Investing’s Single Most Important Decision Is Almost Always Fumbled by the Public

Almost no one questions if this investment approach is actually bad advice. They should. Plus, having little to no exposure to one asset class right now is likely to turn out to be a major mistake.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Most financial planners offer similar advice. They say, “Split your assets into stocks, bonds and cash in some formula that relates to both your age and your tolerance for risk.”

Very popular, especially inside retirement accounts, target date ETFs and mutual funds aim to provide lazy people with these allocations via a one-stop shop.

Almost nobody questions if the technique being pushed is actually bad advice. They should.

Why do I say that?

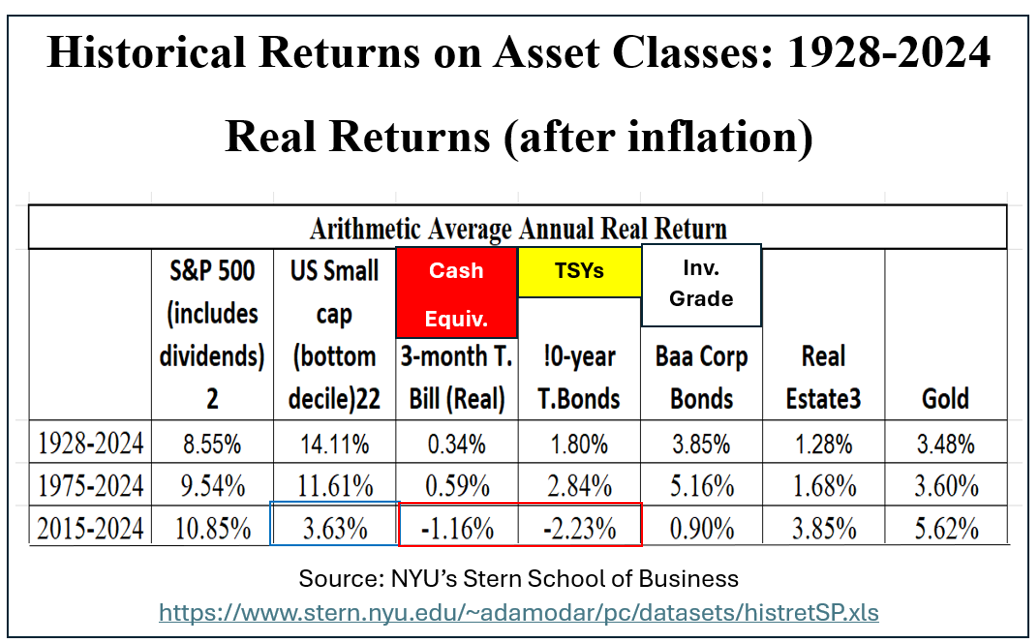

NYU’s Stern School of Business has been kind enough to update both absolute and real (inflation-adjusted) total returns on various asset classes each year since 1928.

The results speak loudly and clearly to what has proven to be the best place to get rich over time.

Over the entire 96-year period, large-cap stocks (S&P 500 or equivalent) averaged 8.55% annualized above the cumulative inflation rate. 90-day T-bills (cash equivalents) returned only 0.34% annually. 10-year Treasury bonds provided after-inflation returns of just 1.80%. Investment-grade corporate bonds, which were not government guaranteed, did better than the “safer” Treasury paper at 3.85% annualized. That was more than twice as much as the government-backed rivals.

Gold, often touted as a solid inflation hedge, only brought in 3.48% in annual real returns. That was with gold prices near an all-time high recently.

Ditto for real estate, which many people swear by as a great path to wealth. Cumulative real growth of 1.28% annualized paled in comparison to stocks.

Smaller-company stocks turned out to be the best-performing asset class over the 96-year period [+14.11% above inflation annualized] as well as over the 49 years dating back to 1975. They lagged the S&P 500 badly, though, over the most recent decade.

My previous article referenced regression to the mean as a driving force of nature. The severe underperformance of smaller-cap equities since 2015 suggests that trend is long overdue for a change of fortune. Many people have little to no exposure to that asset class right now due to its recent poor results. That is likely to turn out to be a major mistake going forward.

Both 3-month T-bills and 10-year Treasuries showed negative real returns since 2015.

Knowing all of the above facts, why do advisors consistently recommend major allocation to bonds and cash?

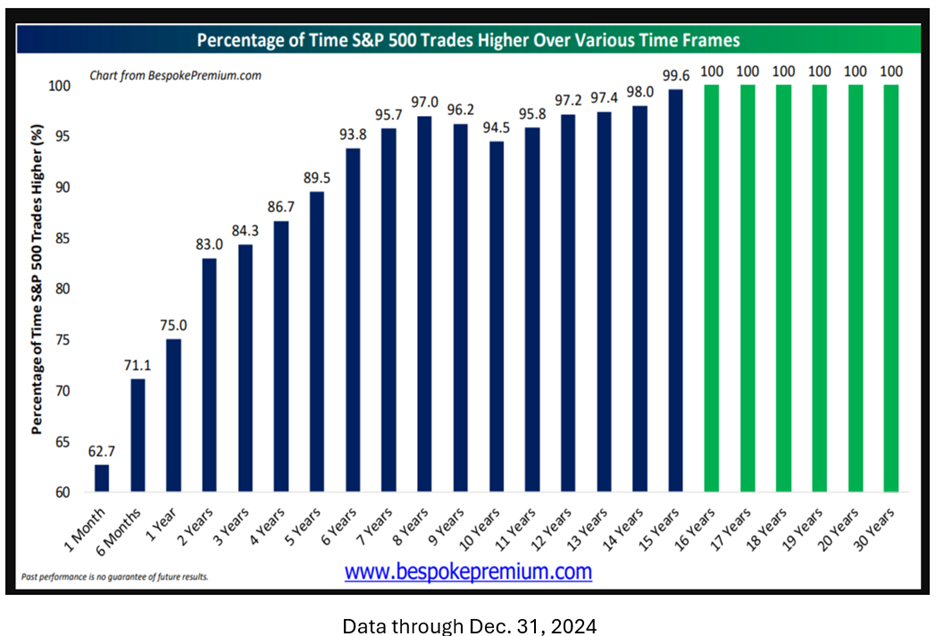

Stocks not only performed best, they did so with a high degree of confidence for success over all but the shortest time horizons.

The data below is courtesy of Bespoke Investment Group Premium research.

It shows that 75% of all single years since 1928 were profitable. That percentage grew to 83% over all rolling two-year periods and topped 90% for all holding periods of six-years or greater.

Long-term investors achieved positive returns over every single rolling 16 or higher year time frames.

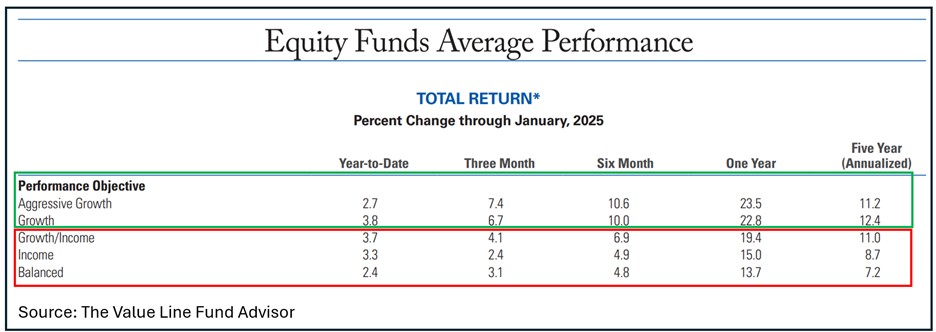

Would you care for just more recent results before allocating your long-term portfolio? Value Line’s equity fund report for various holding periods through Jan. 31, 2025 are listed below.

Pure equity funds (aggressive growth and growth objectives) outpaced the three fund categories that feasted on high-yielding shares only (income funds), balanced funds (50% stocks/50% bonds) and mostly dividend-paying shares (growth and income). Each of the trailing categories focused on total return.

Note that the following results for both stocks and bonds are pre-tax, unlike the NYU numbers which were inflation adjusted.

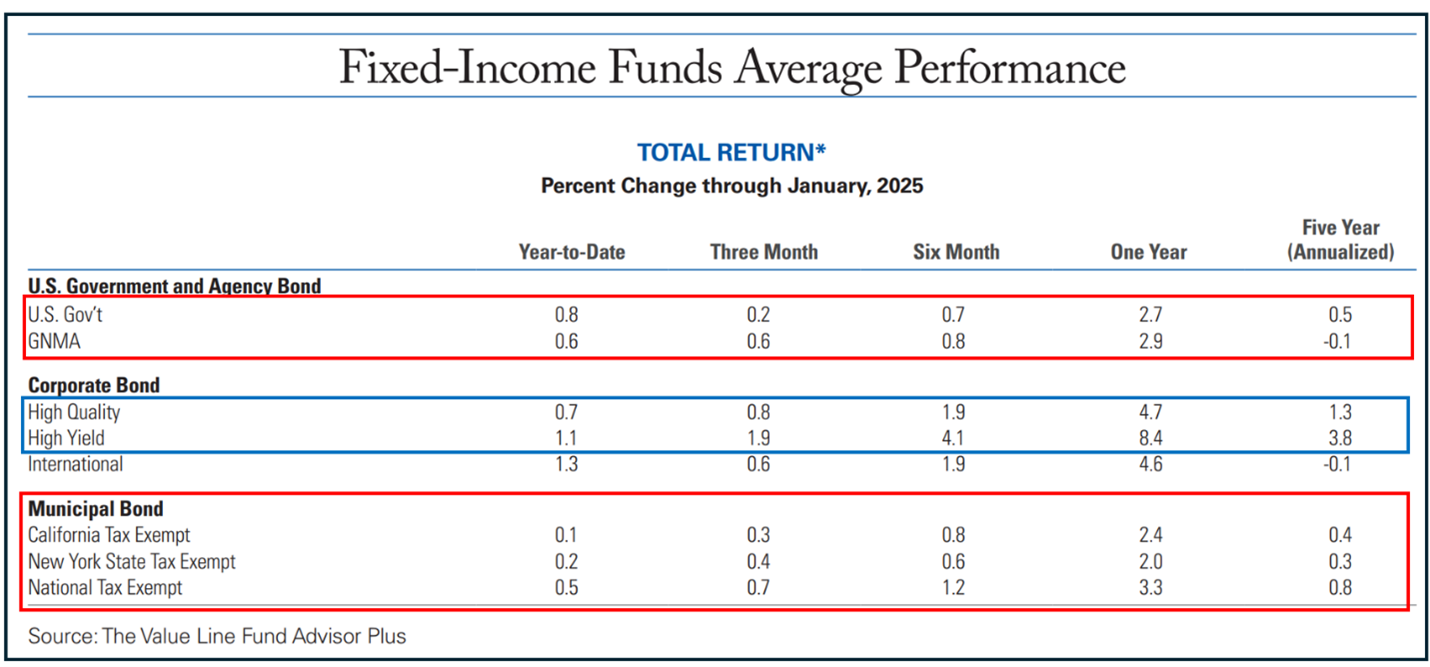

Results from fixed-income funds were putrid over the past half-decade.

10-year maturity Treasury bonds posted just 0.5% annualized returns. Mortgage-backed GNMAs were even worse, at (-0.1%). Nobody should have been happy to have held either of those fund types over those five years.

Investment-grade bonds tallied meager 1.3% annual pre-inflation, pre-tax returns. High-yield bonds (a.k.a junk bond) funds did slightly better but involved more risk. Accepting greater risk often generates better real-world results.

People seeking to avoid taxes think they get great deals on muni bond funds. California residents missed the tax bite but earned only 0.4% annualized over the past five years. New Yorkers out to avoid federal and state taxes fared even worse, at 0.3% annualized.

Subtract inflation from all three muni-fund categories shown and all holders ended up with decidedly less true buying power than they started with over that half-decade.

The most common knock on keeping 100% of your long-term money in stocks is the fear of incurring occasional big declines.

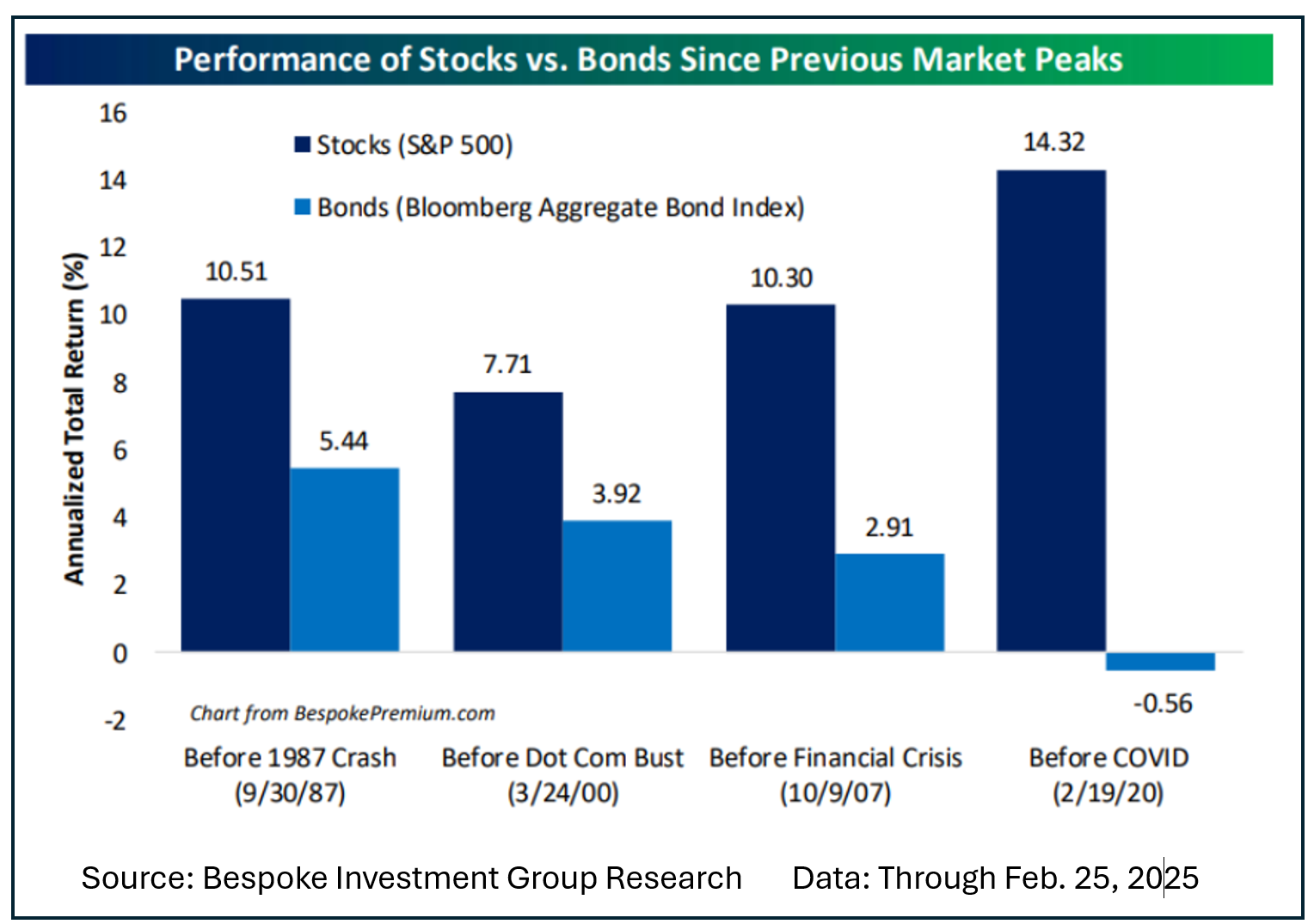

The table below refutes that by showing the S&P 500 total returns for those unlucky enough to invest at the exact worst times since just before the Crash of 1987, when the DJIA suffered its worst single-day percentage decline in history on Oct. 19, 1987.

Continuous holders obtained total returns of 10.51% from Sep. 30, 1987 right through Feb. 25, 2025. That compared with just 5.44% annualized for owners of the bond index who experienced less volatility [but made 48.23% less than equity owners who simply sat tight].

Similar experiences were seen by people with horrible market timing through purchasing just ahead of the dot-com bubble bursting, at the October 2007 market peak or right at the pre-Covid top for the S&P 500 on Mar. 19, 2020.

Those who jumped in just ahead of the Covid panic’s very scary selloff ended up with extremely good gains of 14.32% annualized. Suffering through that major brief, but huge decline paid big rewards to those with the temperament to hang in there when most others would not.

What Are the Lessons Learned From All This?

- There has never been a good reason for keeping any truly long-term money in inferior asset classes.

- The price of real wealth creation over time is the pain endured during the inevitable sharp declines in stocks.

True financial security is never “risk-adjusted.” You can only spend the amount of money accumulated before you retired.

Nobody will offer you discounts on purchases because you chose to forgo trying for maximum total returns.