The Best Retirement Investments for a Market Downturn

Don't let your plans get derailed. Here's how to recession-proof your nest egg.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It's not fun to think about, but recessions happen. So do market downturns. (Crashes, not so much, even though that's the term people like to use if stocks fall suddenly.)

Panic Prevention

Market downturns are inevitable, but contrary to popular belief, it's not a foregone conclusion that they'll derail your retirement.

As a financial advisor, I saw plenty of new clients after the 2008 financial crisis. People had lost 50% or more of their portfolio value. Some were big mad, others were scared, others were just resigned to having less money than they'd planned for.

There were ways to stem the losses, but most people didn't know about them.

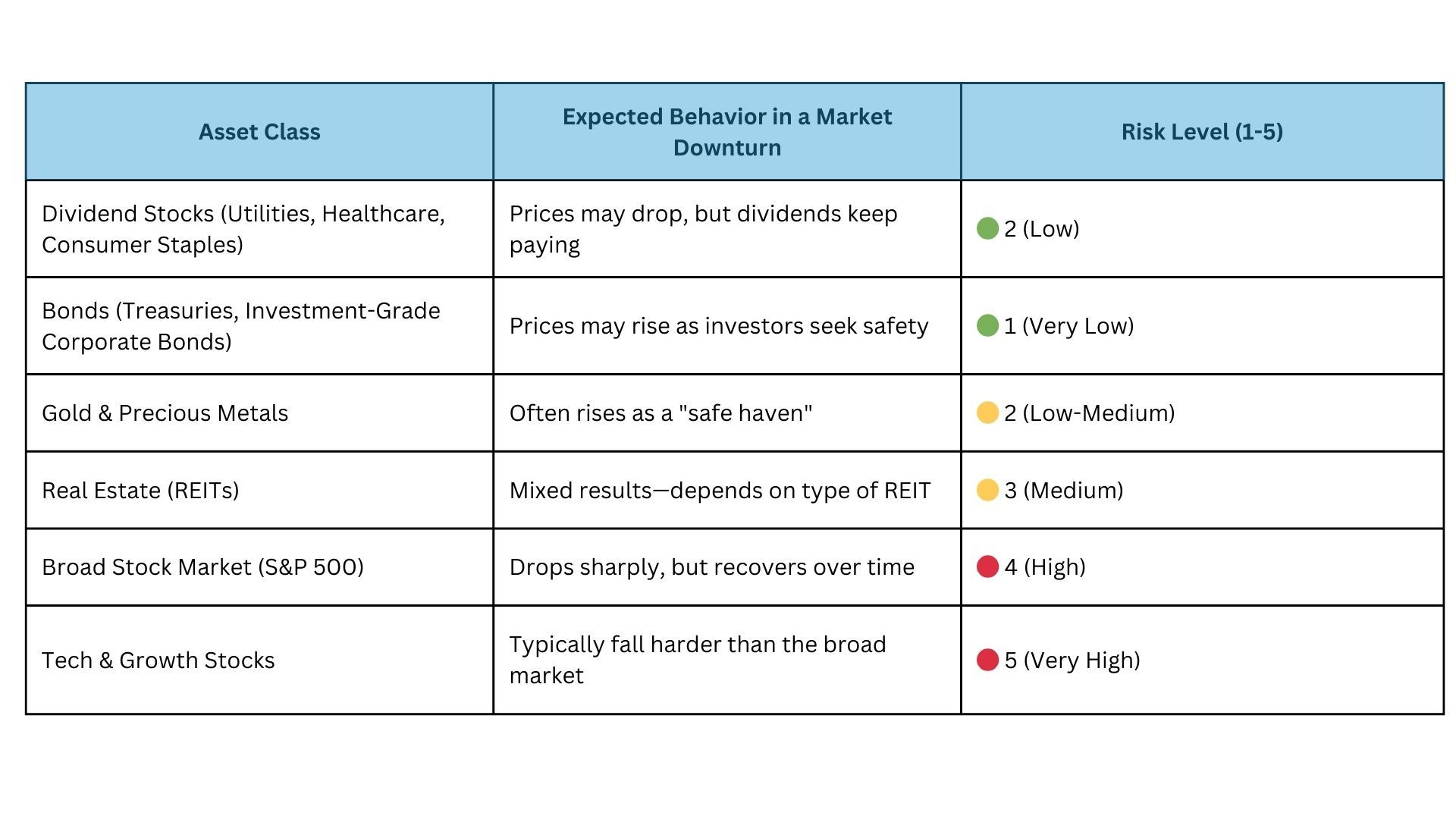

Wait for it .... The key is owning the right mix of recession-resistant assets —investments that generate steady income and hold up well when stocks take a dive.

Here's a glance at how different asset classes may perform in a downturn.

So what are some investments retirees and pre-retirees can include to mitigate effects of a downturn?

1. Defensive Stocks: Stability When the Market Drops

When recessions hit, you're not going to stop buying groceries and toothpaste, paying your electric bill and refilling your prescriptions. That’s why the tried-and-true defensives like consumer staples, utilities and healthcare typically outperform.

The Data: According to Morningstar, defensive ETFs focusing on low-volatility stocks generally show better risk-adjusted returns by smoothing out market fluctuations. These strategies often outperform during downturns but may lag in strong bull markets. For example, during the 2008 financial crisis, low-volatility ETFs declined less than the broader market.

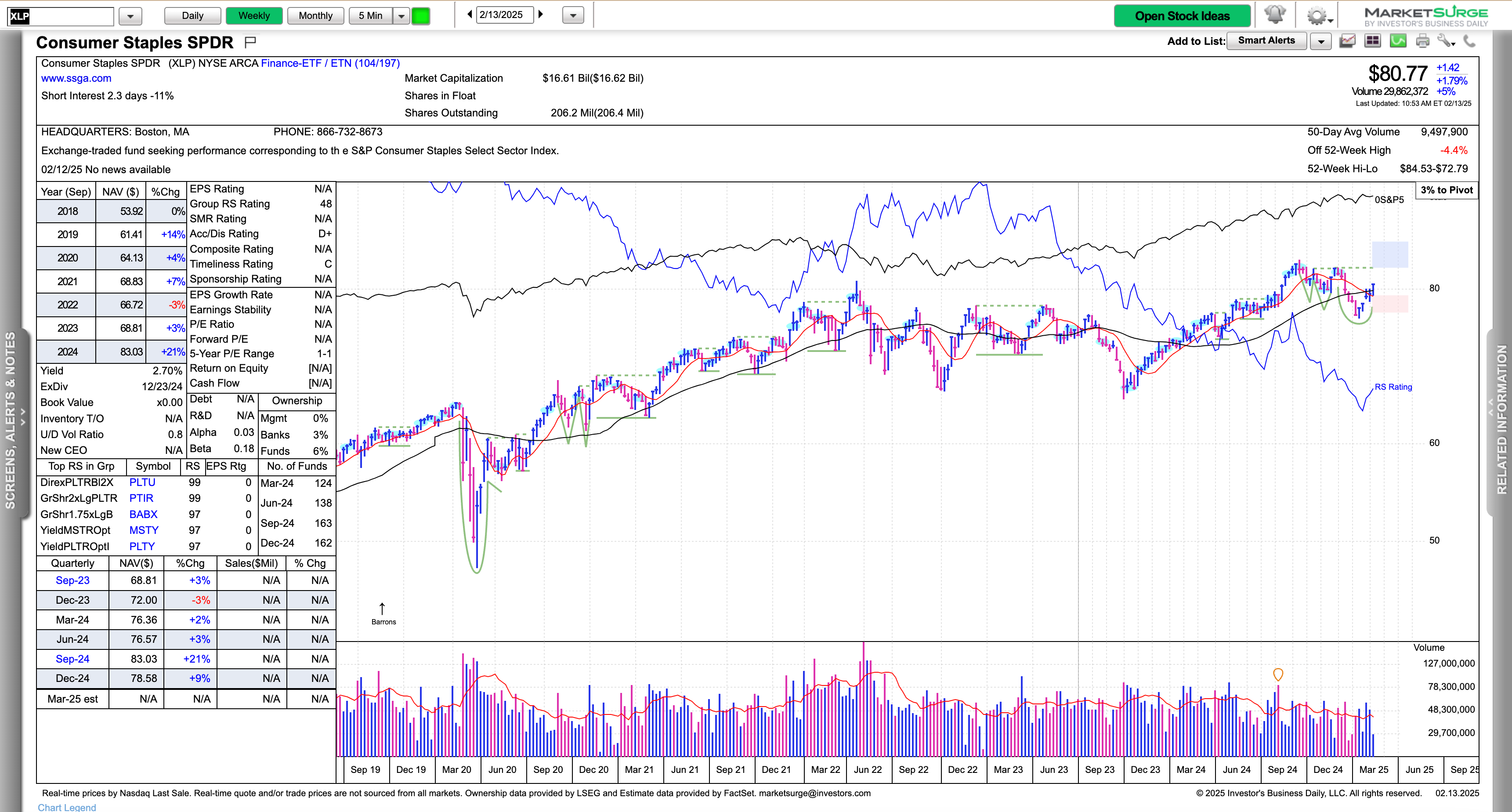

SPDR Consumer Staples ETF (XLP)

This ETF holds stocks of brands you know well. The largest components are household-name companies like Procter & Gamble PG, Coca-Cola KO, and Walmart WMT, firms that keep making money in good times and bad.

Since 2000, XLP has outperformed the S&P 500 in every major recession while providing steady dividend income. Its current yield is 2.62%.

Pro Tip: Consider keeping 15-25% of your stock allocation in defensive sectors to buffer against market downturns.

2. Bonds & Fixed Income: Reliable Cash Flow

Typically, although not always, bonds and stocks have an inverse correlation. However, even when bond prices decline, you'll still get a very predictable income stream and lower volatility compared to stocks.

The Data: The Federal Reserve reports that during past recessions, investment-grade corporate bonds and U.S. Treasury bonds maintained their value, good news for retirees who rely on portfolio income. Even in market crashes like 2008, bonds significantly outperformed stocks.

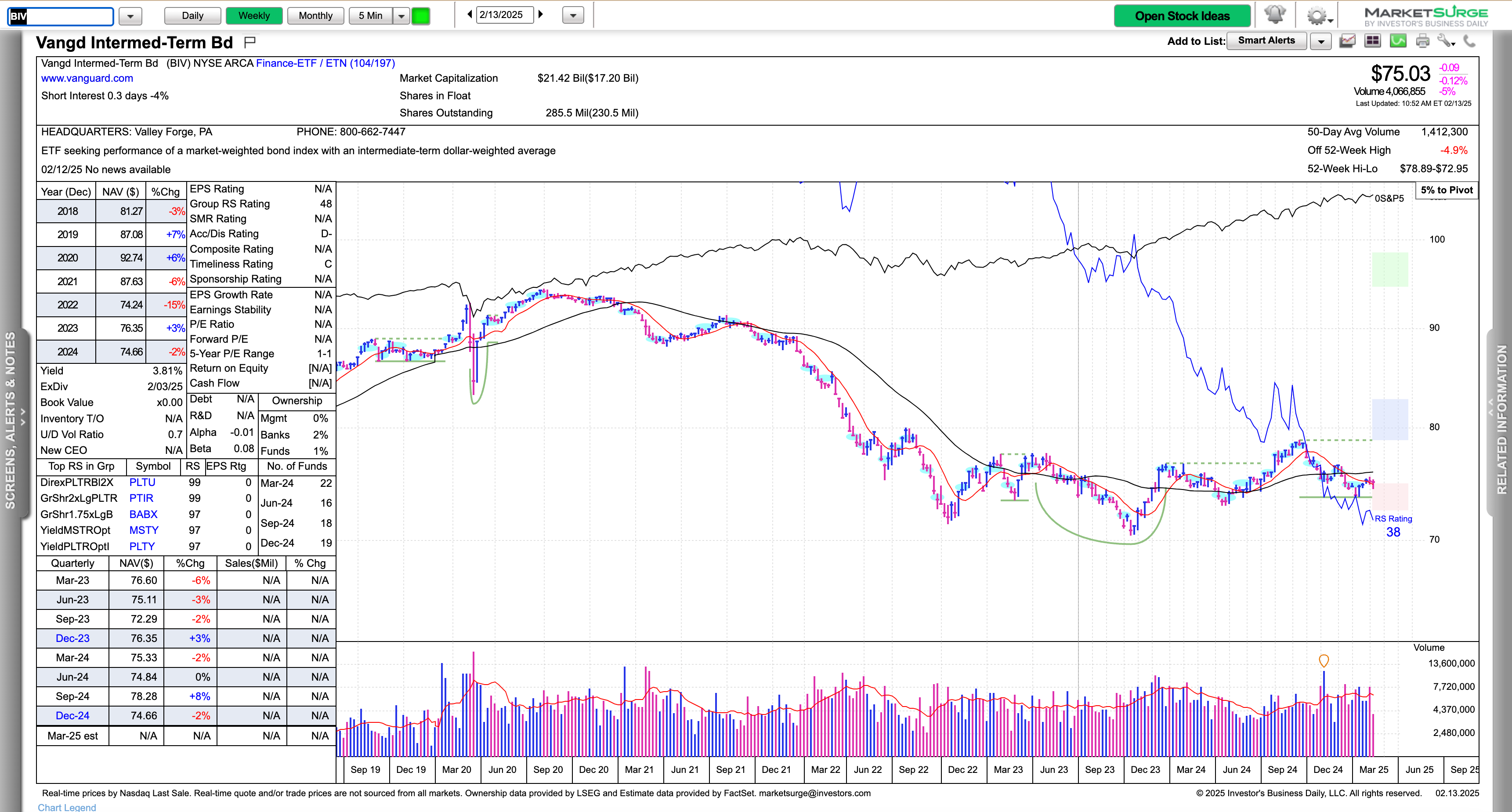

Vanguard Intermediate-Term Bond ETF (BIV)

BIV is a mix of high-quality corporate and U.S. government bonds, offering both safety and steady interest income. Over the past decade, it has delivered consistent, low-volatility returns even when equities struggled.

Its current yield is 3.74%.

Pro Tip: A balanced retirement portfolio should include 30% to 40% in fixed income, depending on risk tolerance, time horizon and income needs. (Yeah, I know: Bonds aren't exciting, especially for anyone who likes the thrill of fast profits from trading. Well, too bad. Mitigating risk and generating income become more important in retirement or even close to it.)

3. Alternative Assets: REITs

Real estate investment trusts (REITs) offer another way to generate steady income, often with higher yields than traditional bonds or dividend stocks. Fortunately, it's easy to buy publicly traded REITs or REIT ETFs.

The Data: According to NAREIT, REITs delivered an average annual return of 10.5% since 1972. That tracks with stock market returns but with higher income payouts. During past recessions, sectors like healthcare and residential REITs have remained resilient and profitable, as these sectors typically see steady income, versus sectors more sensitive to economic conditions.

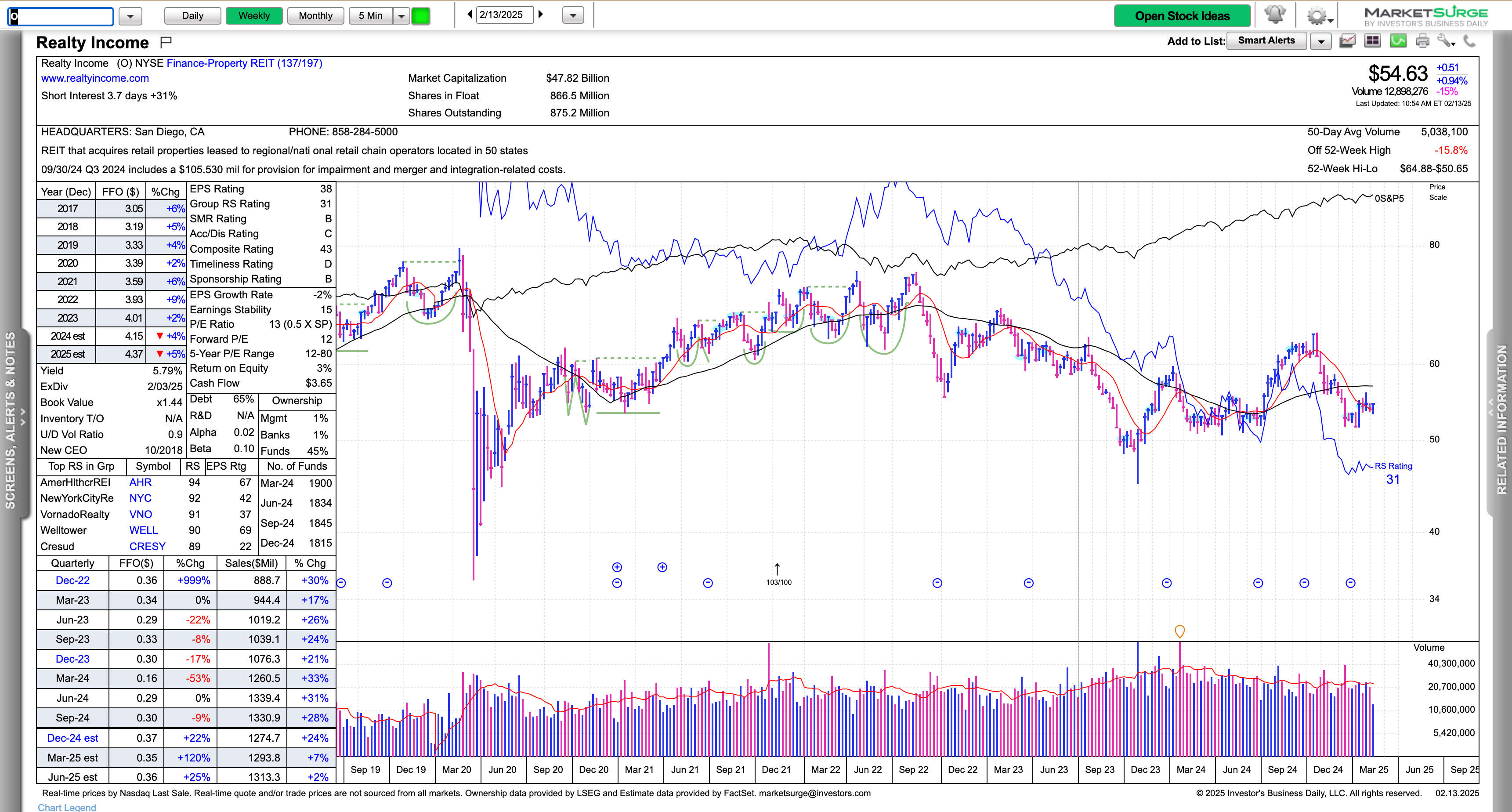

Realty Income (O)

Known as “The Monthly Dividend Company,” Realty Income O has paid and increased its dividends for over 25 years. The company invests in recession-resistant properties, such as pharmacies, grocery stores, and industrial warehouses, which continue generating rental income even in economic downturns.

Its current yield is 5.50%.

Pro Tip: Consider 5-15% of your retirement portfolio in REITs to diversify income sources beyond stocks and bonds. Even for investors years away from retirement, an allocation into REITs can lend stability along with a steady cash flow.