Target-Date Funds Get Lifetime-Income Makeover

Generating payouts as traditional pensions fade away

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Vanguard and TIAA are teaming up to help retirement savers generate lifetime income from target-date funds.

Before I jump into the details, a little background.

The 401(k) was never intended to be Americans’ default retirement vehicle. When it was introduced in 1978, it was designed to allow pre-tax salary deferrals on executive bonuses. In other words, to supplement income from existing defined benefit pension plans and Social Security.

Well, we know that’s no longer the case. Good luck finding defined benefit plans outside of government and unions.

Despite the ubiquitous nature of the 401(k) plan, managing rollovers and distributions is often a complex process.

The idea of the 401(k) is to turn savings into a predictable paycheck that lasts as long as you do. But that’s a tougher challenge than deciding between shares of Nvidia (NVDA) or Tesla (TSLA).

You're On Your Own

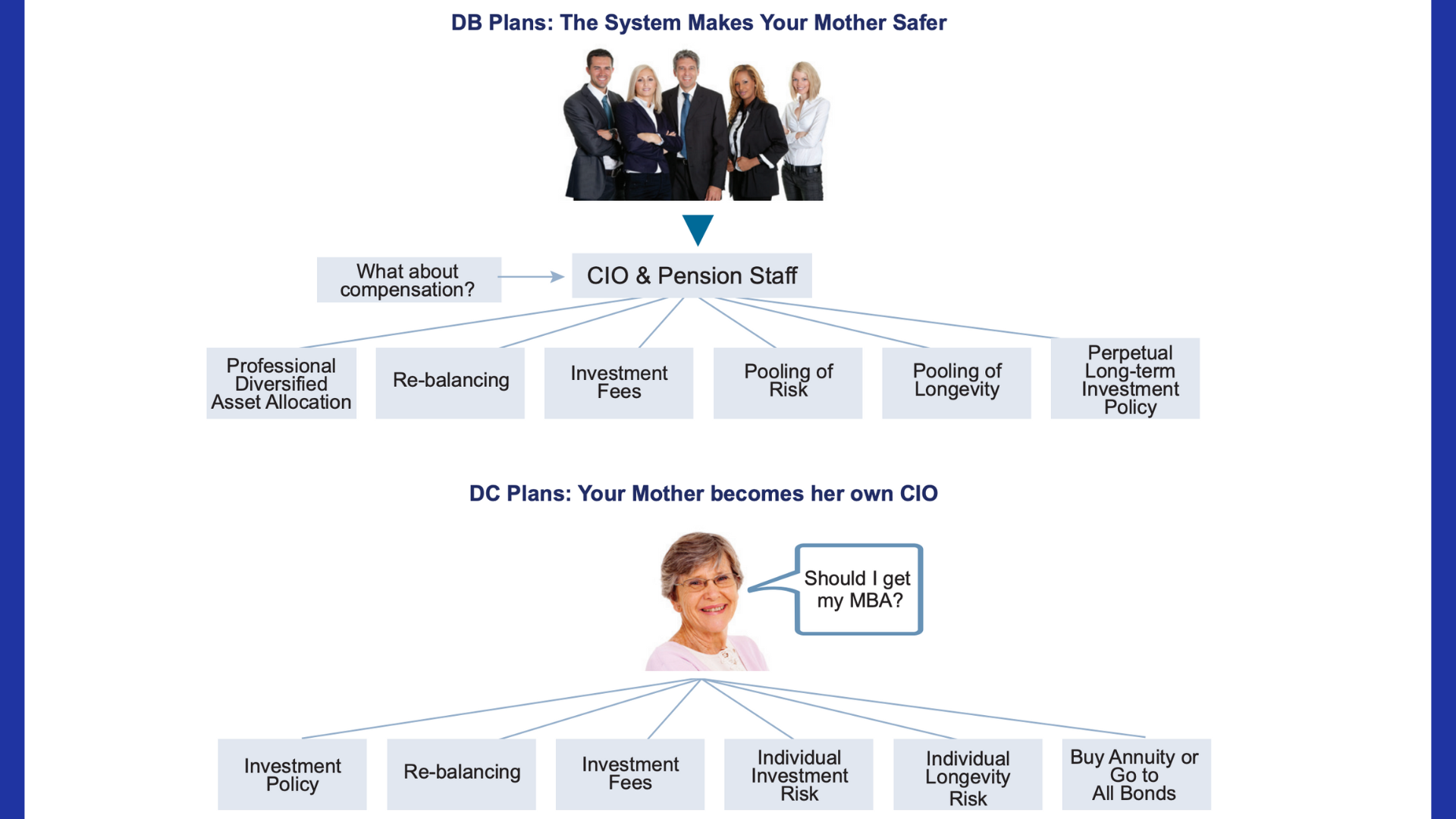

A 2021 report from the Center for Retirement Initiatives (CRI) at Georgetown University noted that traditional defined benefit (DB) plans are designed to provide a lifetime income for the retiree.

“In contrast, a defined contribution (DC) plan establishes an individual retirement savings account for the employee. Upon retirement, the employee often receives a lump sum payout of their account balance,” wrote Georgetown researchers.

“The key difference between a DB plan and a DC plan is that most DC plans today are not designed to generate or protect lifetime income. The retiree is left to manage the savings to make sure they will last through retirement. Unfortunately, one in five individuals spends most of their retirement account within the first five years after entering retirement, and only slightly more than one-half have enough money after five years of retirement to continue to maintain the same standard of living.”

Center for Retirement Initiatives: “Securing a Reliable Income in Retirement”

This image, from the report, is funny in a cringe way because it illustrates how much of the burden for managing retirement income the 401(k) has shifted to ordinary investors.

The process of rolling over a 401(k) is riddled with headaches. In an age when financial transactions are made with a couple of clicks, you frequently find yourself making phone calls and awaiting paper checks when you want to move a 401(k) from a previous employer’s custodian.

It’s almost 2026: Boomers hate these cumbersome processes. For Gen Z, it must seem like something from the Star Wars galaxy: far, far away.

Choose Your Own Adventure

But even before you get to that point, you’re responsible for allocating your portfolio all by yourself. It’s a safe bet that most retirement savers aren’t well versed on how to apportion various market capitalizations, sectors, and regions in the equity portion of their 401(k)s, or even how much to put in stocks versus bonds.

But wait, there’s more!

According to research from Nationwide and the American College of Financial Services, “Extending retirement by just five years increases the risk of running out of money by more than 300% according to The College’s analysis.”

Researchers added, “Both consumers and advisors must shift their mindset, prioritizing longevity risk and placing a stronger emphasis on guaranteed income strategies that can weather uncertainty.”

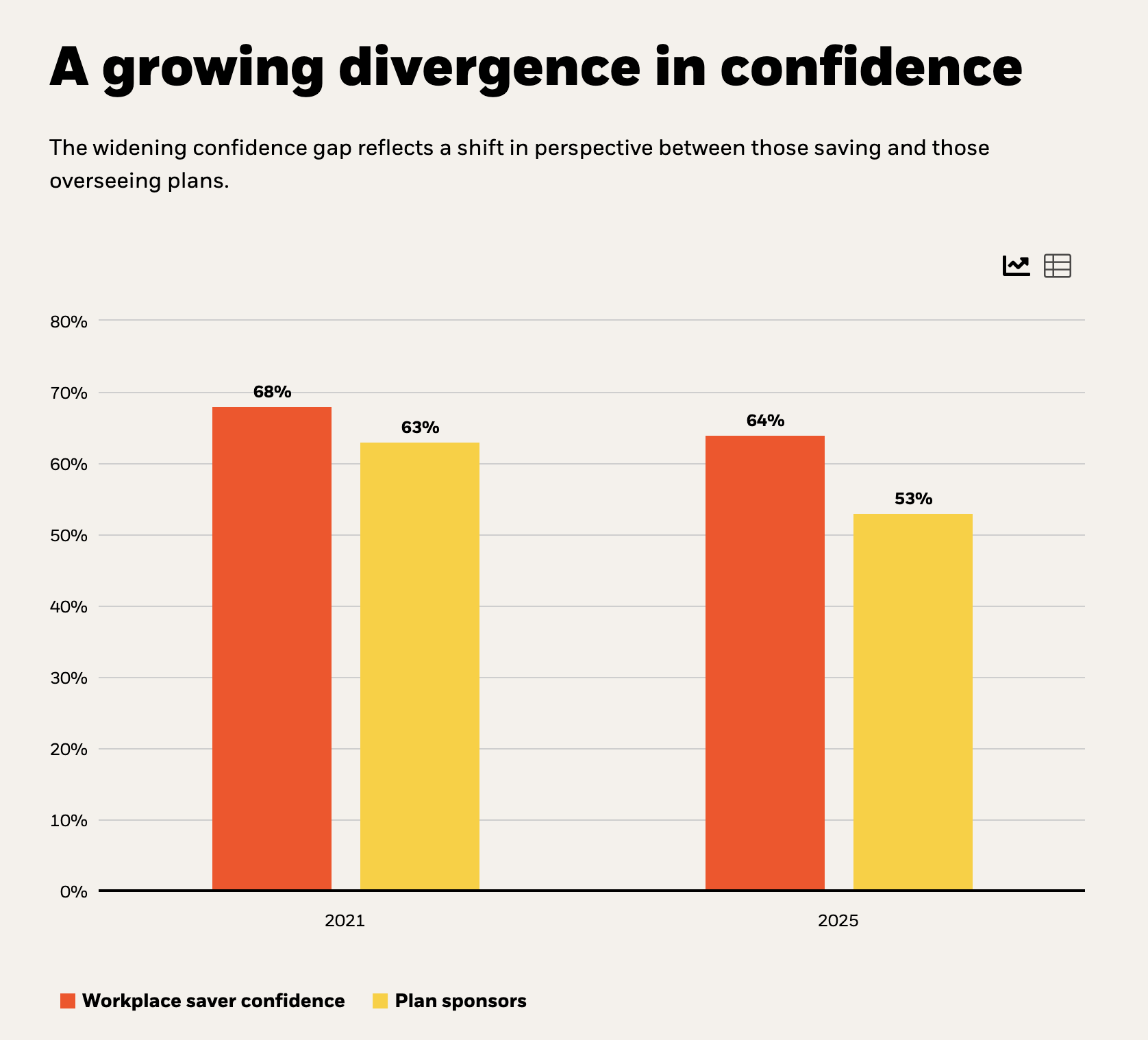

Running out of money is one of retirees’ biggest fears. This chart from BlackRock shows that 401(k) plan participants are less confident about retirement readiness in 2025 than they were in 2021.

Perhaps even more concerning, plan sponsors, who see what’s going on behind the scenes, are even less confident about participants’ probability of success. Their confidence, too, dropped in the past four years.

According to a Vanguard news release, the company is “developing a new target-date collective investment trust (CIT) series, Target Retirement Lifetime Income Trusts, that incorporates the TIAA Secure Income Account as the lifetime income annuity option.”

In other words, the partnership will allow 401(k) savers to turn their savings into guaranteed retirement income using TIAA’s expertise in annuities. The companies plan to unveil more details throughout 2026.

The Disappearing Pension

But they aren’t the first fund sponsors to the annuity party: BlackRock’s LifePath Paycheck and State Street’s IncomeWise programs have similar aims.

“The disappearance of pensions left a massive gap in retirement security. This collaboration fills that gap by embedding lifetime income right where 100 million Americans are already saving,” said Colbert Narcisse, chief product officer and head of insurance solutions new markets at TIAA, in a statement.

It’s true that plenty of investors have it drilled into their brains that annuities are complex and expensive. It’s also true that many, shall we say “unethical” insurance salespeople put unsuspecting clients into products they don’t need.

I’ve seen it plenty of times. Somebody got a nice commission, and the client paid some unnecessary fees and locked up their money. They could have gotten the same growth (or usually better) in an IRA carefully invested.

With the big plan sponsors and fund custodians aware of the problem, savers may see some changes soon.

“Within the next decade, it will seem as strange for a retirement plan to lack guaranteed income options as it would today for a plan to operate without target-date funds,” Narcisse said.