How to Protect Your Nest Egg Against Market Volatility in Retirement

This simple strategy allows retirees to protect their savings against major fluctuations, maintain their lifestyles and afford health expenses.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Have you ever wondered how to invest your nest egg once you retire to keep yourself from running out of money in your 80s and 90s?

You need the right asset allocation: A mix of stocks, bonds and alternatives to maintain your lifestyle while protecting against inflation, interest rate risk and unexpected health expenses.

So, what’s the ideal investment allocation after you’ve retired? Contrary to some old-school advice, you still need growth.

But you also can’t aggressively trade your way into a secure retirement.

Here’s a look at how the retirement investing bucket strategy works.

Why Do You Need a New Investment Strategy in Retirement?

Can’t you just keep your portfolio as it is and withdraw income as needed?

Well, that depends. The biggest investment risk retirees face today is something called the sequence of returns risk.

This is a phenomenon where the timing of poor investment returns and the size of your withdrawals dramatically impact how long your portfolio lasts.

- Let’s say you retired in 2022 with $1 million and were fully invested in the S&P 500 while withdrawing $4,000 per month ($48,000 per year) to maintain your lifestyle.

- The S&P 500 lost 19% in 2022, meaning you not only lost 19% in market value but also withdrew 4.8% in income, bringing your total decline to 23.8%.

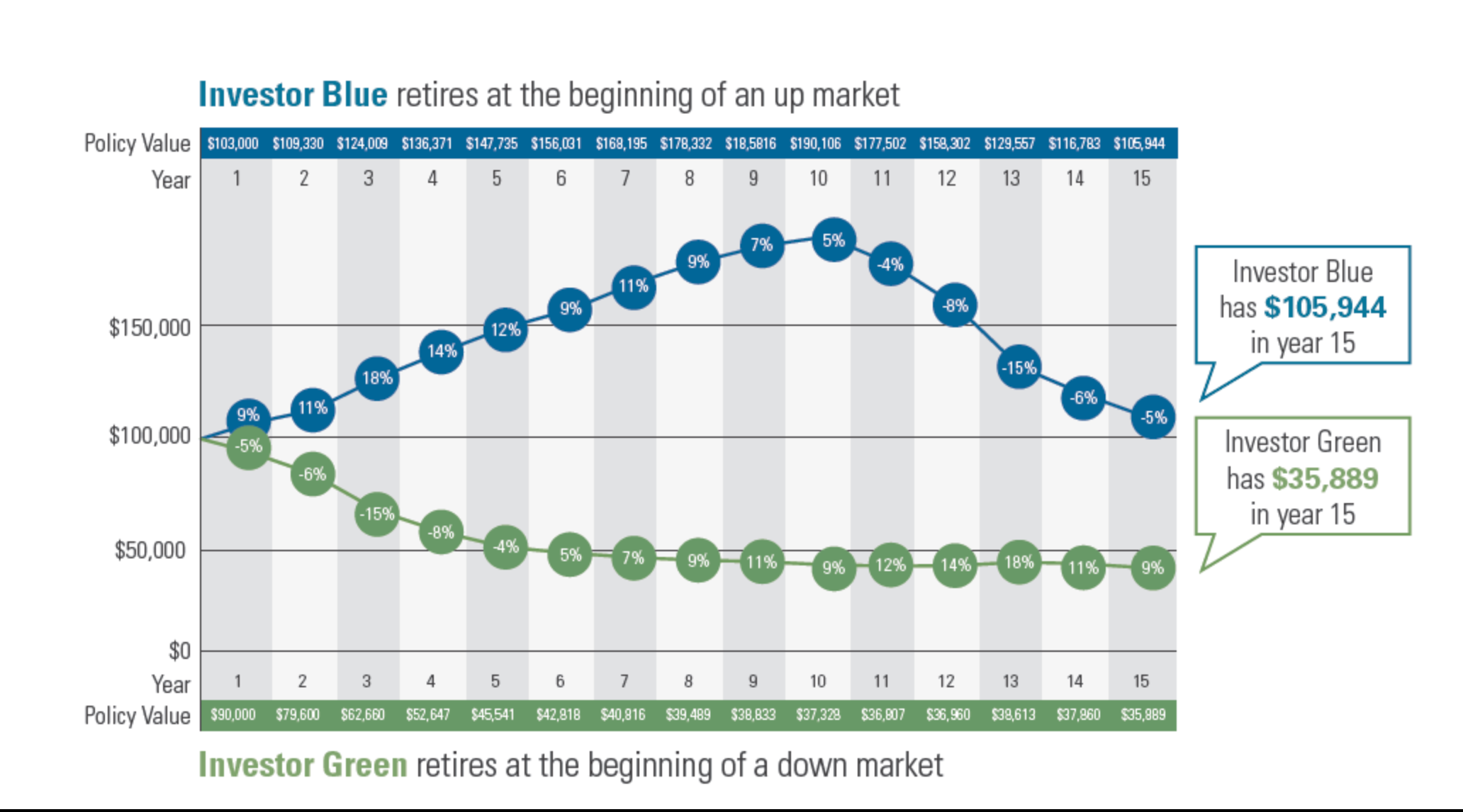

Here’s an illustration from RetireOne showing how that works for an investor who retires at the beginning of an up market, versus one who retires at the beginning of a down market:

If you experience a bad market early in retirement, your chances of running out of money over 20 years are significantly higher than someone who experiences strong early market returns.

Since no one can control market cycles, you need to segment your investments into different time-based buckets to ensure your lifestyle remains protected.

Here’s one way that could work:

The Bucket Strategy for Retirement

There are a few different versions of the bucket strategy, but here’s one that I believe is a sound idea for today’s economic climate. It balances wealth-building potential with income protection.

The strategy is simple: Segment your investable assets into three buckets based on your time frame.

Bucket One: The Green Bucket (Years One to Five of Retirement)

- The goal here is to preserve money with low risk vehicles to meet income needs not covered by Social Security or pensions.

- Invest in low-risk, principal-protected assets, such as:

- High-yield savings accounts

- Treasury bills and bonds

- Fixed annuities

- CDs

- The silver lining of higher interest rates is that these assets now yield north of 4%, more than you would have gotten a few years ago.

Bucket Two: The Yellow Bucket (Years Five to 15 of Retirement)

- This bucket balances growth with safety, giving you steady income along with price appreciation. It includes:

- Treasury bonds and high-quality corporate bonds

- Longer-term CDs and fixed annuities

- Index funds and dividend-paying stocks

- This bucket ensures you have enough stability while still allowing some growth.

Bucket Three: The Red Bucket (15-Plus Years of Retirement)

- This long-term growth bucket is all about building wealth.

- It can be invested exclusively in:

- Stocks (S&P 500, growth funds, value funds or international stocks)

- Real estate investments

- Alternative assets (if appropriate)

- Why 15 years? The S&P 500 has never lost money over any 15-year period in history, giving this bucket time to recover from downturns.

How to Maintain These Buckets

As you spend down Bucket One, the income, dividends and bond coupon payments from Bucket Two will replenish it automatically.

If these yields aren’t enough to fully replace withdrawals, you can:

- Withdraw some principal from fixed assets in Bucket Two while keeping stocks untouched.

- Sell some stocks from Bucket Three every 10 years, allowing the portfolio to grow before trimming positions.

Most retirees should always keep 30% to 40% of their portfolio in stocks at any age. This gives you the potential for growth while also maintaining stability.

Enjoying Retirement Without Stock Market Stress

With this version of the Bucket Strategy, you can confidently fund your retirement without worrying about market fluctuations putting a dent in your ability to pay for your lifestyle.