Laziness Is the Key to Retiring Rich

Don't overthink your investments.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Traders famously tinker with their stock holdings: Adding this, selling that, following trend lines and indicators, and tracking just the right time to make a move.

But with your long-term investments, you should do exactly the opposite!

That’s the philosophy behind “lazy portfolios,” a group of low-maintenance, diversified investment strategies designed to perform well across market cycles, with minimal upkeep.

This isn’t a new phenomenon:

- Vanguard founder Jack Bogle was a fan of keeping things simple.

- So is Taylor Larimore (who turned 101 this year), author of “The Bogleheads' Guide to the Three-Fund Portfolio: How a Simple Portfolio of Three Total Market Index Funds Outperforms Most Investors with Less Risk.”

- So is Bill Schultheis, a financial advisor and author of “The Coffeehouse Investor: How to Build Wealth, Ignore Wall Street, and Get On with Your Life.”

How to Be a Lazy Investor

A lazy portfolio typically consists of two to four low-cost index funds covering broad swaths of the market, such as:

- U.S. total stock market

- International stocks

- U.S. bonds

- In certain cases, REITs (real estate investment trusts) or TIPS (inflation-protected securities)

The core idea: Avoid overthinking, overtrading and trying to play a game of “beat the market.” Instead, you’re investing in the market and relying on broad diversification, low costs and occasional rebalancing.

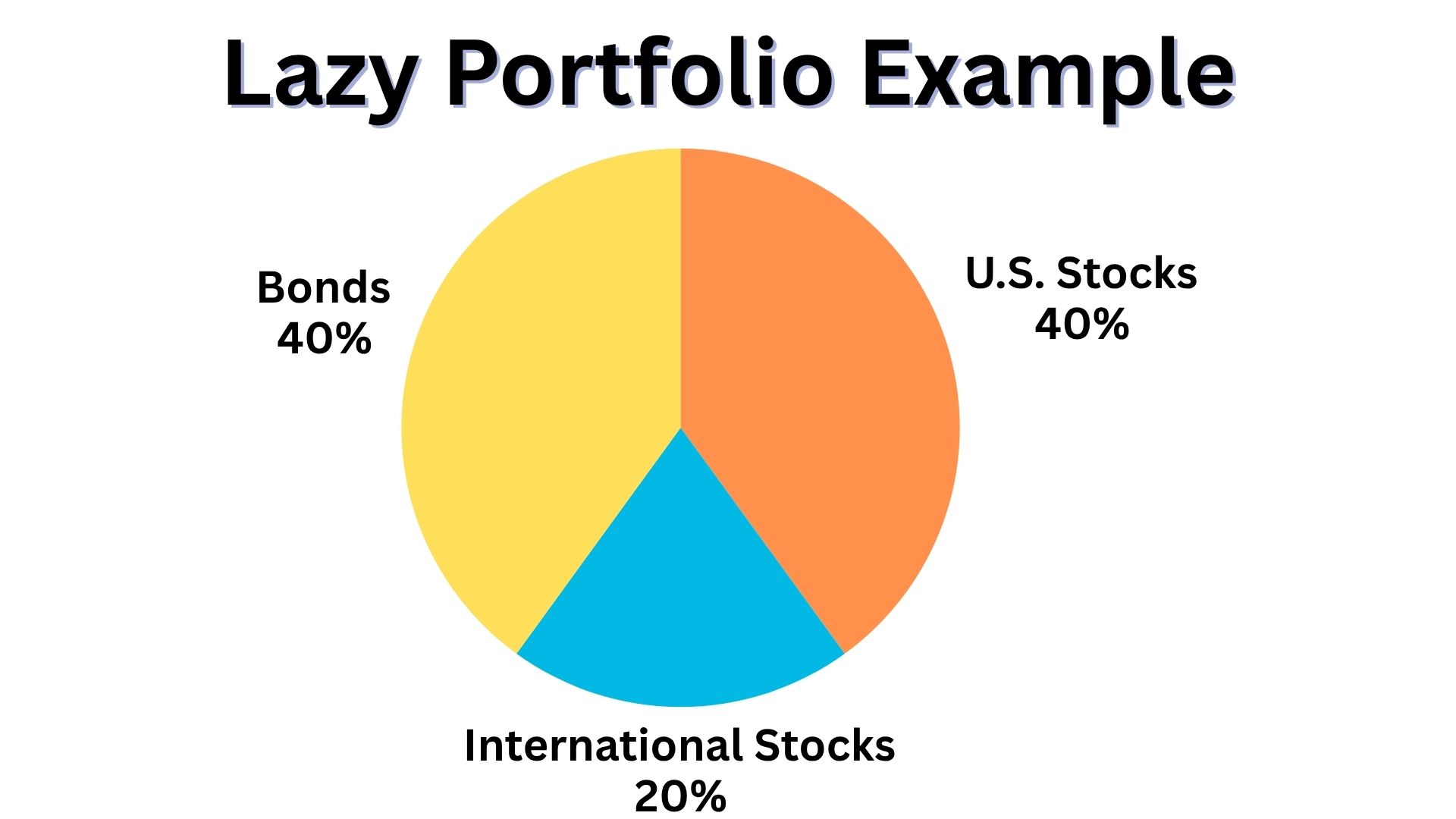

The Classic Three-Fund Portfolio

The most well-known lazy portfolio is the three-fund portfolio made popular by Taylor Larimore and the Bogleheads community. This can be constructed using either mutual funds or ETFs.

It includes:

- Vanguard Total Stock Market Index (VTSAX /VTI)

- Vanguard Total International Stock Index (VTIAX /VXUS)

- Vanguard Total Bond Market Index (VBTLX /BND)

This trio offers instant global diversification and a balanced mix of growth and income.

Your allocation could be similar to the pie chart shown above, or can be adjusted with more exposure to stocks, or less, depending on factors such as your time horizon and ability to take on equity risk at this juncture.

Good starting points can be found in prior articles I've shared that are related to your age. Like this one for investors in their 20s, or this one for mid-career investors, or this one for those of us who may be retired.

Of course, you can achieve this goal with any fund family, or a combination of several, such as Fidelity, Schwab, iShares, and State Street’s SPDR ETFs.

You can mix and match these depending on your preferred platform, fee structure, or account type, such as 401(k), IRA or taxable brokerage account.

Portfolio 1: Fidelity Core Lazy Portfolio

- 40% Fidelity Total Market Index Fund (FSKAX)

- 20% Fidelity Total International Index Fund (FTIHX)

- 40% Fidelity U.S. Bond Index Fund (FXNAX)

Portfolio 2: Schwab & iShares Blended Lazy Portfolio

- 40% Schwab U.S. Broad Market ETF (SCHB )

- 20% iShares Core MSCI Total International Stock ETF (IXUS)

- 40% Schwab U.S. Aggregate Bond ETF (SCHZ)

Portfolio 3: SPDR & iShares Lazy ETF Portfolio

- 40% SPDR® Portfolio Total Stock Market ETF (SPTM – 0.03%)

- 20% iShares Core MSCI Total International Stock ETF (IXUS – 0.09%)

- 40% iShares Core U.S. Aggregate Bond ETF (AGG – 0.04%)

So you get the idea. You can even tilt your stock holdings toward dividends or value, if you want income or more exposure to an equity asset class that’s historically shown outperformance.

Why These Portfolios Work

- Diversification

You own the entire market: U.S., international and fixed income. - Low Fees

Index funds typically have expense ratios as low as 0.03%, far lower than the actively managed funds you often find in 401(k) plans. - Behavioral Discipline

A simple portfolio discourages impulsive trading and market timing. - Automatic Rebalancing (if using target-date funds or robo-advisors)

Even without automation, rebalancing once or twice a year is often enough. Constant tinkering and trading is almost always a bigger problem that leads to diminished performance.

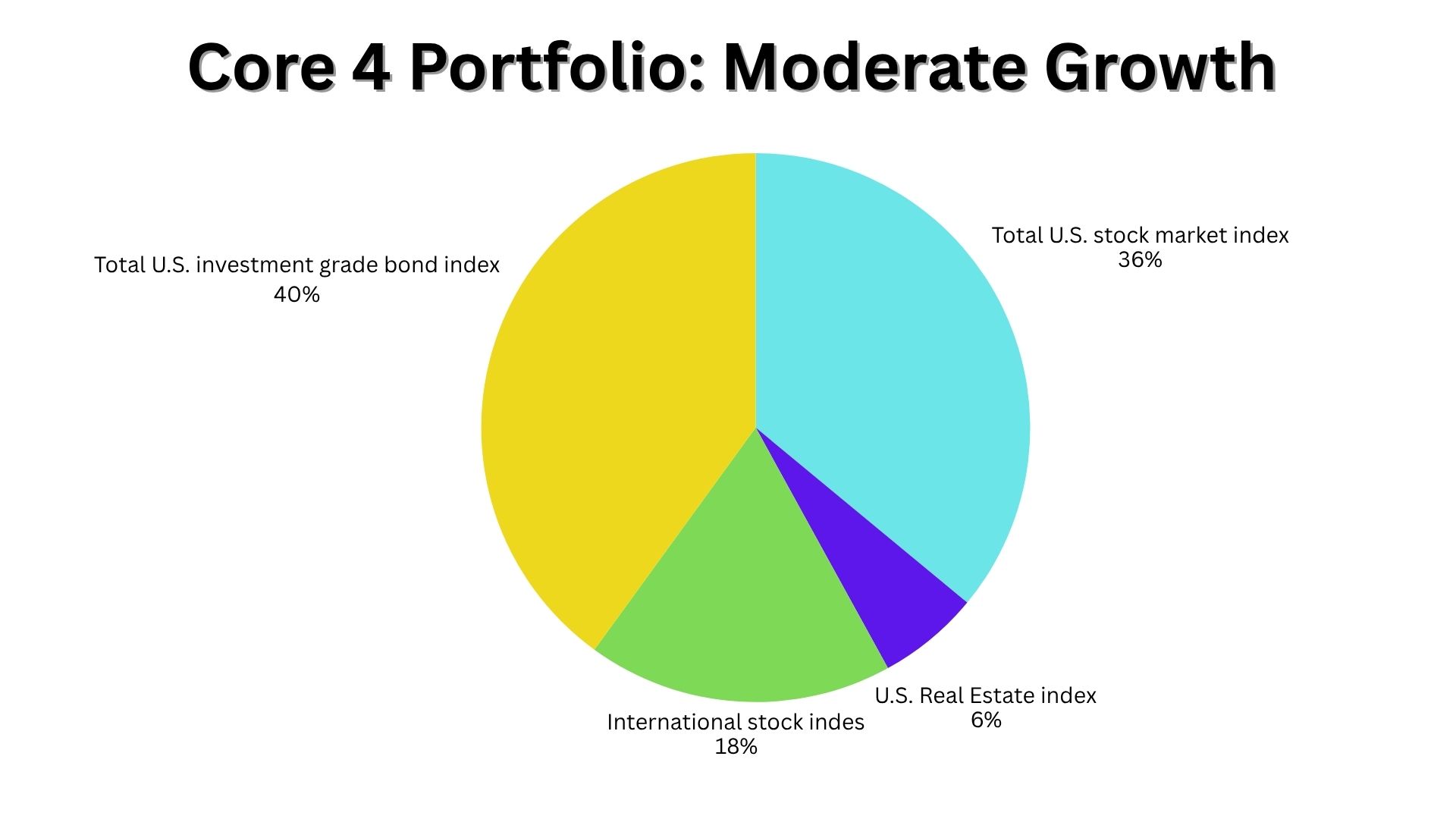

Still More Variations

Far from being an ironclad prescription, lazy portfolios can be adjusted and parsed into narrow slivers of asset classes. Here a couple other ways investors can allocate a lazy portfolio.

Although these contain more instruments than the basic three-fund model, the idea is the same: Don’t fiddle with the holdings themselves or the percentages, other than to occasionally rebalance.

Rick Ferri’s Core Four Portfolio:

- Total U.S. Stock Market Index: 36%

- U.S. Real Estate (REIT) Index: 6%

- International Stock Index: 18%

- Total U.S. Investment Grade Bond Index: 40%

This adds real estate exposure, offering income and potential for greater inflation protection.

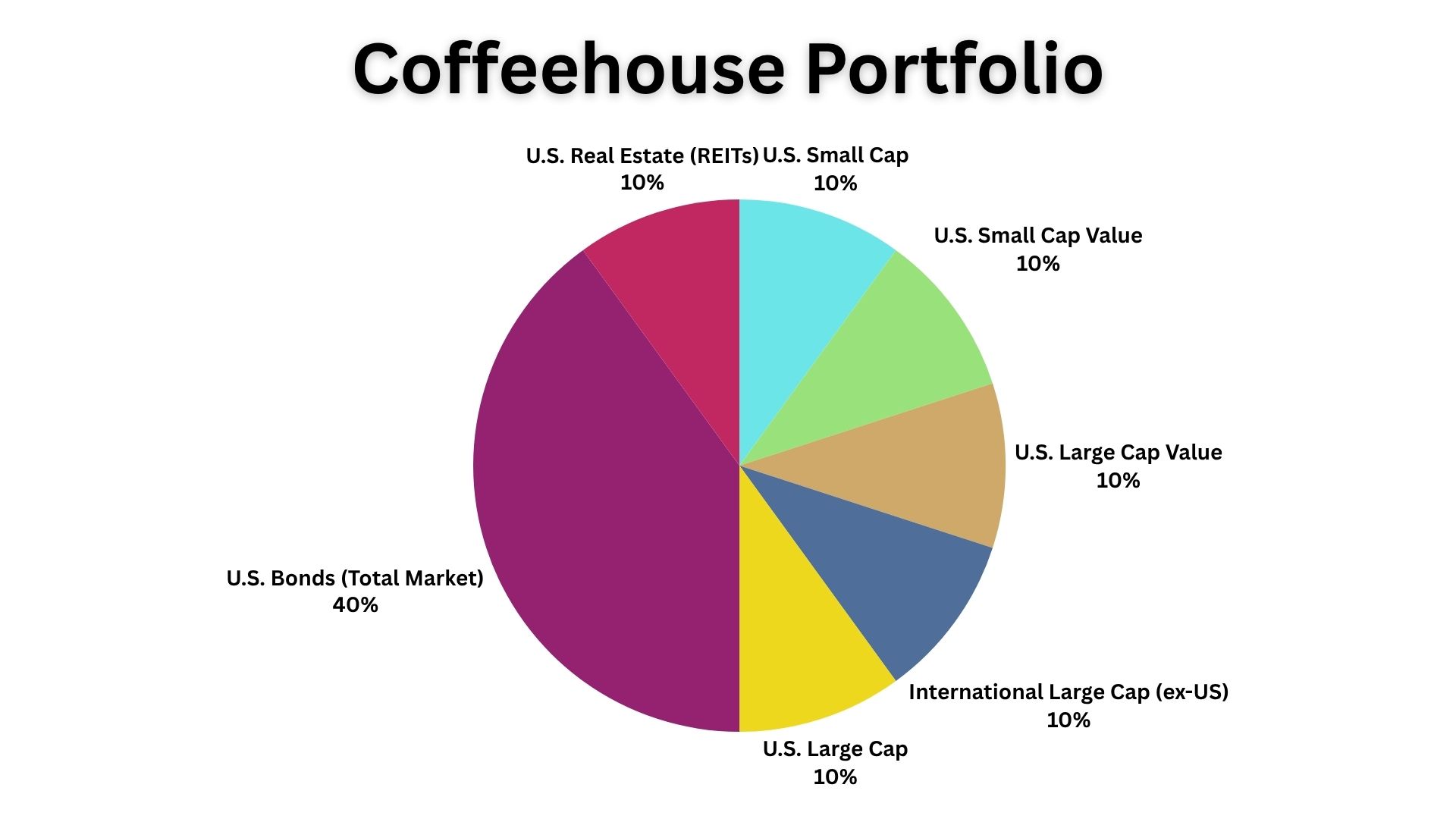

Bill Schultheis Coffeehouse Portfolio

This one slices the U.S. market into value and small-cap funds, giving investors more tilt toward asset classes that have historically outperformed. It’s still easy to manage, and the same rules about rebalancing apply.

- U.S. Small Cap: 10%

- U.S. Small Cap Value: 10%

- U.S. Large Cap Value: 10%

- International Large Cap (ex-US): 10%

- U.S. Real Estate (REITs): 10%

- U.S. Large Cap: 10%

- U.S. Bonds (Total Market): 40%

Why Lazy Works for Retirement

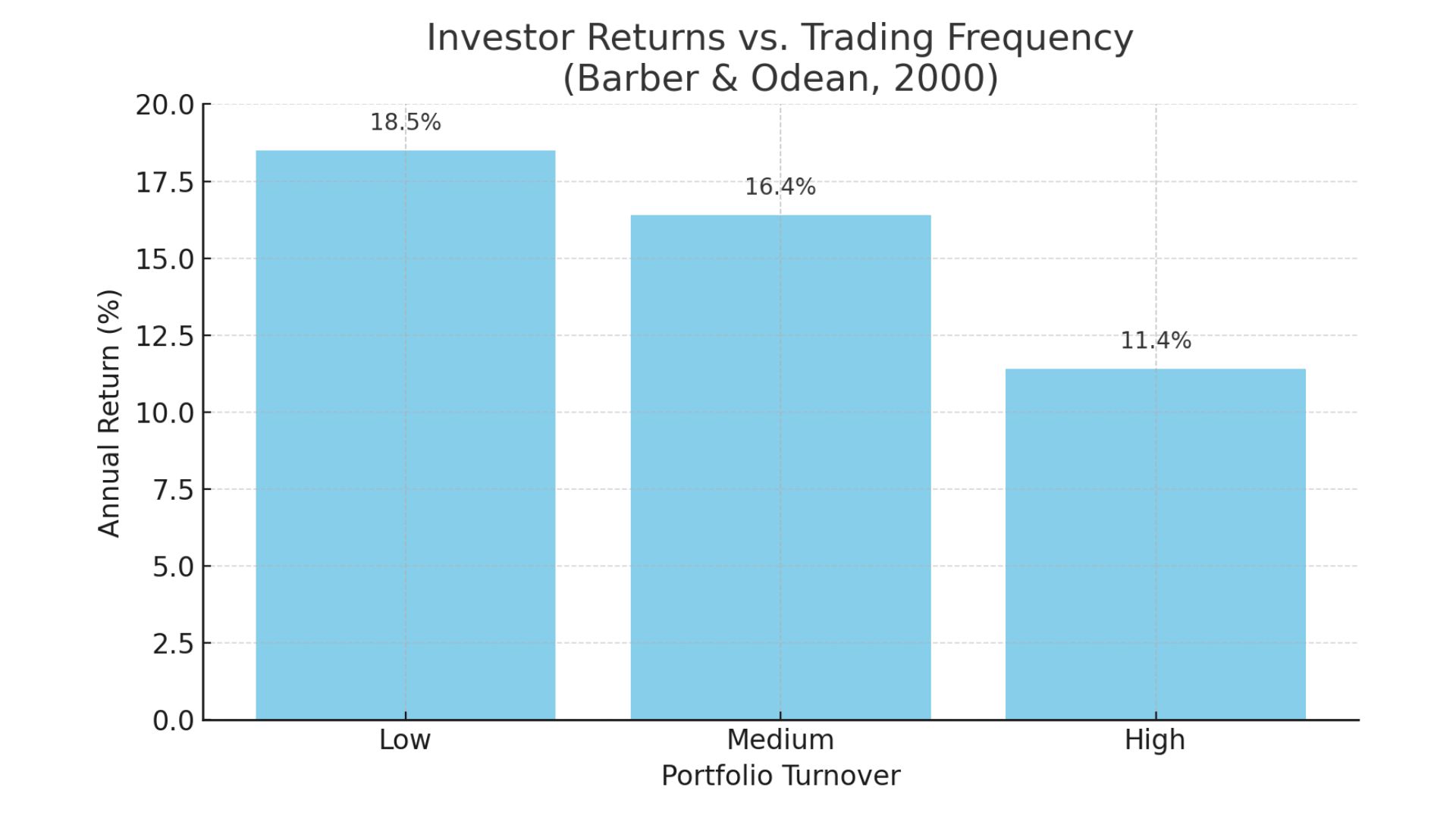

This stuff isn't new. It's been the subject of studies for decades.

There have been more recent publications, but a groundbreaking 2000 paper by Brad Barber and Terrance Odean (2000) documented that individual investors who trade the most underperform the market by a wide margin, achieving an annual return of just 11.4%, compared to a 17.9% market return during the period studied. (For their purposes, “the market” was a composite of indexes, not simply the S&P 500, and the data set was limited to a specific period of time).

But the point is applicable across various timeframes.

This chart visually underscores the issue, showing a steady drop in net performance as turnover rises, highlighting the familiar truth: The more you trade, the more your returns suffer.

I’ll close with a quote I’ve probably used here before, from Nobel Prize-winning American economist Paul Samuelson:

Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas.