Retirement Investors Are Getting It Wrong: Here’s a Smarter Way to Do It

Flip your strategy for a better retirement outcome

You've reached your free article limit

You've read 0 of 1 free Pro articles.

If you're saving for retirement or are already retired, you've probably heard traditional advice: Invest heavily in stocks when you're young, then gradually shift into bonds as you age.

It’s good advice, overall, and most target-date funds follow this glidepath.

Research from Dimensional Fund Advisors (DFA), along with some not-so-common wisdom from retirement experts like Bill Bengen, inventor of the well-known 4% rule, and authors Wade Pfau and Michael Kitces, shows that a more flexible, income-focused approach may help retirees spend more confidently and also avoid running out of money.

A retirement plan that balances stable income sources with strategic equity exposure, including increasing stocks slightly after retirement, can help you enjoy more income with less risk of financial shortfall.

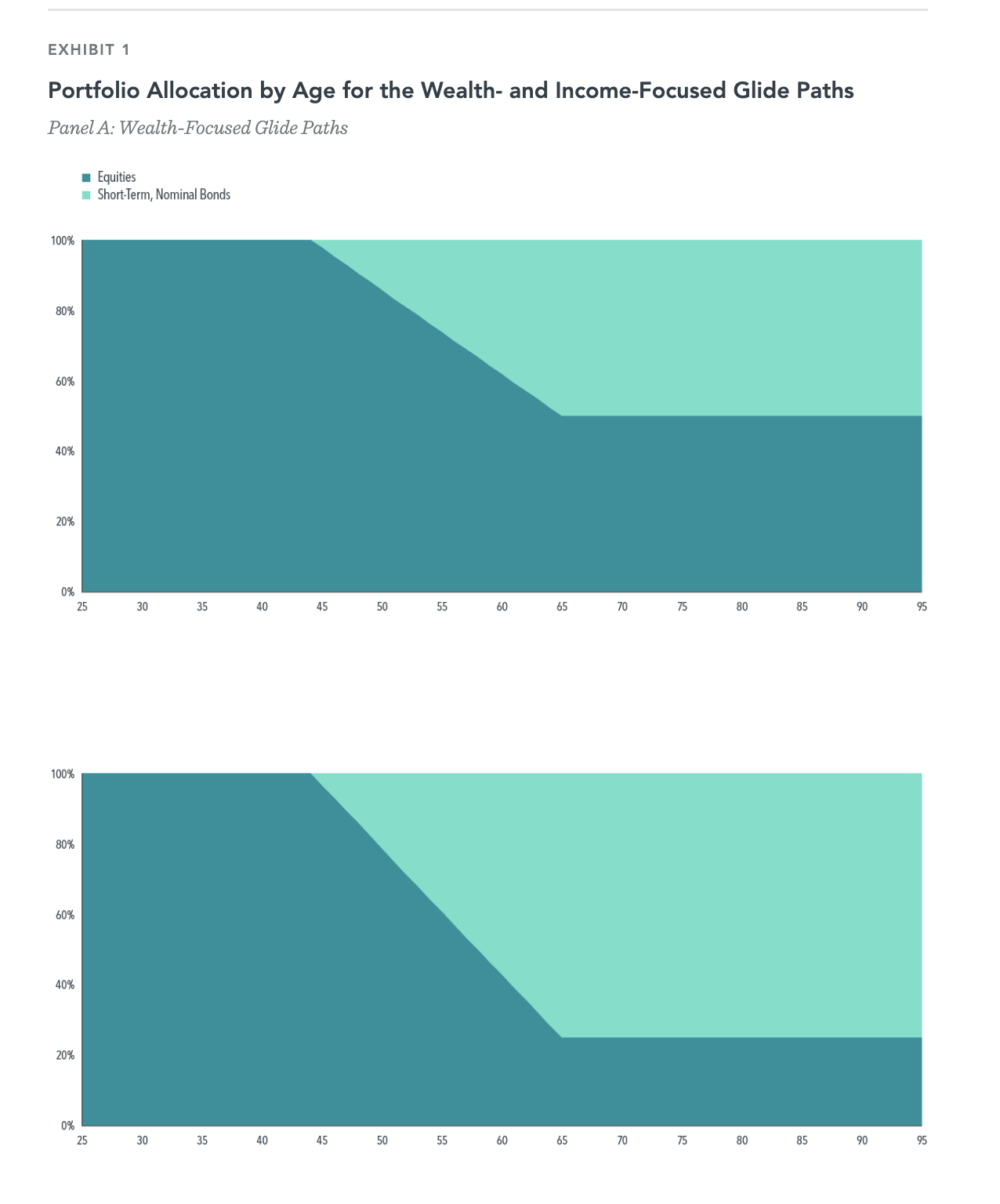

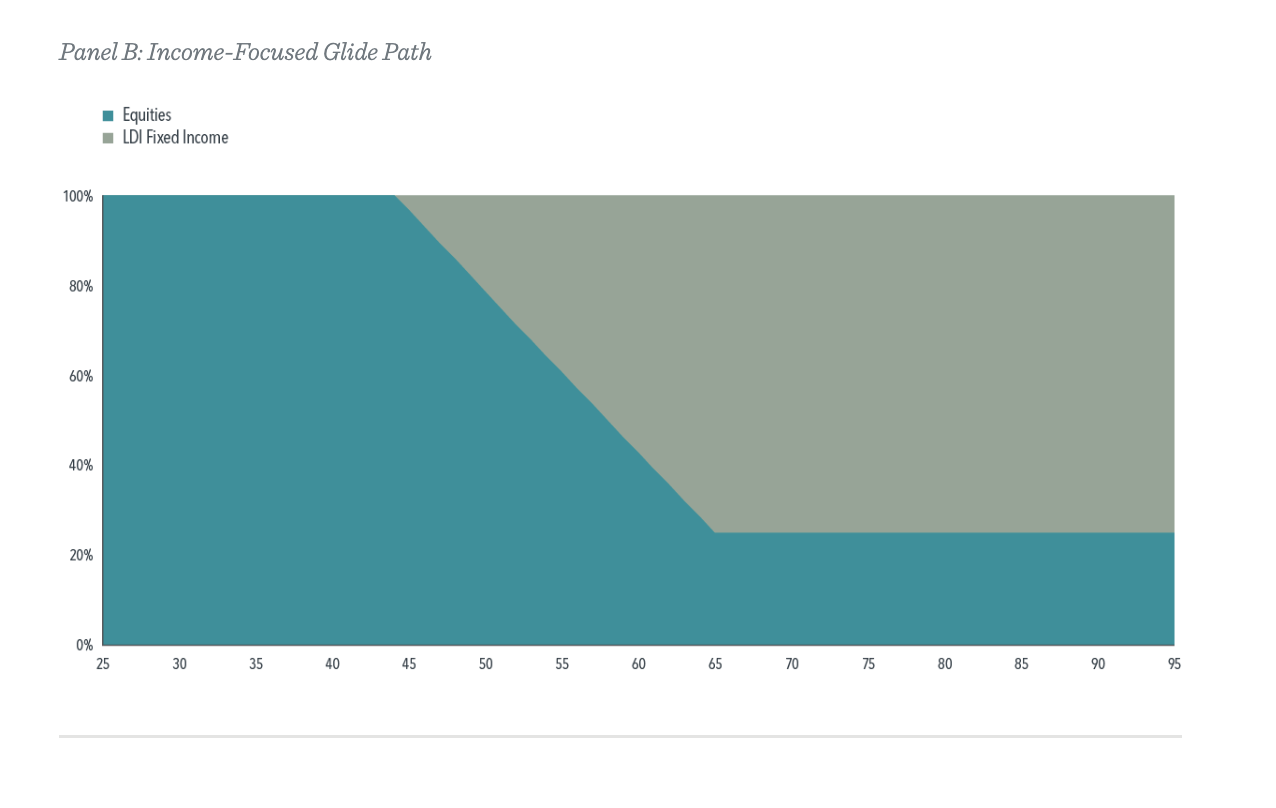

Income vs. Wealth-Focused Portfolios

DFA compared three investment approaches:

- Two "wealth-focused" portfolios, modeled after common target date funds, which gradually reduce stocks and replace them with short-term bonds.

- One "income-focused" portfolio, which uses liability-driven investing, or goals-based investing, as well as inflation-protected bonds to match expected retirement spending.

All three portfolios begin with 100% in stocks at age 25, reducing stock exposure starting at age 45. By retirement at age 65, the stock allocation is either 25% or 50%, depending on the strategy.

The income-focused portfolio is different: Instead of shifting into short-term bonds, it uses longer-duration inflation-protected bonds that are better aligned with retirees' future spending needs.

This strategy also allows for a stable equity allocation in retirement, something Bengen, Kitces and Pfau have advocated for years.

Here are the glide paths for each of those three approaches.

Wealth-Focused Glide Paths

Income-Focused Glide Path

Forecasting Retirement Outcomes

To compare the portfolios, DFA modeled a hypothetical saver who contributes $12,500 annually for 40 years and then retires at age 65. The goal: generate consistent, inflation-adjusted income for 30 years.

The results may be surprising:

The income-focused portfolio delivered a similar or better outcome than the traditional approaches, with a lower chance of running out of money.

That’s a big deal. It shows you don’t have to take on more risk to secure your retirement income.

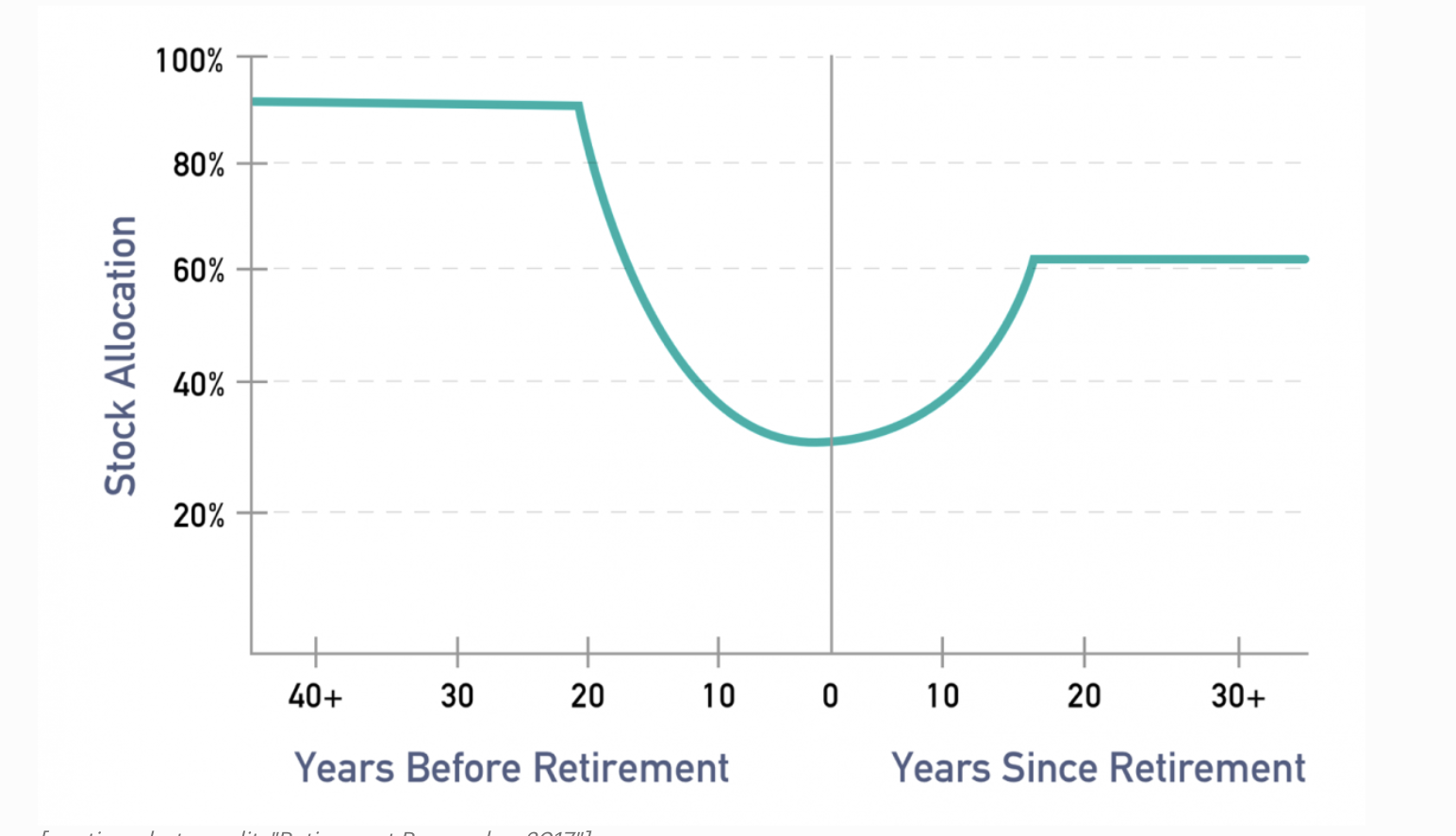

But what happens next is even more interesting, because it aligns with recent thinking from Kitces, Pfau and Bengen: Raising equity exposure during retirement may help your money last even longer.

Myth #1: Short-Term Bonds Are Always Safer

Many investors assume short-term bonds are the safest choice in retirement. Intuitively, it makes sense: You’re trading return for stability, but the latter is frequently more important in retirement, as capital preservation becomes a key concern.

But DFA’s research shows that when the goal is income stability, longer-term bonds that match your spending horizon are actually safer.

For example, in very simple terms, if you know you’ll need income of $25,000 in 10 years, a bond that pays exactly that, regardless of market fluctuations, is your safest bet.

That’s the principle behind liability-driven investing (LDI).

Short-term bonds may look less volatile on paper, but they leave retirees exposed to reinvestment risk and inflation.

Short-term bonds seem safer because their prices don’t fluctuate much, but they mature quickly. That means retirees must reinvest often, potentially at lower rates, while inflation erodes their future purchasing power.

That’s why DFA’s income-focused portfolio uses longer-dated, inflation-protected bonds: They’re better suited to meet known future needs.

Myth #2: More Stocks Always Mean More Income

What if you just keep a higher percentage of your money in stocks? Wouldn’t that deliver better long-term returns and more income?

Not necessarily.

DFA compared two wealth-focused portfolios: one with 25% stocks at retirement, and one with 50%. Surprisingly, the higher-stock version did not generate much more retirement income, but it did have a higher chance of running out of money.

This finding supports a middle-ground approach: Maintain moderate stock exposure at retirement, and gradually increase it afterward, a strategy supported by Bengen, Pfau and Kitces.

Adding Stock Exposure After Retirement

Why increase stocks in retirement?

- After you’ve secured near-term spending with stable bonds or annuity income,

- You can take incremental equity risk with long-term money by adding small amounts of equity in retirement.

- This money may grow faster over time and protect against outliving your savings.

This “rising equity glidepath” gives retirees the emotional benefit of safety early in retirement and the financial benefit of growth later.

Myth #3: High Stock Exposure Protects Against Longevity Risk

Living a long life is a wonderful thing. but financially, it means your money needs to last longer.

You might intuitively think that more stocks = more growth = more longevity protection.

But DFA’s analysis shows that this may not be the best approach.

Their stock-heavy portfolios had the highest failure rates, even in simulations where retirees lived to age 95.

A better solution? Use a combination of:

- Inflation-protected bonds to cover near-term needs,

- Strategic equity exposure to support long-term growth,

- And possibly annuities or delayed Social Security to provide guaranteed lifetime income.

Kitces has long recommended delaying Social Security to age 70 and using portfolio withdrawals to bridge the gap.

(Yes, I realize the Social Security Administration basically reiterated its previous research showing that it will be unable to pay 100% of benefits in 2033 without Congressional action. A similar thing happened in the past, and Congress made sweeping changes in 1983, just in the nick of time. Watch for something similar to happen again.)

These steps effectively buy you a larger, inflation-adjusted annuity, without needing to rely on the stock market for income in your early retirement years.

What It Means: Income Stability First, Growth Second

DFA’s research, along with insights from Bengen, Pfau and Kitces, suggests a smarter retirement strategy:

- Use high-quality, longer-term bonds that align with your expected income needs in the early years of retirement.

- Start with modest equity exposure of around 25% at retirement, then gradually increase your stock allocation over time.

Don't rely on equity returns to solve for longevity. Instead, use tools like Social Security timing, annuities, and spending flexibility.

So yes, you can actually lower your risk and still enjoy more income. Turns out, the real retirement flex is not running out of money.