Has Your Portfolio Gone Adrift?

Let's talk about why you should rebalance your portfolio and the best ways to do it.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

So, your portfolio's all set up, nicely organized with various asset classes represented to create just the right balance of risk and return.

What now?

You might think the hard part (or the fun part, depending on how you look at it) is over.

The trickiest part may be resisting the urge to tinker with your retirement account, adding this, subtracting that, trying to time your exposure to gold or that crypto ETF.

But that ignores the one thing that actually matters: periodically resetting your portfolio percentages back to your original intent.

The fancy term for that is rebalancing, and it's a critical part of having a healthy, diversified portfolio.

How It Started, How It’s Going

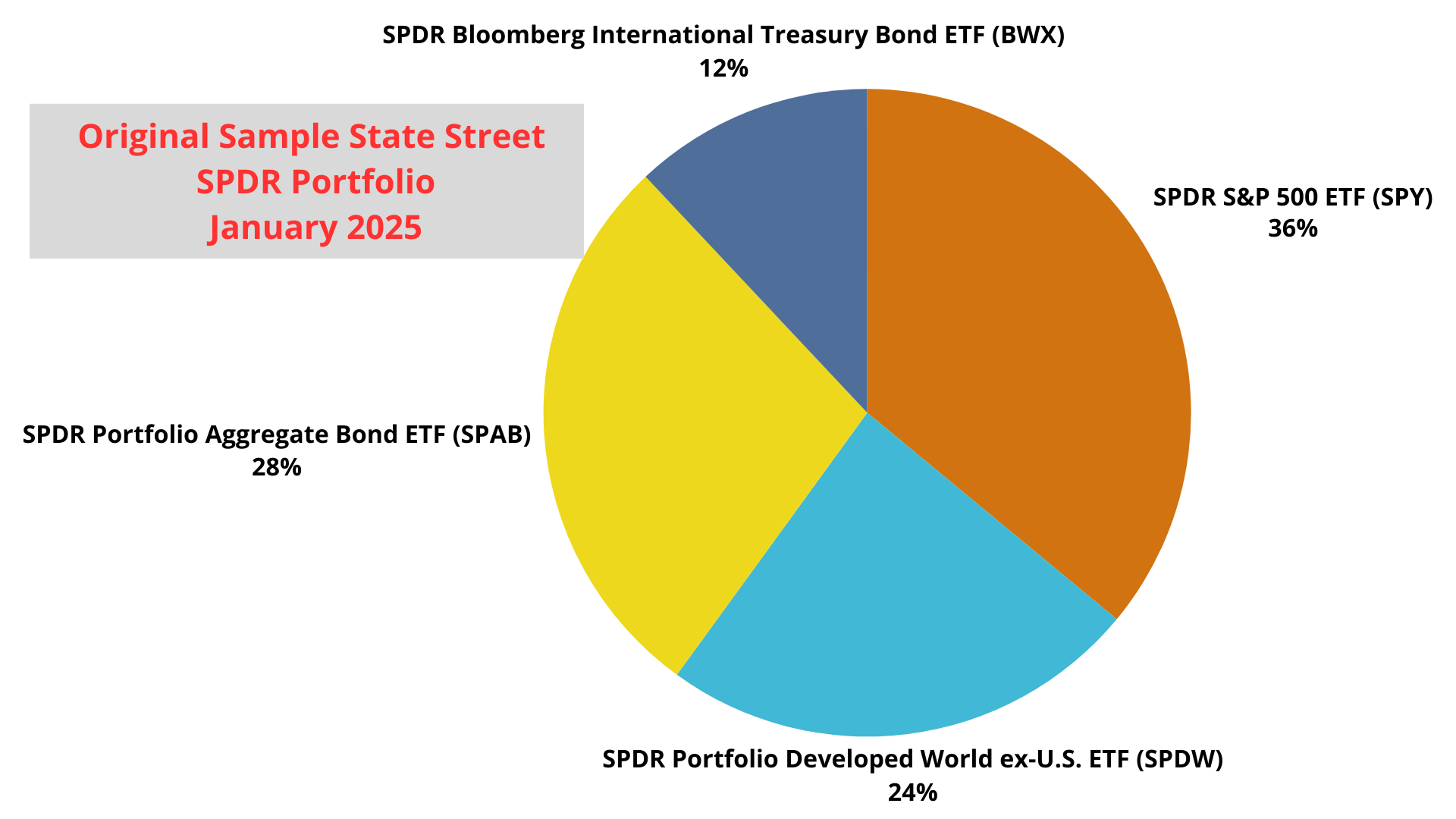

Here’s the 60% stocks, 40% fixed income allocation I developed for last week’s article on using State Street ETFs to construct a balanced portfolio.

- 36% SPDR S&P 500 ETF (SPY): Broad U.S. equities

- 24% SPDR Portfolio Developed World ex-U.S. ETF (SPDW): International equities for global diversification

- 28% SPDR Portfolio Aggregate Bond ETF (SPAB): Core U.S. bonds for stability and income

- 12% SPDR Bloomberg International Treasury Bond ETF (BWX): International government bonds from developed markets

Let's say you implemented that on January 2, 2025. You’ve had a good year, with each of those investments posting gains!

But they haven't all gained equal amounts, so your portfolio allocations will have drifted.

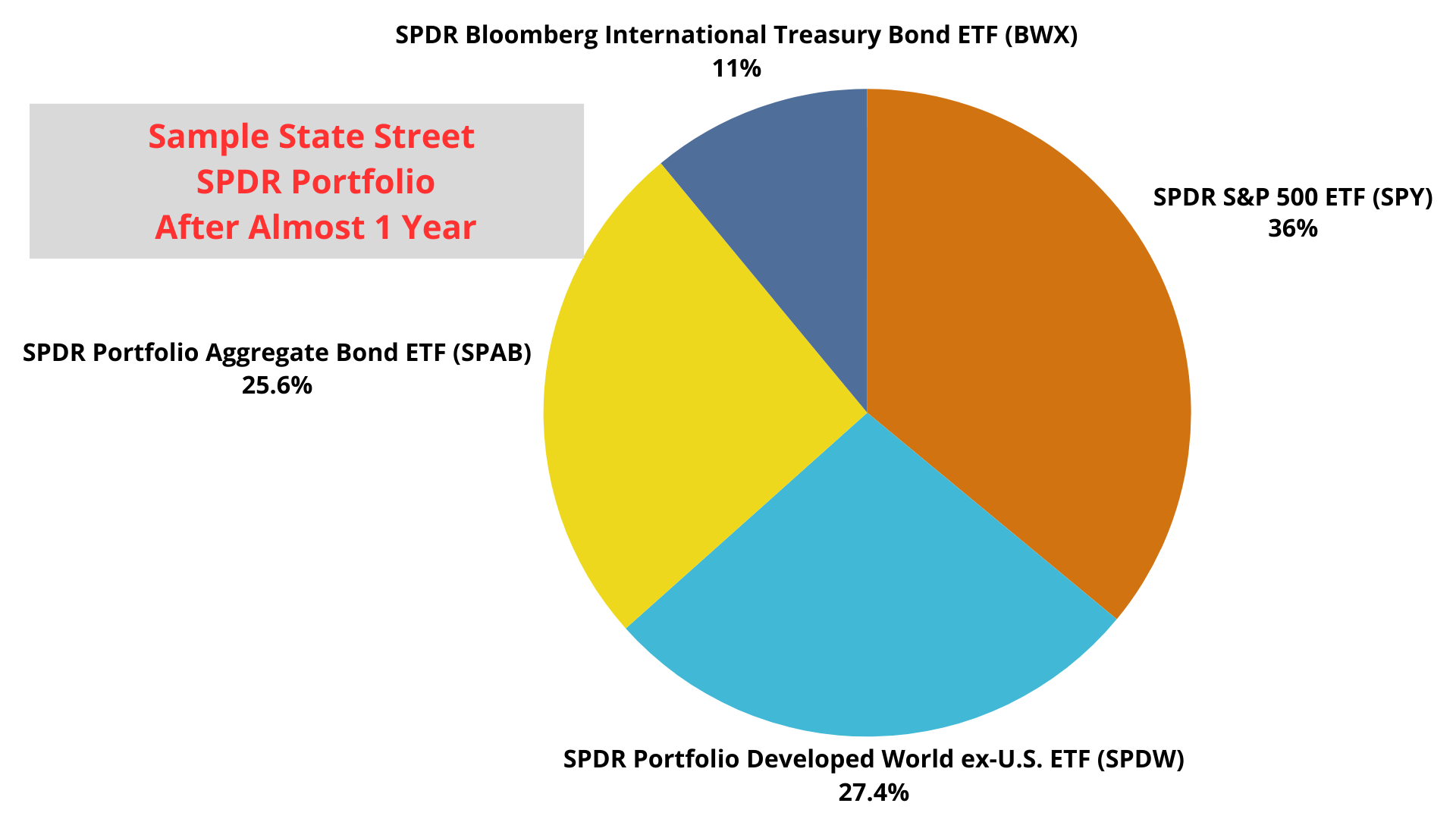

As of December 16, your portfolio allocations look like this:

- 36.0% SPDR S&P 500 ETF Trust (SPY)

- 27.4% SPDR Portfolio Developed World ex-U.S. ETF (SPDW)

- 25.6% SPDR Portfolio Aggregate Bond ETF (SPAB)

- 11.0% SPDR Bloomberg International Treasury Bond ETF (BWX)

Your portfolio started the year with 60% allocated to stocks and 40% to bonds, but is now about 63% stocks and 37% bonds.

No, the percentage allocations haven’t changed much, and depending on the bands you set for rebalancing, you may not have take action yet.

But if you ignore your account indefinitely, there could be adverse consequences.

Over the past 30 years, rebalancing hasn’t had the widespread effect of increasing overall returns because you're effectively selling your winners to buy more of the laggards.

However, and this is the key, rebalancing your portfolio should lower your risk to keep you out of trouble. And that's the goal, right? To stay on track so you can stop working one day.

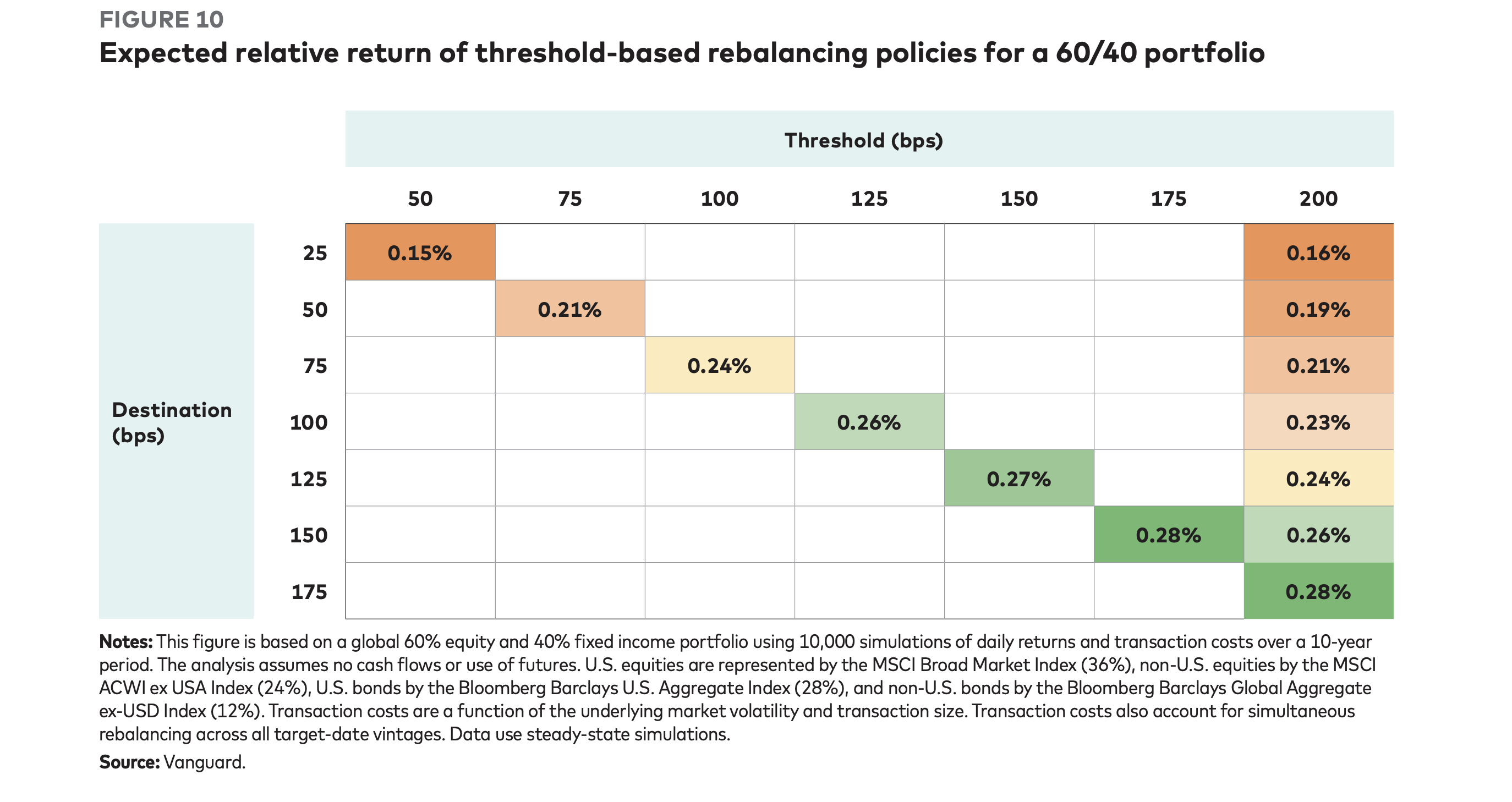

This chart from Vanguard shows that the cadence of rebalancing is just as important as whether investors rebalance at all. It compares how much portfolio drift an investor tolerates before rebalancing (horizontal x-axis) with how aggressively the investor rebalances once they do act (vertical y-axis).

In other words, you should rebalance when your portfolio drifts by a meaningful amount rather than on a fixed schedule. That way, you get better results by reducing unnecessary trading costs.

That approach strikes a balance: It keeps risk from drifting too far from the initial target while avoiding overtrading. That can improve long-term returns.

Portfolios Are Not Static

But here’s a common mistake many financial writers make when analyzing the need to rebalance: They assume no additional dollars are invested into a portfolio, or that none are withdrawn. That’s not usually how things work.

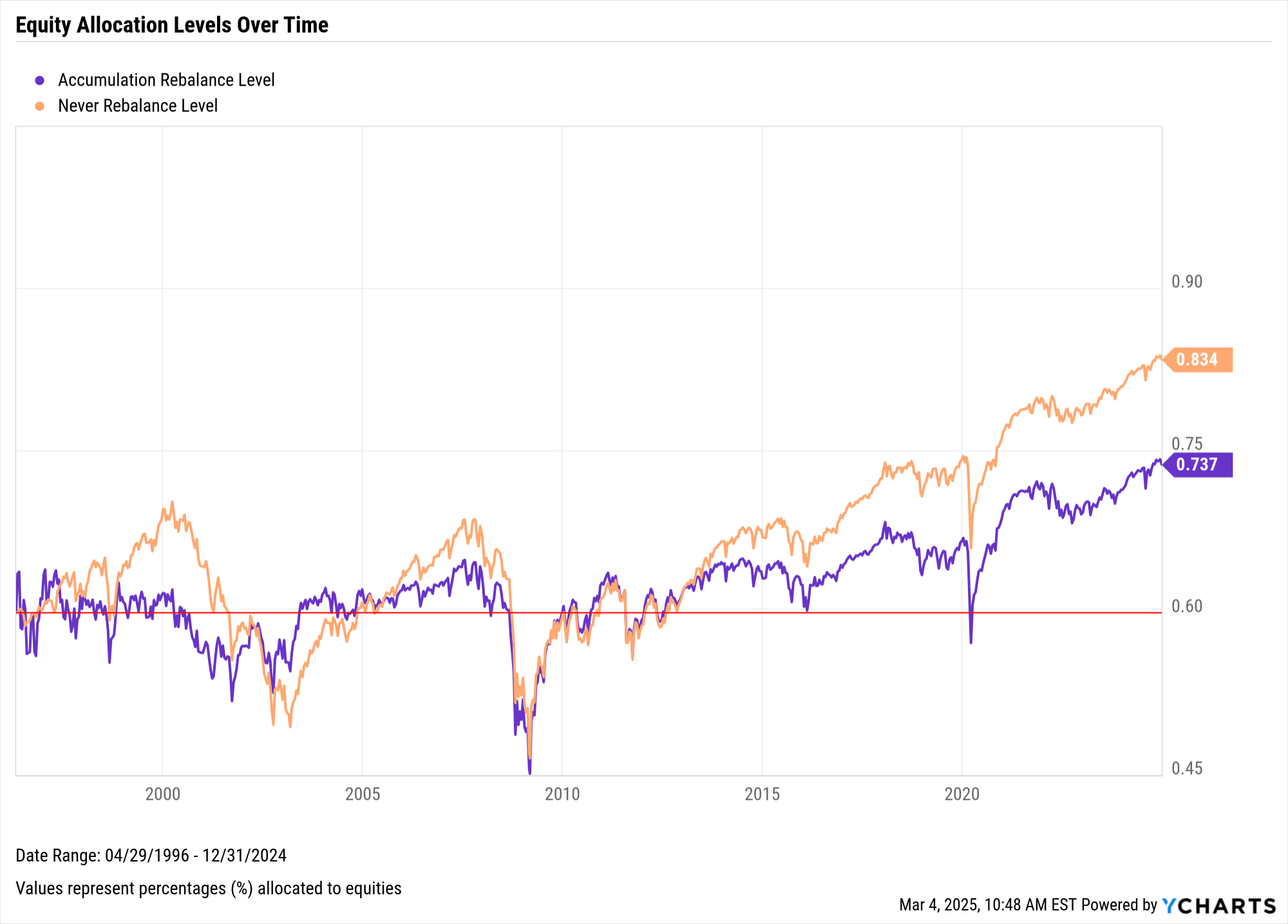

According to YCharts, for people who are adding money to their portfolios over time, a better way to rebalance is by directing new funds to the most underweight assets.

This is called an accumulation rebalance. You can particularly see the benefit in a taxable account, as it allows you to keep the portfolio closer to its target allocation without triggering the tax consequences of selling.

In other words, rather than selling stocks to buy bonds, you might simply direct new investments to purchase only the underweight asset and move the whole shebang back to the original target allocation. See? You're accumulating the stuff you were underweight.

This image from YCharts illustrates how that would have looked when implemented between April 1996 and December 2024.

Rebalancing isn’t about finding one “perfect” rule. Instead, it’s about managing the various elements of performance, risk, costs, and investor comfort. Over time, strategies that rebalance less frequently tend to outperform those that rebalance too often, mostly because overtrading erodes returns and reduces risk-management benefits.

At the same time, never rebalancing can allow portfolios to drift in ways that miss long-term growth or stray too far from the originally intended risk levels.