Supply, Demand, Nvidia and Taxes

Navigating Stock Market Dynamics and how a bad investment can save you money on taxes.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

This is the tenth of ten articles in the Filthy Rich Animal Investing Basics Series.

If you like what you see, are not yet subscribed, or want to share with a friend, please visit this link to join us. It's free!

Next week, we'll begin providing actionable advice and weekly educational content.

And that's when the real fun will start!

So you have an investment plan that’s a little more sophisticated than “make a lot of money.” (That’s not a plan, BTW.)

Your investing plan is tailored to your financial goals and your time horizon. Yes, you’ve heard that before, but as you approach retirement, it becomes more important than when you were 25 or 30.

Of course, your plan should include risk management, which is where market pricing comes into play.

You almost certainly know how to execute a buy or sell order with your online brokerage, but there are points to consider, depending on what types of securities you’re buying.

Quick refresher: The stock market operates on the principles of supply and demand, much like any other marketplace. For every buyer, there must be a seller. If more investors want a stock (demand) than are willing to sell it (supply), the buyers need to raise their prices in order to entice sellers to part with their shares.

Conversely, if more investors wish to sell a stock than buy it, the price falls. Again, in this case, sellers need to lower their price in order to find more buyers.

For example, let’s say that your local auto dealer has a car for sale that costs $20,000. If there’s a buyer who thinks $20,000 is fair and has enough cash, the dealer will be able to sell the car.

What if there’s no demand for that car? Maybe the economy is weak and nobody is buying cars. Or maybe I can buy a better car for $19,000 from a different dealer.

What will the dealer do? That’s right! They’ll put it on sale.

The stock market works the same way. Company share prices increase when demand outstrips supply. You can see that on the stock’s charts as shares get bid up.

For instance, if a company reports strong earnings, more investors may want to buy its stock, exhausting the number of people willing to sell at lower prices and driving up the price.

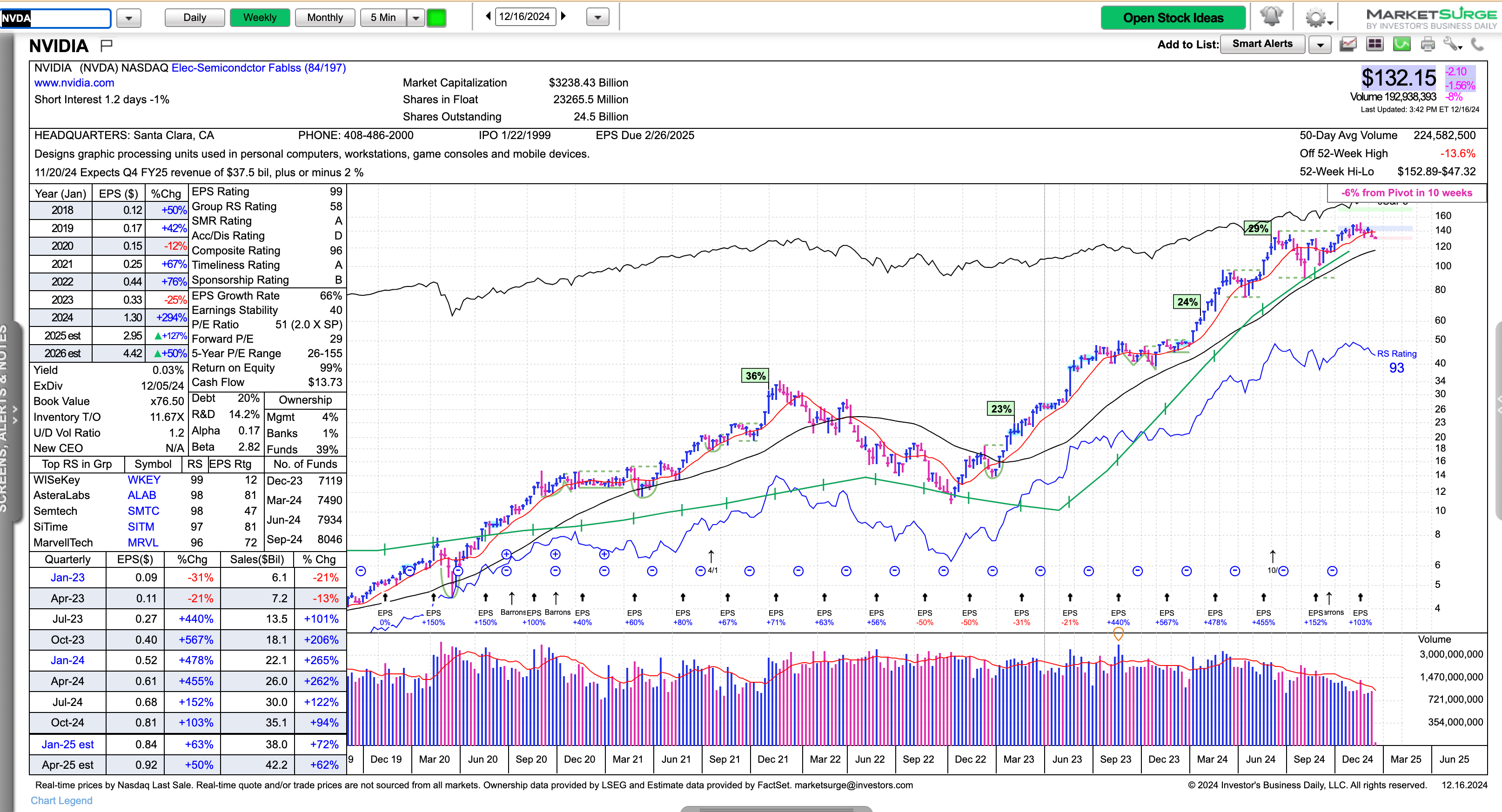

Here’s a chart of Nvidia (NVDA) through December 2024. Investors couldn't get enough of it.

At the time, Nvidia’s three-year earnings growth rate was 94%, something that would attract investors even without the red-hot AI theme.

Trading Volume Shows Buying, Selling

As investors nabbed more shares, the daily trading volume increased; that contributed to the stock’s increase.

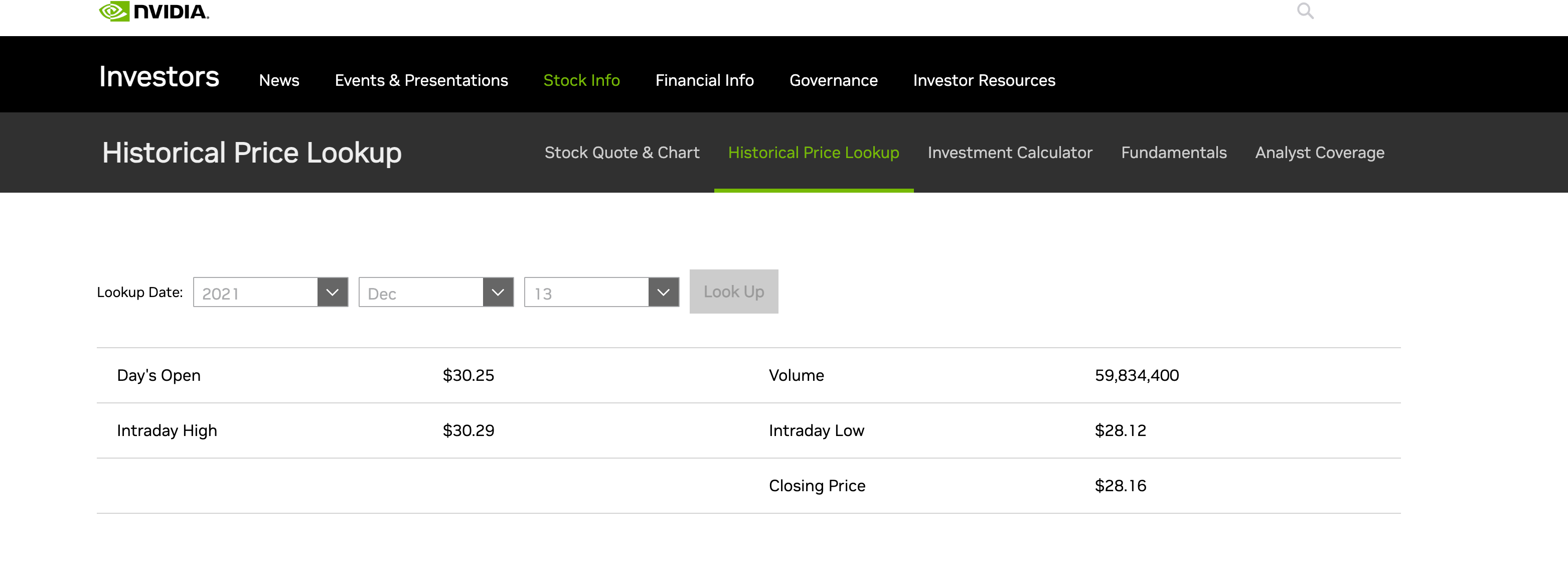

For reference, on December 13, 2021, daily trading volume was 59.8 million shares.

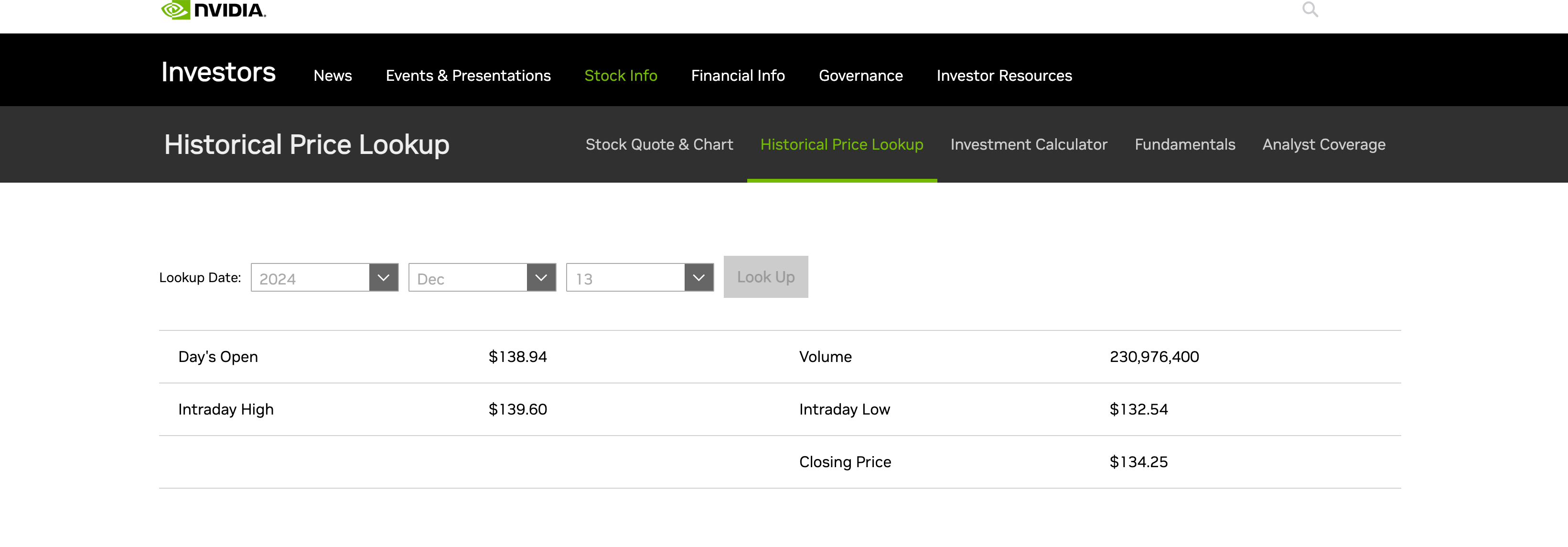

By 2024, that had skyrocketed to nearly 231 million.

Now, we know the story that drove Nvidia higher, and at the time of this writing, investors continue to believe the case for AI growth is compelling.

On the other hand, if a company faces negative news, investors might rush to sell, increasing supply and lowering the price.

That can work industry-wide, as well.

In December 2024, health insurers as a group were pummeled. The selloff wasn’t just limited to UnitedHealth Group (UNH); the iShares U.S. Healthcare Providers ETF (IHF), made up of large-cap insurers, was down more than 12% that month.

On this chart, you can see IHF trading volume spike throughout December while the price cratered. That means investors were unloading shares, causing the price to drop.

Tax-Loss Harvesting

Investors look at a falling stock with dismay; I get that.

But there’s often a silver lining: Tax-loss harvesting. This means selling investments at a loss to offset capital gains with the idea of reducing taxable income.

Just to follow up on the examples above, say you owned the health insurers’ ETF, and had bought it close to the all-time high around 59 (hey, Earny has done this more than once! It happens). You could sell that to partially offset some of your gains in Nvidia.

It's a strategy used by all of the best investors and it works in a taxable account; in a qualified account, such as an IRA or 401(k), this strategy doesn’t matter, because you're not paying taxes on the gains of any individual holding.

In retirement, taxes can be a major expense, so It’s important to understand how Uncle Sam gets his cut.

In the U.S., investment income, such as dividends or interest, are taxed differently from capital gains.

- Investment Income: Taxed at ordinary income tax rates, which vary based on your total taxable income.

- Capital Gains:

- Short-Term: Gains from investments you’ve owned for a year or less are taxed at your ordinary income rates.

- Long-Term: Gains from investments owned held for a year or longer are taxed at lower rates, typically 0%, 15%, or 20%, depending on your income, and subject to change based on IRS rules.

To optimize your after-tax returns, tax-loss harvesting can be a useful strategy.

However, be mindful of the "wash-sale" rule, which disallows the deduction if you repurchase the same or a substantially identical security within 30 days.

Understanding the influence of supply and demand on stock prices, and the tax implications of your trades is crucial to effectively manage your retirement portfolio.

When you’re retired and no longer collecting a paycheck from your job, navigating the stock market and taxes becomes even more important than it may have been a few short years ago.