Buckle Up, It's a Trade War

Markets have suddenly become a bit confusing. Here's what the charts say, how the markets are reacting and what's ahead this week.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

U.S. equity index futures opened sharply lower on Sunday evening, as the U.S. Dollar strengthened, against the Canadian dollar and Mexican peso in particular. Adjacent to those moves, crude prices popped nicely, but cryptocurrencies met up with the "ugly stick." On Friday morning, Bitcoin traded as high as $105,740 per token. On Sunday evening, I saw Bitcoin trade just above $93,000. As the zero-dark hours pass on Monday morning, Bitcoin is trading above $95,000.

Though there have been some sharp moves in market prices for risk assets since Friday afternoon, there really aren't any surprises in what we are seeing. Under the International Emergency Powers Act, the Trump administration began collecting 25% tariffs on Canadian and Mexican imports on Saturday, which broke as news (though we all saw it coming a mile away) during the regular trading session on Friday. Energy-related imports from Canada were subjected to a lesser 10% tariff, while Chinese imports were also tagged with an additional tariff of 10%. The underlying reason for use of that particular act was the "major threat of illegal aliens and deadly drugs."

It did not take long for our largest trade partners to respond. Canada came out swinging, and placed a 25% tariff on what may be scaled up to $155 billion worth of U.S. exports to the great white north that will start on Tuesday and take three weeks to hit that full number. Mexico's President Claudia Sheinbaum has reportedly ordered "Plan B" measures that are said to include both tariffs and non-tariff-related measures. China's Ministry of Foreign Affairs openly complained, and without laying out specifics, said that countermeasures would be taken.

Will these actions impact consumer prices? In all likelihood, yes, if this goes on for a while. Will this hurt corporate earnings? Almost definitely, and not just for large multinationals, again, if it goes on for a while. Have we targeted the EU or U.K. for higher tariffs? Not yet, as far as I can tell. All of the U.S. automakers will be impacted. Energy will be impacted. Agriculture will take a hit.

Canada supplies a rough 60% of all U.S. crude oil imports down to U.S. refiners that mix it with the light, sweet stuff, making gasoline. Of course, a significant enough portion of that gasoline heads back north, so how that plays out will be interesting. Mexico provides 23% of U.S. agricultural imports. The raspberries, blackberries and strawberries were all on "BOGO" sale at my local Publix on Sunday. I don't expect to see that again for a while. Needless to say, I loaded up.

In Other News...

-- On Friday, in an appearance at Fox News, Secretary of Defense Pete Hegseth did not rule out military action in dealing with the cartels (now designated at foreign terrorist organization) at the southern border after U.S. border agents had recently come under gunfire. Hegseth said, "All options will be on the table."

-- The United States armed forces conducted airstrikes against ISIS targets operating inside Somalia on Saturday. The attack was coordinated with the Somalian government.

-- Secretary of State Marco Rubio warned Panama's Jose Raul Mulino on Sunday that Chinese influence over the Panama Canal may violate the treaty that ultimately gave control of the canal to Panama in 1999 and was unacceptable.

Last Week

Markets have suddenly become a bit confusing. Stocks traded lower last week but were up for January. Is this positive? What about now, that this trade war has gotten under way? Could there be a hot war at the southern U.S. border? These are the questions that we are all asking. Though we did not truly have a real "day one" bearish reversal of trend last week, it sure feels like we may have one on Monday.

The week started out with an ugly jolt as Chinese AI startup DeepSeek had apparently created a much lower cost large language model. This put tech stocks, AI stocks, and semiconductor designers at the elite end of the pool, such as Nvidia NVDA under the gun as severe beat-downs were handed out en masse. Nvidia gave up nearly 17% last Monday and closed the week down 15.8%, so there was no real recovery. Unlike most of the mid-major to major equity indexes, NVDA closed out January down 10.6% from where the stock had ended December.

So, is the January Barometer for real? If it is, U.S. stocks will have another good year. The S&P 500 was up 2.7% in January. Historically, when the S&P 500 gains more than 2% in January, the full year has about an 88% probability for a positive finish and that finish averages a gain of almost 18%.

On Wednesday, the Fed's FOMC chose not to change short-term interest rates at the moment, but hinted at a hawkish change in demeanor, acknowledging that progress in the fight against consumer level inflation has stalled.

The macro was a little on the light side for the week, but there were some headline-level releases. December Durable Goods Orders were weak on the surface due to Boeing's BA inability to deliver aircraft, but core capital goods were rather strong. On top of that, the BEA printed their first estimate for Q4 GDP at growth of 2.3% (q/q, SAAR), which was a little on the light side versus expectations.

Marketplace

Among the major to mid-major U.S. equity indexes....

-- The S&P 500 gave up 0.5% on Friday, and 1% for the week, but gained 2.7% for January.

-- The Nasdaq Composite gave up 0.28%, and 1.64% for the week, but gained 1.64% for January.

-- The Nasdaq 100 gave up 0.14% on Friday, and 1.36% for the week, but gained 2.22% for January.

-- The Russell 2000 gave up 0.86% on Friday, and 0.87% for the week, but gained 2.58% for January.

-- The S&P SmallCap 600 gave up 0.83% on Friday, and 0.49% for the week, but gained 2.85% for January.

-- The S&P MidCap 400 gave up 0.9% on Friday, and 1.12% for the week, but gained 3.78% for January.

-- The Dow Transports gave up 1.24% on Friday, and 1.8% for the week, but gained 2.59% for January.

- -Philly Semiconductors gave up 0.29% on Friday, and a stunning 6.1% for the week, but still gained 0.72% for January.

-- The KBW Bank Index gained 0.63% on Friday but gained 0.59% for the week and 8.6% for January.

On Friday, 10 of the 11 S&P sector SPDR ETFs closed in the red, led lower by Energy XLE. Only Communication Services XLC posted a gain for the day, after the trade tariff headlines broke.

For the week, five of the 11 S&P sector SPDR ETFs closed in the green, as four of these funds gained at least 1%. Communication Services was the winner for not just Friday, but for the week, up 1.96%. Health Care XLV and the Staples XLP followed closely, which does make one look sideways at what positivity there had been mid-week. Energy gave up 4.02% for the week, as Tech XLK gave up 3.55% on semiconductor softness.

What Do the Charts Say?

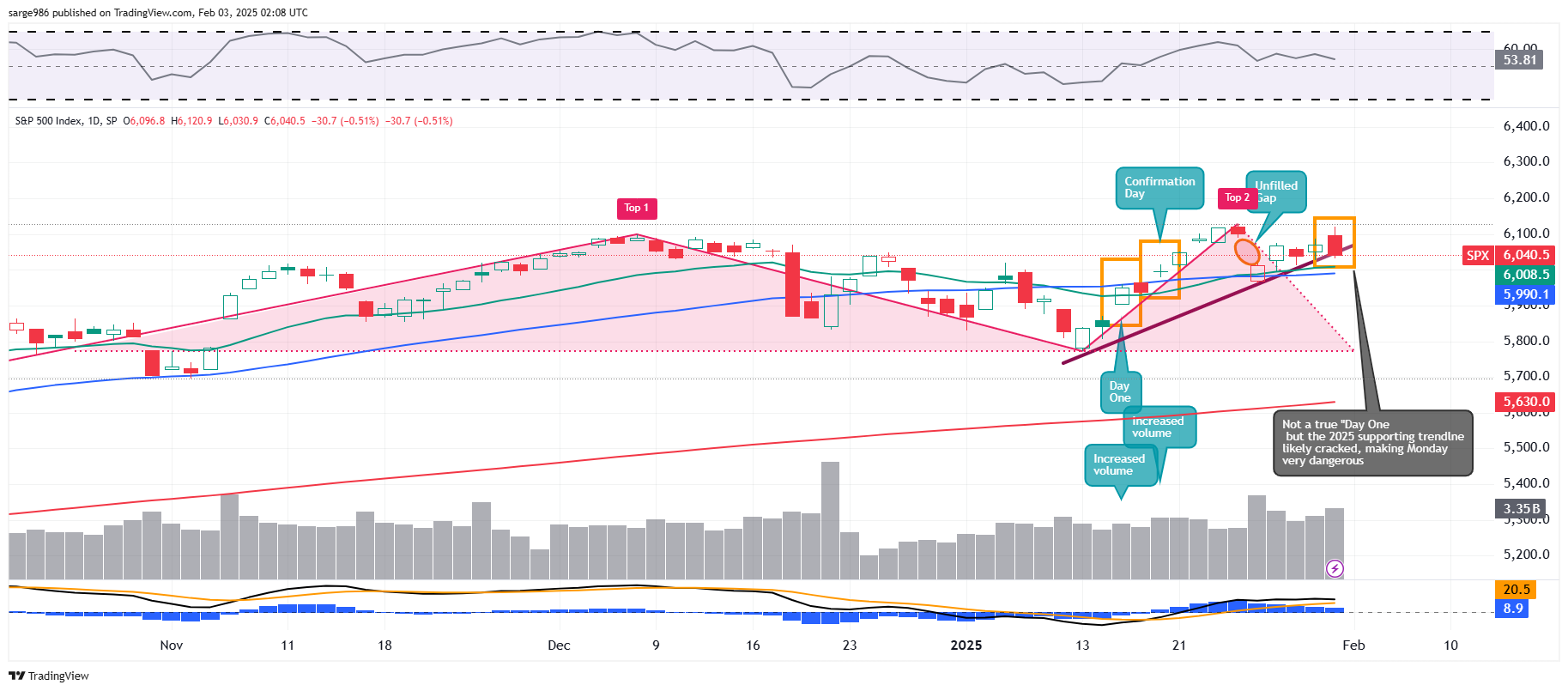

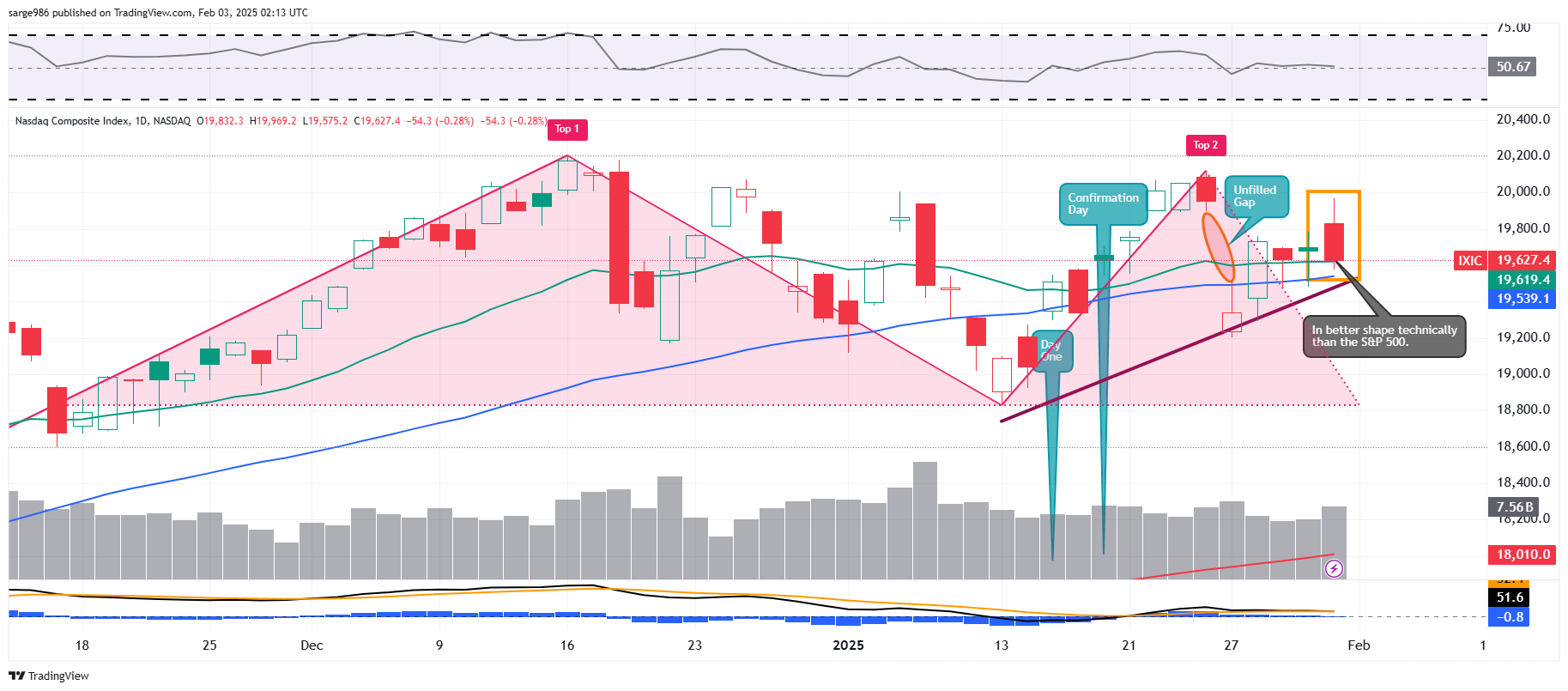

Friday's reversal was ugly. but what did it mean? Losers beat winners at the NYSE on Friday by roughly 8 to 3 and by almost 2 to 1 at the Nasdaq. This is where it gets tricky. Advancing volume took just a 23.5% share of composite NYSE-listed trade on Friday, but somehow a 53.1% share of composite Nasdaq-listed activity.

Aggregate trade was higher for listings of both exchanges, but that majority share of composite volume for Nasdaq-names prevents Friday from being a true "Day One" reversal of trend. Now, that doesn't mean that the trend did not turn on Friday. It just means that the "Day One" for confirmation purposes may or may not still be on the way. Remember, we did warn last week that a double-top pattern of bearish reversal was indeed threatening the markets.

Relative strength and the daily MACD (moving average convergence/divergence) are both still "okay" for the S&P 500. Readers will note the trendline that I had drawn underneath the January 13th through last week's lows. That line came under pressure on Friday afternoon and will very likely crack on Monday morning.

Readers can easily see that the Nasdaq Composite has not yet threatened that supporting trendline. The Nasdaq Composite is in better shape, technically, right now than is the S&P 500. The short-term threat to both indexes would be an algorithmic overreaction to the tariff news that costs both major indexes their respective 50-day SMAs (simple moving averages).

Earnings

According to FactSet, with 36% of the S&P 500 having reported their fourth-quarter earnings, 77% of those firms reporting have beaten earnings expectations, while just 63% of those reporting have beaten revenue expectations. At this point, for the quarter, earnings growth is running at a blended (results & expectations) rate of 13.2% (up from 12.7% a week ago) on revenue growth of 5.0% (which is up from 4.6% a week ago).

For the quarter, the Financials are expected to post by far the greatest earnings growth at +50.7%, with Communication Services in second place at +28.5%. Four sectors are expected to show a year-over-year earnings contraction, led lower by Energy at -28.8%.

As for the current quarter (Q1 2025), consensus is currently for earnings growth of 10.1% (down from 11.3%) on revenue of 4.8%, down from last week's 5.0%. For the full year 2025, Wall Street sees earnings growth of 14.3% on revenue growth of 5.7%. It does appear that at least for the current quarter, analysts are starting to price in the impacts of these tariffs.

As for valuation, the S&P 500 went into the weekend trading at 22.0 time (down from 22.2) 12-month forward looking earnings and 28.3 time (down from 28.6) 12-month trailing earnings. These ratios both remain well above their respective five-year and 10-year averages.

What's Ahead?

Well, this morning there will be a selloff across the spectrum of U.S. risk assets, Asian stocks were lower, followed by European equities. Now, it's our turn. That said, as ugly as it looks, it was worse last night. As for those long cryptocurrencies, this has been an especially tough weekend. Those calling for a higher U.S. dollar, such as our own Carley Garner has been doing, have simply nailed that trade.

The main event this week, outside of the political and perhaps the geopolitical, will be January Jobs Day this Friday. Job creation is expected to have slowed somewhat in January. The unemployment rate may not have been directly impacted, but wage growth is expected to show visible signs of deceleration. As far as the U.S. macro is concerned this week, ahead of that BLS employment report, there are a number of sub-headline level numbers coming at us.

This morning, we'll see the January ISM Manufacturing PMI and December Construction Spending. The December JOLTS reports will be released tomorrow (Tuesday), followed by the ADP Employment Report on private sector job creation for the month of January on Wednesday. Then on Friday, after the report on weekly jobless claims lands on Thursday, alongside the BLS surveys, the University of Michigan will release its preliminary survey results for February covering consumer sentiment and inflation expectations.

It's been a while, with the exceptions of the FOMC policy statement last week and Fed Chair Powell's press conference, but this week, almost as if they were ordered to get out there, the Fed will be out in force. Making public speaking appearances every single day of this workweek, we'll hear from Vice Chair Philip Jefferson, Fed Governors Bowman, Waller, and Kugler, as well as several regional branch presidents. The U.S. Treasury Department will also publish the agency's refunding plans this Wednesday morning.

Earnings season remains very active this week. This morning, we'll hear from Tyson Foods TSN, followed this evening by long-time Sarge focus name Palantir Technologies PLTR. Be prepared to trade that one overnight as the shares will be volatile. Tuesday brings quarterly numbers from Merck MRK, PayPal PYPL, PepsiCo PEP, Spotify SPOT, Advanced Micro Devices AMD, and Alphabet GOOGL. Disney DIS will report on Wednesday morning, along with Uber Technologies UBER, followed by Ford Motor F and Arm Holdings ARM that evening. Thursday will present numbers from Eli Lilly LLY, and Amazon AMZN to be followed by the CBOE CBOE on Friday morning.

Economics (All Times Eastern)

09:45 - S&P Global Manufacturing PMI (Jan-F): Flashed 50.1.

10:00 - ISM Manufacturing Index (Jan): Expecting 49.4, Last 49.3.

10:00 - Construction Spending (Dec): Expecting 0.2% m/m, Last 0.0% m/m.

The Fed (All Times Eastern)

12:30 - Speaker: Atlanta Fed Pres. Raphael Bostic.

18:30 - Speaker: St. Louis Fed Pres. Alberto Musalem.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: TSN (0.88)

After the Close: CBT (1.77), CLX (1.40), KD (0.41), NXPI (3.13), PLTR (0.11)

At the time of publication, Guilfoyle was long PLTR, NVDA, AMD, AMZN equity.