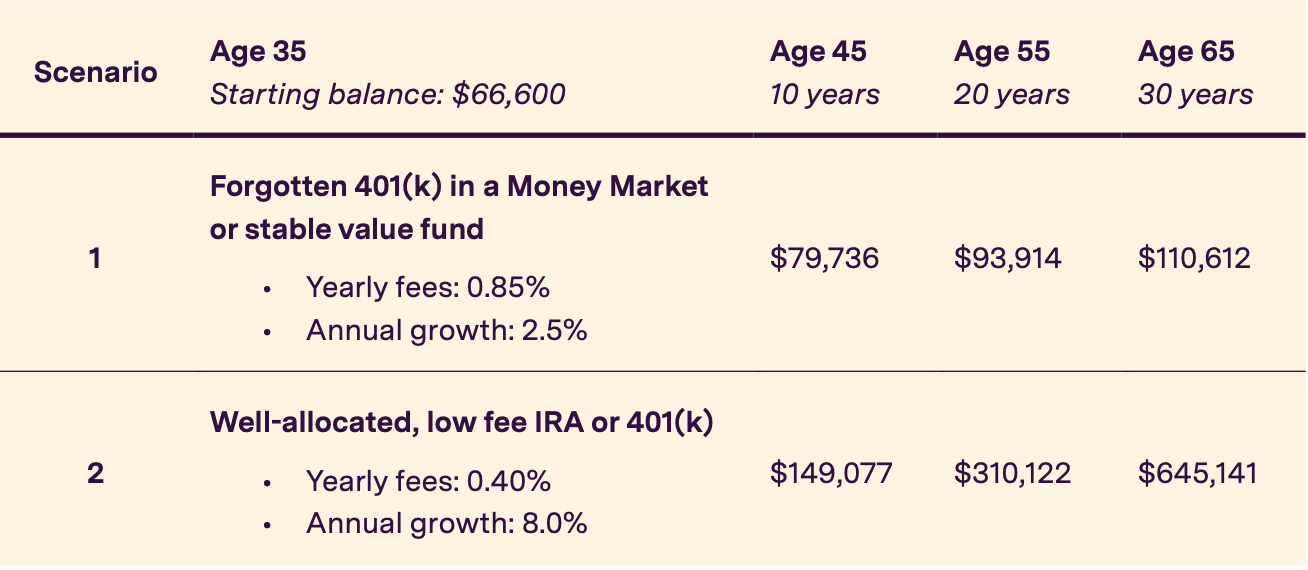

Your 401(k) may have great fund choices and you may have it allocated in a way that’s suitable for your time horizon and risk tolerance. But you’d only know that if you researched the funds, including expense ratios and composition, and determined whether your account was balanced, holding numerous non-overlapping asset classes.

Spoiler alert: Most 401(k)s are not so well allocated. This chart from the Capitalize report shows the performance and expense gaps between a forgotten 401(k) account and one that’s been rolled over.

Most of the time, moving your money to an IRA, whether traditional or Roth, will give you more fund choices at a lower cost. If you use a robo-service or get help from a planner, you have the option of low-cost ETFs, rebalanced at intervals so you don’t have to worry about getting the allocation right.

Are Safe Harbors Too Safe?

There’s something else to keep in mind. Because of changes in the SECURE 2.0 act, more 401(k)s will be forced into “Safe Harbor” IRA rollovers, which typically invest in ultra-conservative vehicles, namely cash and cash equivalents, like money market funds.

These returns will, by definition, fall short of a portfolio made up of stocks, bonds and other assets, like alternatives.

How to Approach the Rollover Process

Weirdly, in 2025, rolling over a 401(k) often requires phone calls and mailing paper checks, things even Boomers don’t want to mess with anymore, never mind Gen Zers. That cumbersome process discourages people from getting started, but it’s usually worth it,

I’ve written many times here about the importance of proper asset allocation and glide paths to help investors reach retirement goals, so I won’t repeat all that today.

Here’s a look at how a 35-to-45-year-old might implement new rollover IRA investments. As always, these ETFs are examples; other products serve the same purpose and get similar returns, at a similar cost. Think of this as the packaged food box with a pretty picture that says, “Serving suggestion.”

Equity (60%-75%)

• U.S. large-cap: iShares Core S&P 500 ETF (IVV)

• U.S. small/mid-cap: iShares Core S&P SmallCap ETF (IJR)

• International developed/emerging: Fidelity Global ex U.S. or iShares MSCI EAFE (EFA)

Fixed income (15%-30%)

• iShares Core U.S. Aggregate Bond ETF (AGG)

• iShares TIPS Bond ETF (TIP)

Alternatives (5%-10%)

• Schwab U.S. REIT ETF (SCHH) or iShares U.S. Real Estate ETF (IYR)

• Invesco DB Commodity Index Tracking Fund (DBC)

These portfolios are tilted toward equities, which is a suitable approach for investors in their 30s or 40s. Older investors should, in general, tilt more heavily toward less risky assets, although that guideline should be tailored toward each investor’s unique situation.

A Glimpse Into Returns

While you might think of rollovers as something you do at retirement, there’s a lot of power in the middle years when you can shape the trajectory of your returns.

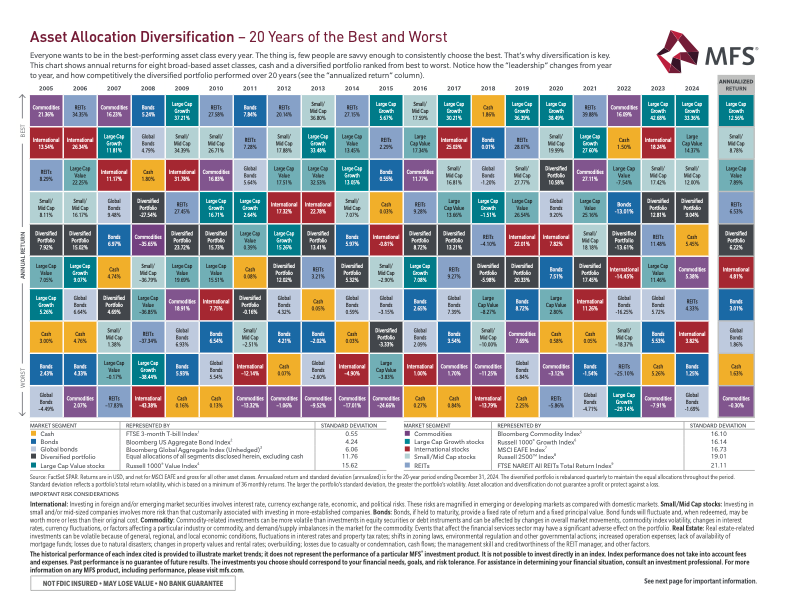

I like this periodic table of investment returns, which shows how various assets cycle in and out of leadership; that’s why it’s so important to maintain a balanced portfolio.

You have more ability to own the right asset mix, at the right cost, if you opt for a rollover IRA, instead of the more limited selections in a 401(k).