Retirement Investing in 2025: Why Old Rules No Longer Work

Smart income beats market timing panic

You've reached your free article limit

You've read 0 of 1 free Pro articles.

If you’re planning to retire in the next decade or so, you’re facing some hurdles that previous generations didn’t have to deal with.

Market volatility rears its head on a regular basis, so that’s actually not anything special. It’s natural to want to sell out when markets head south, but that benefits institutions that swoop in to buy assets on the cheap.

A real concern now is the bond market: We’re seeing interest rates continuing to rise; the 30-year Treasury yield is hovering near 5%

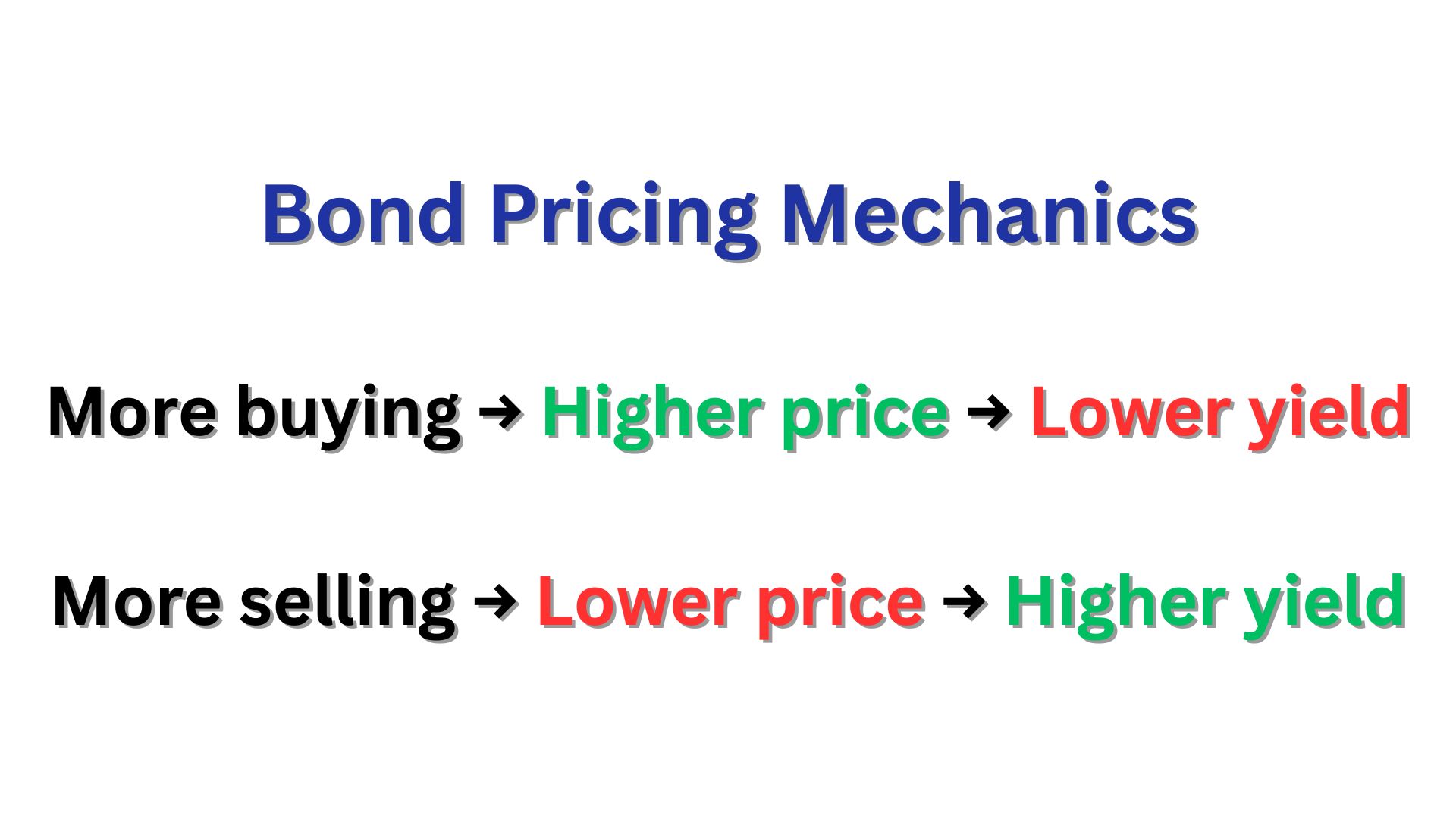

Here’s a breakdown of what’s going on:

- When investors buy bonds, demand goes up, and that raises the price of the bond.

- But as a bond's price rises, its yield goes down. This is just how bond math works.

That’s why, when investors are fearful, you generally see a flight to bonds for safety. That buying pressure pushes bond prices up and interest rates down.

But recently, even as markets fell and uncertainty rose, people are not buying bonds in the usual way.

So instead of bond prices going up and yields dropping, we’re seeing yields rising, meaning bond prices are falling.

This isn’t what you typically see in the traditional “safe haven” scenario.

This current situation is unusual, and it may signal market stress or lack of confidence in U.S. government debt, in an era of inflation, high government spending, the threat of tariffs and growing geopolitical risk.

But you’re not stuck with sub-optimal investments that could inadvertently add risk. Let’s take a look at portfolio construction.

Why Smart Asset Allocation, Not Panic Selling, Matters in Retirement

Here’s a newsflash: The purpose of your retirement funds is not to “make as much money as possible” or even “beat the market.”

I know that may sound counterintuitive, because we’re bombarded with messages that reward excitement, not discipline. Trading feels like action and progress, even if it’s actually detrimental.

The point of your retirement investments is to generate the income you need for as long as 30 years, without taking the risk of chasing headlines or jumping in and out of the market.

I understand: That’s less exciting than stock picking, but smart portfolio construction is the proven way to make and keep the money you’ll need in retirement.

It’s crucial to rebalance your portfolio as you age, and contrary to the so-called conventional wisdom, that doesn’t necessarily mean getting more conservative.

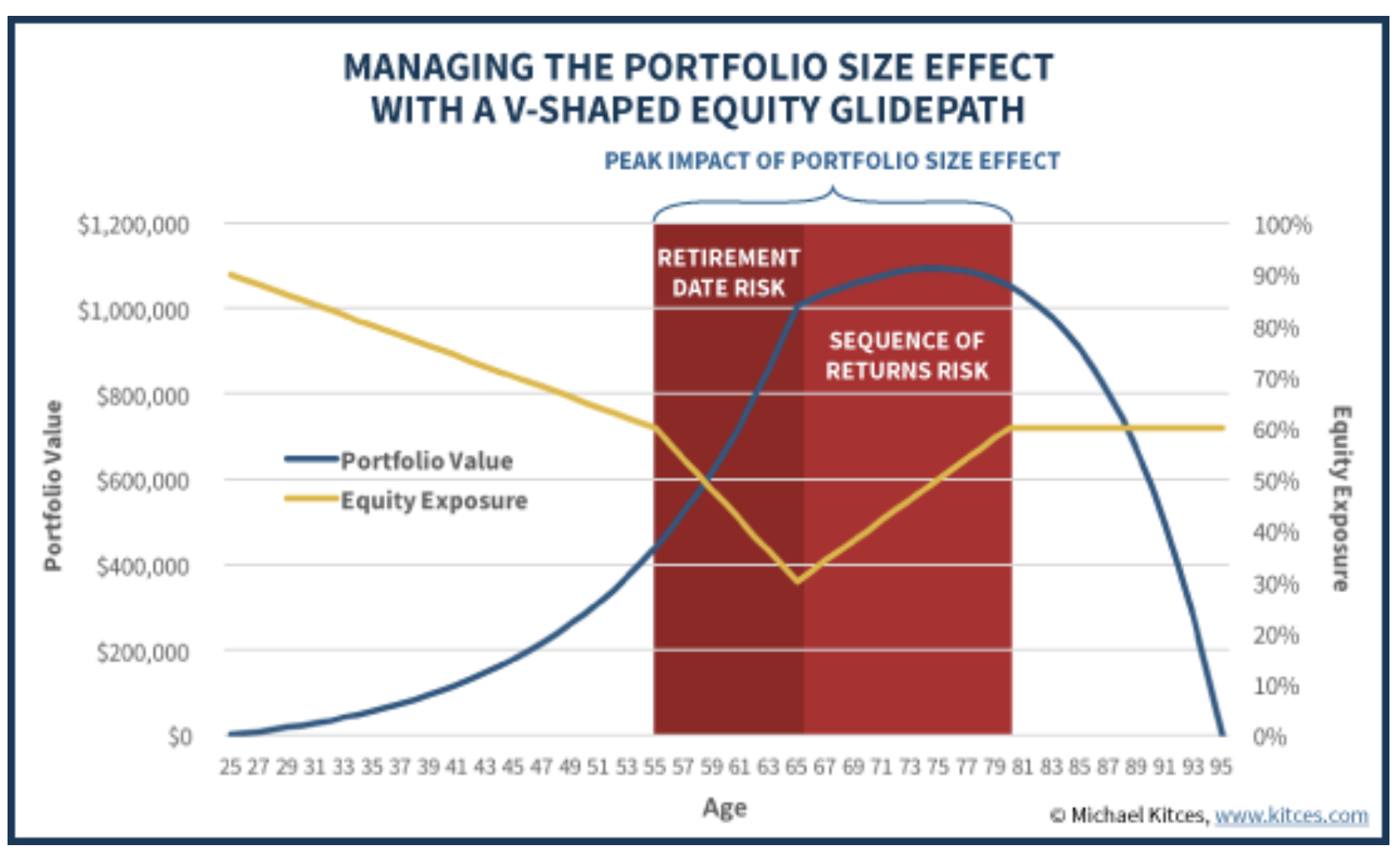

In fact, retirement researchers Michael Kitces and Wade Pfau have shown that slightly increasing equity exposure after retirement can actually reduce the risk of running out of money.

[T]he optimal equity exposure to manage the risks associated with the portfolio size effect over an individual’s full lifecycle would take on a V-shaped glidepath, getting more conservative in the decade leading up to retirement, remaining conservative in early retirement, and then drifting at least somewhat higher again in the later years. -Michael Kitces

This strategy helps balance the risk of market downturns with the need for long-term growth.

Here’s a graphic showing how that glide path might look. Notice the gradual decrease in equity exposure until about age 65, when it shifts higher again.

Remember, a target date fund's glide path is the shift in its asset allocation to become more conservative as it gets closer to the target date.

William Bengen, creator of the 4% withdrawal rule, echoes this idea in his upcoming book A Richer Retirement: Supercharging the 4% Rule to Spend More and Enjoy More. I recently interviewed Bengen, and I’ll write more about this in a future email.

What Kind of Stocks to Own

Most retirees need reliable income. But there are some valid concerns about treasuries and rising interest rates.

At the same time, you need to generate growth to be sure your portfolio can outpace inflation.

One way to achieve those objectives is through dividend-paying stocks. Please note: That doesn’t necessarily mean picking single stocks; it can also mean using dividend-paying ETFs like the Schwab US Dividend Equity ETF (SCHD), which has returned 12.30% since its inception in 2011.

No, that’s not as much as the SPDR S&P 500 ETF (SPY), but that’s because dividend payers tend to hail from the ranks of established companies with a long history of profitability and stability. In other words, not the fast-growth movers like Nvidia NVDA or Palantir PLTR that send the S&P 500 to new heights.

Dividend Stocks Versus Treasuries

Here’s a single stock example.

Pfizer is currently offering a 7.20% dividend yield. Even if that gets trimmed to 5%, it still outpaces what many treasuries offer. For retirees looking for consistent income, this kind of opportunity deserves consideration as part of a broader allocation strategy, not a one-off trade.

Time Horizon for Dividend Stocks

Now, you might be wondering if you should invest in dividend stocks or ETFs if you need the money for income in the not-so-distant future. For the most part, that’s a sound strategy, since you don’t want to sell the stock to meet income needs.

But here's a twist: When you invest for income, like with dividend-paying stocks, you often don’t have to sell shares to generate cash. Here’s why:

- As long as the dividend is reliable, short-term ups and downs in the stock price don't matter as much.

- The risk is only a problem if you're forced to sell during a downturn, which is why having other sources of cash or a cushion, like a bond ladder or cash bucket, is important.

- The “five-year rule” mainly applies to investments where you’ll need to sell shares for income.

- If your income is coming from dividends, and you don’t need to touch the principal, price volatility becomes much less of a concern.

Today’s retirees need to be more flexible and adaptable than their parents. That means using strategies that go beyond outdated rules of thumb. By focusing on income and a dynamic approach to asset allocation, you can build a portfolio that won’t kick the bucket before you do.