Retirement Investors Get Surprise 401(k) Update in Reported Trump Order

New retirement investment options offer more upside, but there's a cost.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Private equity and private credit used to be off-limits for everyday retirement investors.

These instruments, which represent debt and equity financing outside of the public markets, have historically been limited to institutions such as pension funds, university endowments, insurance companies, hedge funds or qualified individuals with at least $5 million, and usually much more.

But that’s changing.

Traditional fund managers, those that manage large 401(k) plans, are scurrying to make these investments available to retirement savers.

They're getting an assist from the Trump administration.

According to The Wall Street Journal, Trump is expected to sign an executive order soon that would bring private-market investments to retirement plans, like 401(k)s.

The Appeal of Private Markets

Advocates claim private assets can outperform a mix of stocks and bonds.

For example, BlackRock forecasts that target-date funds with private investments could return an extra 0.5% per year, on average, before fees.

That may sound small, but compounded over four decades, a reasonable time span for a retirement saver, that would generate a 401(k) balance 15% higher than a similar target-date fund without private investments, according to BlackRock.

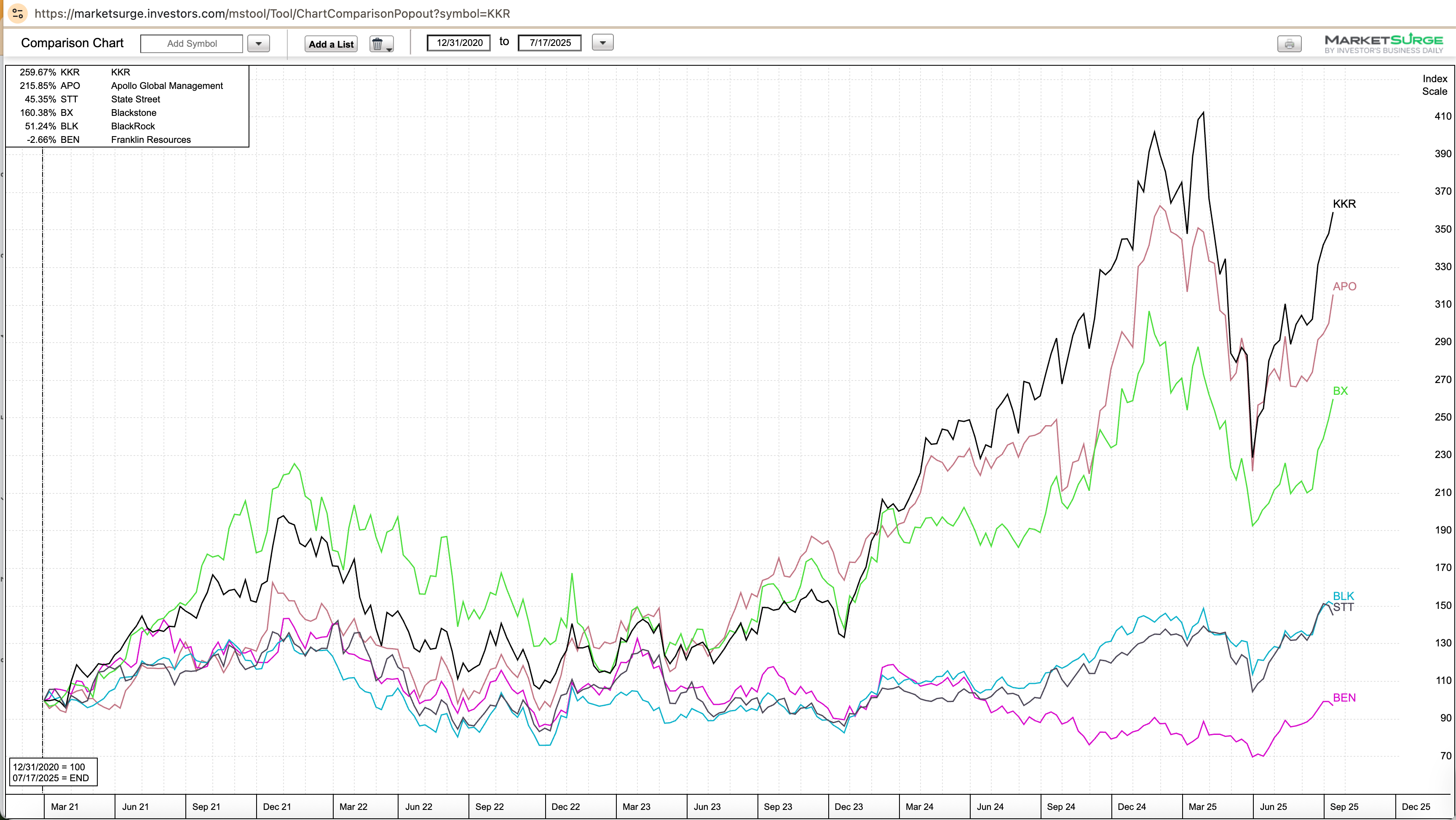

As a way of understanding the potential for private markets to outperform, this chart compares the returns of private equity firms KKR, Apollo and Blackstone with traditional asset managers State Street, Franklin Templeton and BlackRock.

The three private equity firms are at the top of the chart, showing higher returns over the past five years.

The higher returns sound great, of course.

But you do remember the risk-and-return tradeoff, right?

Right?

I’ll get to the risk part in a minute. It can’t be overlooked, sorry to say.

What’s Behind the Move?

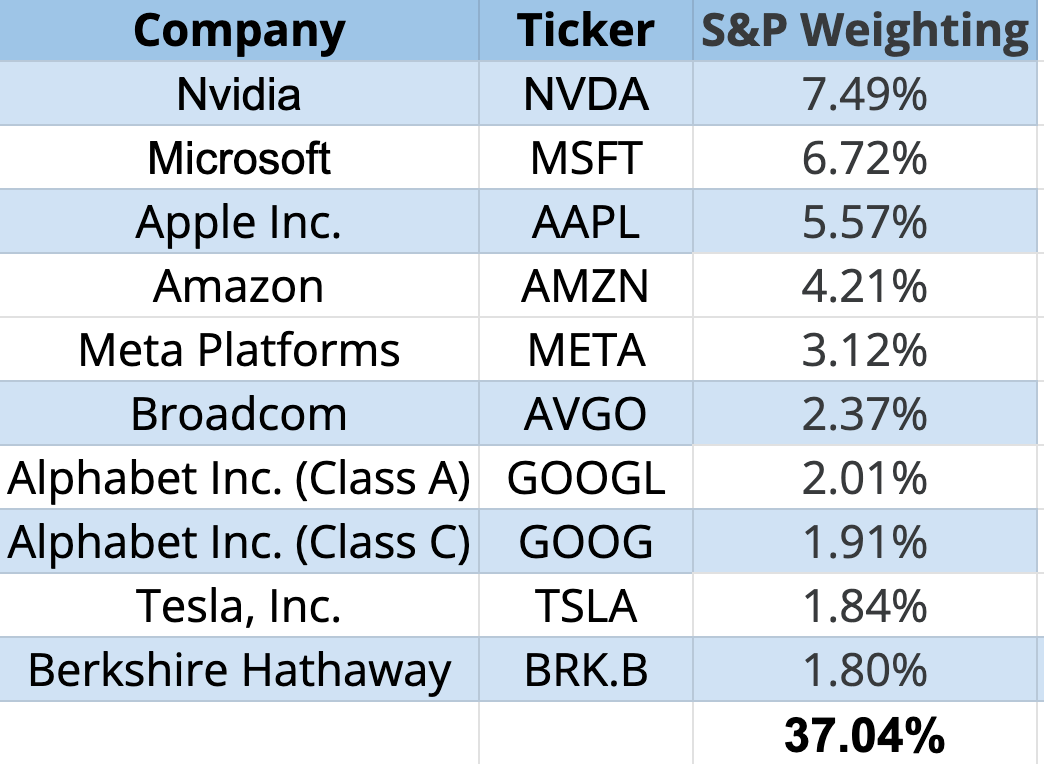

One major factor contributing to the increased popularity of private markets is a shrinking universe of stocks.

U.S. investors are already familiar with the dominance of a few big techs in the S&P 500, with the most heavily weighted S&P stocks accounting for 37% of index weighting.

There are currently around 4,300 stocks that are publicly traded on U.S.-listed exchanges like the New York Stock Exchange. This number has significantly declined from a peak of over 8,000 in the mid-1990s.

This means fund managers have fewer places to get an outperformance edge over other investments. To remedy this, they’re turning to private markets.

But it shouldn’t be forgotten: These managers can charge higher fees for the more active management in these private funds.

Some private market funds charge more than 1.5%, plus a cut of the profits.

That’s another powerful incentive

Rolling Out New Target-Date Funds

Already, some of the largest asset managers, like Blackstone, Apollo and KKR, are partnering with firms like State Street, Capital Group and Franklin Templeton to create retirement investment products that include private markets.

Vanguard, long held up as the paragon of low-cost, investor-first strategies, is also getting into the game.

According to The Wall Street Journal, “A new fund it is developing with Blackstone and Wellington Management will offer a mix of public and private assets.”

The Catch

In addition to investors paying higher fees for these products, lack of liquidity is often an issue, with money locked up for as much as a decade. Of course, that’s not the case with an ETF, which you might find in a 401(k), but it’s something for investors to be aware of.

These funds are also more complex than a basic index fund or even an actively managed stock or bond fund. They’re also less transparent, are more lightly regulated and the pricing mechanisms can be difficult to understand.

Understand What You’re Buying

Investors often run into a trap when trying to be too sophisticated.

I can’t tell you how many times I’ve met with a new client who’s been sold some kind of illiquid, private market fund they don’t understand, and can’t explain why they own it.

Retirement portfolio construction isn’t all that difficult. Understand the role of alternative assets. It’s OK to diversify into alternatives if you have a good reason for them being there, and are aware there may be higher fees and less transparency.

Ultimately, the goal of your retirement portfolio is to generate the income you’ll need after you stop working, not to make you sound cool for owning private equity.