Mutual Funds, ETFs or Both? How to Choose Wisely

Here's how these investments are similar, and how they differ.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Is your portfolio a mix of ETFs and mutual funds? Maybe IRAs rolled over from 401(k)s are now invested using ETFs, but your employer-sponsored retirement account still holds mutual funds.

Is one better than the other?

ETFs and Mutual Funds: Same Goal, Different Tools

Both ETFs (exchange-traded funds) and mutual funds can give you access to diversified portfolios, including broad market indexes; market-cap, sector-specific or regional strategies; or more complex multi-asset allocations.

The key difference lies in their structure and trading mechanics:

- ETFs trade on exchanges throughout the day, offering real-time pricing, intraday liquidity, and often lower expense ratios.

- Mutual funds are bought or sold at the end-of-day net asset value (NAV) and may carry higher internal costs, especially for actively managed funds.

So while the underlying investments may be similar, some aspects of the investor experience, such as fees, trading, and taxes, can be quite different.

ETFs: More Flexibility, Lower Fees

- You can buy or sell shares anytime during the trading day, just like a stock.

- ETFs often have lower expense ratios and are generally more tax-efficient. Many ETFs disclose holdings daily, making them more transparent than mutual funds.

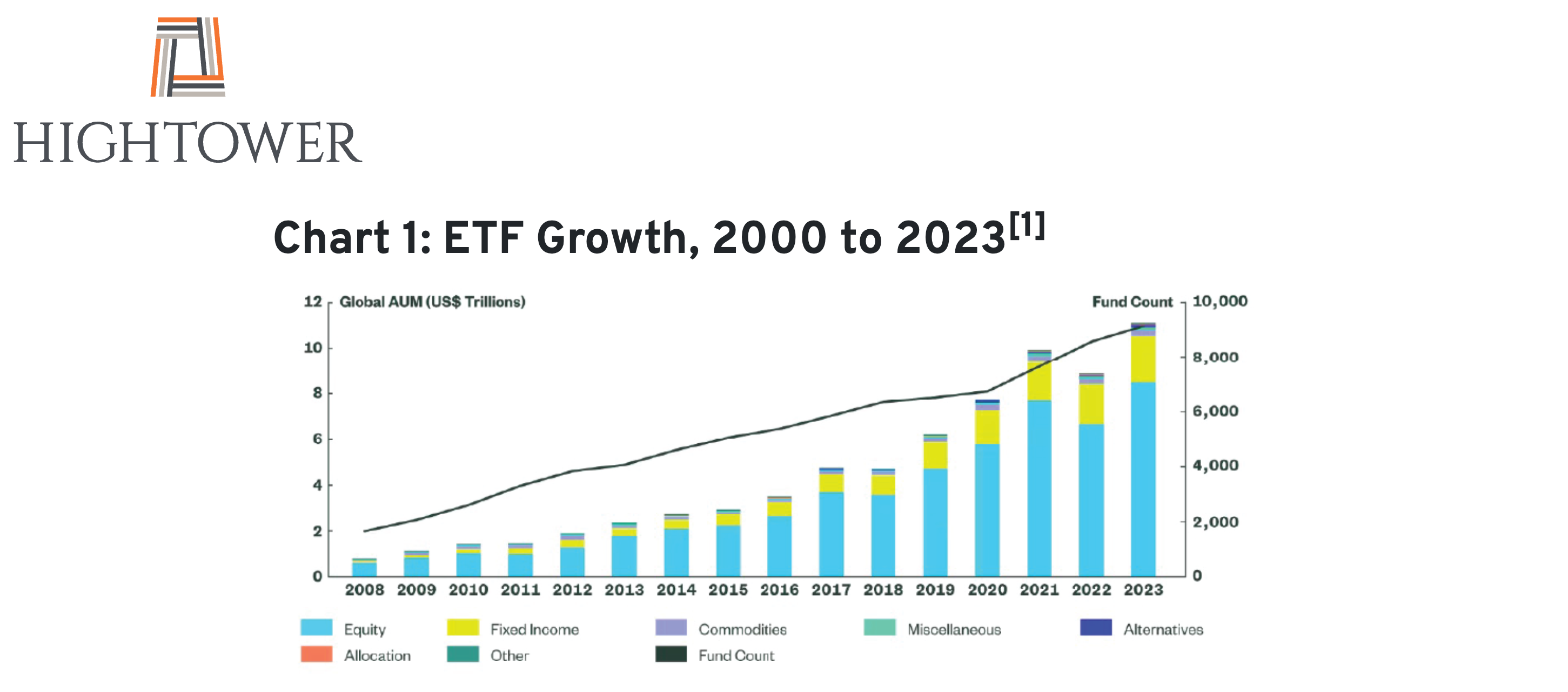

This chart from Hightower shows the fast adoption of ETFs between 2008 and 2023.

Understand What You Own

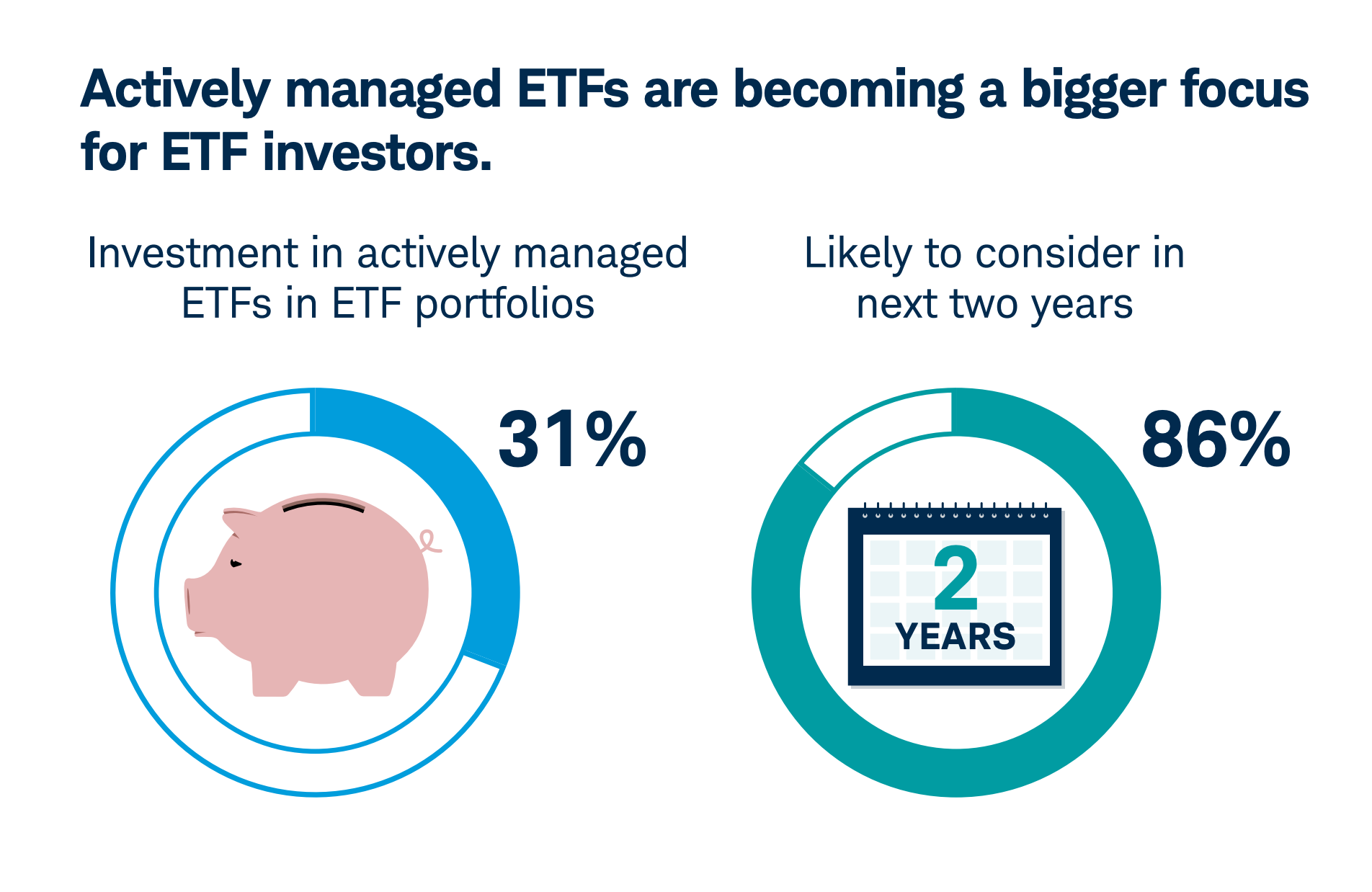

With a growing number of actively managed ETFs, expense ratios are on the rise. Be sure you understand whether you’re buying an index fund or one that has a manager picking the investments.

According to the Financial Times, “Active ETFs charge 0.4 per cent a year (using an industry asset-weighted average) around three to four times as much as a typical passive fund.”

This graphic from Schwab Asset Management’s 2024 “ETFs and Beyond Study,” which surveyed 2,200 investors from various age groups, and with varying investment strategies, shows increasing interest in active ETFs.

Tax Benefits of ETFs

ETFs are built with a unique structure using what are called “creation units.”

This lets the ETF manager handle investor redemptions without having to sell securities, so you’re less likely to be hit with capital gains taxes.

Mutual funds, by contrast, may trigger taxable events whenever the fund manager sells assets to meet redemptions.

Mutual Funds: Tried-and-True (but a Bit Old School)

Mutual funds have been at the center of retirement and long-term investing for decades. They’re very reliable in offering diversified exposure to stocks, bonds, or other assets within a single product.

Some characteristics include:

- Priced once daily after the market closes.

- Often have higher fees than ETFs.

- Still widely used in 401(k) and other retirement plans.

Here’s the catch with mutual funds and taxes:

You may owe capital gains tax even if you didn’t sell your shares. That’s because the fund did. This quirk is due to distribution rules that apply to all mutual fund shareholders.

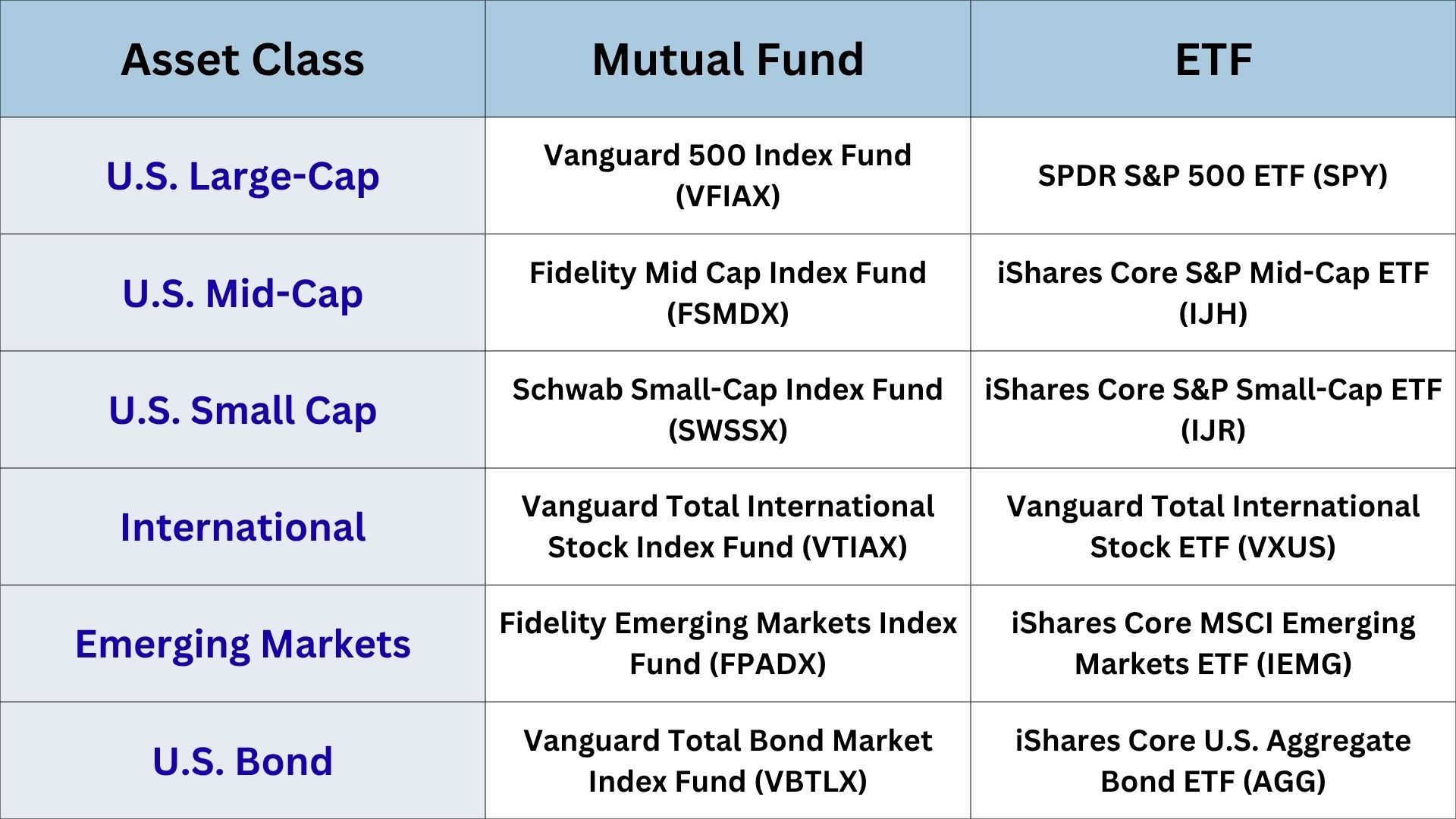

Mutual Funds vs. ETFs: Real Examples

Here’s a comparison of a basic diversified portfolio using low-cost index mutual funds vs. ETF equivalents. I included examples from various fund families, but there are many other choices available.

This is for illustration purposes only, and is not a recommendation.

So Why Aren’t ETFs More Common in 401(k)s?

- Historically, mutual funds paid revenue-sharing fees to plan providers, helping cover administrative costs.

- ETFs didn’t, so there was less financial incentive for providers to offer them.

- That’s now shifting. Zero-revenue-share and ETF-based 401(k) plans are gaining ground, so you’ll likely see more ETF options in retirement plans soon.

It Shouldn’t Be an Either/Or Choice

If you’re investing through a 401(k) or IRA, mutual funds may work just fine, especially since taxes on capital gains don’t apply in retirement accounts. Intraday trading (an ETF feature) doesn’t matter if you’re investing for the long haul and not making reactive moves.

But in a taxable brokerage account, ETFs can offer significant advantages, especially when it comes to managing tax exposure and keeping fees low.