Can Target Date Funds Put Your Nest Egg at Risk?

Set-and-forget funds may not be the right choice as you approach retirement

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The appeal of target-date funds is easy to understand. You put your retirement funds on “set and forget,” with the notion that you’re taking the appropriate amount of risk while simultaneously getting the growth you need for retirement, at a specified future date.

Target-Date Funds: A Solid Start

When you signed up for your company’s 401(k), you may have been assigned to a target-date fund by default. These funds, offered by numerous investment managers, provide a diversified portfolio that adjusts its asset allocation based on the investor's retirement timeline.

This makes them a relatively easy and hands-off option for those who may not have a strong investment background or prefer a more passive approach.

Now, I always opt in favor of some investment over none. Spend some time on financial LinkedIn, and you’ll see no shortage of advisors debating the finer points of portfolio holdings, expense ratios and tax treatments.

I get it. Some ways of investing are more efficient than others. So if you’re in a target-date fund and you’ve been contributing regularly, kudos. You’re far ahead of someone who nitpicks every aspect of the plan but is meanwhile losing money trading penny stocks in the hope of getting rich overnight.

However, in some ways, you may be able to do better than target-date funds.

As Safe As They Seem?

We’re all drawn to the investment with the best performance, right?

That’s natural, but there’s a reason why some assets perform better in certain cycles: Risk. Take too much risk at the wrong time, and you can jeopardize your nest egg.

Let’s compare two of the largest 401(k) target-date fund providers.

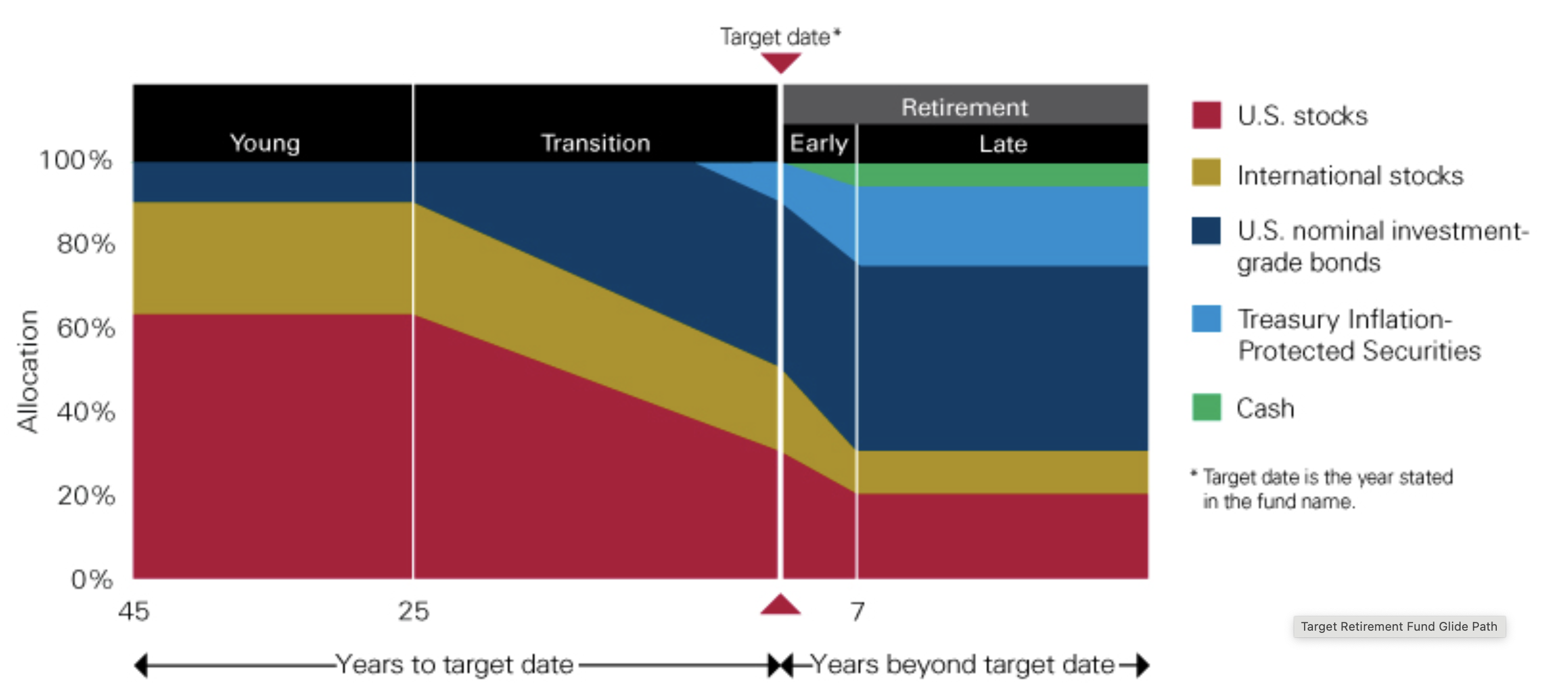

Vanguard Target-Date Glide Path

Pros:

- Gradually shifts to bonds before retirement, reducing volatility near the target date.

- Includes TIPS and cash after retirement, offering inflation protection along with liquidity.

- Simplified allocation buckets, using U.S. stocks, international stocks, bonds, TIPS and cash. This makes it fairly easy to understand and track investments.

- Lower equity allocation in retirement (about 30% to 40%), reducing sequence of returns risk during withdrawals.

- Passive strategy leading up to retirement aligns with traditional risk mitigation strategies.

Cons:

- May underperform in uptrending markets due to limited equity exposure. That can hurt purchasing power in retirement.

- Less aggressive growth potential, possibly requiring larger contributions to fully fund retirement.

- Might not fully protect against longevity risk.

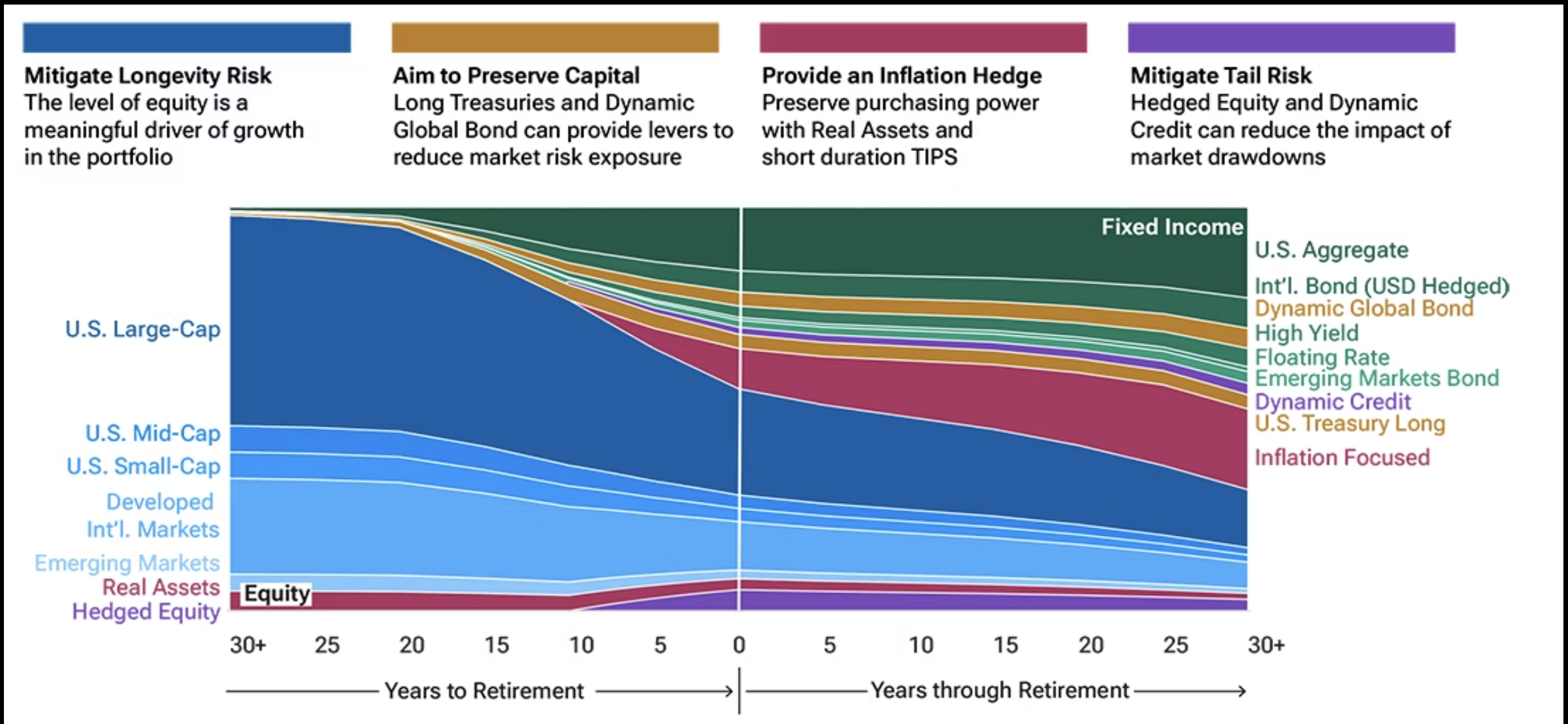

T. Rowe Price Glide Path

Pros:

- Higher equity exposure, at approximately 55%, even past retirement, which may help combat inflation and longevity risk.

- Greater asset class diversification, including mid-cap, small-cap, real assets and emerging markets.

- Emphasizes protection against inflation and negative retirement outcomes, using dynamic bonds, TIPS and hedged strategies.

Cons:

- More complex glide path and actively managed holdings can be harder for investors to understand.

- Higher risk of loss near retirement, especially during market downturns.

- May not suit risk-averse retirees who prefer a more conservative glide down.

What to Watch Out For

The point here is not to dunk on either plan; as you can clearly see, each has its pros and cons.

But that doesn’t mean you’re locked into a plan just because you’ve been contributing for years; you can change your allocation any time. For example, if you have other sources of retirement income, or you’ve gotten a sizeable inheritance, you may be able to take a little more risk even as you age.

On the flip side, if capital preservation is your main concern, then ratcheting back the risk could be he right move.

You’ve heard this before (including from me), but that’s where a comprehensive financial plan is useful. I’ve seen way too many retirees just guess and wing it, which usually results in a potential shortfall. I’ve seen the other side of that too, when retirees are holding the purse strings too tightly, when, in fact, they can afford to loosen up a bit.

The Perils of Set-And-Forget

Target-date funds can be an excellent foundation for retirement investing, especially if you prefer a hands-off approach. But like any investment product, they’re not one-size-fits-all.

The real risk isn’t in choosing a target-date fund. It’s in assuming that your default choice is automatically the best option for you as your circumstances evolve over time.

Revisit your allocation with fresh eyes. If that means hiring a planner, then do it. These funds are tools; not magic wands that will make everything OK once you leave the workforce.

A well-designed retirement plan should reflect your income needs, risk tolerance, longevity expectations and tax situation, not just your birth year.