Start Strong: Why Early 401(k) Investing Pays Off

Small contributions today, big gains tomorrow

You've reached your free article limit

You've read 0 of 1 free Pro articles.

“Compound interest is the eighth wonder of the world. He who understands it, earns it... he who doesn't... pays it.”

Attributed to Albert Einstein

There’s no definitive proof that Albert Einstein ever said or wrote the words above, but it’s still pretty smart advice: Investing early in a 401(k) is one of the smartest things you can do for your future self.

Even if you’re not making much money early in your career, and many people don’t, small contributions add up over time. That’s where the magic of compounding comes in.

Why Starting Now Makes a Huge Difference

When you stash away money - even a small amount - in your 20s or 30s, you’re giving your funds plenty of time to grow exponentially.

This approach, known as dollar-cost averaging, also has the advantage of allowing you to buy stocks at low prices, and benefit from their subsequent growth.

Academic studies have shown that consistent contributions to your employer-sponsored plan can benefit you over various market cycles, even though some years will inevitably underperform.

“Since investments are made over time at various prices per share, the approach reduces the sensitivity of your portfolio’s return to a single trade date, potentially making it easier for you to ride out the market’s ups and downs … During periods of market volatility, it may also help you feel less compelled to alter your underlying strategy for achieving your long-term goals.”

Morgan Stanley

Keep It Simple with Your Portfolio

New investors don’t need complexity. Here are some ideas for starting out.

- Target‑date fund, matched to your planned retirement year. For example, if you’re 30, you might choose a fund matched to a retirement in 2055 or 2060. Yes, that seems like an impossibly long way away, but that day will arrive. You’d rather be prepared than not.

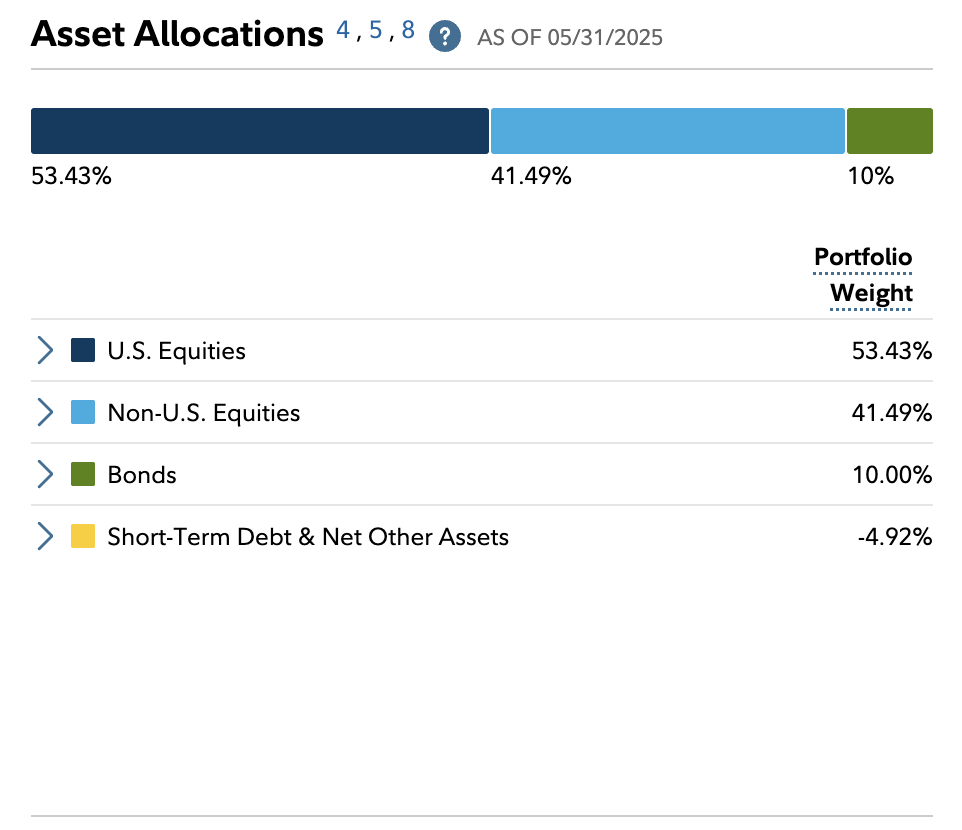

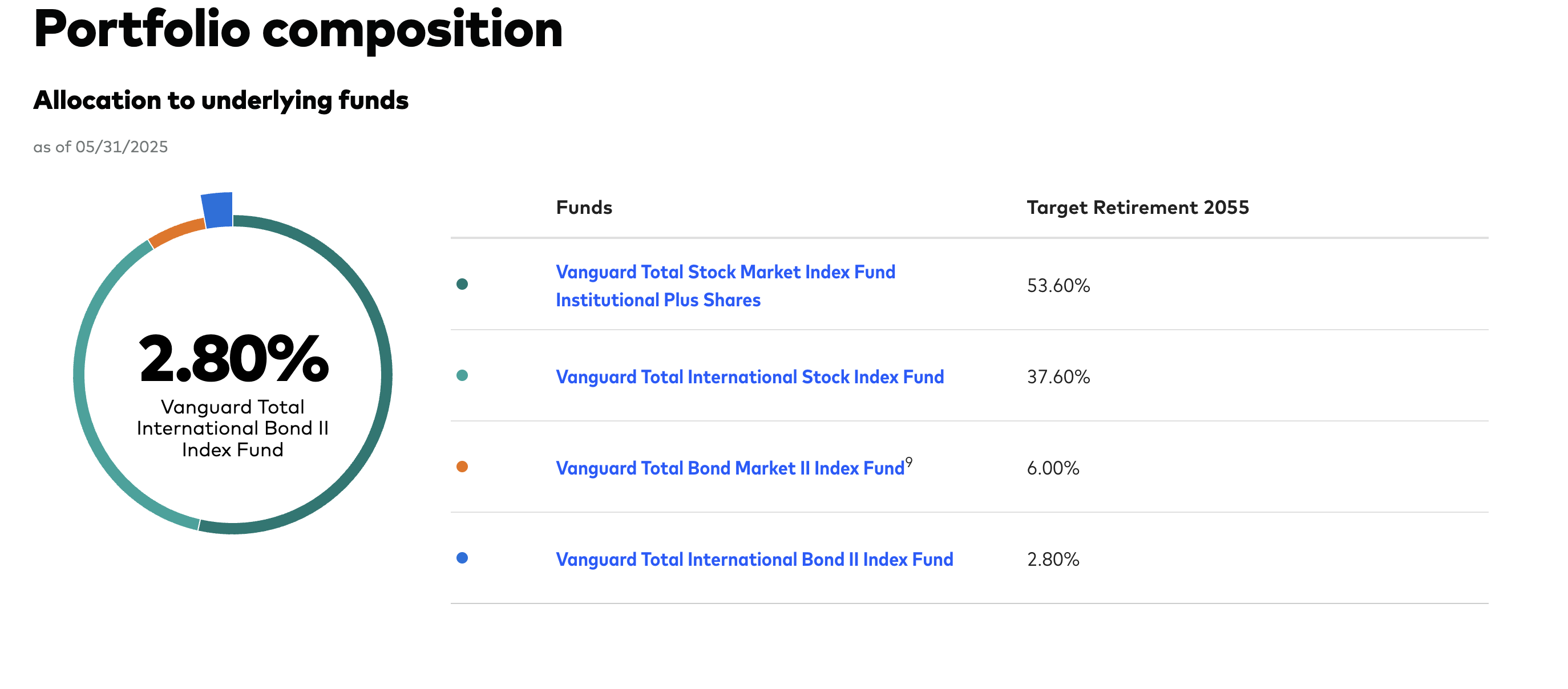

Target-date funds you’ll find in many employer plans include the Vanguard Target Retirement 2055 Fund VFFVX and the Fidelity Freedom 2055 Fund FDEEX.

Here’s a look at the composition of these portfolios. You can see they are heavily tilted toward equities, as you have plenty of runway at this point to take more risk.

- Build your own portfolio: In this case, you’d keep the same tilt toward equities, but instead of a pre-packaged fund, you can create your own mix.

Keep in mind: If you use a roboadvisory service, available through many 401(k) plans, you won’t have to rebalance. However, if you’re monitoring your own investments, you’ll have to check your allocation levels on occasion to be sure they’re aligned with your time horizon.

Here is a sample allocation, using a choice of funds, that young investors might consider for a long-term retirement account.

Total Portfolio Allocation: 100%

Equities: 90%

U.S. Stocks (60%)

- Vanguard Total Stock Market ETF VTI: 30%

- Fidelity Total Market Index Fund FSKAX: 15%

- Schwab Total Stock Market Index Fund SWTSX: 15%

International Stocks (30%)

- Vanguard Total International Stock ETF VXUS: 15%

- Fidelity Total International Index Fund FTIHX: 7.5%

- Schwab International Index Fund SWISX: 7.5%

Bonds: 10%

- Vanguard Total Bond Market ETF BND: 3.5%

- Fidelity U.S. Bond Index Fund FXNAX: 3.5%

- Schwab U.S. Aggregate Bond Index Fund SWAGX: 3%

A portfolio using these funds, or similar ones, would offer you built-in diversification with minimal hassle.

Resist Market Timing

Shuffling around your portfolio because of the headlines usually backfires.

People get scared because of the news (which is always bad, in case you hadn’t noticed) which generally results in a lower return than you would have if you’d just left your investments alone.

“Far more money has been lost by investors preparing for corrections or trying to anticipate corrections than has been lost in the corrections themselves.”

Peter Lynch, former manager of the Fidelity Magellan Fund

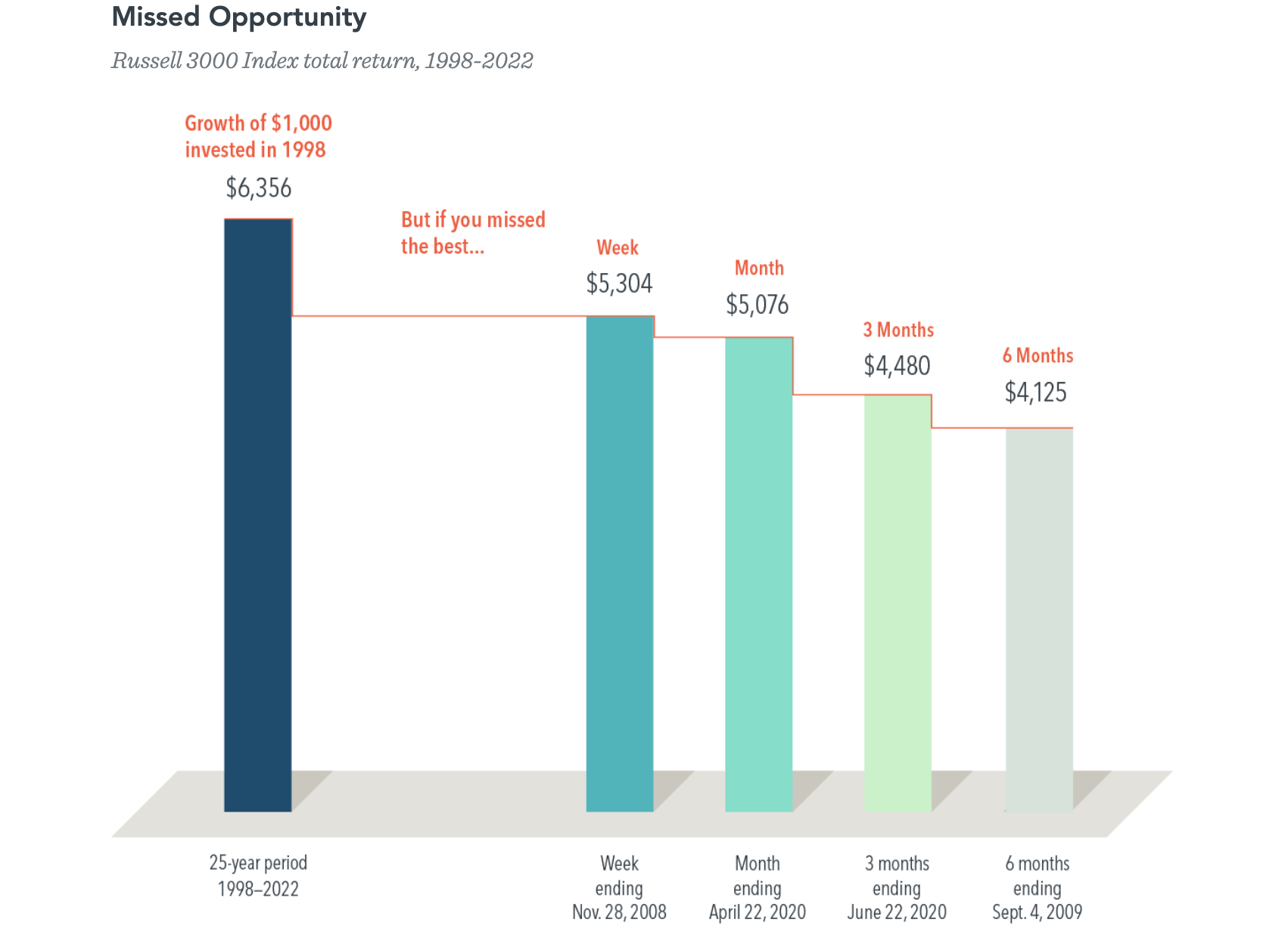

Here’s a graphic from Dimensional Fund Advisors that illustrates the perils of missing out on the market’s best days. It shows what would have happened if an investor had put $1,000 into the Russell 3000 index in 1998.

If that investor had left the money there through the end of 2022, that $1,000 would have grown to $6,356. But that number would have been less if the investor had missed the times of best growth in the market over those years.

In my experience as a financial advisor, people usually make big portfolio changes out of fear, not greed. I can’t think of a time when that worked out well.

Set Yourself Up for Long-Term Success

Here’s what to remember as you get started with your 401(k).

- Start early and contribute consistently, even if the amount feels small.

- Keep your portfolio simple with target-date funds or broad index funds.

- Avoid trying to time the market and stay focused on your long-term goals.

Thanks for reading and have a great weekend!