Beating the S&P 500 Won’t Save Your Retirement — But This Will

Outperforming the S&P 500 may feel like winning, but this should be your real goal.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

1-15-25-millionaires-are-terrified-of-this-one-thing-in-retirement

1-15-25-millionaires-are-terrified-of-this-one-thing-in-retirement

You know that investor. The one who measures success in one way: Did I beat the S&P 500?

If the S&P 500 returned 12% and they made 14%, it’s a win. If they made 10%, it’s a failure, even if their retirement timeline, tax plan and lifestyle flexibility are exactly on track.

That kind of framing misses the point entirely, says Dr. Preston Cherry, CFP, founder of Houston-based Concurrent Wealth Management, and author of Wealth in the Key of Life: Finding Your Financial Harmony.

“When I sit with a client and we start talking about retirement or a major life transition, ‘purpose’ stops being abstract very quickly,” he says. “It becomes a practical question: which dollars are meant to fund which years of your life?”

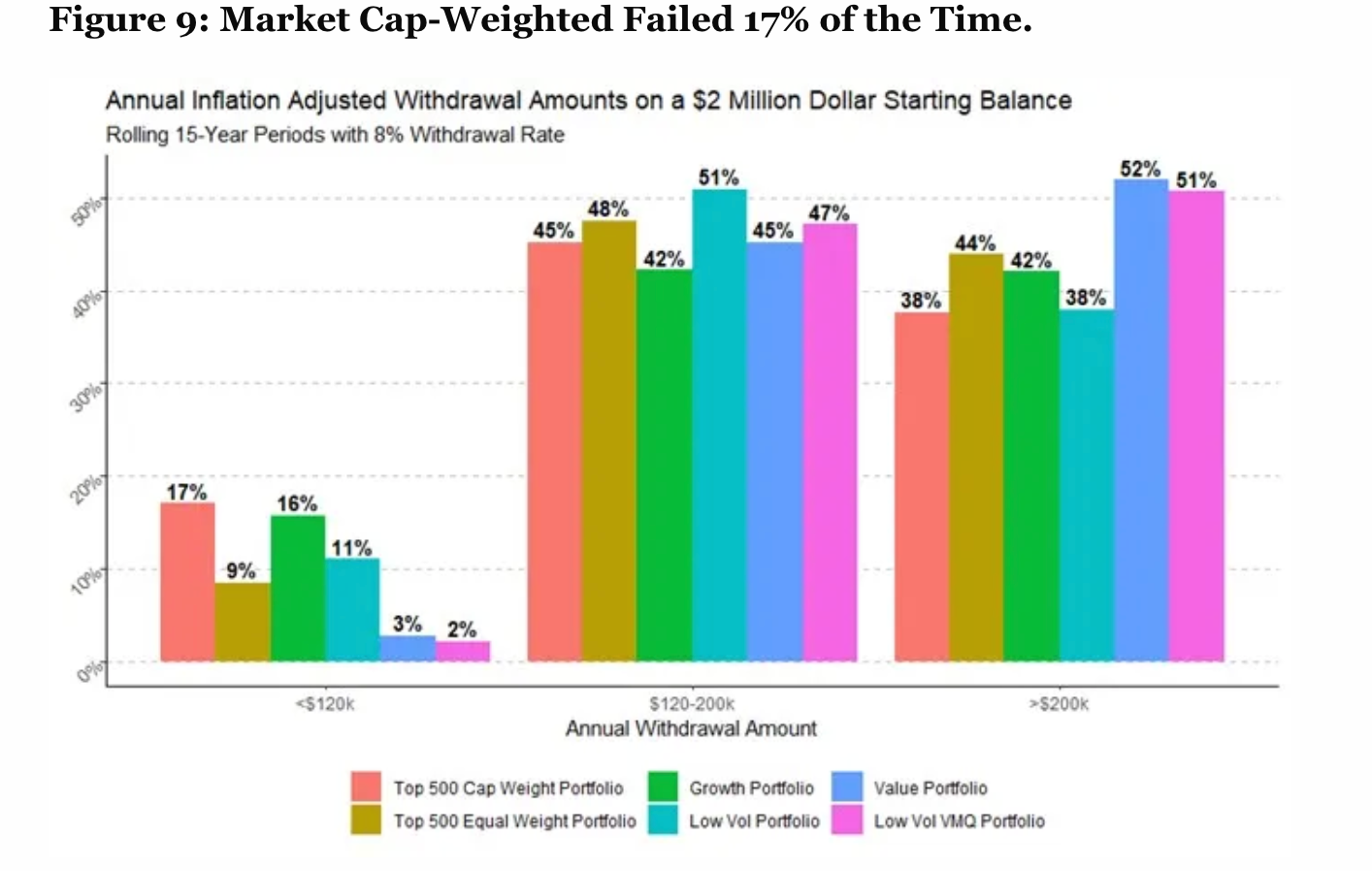

Beating the S&P 500 might feel like winning, but a 2026 study published by the CFA Institute, found that the standard market-cap-weighted index, the one everyone benchmarks against, couldn’t generate enough retirement income 17% of the time when tested across 60 years of market history.

CFA Institute

As the above image shows, when researchers zeroed in on retirement income sustainability instead of performance, value-focused and diversified portfolios outperformed the S&P benchmark by a long shot.

This wasn’t because they delivered flashier returns (they didn’t), but because they delivered consistency, which is what retirees need more than market-beating bragging rights.

What the Money Is Really For

Cherry notes that he doesn’t just focus on return targets with clients; instead, he defines assignment of the dollars.

“Some assets are there to provide stability through early retirement or during a major transition. Some are mid-term flexibility assets, covering travel, business reinvention, or helping family,” he says. “Others are long-term growth assets meant to preserve today’s lifestyle preferences in tomorrow’s dollars and manage longevity risk.”

Did you get that?

There’s no “beating the market” that factors into this plan.

According to Cherry, a money preference is what happens when an instinct starts overriding the plan, like when an investor sees the market riding higher, and decides to make bigger bets on stocks or trade faster than their actual financial situation can support.

I’ve seen people who hadn’t saved enough try to aggressively trade to make up the difference. In recent years, they may have had some success, but even that wasn’t sustainable through every market cycle.

The 20% Drop That Changes Everything

“When someone sits across from me at 57 or 60 and is still trading like they’re 35, the issue usually isn’t skill. It’s sequencing and stage of life,” Cherry says.

At 35, he adds, most professionals are still pre-peak earning, building momentum, contributing aggressively to their retirement accounts, and letting volatility work in their favor.

“Between 45 and 55, many high achievers hit peak income years, a stage many Gen X professionals are navigating right now, often managing equity compensation, business growth, and larger tax exposure,” he says.

But after age 55, especially for high earners planning to retire between 55 and 62, the age when they are first eligible for Social Security benefits, if they choose to claim on the early side, the conversation shifts again, Cherry says.

“The same 20% drawdown that felt like noise at 35 can materially affect not just retirement income durability, but career flexibility and lifestyle optionality,” he says.

Panic-Driven Trades

This is one reason why events like the current war with Iran can send retirees into a panic. Any indication that markets will “crash” (the word many investors instinctively use even for a normal bear market decline) creates worry.

The emotion is understandable; nobody wants to see years of saving go down the drain for reasons completely outside their control. But that’s where a solid plan comes into the picture.

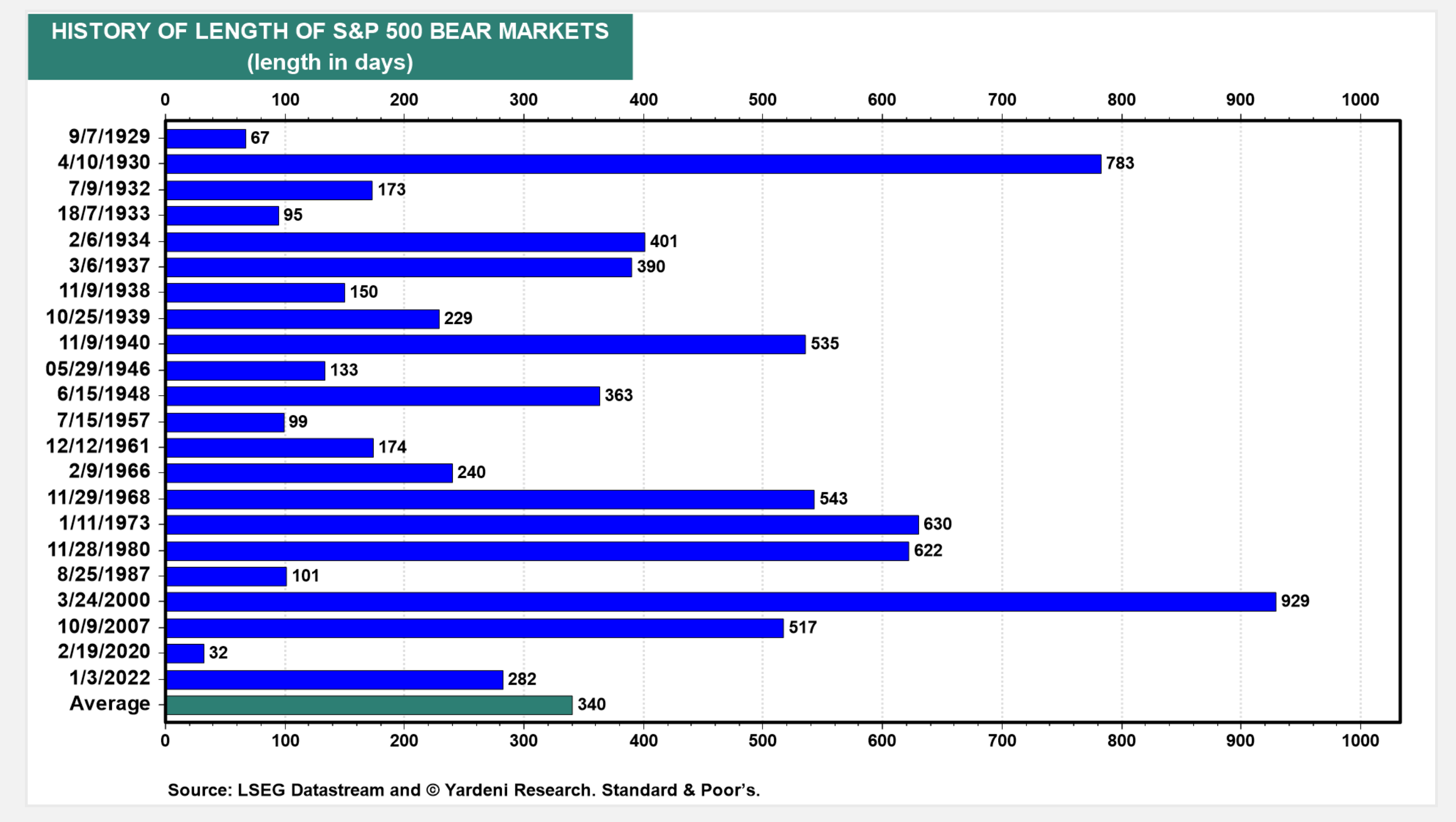

“Markets don’t move in straight lines. A pullback of 5% to 10% is normal,” Cherry says.

He adds that a correction of 10% to 20% historically happens about every 16 months and lasts roughly six weeks. In other words, that’s normal, too.

“A bear market of 20% or more can stretch for months, while a crash is defined by speed and can unfold in days,” he says. “A durable plan anticipates all four. Especially for clients within ten years of retirement, sequence-of-returns risk becomes a planning variable, not just a market headline.”

This graph, compiled by Yardeni Reserch, illustrates the frequency and length of bear markets.

Yardeni Research

And it’s not just retirees who are concerned about market ups and downs: For investors in their peak earning years, volatility also affects their equity compensation strategy, liquidity planning, and career timing decisions, Cherry notes.

When 'One More Trade' Stops Adding Value

At some point, beating the benchmark becomes less relevant than preserving flexibility.

“This conversation comes up often with successful investors who genuinely enjoy trading,” Cherry says. “When we sit down together, I’ll ask a simple question: If your current allocation already supports your retirement goals and broader lifestyle objectives with acceptable risk, what exactly is the next trade meant to accomplish?”

Now, if a person understands the purpose of his or her plan and just enjoys trading and wants to take a flyer on a small number of Nebius Group (NBIS) shares, then I’ve always said “go for it.”

However, attempting to beat the S&P just because you think you’re supposed to, for some reason, or because you’re trying to amplify your return, any incremental outperformance may not actually improve your situation, Cherry says.

“That’s where the ‘Enough Paradox shows up,” he says.

"Wealth in the Key of Life: Finding Your Financial Harmony," by Dr. Preston Cherry, CFP

“In Wealth in the Key of Life, I write about how many high achievers struggle not because they lack wealth, but because they haven’t defined ‘enough.’ Without that clarity, performance becomes a moving target,” he adds.

Cherry notes that in his advisory work, prosperity is not defined by beating the S&P 500 in a given quarter. Instead, it’s defined by whether an investor’s portfolios are doing their jobs: Supporting sustainable income, preserving flexibility, managing taxes, and protecting long-term independence.

“Once a plan reaches the point where it works, the objective changes from maximizing to optimizing. More risk does not automatically equal more prosperity,” he says. “The goal isn’t to stop investing. It’s to recognize when your strategy has already secured what matters, and to avoid undermining stability in pursuit of one more win.”