How Target Date Funds Handle Crashes and Volatility: It's All About the 'Glide Path'

Are TDFs as safe as they claim to be, or could they expose investors to significant risks at the worst possible times? Understanding glide paths is key.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

If you participate in a 401(k) or employer-sponsored retirement plan, you've likely seen Target Date Funds (TDFs) among your investment options.

Designed to streamline retirement investing, TDFs gradually shift from stocks to bonds as you approach retirement.

But how do these funds perform during market crashes and periods of high volatility?

Understanding how TDFs handle market downturns is crucial for anyone depending on these funds for retirement income.

Are they as safe as they claim to be, or could they expose investors to significant risks at the worst possible times?

The Glide Path: Does It Really Reduce Risk?

Glide Path and Risk Exposure

- A TDF follows a glide path that adjusts its asset allocation over time.

- Early on, these funds are heavily invested in stocks for growth, which are riskier but more suitable for younger investors.

- As the target retirement date approaches, the fund shifts toward bonds to reduce volatility.

Market Crashes and Near-Retiree Risk

- During a market downturn, this transition to bonds should help protect near-retirees.

- But some TDFs remain too aggressive too close to retirement, exposing investors to unexpected losses.

Performance in Different Market Conditions

- In a bull market, TDFs with a heavier stock allocation tend to outperform their peers.

- During a sharp stock market pullback, some investors may be gobsmacked to find their "safe" phase is still pretty risky.

What TDFs Are Designed to Do

TDFs are designed to simplify retirement investing by automatically adjusting their asset allocation as the target retirement date approaches.

But, not all TDFs are created equal, especially when it comes to handling market crashes and volatility.

Here are some popular fund families’ TDFs, showing how their glide paths can influence performance during market volatility.

1. Vanguard Target Retirement Funds

Vanguard's TDFs start with a 90% equity allocation, which gradually decreases to 50% at the target retirement date.

After retirement, the stock portion continues to fall, reaching about 30% seven years after retirement. This is called a “through" glide path strategy, which aims to balance growth potential with risk reduction as investors age.

Here's a look at Vanguard's glide path.

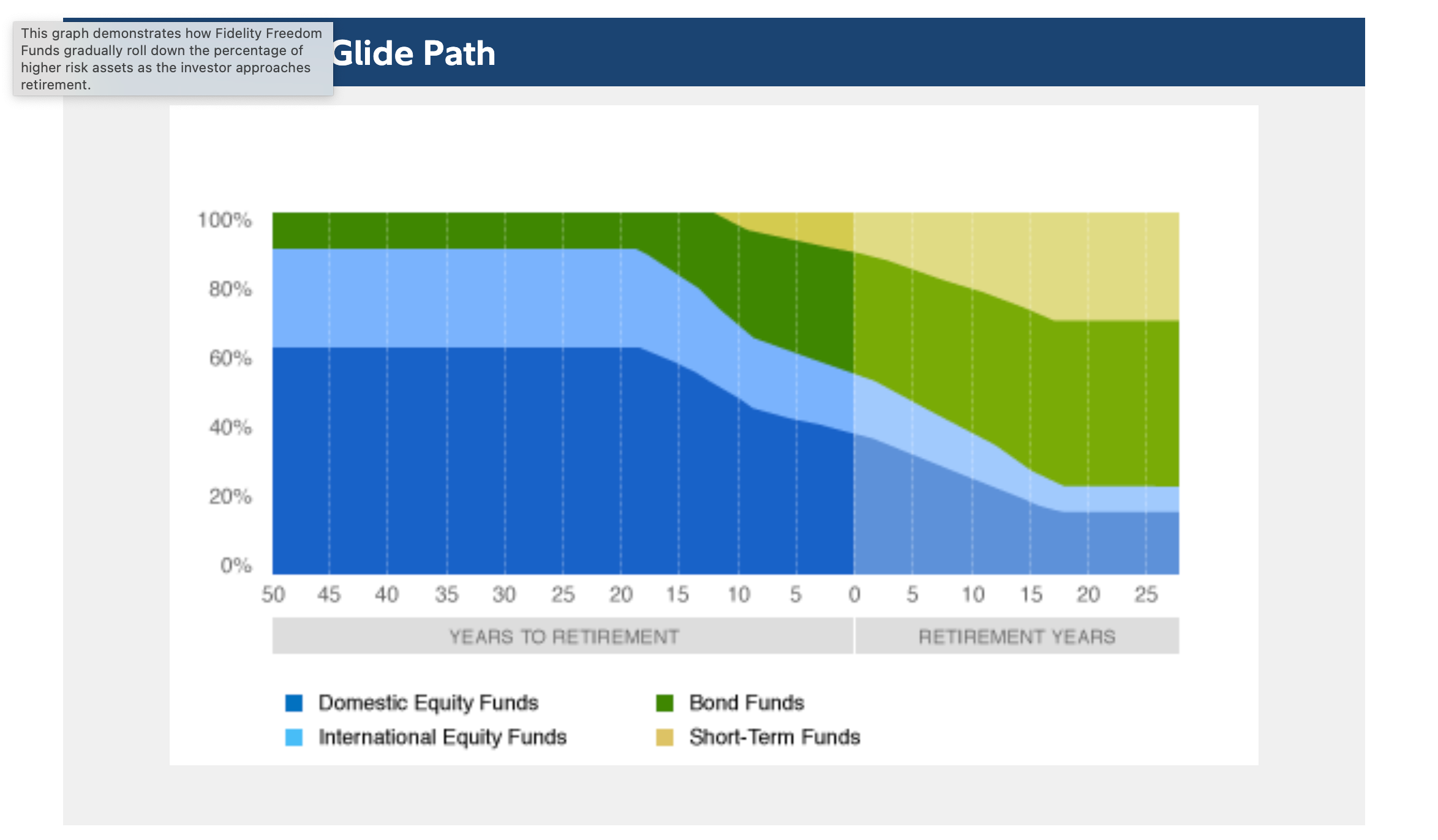

2. Fidelity Freedom Funds

Fidelity offers several TDF series, including the Fidelity Freedom Funds, which are actively managed, and the Fidelity Freedom Index Funds, which, as the name suggests, are passively managed.

Both series use a "through" glide path, starting with approximately 90% in equities and reducing to about 51% at retirement.

The stock allocation continues to decrease for about 18 years post-retirement, eventually settling at around 19%.

Here's the glide path for Fidelity Freedom Funds.

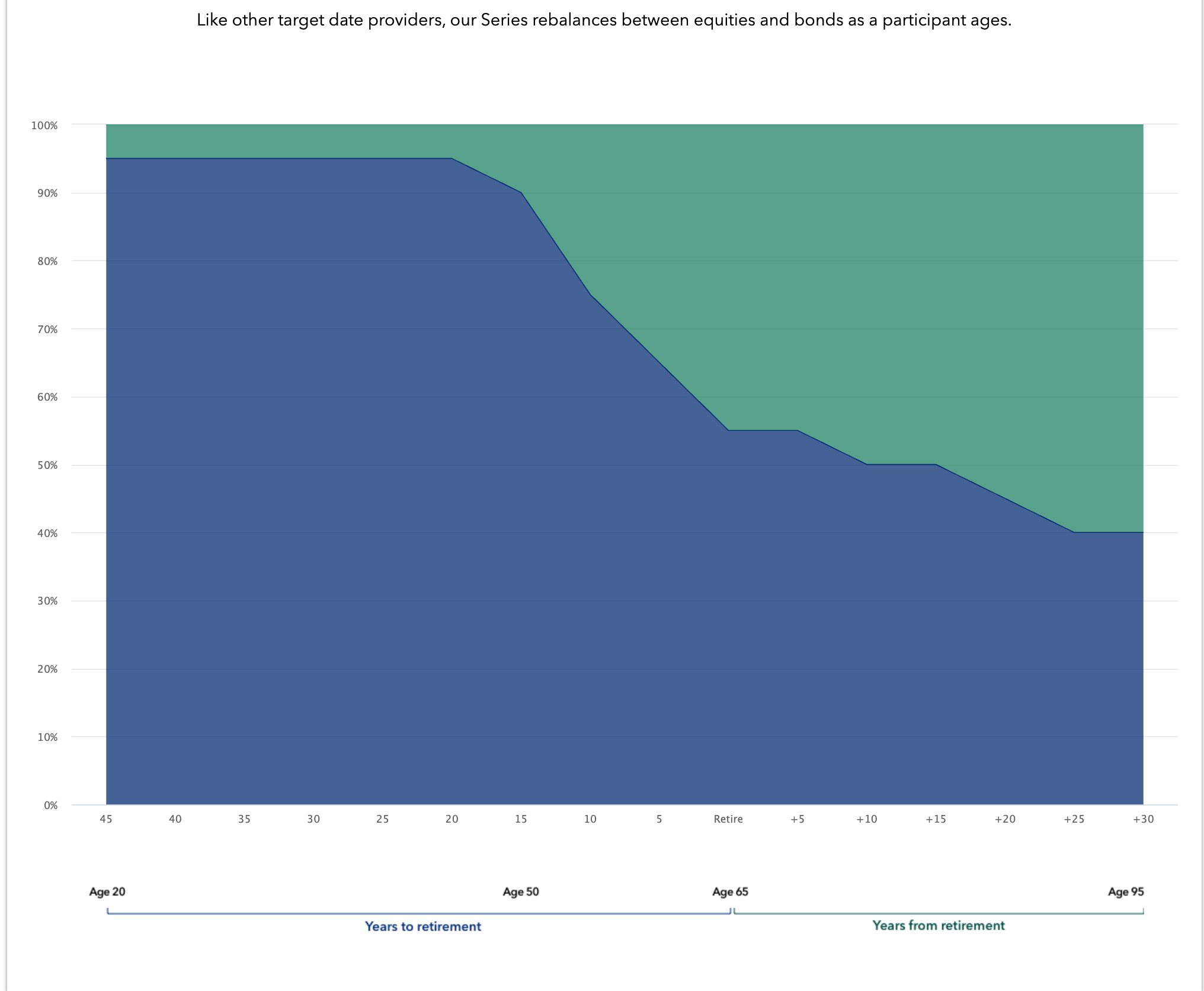

3. T. Rowe Price Target Retirement Funds

T. Rowe Price's TDFs are known for their more aggressive approach, starting with an equity allocation as high as 98% for younger workers.

At the target retirement date, the equity sleeve is about 55%, and it continues to decrease after retirement, reflecting a "through" glide path strategy.

Because they tilt more toward equities than other TDFs, T. Rowe Price’s funds often outperform others in a market uptrend. That makes them more risky in a downturn, though.

Below is the T. Rowe Price TDF glide path.

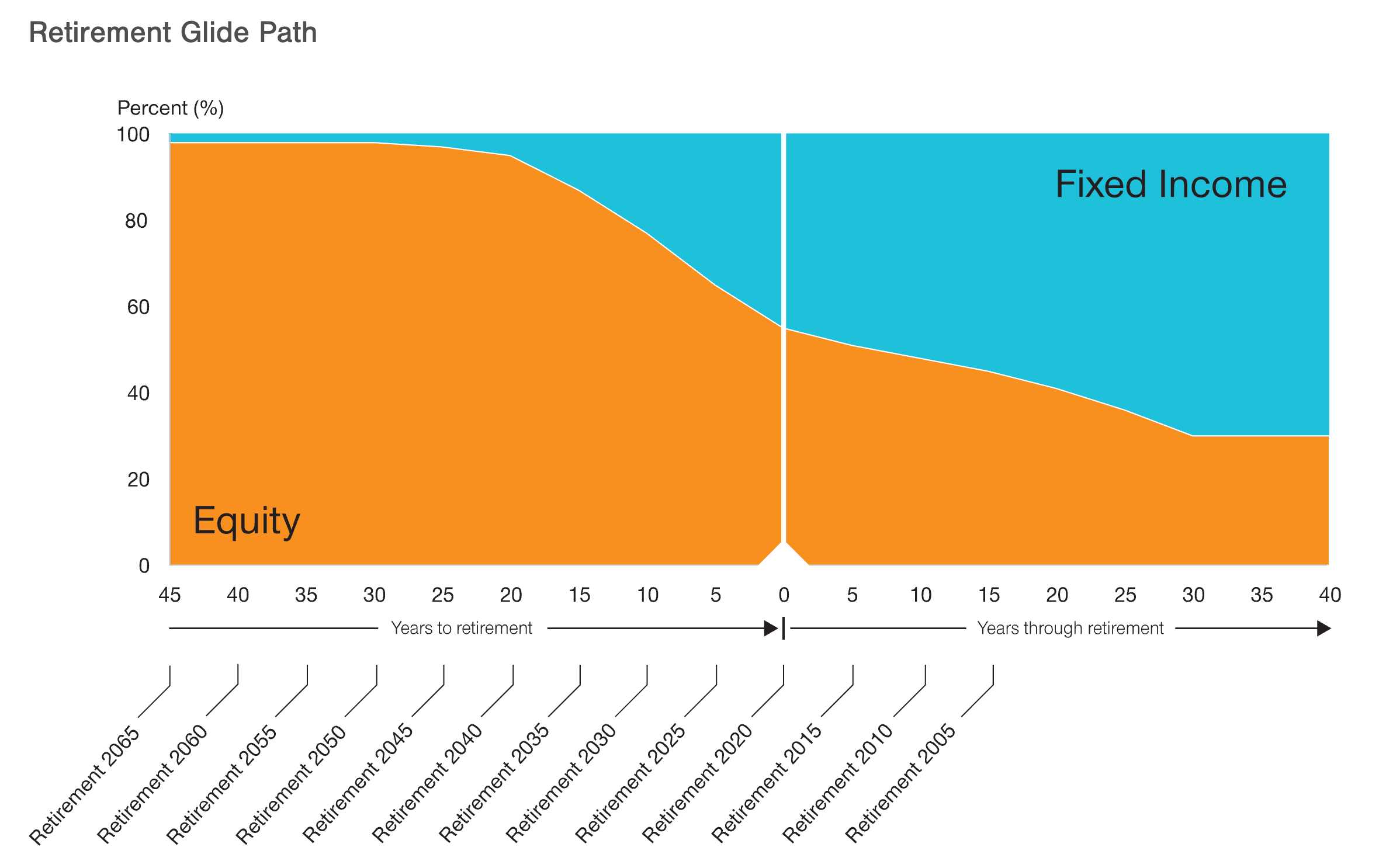

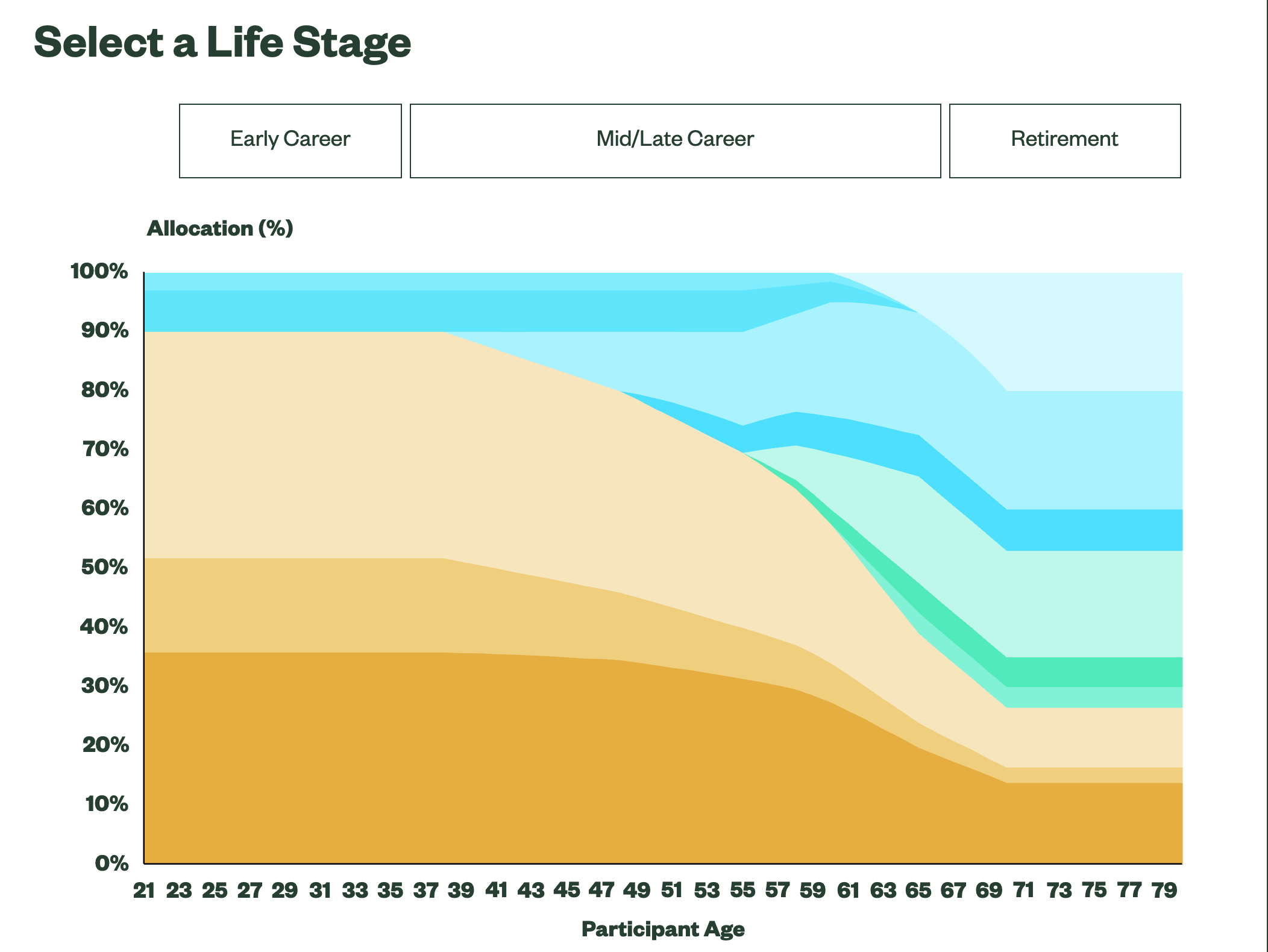

4. American Funds Target Date Retirement Series

American Funds' TDFs begin with a 90% equity allocation, which decreases to 45% at retirement and gradually reduces to 30% in retirement.

This glide path is designed to balance growth and capital preservation, aiming to provide investors with a smoother transition into retirement.

Here's the American Funds glide path as investors approach retirement. The green is fixed income and the blue is stocks.

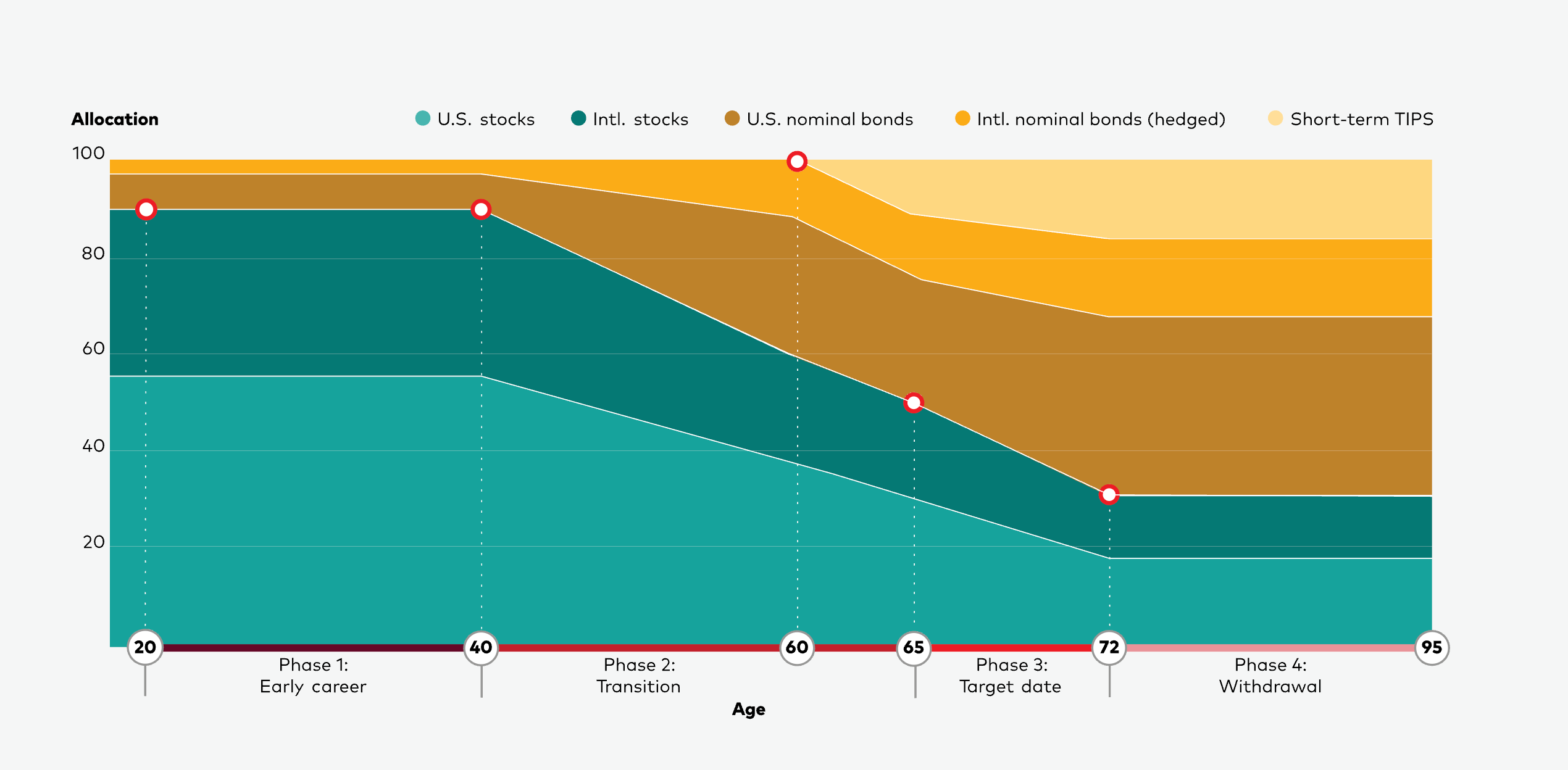

5. State Street Target Retirement Funds

State Street's TDFs start with a 90% allocation to growth assets, including U.S. and international equities.

At retirement, which for these purposes is assumed to be age 65, the allocation to stocks decreases to approximately 47.5%. Growth assets here also include real estate investment trusts (REITs) and commodities.

The glide path reaches its most conservative point at age 70, with about 35% in growth assets.

You can see how that looks here.

Impact of Glide Paths in a Downturn

As you might expect, the precise glide path of a TDF affects its performance during a downturn.

Funds with higher equity exposure near retirement may experience greater losses during market crashes but also have higher growth potential.

On the flip side, funds with more conservative allocations may offer protection during downturns but might not keep pace with inflation over the long term.

For instance, during the brief Covid-induced 2020 market pullback, long-dated TDFs (target date 2045 and beyond) saw losses between 30% and 35%, while 2025 funds, designed for those nearing retirement, lost between 20% and 25%.

Those funds did their jobs. Investors with a longer time horizon can take more risk with stocks, since they have a longer time to make up for losses.

Buyer Beware

It’s not all sunshine and roses with target-date funds.

While convenient, these vehicles have some notable drawbacks.

For example, they often lack customization, potentially misaligning with individual risk tolerances and financial goals.

Higher fees compared to other investment options can erode returns.

Also, their standardized glide paths may become too conservative too quickly, potentially impeding growth for longer retirements.

But wait, there’s more:

Some TDF sponsors bundle their own underperforming or expensive proprietary funds within their investment mix.

This practice can lead to higher fees and suboptimal performances. If you work with an advisor, ask him or her to evaluate your target-date fund to determine whether there might be a better option.

How to Evaluate a TDF

- Equity Allocation Near Retirement: Higher stock exposure near retirement can lead to higher volatility. Be sure to understand if your TDF aligns with your risk tolerance and time horizon.

- Fund Management: Understand whether the fund is actively or passively managed, as this impacts fees and potential returns.

- Performance During Downturns: Review how the fund has performed during past market downturns to gauge its resilience.