Beware, or Profit From, Extreme Stock Market Deviations

Today’s blue-chip names have rarely seen valuations this many standard deviations above normal. Here's my advice on how to put the odds heavily in your favor.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

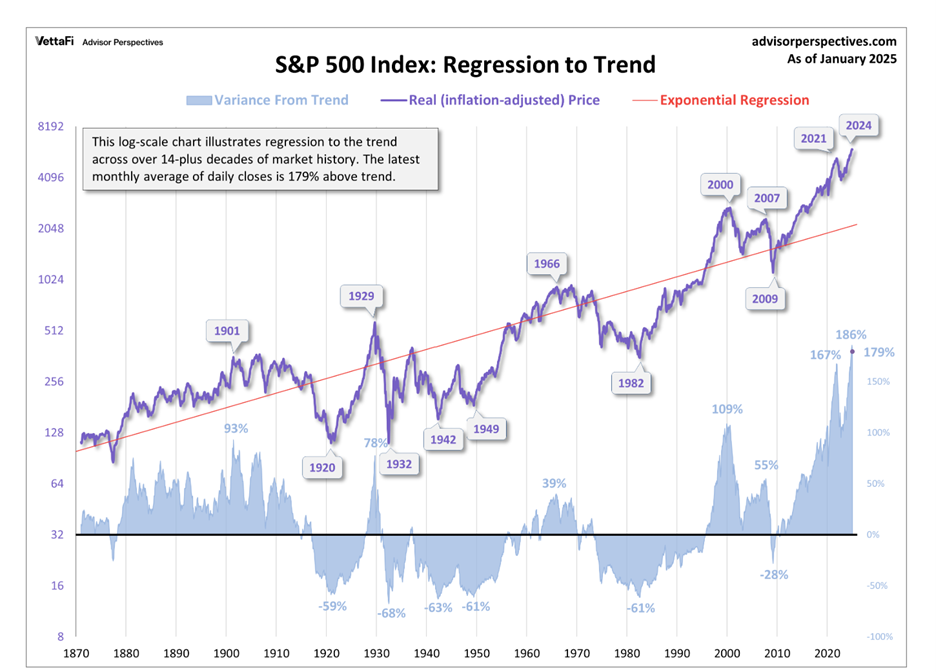

Students of statistics understand that everything in life tends strongly towards “regression to the mean” when things stray too far from normal in either direction.

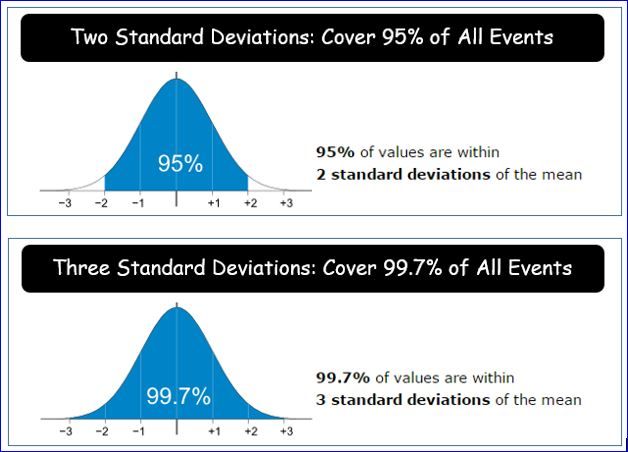

Ninety-five percent of values are covered in a two-standard deviation (2 S.D.) bell curve. Three S.D. extremes account for close to 100% of all situations.

That absolutely applies to stock market valuations over time.

The chart below illustrates how large deviations from normal have always followed that immutable law of nature.

Post World War I doldrums saw stocks crater until extremely cheap valuations led to sharp rebounds. Reversion to the mean [and beyond] then extended until the Crash of 1929, correcting what had become unusually high equity valuations.

The market’s 1966 peak was driven by the Nifty Fifty companies which were considered “one decision” stocks back then. “One decision” referred to the act of buying and then holding forever the top names at that time because they would never go down again.

Currently, mostly forgotten names like Kodak, Polaroid and Xerox were among those "never to fall again” companies.

That concept proved to be as wrong as the current view on the Magnificent 7 stocks in recent years will likely turn out.

Where does that leave us today?

History [and the chart above] says that today’s blue-chip names have rarely seen valuations this many Standard Deviations above normal. The current excesses exceed those of both March 2000, just before the end of the tech-internet bubble, and the October 2007 peak.

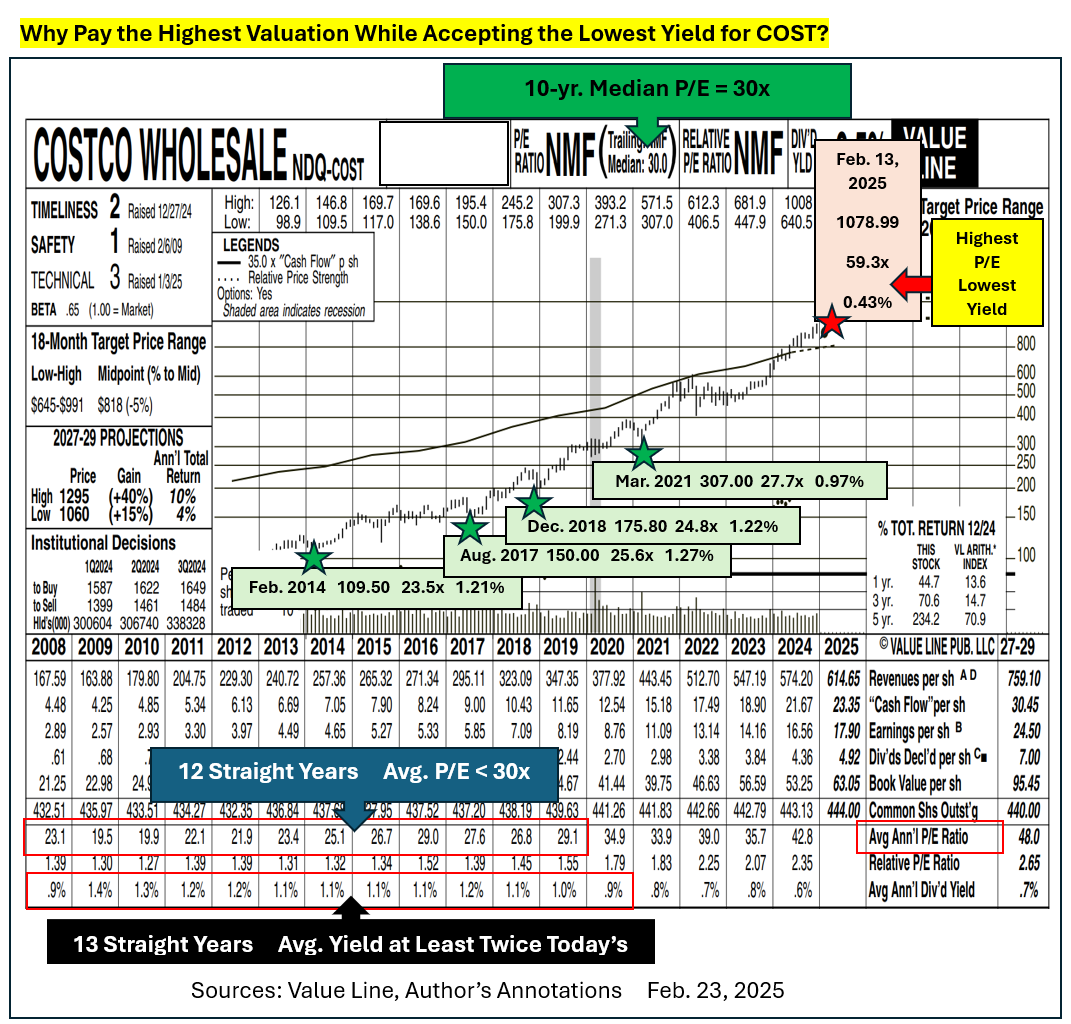

I will use Costco COST as an example. It is an excellent company that used to sell consistently for between 19.5 and 29.5 times earnings, while typically yielding a bit over 1%.

At its Feb. 13, 2025, recent high of $1,078.89, COST fetched almost 60 times this year’s estimate accompanied by a skimpy 0.43% current yield.

Costco is a superior growth company. As such it usually commanded premium multiples. Even so, investors could have purchased shares in it for much more reasonable P/Es in every single year from 2008 through 2019.

Dividends during the entire 13 years from 2008 through 2020 average at least twice today’s dividend yield.

If I created similar graphics for Walmart WMT, Apple AAPL, Berkshire Hathaway BRK.A BRK.B, Microsoft MSFT and most other mega-cap and large-cap stocks, most would show the same pattern of gross overvaluation based on all previous history.

That situation does not body well for the prospects of index fund or ETF investing going forward. The excesses appear most dramatic in technology stocks, which now dominate the ranks of their largest components.

Just as in the wild days of early 2000, more mundane and mostly smaller companies often sported extremely cheap valuations and much higher than typical yields. Shares of those firms were priced at 1 or 2 standard deviations below normal.

Unsurprisingly, “value” stocks made huge gains after the tech bubble burst even as formerly beloved shares faced steep losses for years to come.

Today’s Advice

- Sell or avoid purchasing pricey shares with great momentum.

- Take profits in index funds representing the S&P 500, DJIA and Nasdaq 100 names.

- Hold or accumulate stocks selling well below their historical valuation parameters.

- Ignore most analyst buy recommendation advice as it mainly focuses on “good looking” charts of shares, which have already been marked-up dramatically.

My coming articles will spotlight the best bargains I have identified for their prospects of oversized gains over the coming months and years.

Let your knowledge of standard deviations put the odds heavily in your favor.

At the time of publication, Price had no positions in any securities mentioned.