The Hidden Trap Costing Investors Thousands — And the Simple Shift That Fixes It

There a cost that most fund investors overlook, which can significantly drag down returns over time. Here's what you can do to avoid the hit.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

You might have money outside of tax-advantaged accounts for a few reasons.

Maybe you maxed out your 401(k) or IRA; maybe you inherited money, cashed out stock options or rolled over funds from an IRA. Perhaps you just need some liquidity before you turn 59 ½, and want the potential of bigger gains than you’d find in a savings account.

Those are great reasons, but there’s a problem with investments held in taxable brokerage accounts.

When mutual fund managers sell stocks inside the fund, whether to rebalance the portfolio, meet redemptions or take profits, those gains get passed through to you as taxable income. You owe taxes even if you never sold a single share. Ouch!

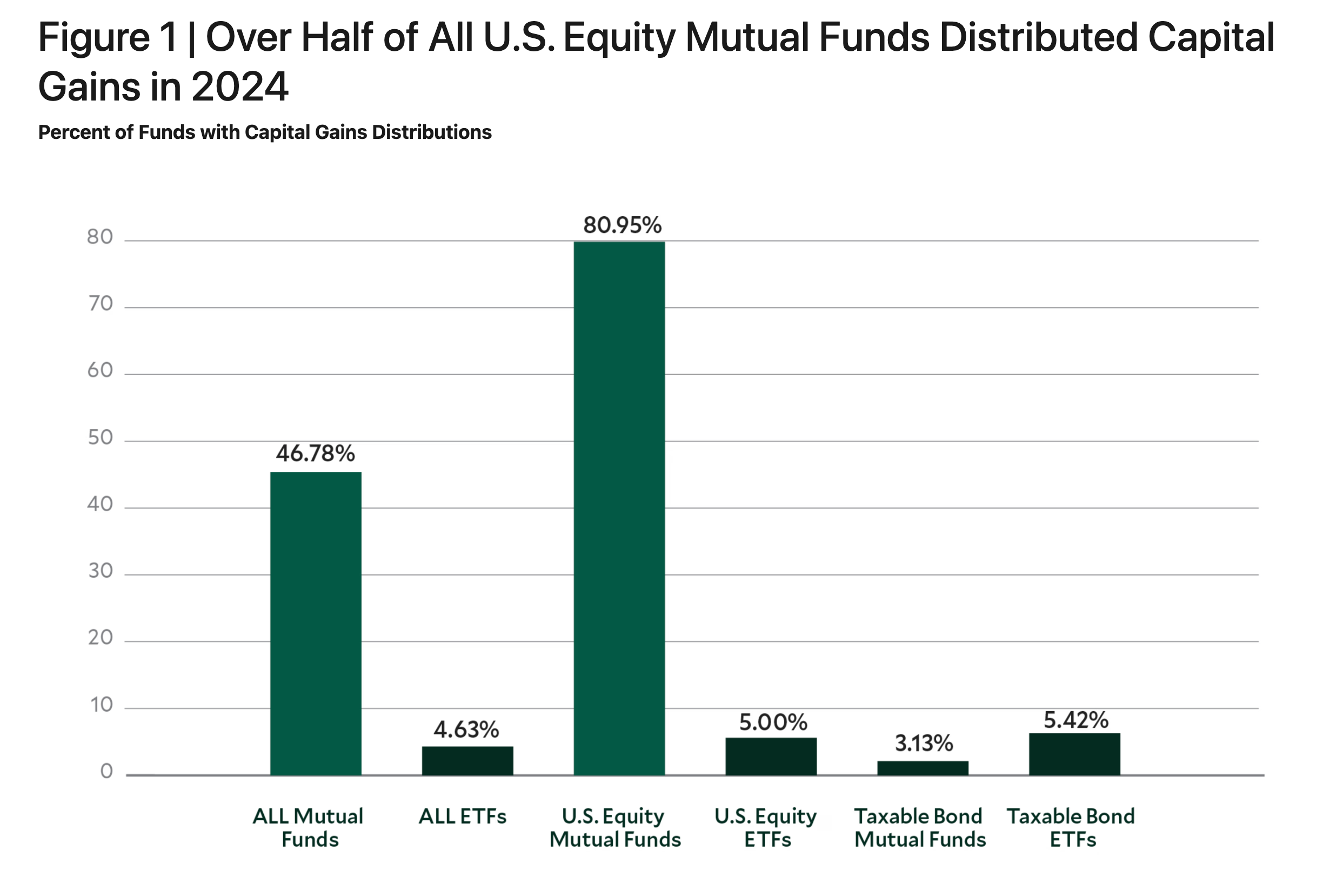

As this image from American Century Funds shows, more than 80% of U.S. stock mutual funds kicked out capital gains distributions to shareholders in 2024.

“The typical large-blend fund in Morningstar's database posted an annualized return of 11.97% over the decade ended July 2025. Meanwhile, the median tax-cost ratio of that same group of funds was 1.57%,” according to Christine Benz director of personal finance and retirement planning for Morningstar.

Benz points out that an investor in the highest tax bracket who owned an average-performing large-blend fund, held for a decade in a taxable account, would have owed about 13% of that return to tax collectors.

The difference compounds: Over time, choosing the wrong funds in taxable accounts can cost thousands in unnecessary tax bills.

Factoring in Tax Costs

The tax-cost ratio measures how much of a fund's annualized return is eroded by these taxes on distributions. It’s a good metric that quantifies a cost that most investors overlook, but which can significantly drag down returns over time.

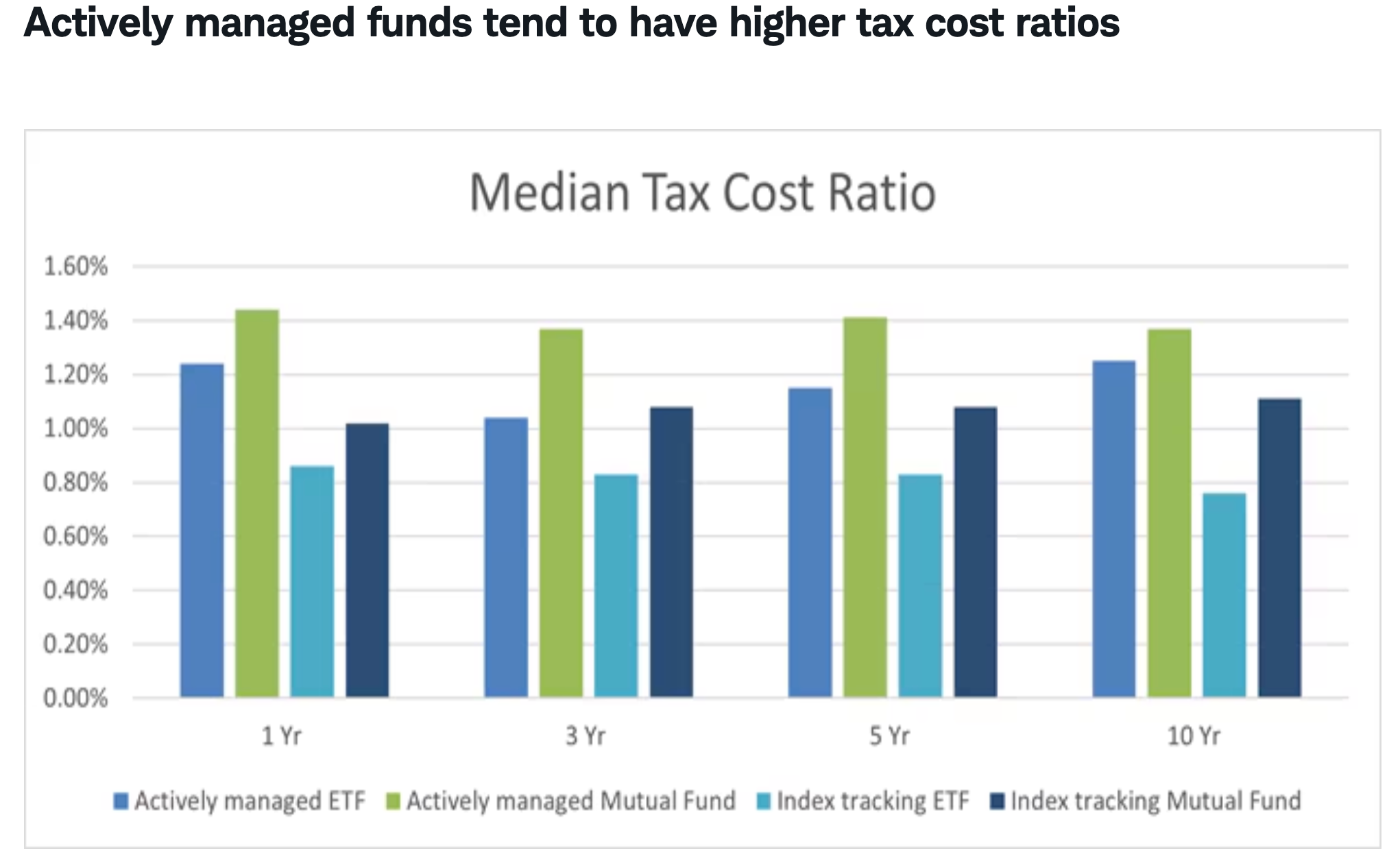

This chart from Schwab shows median tax-cost ratios by fund type, assuming the investor is in the highest tax bracket.

So What Should You Do?

Index funds keep trading to a minimum, versus active management. This low turnover equals fewer taxable events. Examples of tax-efficient index mutual funds include:

- Vanguard Total Stock Market Index Fund (VTSAX): Tracks entire U.S. market with minimal buying and selling.

- Vanguard S&P 500 Index Fund (VFIAX): Mirrors the S&P 500, only trades when index composition changes.

- Fidelity ZERO Total Market Index Fund (FZROX): Zero expense ratio, tracks total market passively.

- Schwab S&P 500 Index Fund (SWPPX): Low-cost S&P 500 tracking.

Another possibility is to lean into ETFs in taxable accounts. ETFs use an "in-kind" redemption process to avoid triggering capital gains.

Examples of tax-efficient ETFs include:

- Vanguard Total Stock Market ETF (VTI): Around 2% to 4% annual turnover, ETF version of VTSAX.

- Vanguard S&P 500 ETF (VOO): Low turnover with tight spreads, ETF version of VFIAX.

- Schwab U.S. Broad Market ETF (SCHB): Broad market exposure with minimal capital gains distributions.

- iShares Core S&P Total U.S. Stock Market ETF (ITOT): Comprehensive U.S. equity coverage.

These funds still generate dividend income, but it's typically qualified and taxed at lower rates.

Muni Bonds for Income Investors

Municipal bond interest is exempt from federal taxes and usually state taxes for bonds issued by your state, or a municipality within your state, with a few exceptions.

These are generally most suitable for investors in loftier tax brackets, such as 24% or higher.

- Vanguard Core Tax-Exempt ETF (VCRM): Actively managed by Vanguard's municipal bond team.

- Fidelity Tax-Free Bond Fund (FTABX): Diversified portfolio of investment-grade municipal bonds.

- iShares National Muni Bond ETF (MUB): Broad exposure to the U.S. municipal bond market.

- Vanguard Tax-Exempt Bond ETF (VTEB): Passively managed, tracks the S&P National AMT-Free Municipal Bond Index.

Municipal bond funds have the lowest tax-cost ratios due to low turnover and tax-exempt income. This actually means they’re not suitable for retirement accounts, since you’d be squandering the tax advantage.

Tax-Managed Funds

Another approach is to use funds with built-in strategies like harvesting losses, avoiding short-term gains, minimizing turnover and underweighting dividends.

Some examples of these investments are:

- Vanguard Tax-Managed Capital Appreciation (VTCLX): Tracks the Russell 1000 while underweighting dividend stocks and using tax-loss harvesting.

- Vanguard Tax-Managed Balanced (VTMFX): Invests roughly half in stocks tracking the Russell 1000 and half in municipal bonds.

- Vanguard Tax-Managed Small-Cap (VTMSX): Tracks the Russell 2000 while underweighting dividends and employing tax-loss harvesting.

- Alpha Architect 1–3 Month Box ETF (BOXX): Uses Treasury box spreads to convert ordinary income into deferred long-term capital gains.

- Separately Managed Accounts (SMAs) and Direct Indexing: Provide individualized tax-loss harvesting for investors with significant assets (typically $100,000 or more).

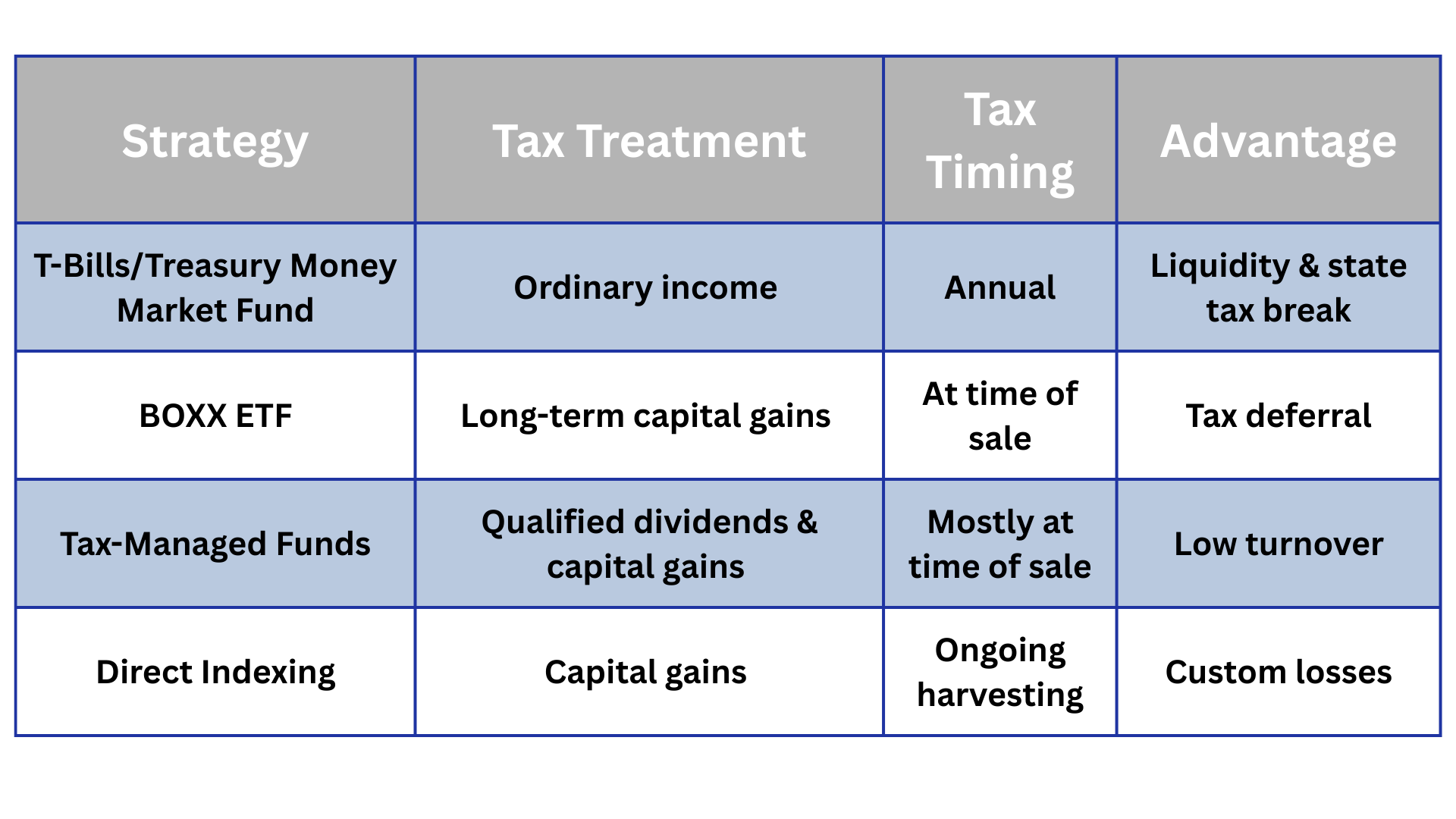

These funds vary in structure and objective; the chart below illustrates some of the potential advantages.

What to Avoid

If you want to mitigate the effects of taxes outside of accounts like 401(k)s, IRAs, 403(b)s and the like, steer clear of actively managed funds with high turnover.

Also, real estate investment trust (REIT) ETFs should be held in tax-advantaged accounts. By law, REITs must distribute 90% of their taxable income, with dividends taxed to investors as ordinary income.

You don’t want those tax bills popping up every year in a taxable account when they could be sheltered inside an IRA or 401(k).

Tax efficiency becomes more important as account size compounds. When looking at your portfolio, coordinate taxable and retirement holdings. Yes, this is absolutely where a financial planner can add value.

Tax-loss harvesting, distribution timing and capital gain management require regular monitoring so you don’t get an unpleasant surprise around this time every year.