The Hidden Risks in Your 'Safe' Portfolio

For investors in their 30s and 40s, simplicity is great, but so are rebalancing, diversifying, and adapting to changing conditions

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Do you know what your retirement portfolio is really doing?

A couple years ago, we bought a Kia Sportage.

Like other newer cars, its dashboard will show a coffee cup icon if the car’s robotics (somehow) detect that the driver is becoming drowsy or inattentive.

Unfortunately, your investment portfolio doesn’t have that kind of warning built in.

So if you invested in a 401(k) in 2015 and haven’t looked at it since, it may be time to grab a cup of coffee and see what your investments have been doing while you were sleeping.

If you're like a lot of mid-career investors, you may have put your retirement money into a target-date fund or created your own stock and bond portfolio.

Using the past 10 years as our baseline, you would probably have done OK by just letting your investments ride.

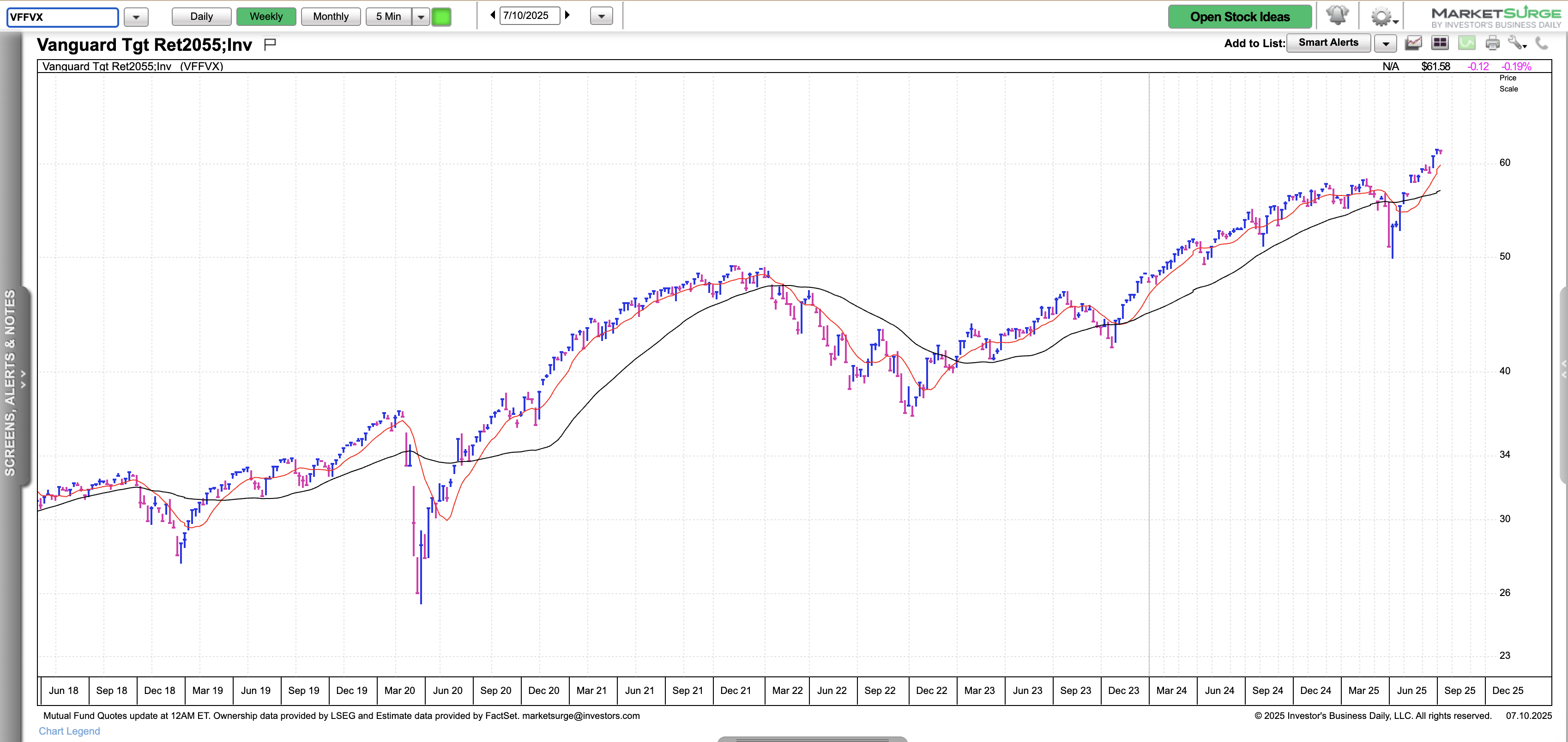

For example, say you began saving in your 401(k) 10 years ago at age 25, putting your money into the Vanguard Target Retirement 2055 Fund VFFVX.

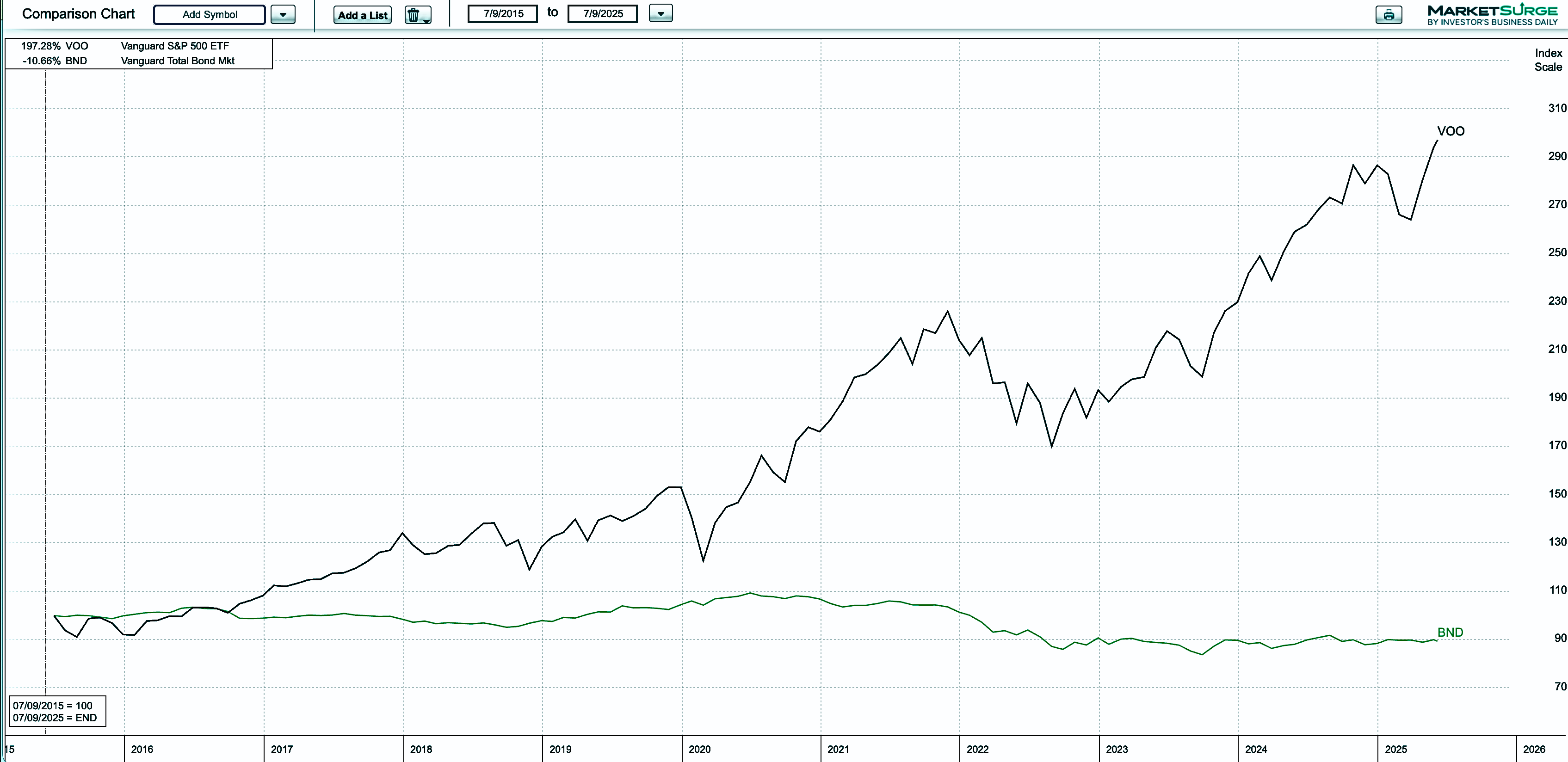

That target-date fund has returned 9.71% over the past decade, better than if you’d purchased a 50% stake in the Vanguard S&P 500 ETF VOO and 50% in the Vanguard Total Bond Market ETF BND and called it a day. In that case, you’d be up 7.675%.

Now, that 9.71% may not sound too exciting to someone who wants the promise of eye-popping overnight returns from penny stocks, but the idea behind that, and any other target-date fund, is to deliver steady growth while managing risk.

VFFVX is a "set it and forget it" fund designed for someone retiring around 2055. Its priorities include:

- Growth over decades: Not just high returns in bull markets

- Global diversification: U.S. and international exposure

- Risk reduction over time: Glidepath to more bonds near retirement

9.71% is excellent in this context, especially considering:

- It includes underperforming asset classes. Like international and emerging markets in recent years.

- It weathered inflation, Covid, the 2022 broad market downturn and regular bouts of market volatility

Is A Hands-Off Strategy Enough?

But in today’s economic environment—rising interest rates, global uncertainty, and persistent inflation—this hands-off strategy may not be enough.

According to Morningstar, more than 80% of workplace retirement plans default to target-date funds, and most investors never opt out.

While these funds are convenient, and as we just saw, do their job pretty well, they often mask unintended risks. Those include high exposure to U.S. large-cap stocks and core bonds, limited international diversification, and minimal protection against inflation.

Consider the classic 60/40 portfolio using VOO and BND that I mentioned above.

In a falling interest rate environment, that worked well.

So does it make sense to construct your own portfolio, with all the responsibilities of rebalancing and making sure your holdings match your time horizon, or turn to the set-and-forget ease of a target-date fund?

How Target-Date Funds Have Fared

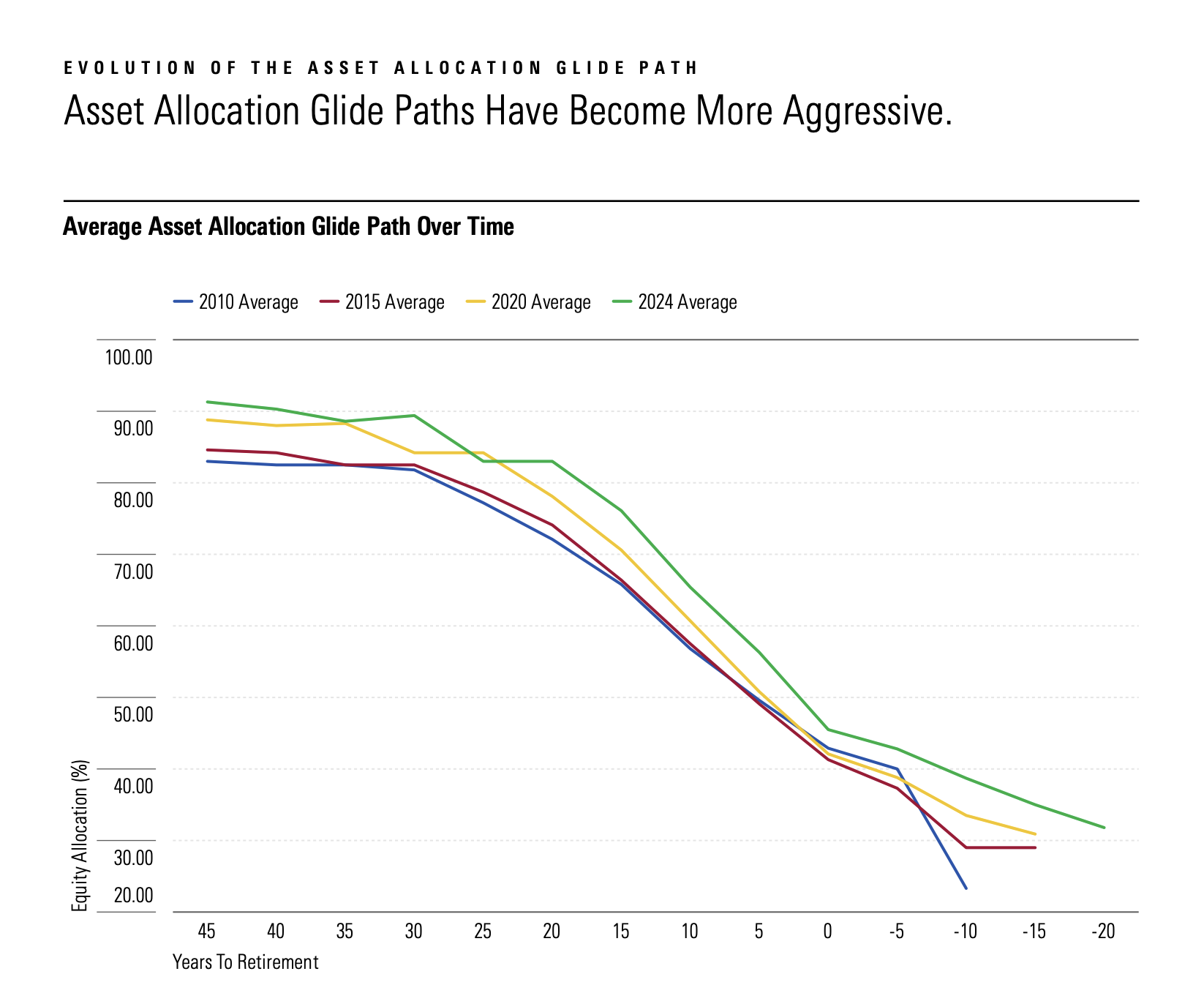

In its recent report, “2025 Target-Date Fund Landscape,” researcher Morningstar found that TDF returns, on the whole, have easily outpaced expectations from models commonly used around 2010.

According to Morningstar, that resulted in higher balances than models were predicting 15 years ago.

There’s a pretty simple explanation for this: Glidepaths have become more aggressive over the years, as you can see in the graph below.

TDFs are more equity-heavy in 2025 than in 2010. Morningstar cites three factors behind these allocations, which have the potential to boost return, but also add risk.

- Interest rates: Low interest rates for much of the 2010s and early 2020s dampened bond yields and made them less attractive relative to stocks, which tend to thrive in low-rate environments.

- Growth potential: Equities should provide greater growth potential over longer periods compared with bonds. Higher allocations are suitable for younger investors, who can take on more risk and benefit from longer periods of growth and the effects of compounding.

- Life expectancy: While life expectancy in the U.S. took a dip during the Covid pandemic, it has generally risen over time, meaning people are more at risk of outliving their assets. Equities should provide greater growth potential over longer periods compared with bonds.

What Should Mid-Career Investors Do?

I’m generally in favor of just taking the leap into investing, rather than giving in to analysis paralysis and keeping your money in cash.

Over the years, I’ve had many clients who came to my firm with expensive mutual funds and stuff that just didn’t make sense. One had a huge treasure trove of MetLife MET shares he’d inherited from his father. Another had not one, but two target date funds, neither of which was remotely pegged to his planned retirement year.

I also had many people approach me with almost nothing invested, and there was one woman who had nearly $2 million parked mostly in cash.

Guess who had the better return, even though it wasn’t perfect? Of course. It was the people who had taken on the stock market risk over the years.

Could their situations have been improved? Of course. And that’s exactly how I helped them.

So if you’re in a target-date fund, great. And if you choose the do-it-yourself method, that’s also good, as long as you don’t take too much risk (or too little) and be sure to rebalance at least once a year.

Tips for Allocating Mid-Career Portfolios

1. Add global diversification. Most U.S. investors are overweight domestic stocks. Consider adding the Vanguard Total International Stock Index VTIAX or DFA World ex-US Core Equity Portfolio DFWIX, or the equivalent ETFs, to broaden your exposure. Over the past decade, U.S. stocks have dominated, but mean reversion is real; both emerging market and non-U.S. developed market stocks are outperforming the S&P 500 this year.

2. Include inflation-sensitive assets. To reduce long-term purchasing power risk, consider allocating to TIPS through Vanguard Inflation-Protected Securities Fund VAIPX or real assets via PIMCO Commodity Real Return Strategy PCRAX.

3. Use valuation-aware rebalancing. Firms like GMO and Research Affiliates emphasize dynamically adjusting your allocation based on valuation, rather than sticking to a fixed ratio. As Research Affiliates founder Rob Arnott has said, “Even asset allocation ‘clairvoyance’ can lag” when valuations shift, implying that unchanging, static allocations fail to adapt to changing market risk and opportunity.

This reflects his broader point: without active adjustments for valuation and risk, holding a static 60/40 or similar mix can become a passive delegation that misses evolving market conditions. That’s when you need that coffee cup icon to help you wake up to what’s going on.

4. Stress-test your portfolio annually. Tools like Morningstar Portfolio Analyzer or Portfolio Visualizer, which have some limited functionality for free, can help you assess your exposure to interest rate risk, equity concentration, and inflation.

If you’re in your 40s or even early 50s, you still have plenty of time to make meaningful adjustments. Just be careful not to confuse simplicity with safety. A static allocation might feel comfortable, but in a market and economic landscape that’s constantly changing, comfort and inattention can be costly.