Consider Location as Much as Allocation

What you own matters. Where you own it is equally important.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

"You can't predict, but you can prepare.”

Howard Marks, founder, Oaktree Capital

Sure, AI is the shining theme of the moment. Elsewhere, I recently wrote about drone stocks, collectively forecast to grow at a rate of about 17% in the next decade.

There are plenty of investing themes, but when looking out at the horizon of your lifetime, there are some strategic decisions you can make that go well beyond picking hot stocks.

I know that for many, a balanced portfolio seems like something for those who don’t understand trading. But I’ve seen enough high-risk trading accounts go south, leaving the owners scrambling to make up for lost time, just when they are thinking about retiring. (Note to younger investors: That time will arrive before you know it.)

It’s Not What You Make; It’s What You Keep

It’s never too early to start considering how you’ll fund your future lifestyle, and what financial resources you’ll have available.

- Focus on after-tax, after-fee returns. A 9% fund return means less if taxes, turnover and high expense ratios chip away at 2% to 3% of that return each year. Use low-cost index ETFs and tax-efficient accounts to boost the compounding effect for you, not some fund manager.

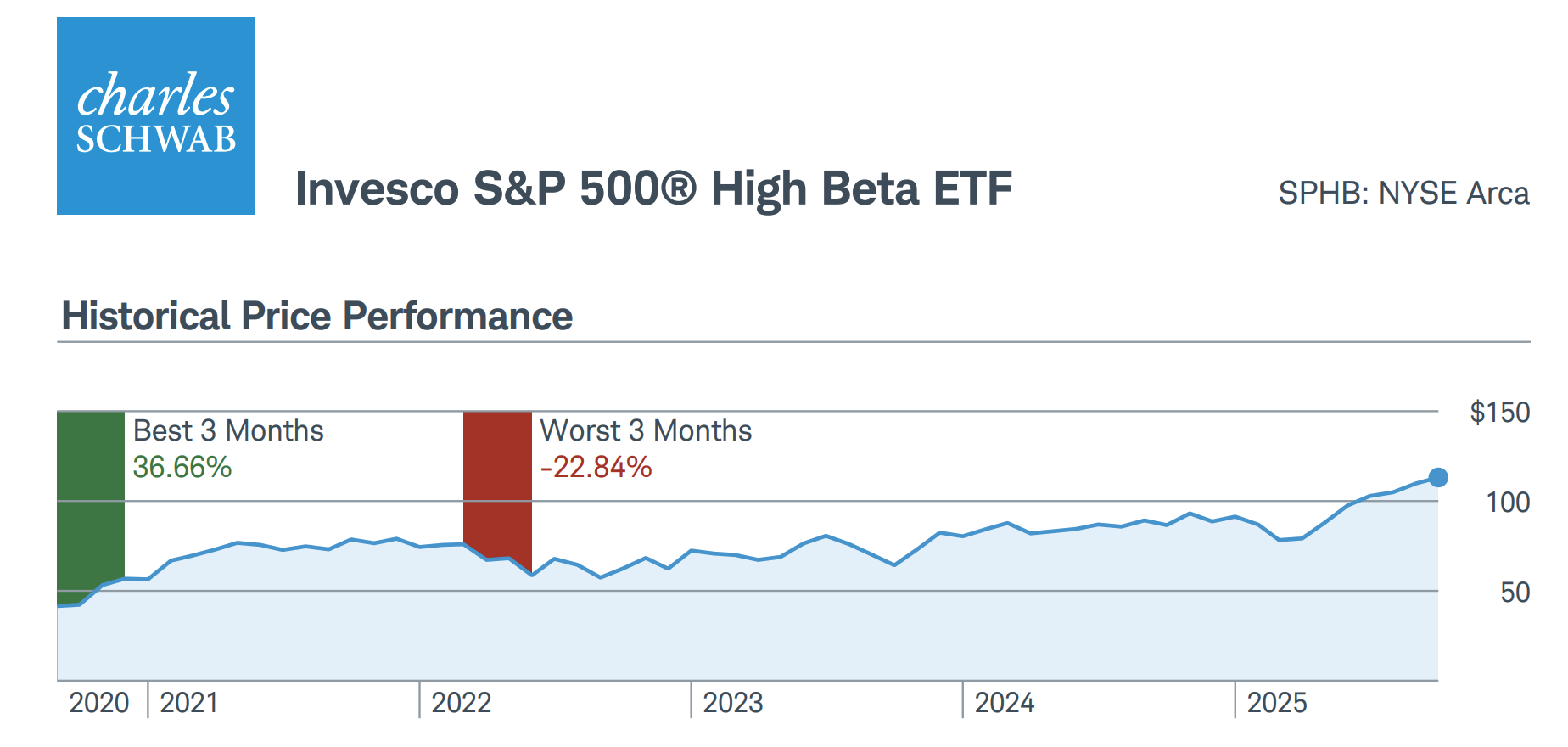

- Higher risk doesn’t mean “better.” Let’s look at the Invesco S&P 500 High Beta ETF (SPHB). It tracks the most volatile S&P 500 stocks, amplifying market moves up and down for investors seeking higher risk and potential reward.

SPHB has shown severe downside risk: Its worst three-month stretch resulted in a decline of 22.84%, underscoring high-beta drawdowns.

- Remember to offset risk. In and of itself, a three-month drawdown of 22.84% for one investment isn’t the end of the world, especially if you’re years away from needing to start taking income. However, if that risk isn’t balanced with a less volatile asset, it could spell trouble.

- Single stocks magnify volatility and shrink compounding. Here’s an example that happens more often than it should: A trader buys a volatile stock, sells for a quick gain, and immediately owes short-term taxes, assuming this is in a taxable account, not an IRA. If there's a loss, there may even be a violation of the wash-sell rule. Re-entering the trade later, they own fewer shares when the big rally comes. Despite “winning” trades, they end up with less wealth than a long-term investor.

It’s OK to Own Risky Assets As Part of A Plan

I say this pretty much every week, but I’m not against owning individual stocks. I had a client who just loved Apple (AAPL) products. He enjoyed owning the stock and after he retired (fairly young, in his mid-50s), he took a job at an Apple store just for fun.

But he had salted away money for years in a 403(b) from his most recent job, and in various 401(k)s before that, and was always very careful about not spending more than he made. For the record, this guy wasn’t Scrooge; he took plenty of vacations and was an avid skier. The point is: He wasn’t betting on that bushel of Apple shares to fund his future retirement.

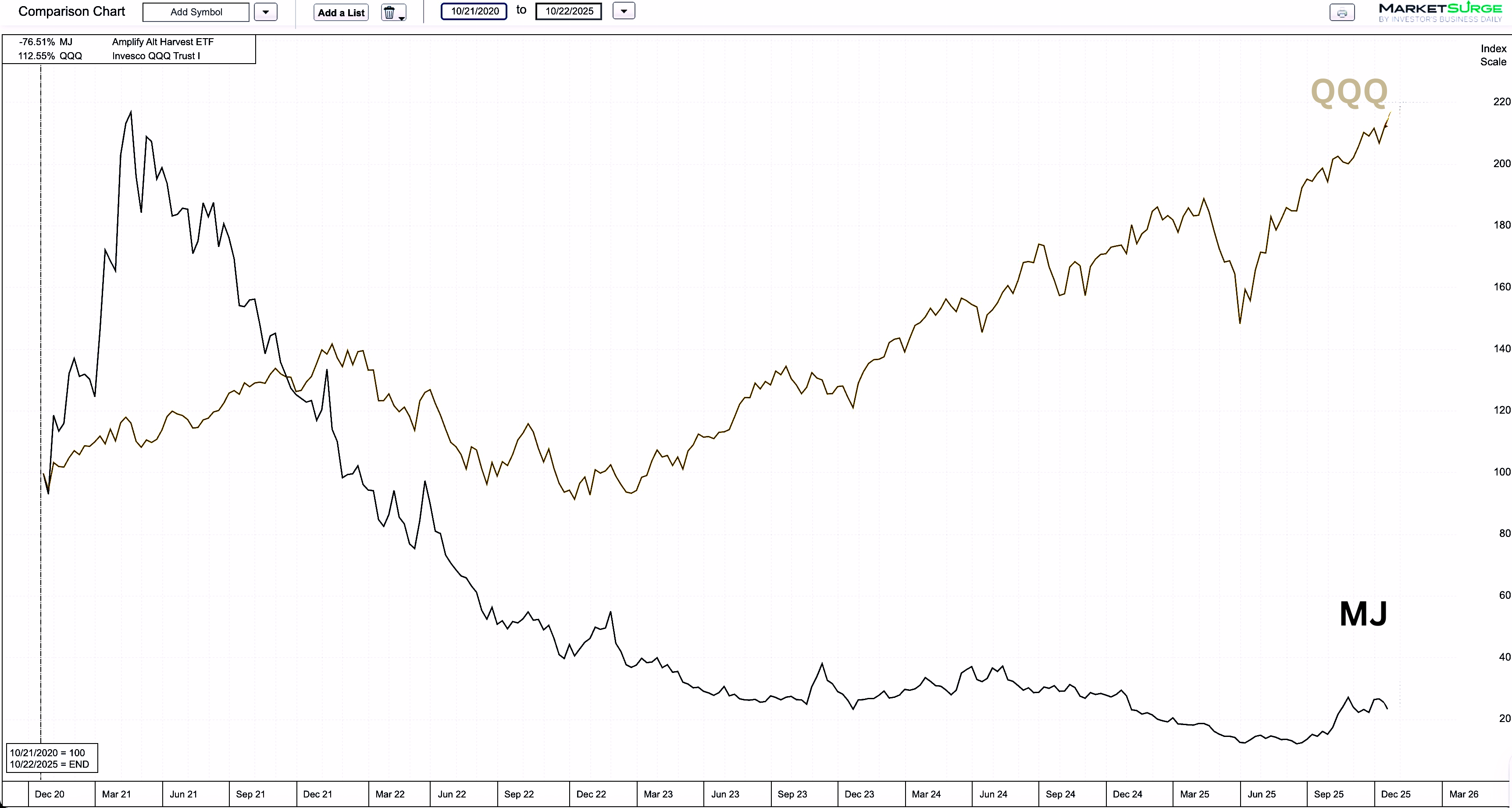

Sadly, I’ve seen others make the mistake of betting on high-risk stocks or trendy ETFs. Remember the cannabis-stock craze from a few years ago? Here’s how the Amplify Alternative Harvest ETF (MJ) got smoked by the Invesco QQQ Trust Nasdaq 100 ETF (QQQ) in the past five years.

Theme investments generally have a limited shelf life and shouldn’t be considered the ticket to buying that retirement yacht.

Asset Location, Not Allocation

At first glance, parking single stocks in an IRA sounds smart: No taxes on capital gains or dividends.

Counterintuitive as it may seem, a taxable account often works better for volatile, concentrated positions. You can harvest losses when a stock crashes, choose which lots to sell to manage the size of a gain, hold for a longer period of time to take advantage of more favorable long-term rates, and even donate appreciated shares or gift them to lower-bracket family members.

None of this works the same way (or at all) inside an IRA.

In other words, for single-stock ups and downs, taxable accounts give you the levers that actually protect what you keep.

Use asset location to match each account type with the right investments:

- Tax-deferred (401(k), traditional IRA): Bonds and REITs, since income will be taxed later anyway. If you have high-turnover active funds, this is the place for them.

- Roth IRA: Highest-growth assets, like total-market or small-cap ETFs. You’ve already paid the taxes here, so you can get tax-free growth.

- Taxable: Single stocks, low-turnover ETFs where you can harvest losses, manage gains, and make tax-smart decisions over time. If you're in a higher tax bracket, you could put municipal bonds here.

Your Future Self Will Thank You

Future-proof investing isn’t about finding the next big thing. It’s not that exciting - at least not in the moment. It’s about aligning your assets with your time frame, taxes and temperament.

Your goal shouldn’t be to beat the market. It’s should be to design a portfolio that funds your best life.