Investing Mid-Career: Maximize Your Financial Momentum

How to invest smarter in your 40s and 50s

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I’ve driven cross-country at least 10 times over the years. The actual number of trips could be more, but I’ve lost count.

If you’ve taken long car trips, you probably know the feeling of being midway through your trip. You’re ready to finally be at your destination and relax with your favorite adult beverage.

The idea of a journey toward retirement applies to your mid-career finances. By the time you're in your 40s or 50s, you've got some miles behind you but haven’t yet reached your destination.

Prime Earning Years

Now that your paychecks are bigger than they were in your 20s, you can, in theory, put more cash in the stash.

However, you may have more competing priorities right now, in the form of college savings and a mortgage. You might still have younger kids at home, a few years away from college. Or your kids might be a little older, out of college and getting ready to fly the coop.

Fortunately, today’s mid-career investors can use GPS-like technologies, from retirement calculators and risk profiling apps to target-date funds, diversified ETFs and even financial planning software.

The road will definitely still have bumps in the form of market volatility, career changes and a slew of unexpected expenses, but you have plenty of time to make sure you’re traveling the right course.

Review Your Financial Picture

Take stock of the allocations in your retirement accounts and taxable brokerage accounts. Even if you don’t have a specific retirement date in mind, it’s not too soon to check whether your current savings rate is on pace, relative to even a general target.

Prioritize paying down high-interest debt and building an emergency fund

Also consider hiring a financial planner to crunch the numbers for you and make any recommendations not only for your investments, but to review other items like insurance, estate planning and tax strategies.

Optimize Asset Allocation

According to a report from brokerage T. Rowe Price, 45-year-olds should have three times their current income set aside for retirement.

“This savings benchmark rises to five times current income at age 50 and seven times current income at age 55. Fortunately, there’s still time for even modest adjustments to have a large impact down the road,” wrote T. Rowe Price analysts.

Maxing out retirement accounts is a great idea, if you can do that. In addition, after age 50, you can contribute even more in the form of catch‑up contributions.

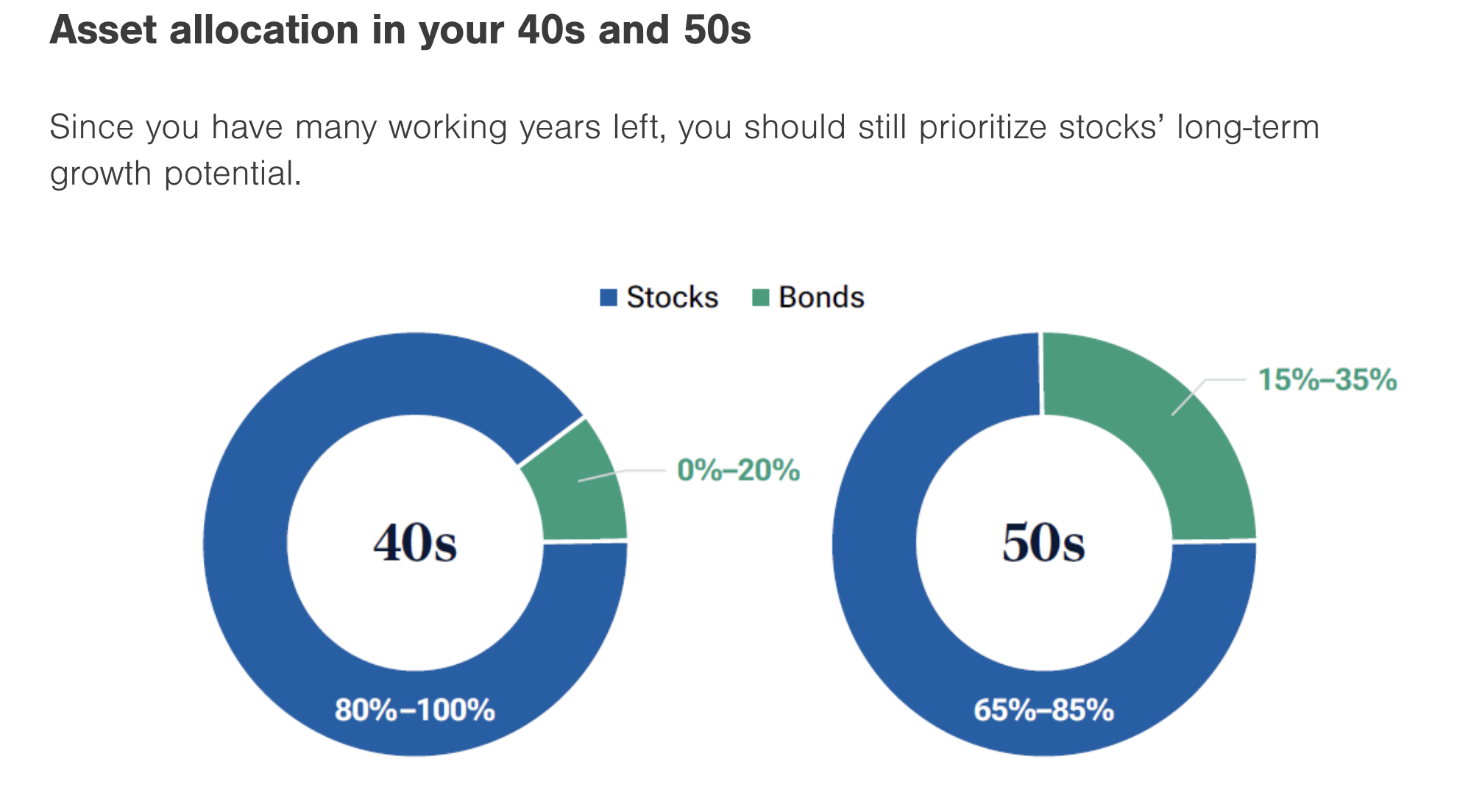

Here’s a look at a sample retirement allocation for investors in their 40s and 50s.

Balancing Growth and Capital Preservation

Although there are some clear guidelines for allocating in your 40s and 50s, you don’t necessarily have to allocate strictly by age.

After a major life event, such as marriage, divorce or a job change, take the time to review your asset mix to make sure it aligns with your revised objectives.

Remember, the assets you own should dovetail. Each one has a specific job; they’re not there just to “make money,” which is vague and not pegged to any particular financial goal. The whole reason to allocate is to smooth returns and minimize risk. Over time, this is a proven way to maximize returns.

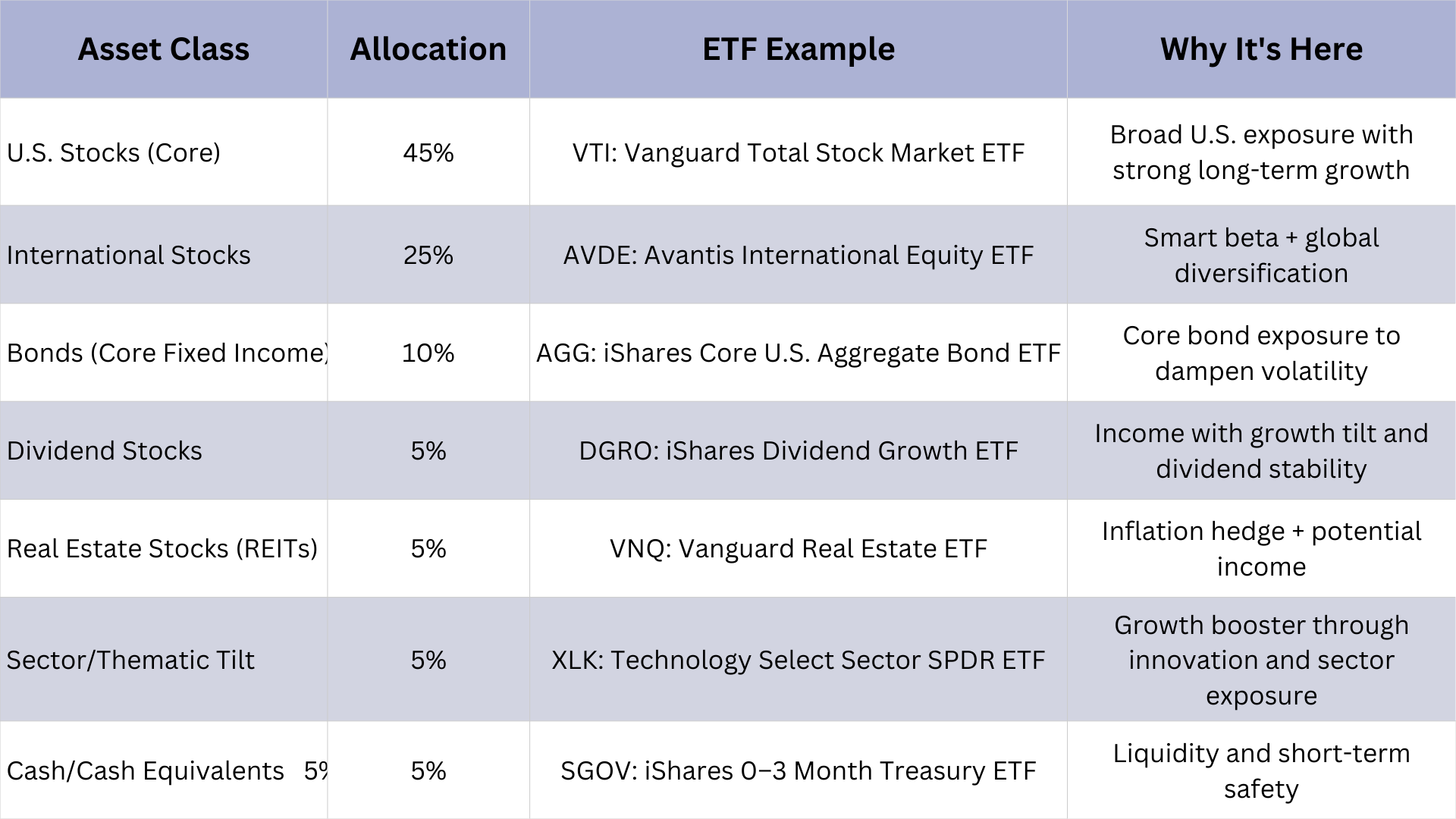

Given all that, below is a sample portfolio, along with allocations for investors in their 40s and 50s.

A couple of points about that sample allocation. This is simply one way your portfolio could look; there are certainly other ETFs that can achieve the same goals for you. Just be sure to understand what you own and why, and review expense ratios of any ETF you are considering.

Second, I realize that I’m talking about a broad age range here; a 40-year-old is at a quite different phase of life and career than a 59-year-old.

With that in mind, adjust those allocations as you go along, gradually tilting more toward fixed income or dividend-paying stocks, while lowering your allocation to higher-risk growth stocks.

Above all, understand what you own, why it’s there, and how much you should own of each asset. This isn’t the time to blindly guess or chase returns.

Mid-career investing isn’t about trying to drive as fast as possible. It’s about plugging away at the journey, even though your destination may not be sight yet. Stay focused, stay diversified, and keep your eyes on the road ahead.