Earny Asks: How Can I Get Free Money in My 401(k)?

Use this simple trick to get free money in your 401(k) account.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Avoiding the easiest mistake in investing

Earny and I spent last weekend in Bloomington, Ind., where we saw the Hoosier football team trounce Indiana State 73-0. I won’t say it was a good game, even if our team won. We made some new friends, however, and had a chance to talk to lots of students. Many were college seniors who were excited to launch their careers upon graduation.

(If you’re hiring, I know of some great people. Email Earny here and I’ll put you in touch!)

This is an exciting time for them. But they’re anxious. The job market is tough, and the trend doesn’t seem to be in their favor, at least not in the short term. Don’t worry, Hoosiers! Tough times are usually followed by good times. Keep at it and you’ll find yourself in a fulfilling career.

The other cause of their anxiety was retirement savings. In fact, one of Earny’s new friends, let’s call her M, asked “what’s the biggest mistake that new investors make?”

I'll answer that one, but I'm going to go a step further and answer Earny's question: How can many people get free money in their 401(k) accounts?

The Answers

If you’ve been reading Filthy Rich Animal since the beginning, you probably already know the answer. The biggest investing mistake is not getting started early.

We’ve already written about that point in these articles:

Our first Filthy Rich Animal article was about how Investing is rigged (in your favor). It makes the case for why you need to be an investor (so you can afford nice things in retirement) and how the market makes it possible because investments go up in value over the long run.

That’s just part of the story. Compound growth is the other part; it's the magic that has allowed vampires to become so incredibly rich.

So, yeah, the market is rigged in your favor, and over time compounding enables your money to grow like it's turbo charged.

I think the students understand that. In M’s case she’s studying business, and this is the kind of stuff I lectured about in my Intro to Finance classes at CU Boulder. Let's Go Buffs!

So, start early but get that 401(k) match!

It's easy to tell people to start early. But we need to be more specific. So, since these Hoosiers (as well as my CU Buffs!) are about to move on to great careers, Earny and I think it's important that they take advantage of their new employers' 401(k) plan offerings.

A 401(k) is a retirement plan that employers offer. There are two versions. a regular 401(k), where you invest pre-tax income today and pay taxes on the investments when you retire; and a Roth 401(k), where you pay the taxes today and withdraw funds tax-free at retirement. We’ll discuss that in more detail another time.

Once the money is in your 401(k), you get to invest it, usually based on a menu of choices that your employer has selected. Again, future Filthy Rich Animal articles will elaborate on this.

Meantime, your HR department will sign you up for your 401(k). But make sure this happens. Don't put it off.

And this is the important part: Don’t forget to get the match. Most employers match your investments up to a certain point. It’s literally free money. Kate also discussed it here, along with two other mistakes some investors make.

Here’s how it works (your plan may differ):

Employers usually will match between 3% and 6% of your salary. It’s a match, which means that you have to invest at least that much. For example, if your employer matches as much as 5% of your salary and you invest 10% of your salary into a 401(k), your employer will kick in 5%. It's like you've invested 15% but had to lay out only 10%.

BUT: If you invest only 1% of your salary, your employer will kick in only 1%. So, that's like investing just 2%. You'll thus miss out on lots of free money! And your retirement savings won't grow nearly as quickly.

You’re allowed to invest up to $23,500 per year in your 401(k), according to current regulations.

Here’s an example:

Let’s say you earn $100,000 per year (to make the math easy!). And you decide to put 10%, or $10,000, into your 401(k). You employer matches the first 5% of your salary that you put in, so it adds another $5,000. Bam! You’ve got $15,000 to invest.

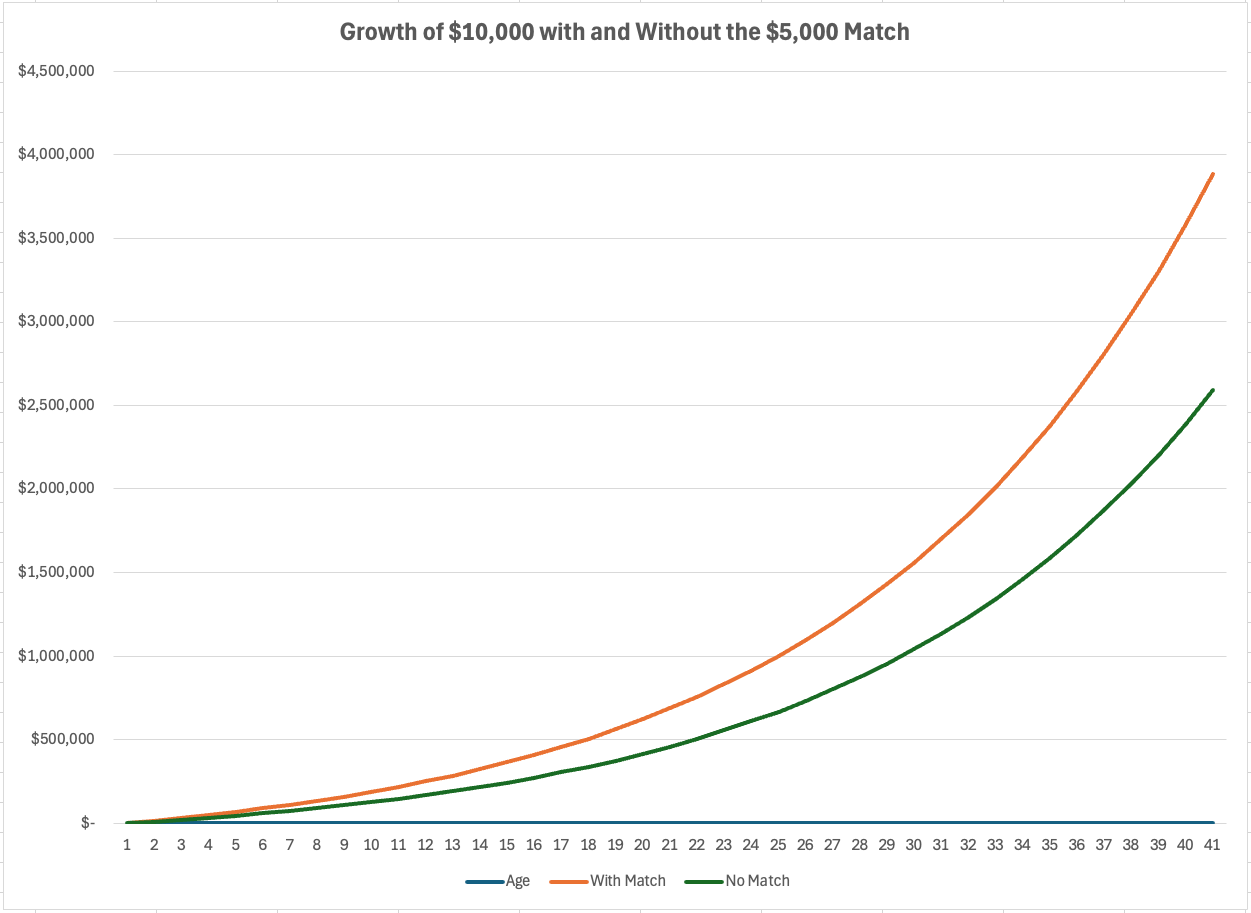

That’s powerful. Here’s a chart showing how much your 401(k) would be worth with and without the match.

If you invest $10,000 annually for 40 years and earn the long-term average of 8% that the S&P 500 has traditionally returned, you’ll end up with $3.9 million if you get that employer match of $5,000 vs. just $2.6 million if you don’t get the match. The difference between getting that match and not grabbing the match is $1.3 million!

Look, you’ll automatically get the match if you invest enough. But my point is that you should not wait. Waiting is the mistake. Your employer is literally giving you a 100% return on the funds that it matches.