Avoiding the Urge to Stir in Extra Portfolio Ingredients

Monitor, adjust, and stick to your plan.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

This is the ninth of ten articles in the Filthy Rich Animal Investing Basics Series.

If you like what you see, are not yet subscribed, or want to share with a friend, please visit this link to join us. It's free!

In two weeks, we'll begin providing actionable advice and weekly educational content.

And that's when the real fun will start!

So at my house, we make a lot of dishes that take time to cook. I’m talking about soups, chilis, or braised beans.

I made a chili not long ago, and it took a while to assemble all my ingredients: Tomatoes, tomato paste, various chile powders, red wine (for real - try this!), canned green chiles, beans and some of that vegetarian fake meat (don’t cringe - I bet you wouldn’t know the difference if I served it to you).

After combining everything, heating it up, stirring, and then tasting to see if it needed anything else, I put it on low heat and left it on the stove. Then I walked away and did something else.

You know where this is headed: Cooking that chili has similarities to investing for the long haul. Once you determine that your portfolio recipe is right, then it’s time to just keep an eye on it and make adjustments, such as rebalancing, as needed.

Famous Stock Trader Got It Right

Some of you may be familiar with “Reminiscences of a Stock Operator,” the book about renowned early 20th century trader Jesse Livermore.

Here’s a quote from that book, published in 1923 that’s relevant to today’s retirement investors, not just day traders from a century ago*:

"It never was my thinking that made the big money for me. It was always my sitting. Got that? My sitting tight! Men who can both be right and sit tight are uncommon. I found it one of the hardest things to learn. But it is only after a stock operator has firmly grasped this that he can make big money.

Because the market does not beat them. They beat themselves, because though they have the brains...they cannot sit tight. It is literally true that millions come easier to a trader after he knows how to trade than hundreds did in the days of his ignorance."

*Yeah, I cringe a little whenever I see the typical 20th-century sexist language, but it is what it is… The point is still valid.

OK, back to the 21st century: Investors today still have a hard time sitting still with their investments.

Let’s return to the chili recipe metaphor to examine that point.

Say your financial plan (Which you have, right? Right?) determines that you should have a 70% allocation in stocks and a 30% allocation into fixed income and cash. That’s the level of risk you can take, at this point in your life, to meet your long-term financial goals.

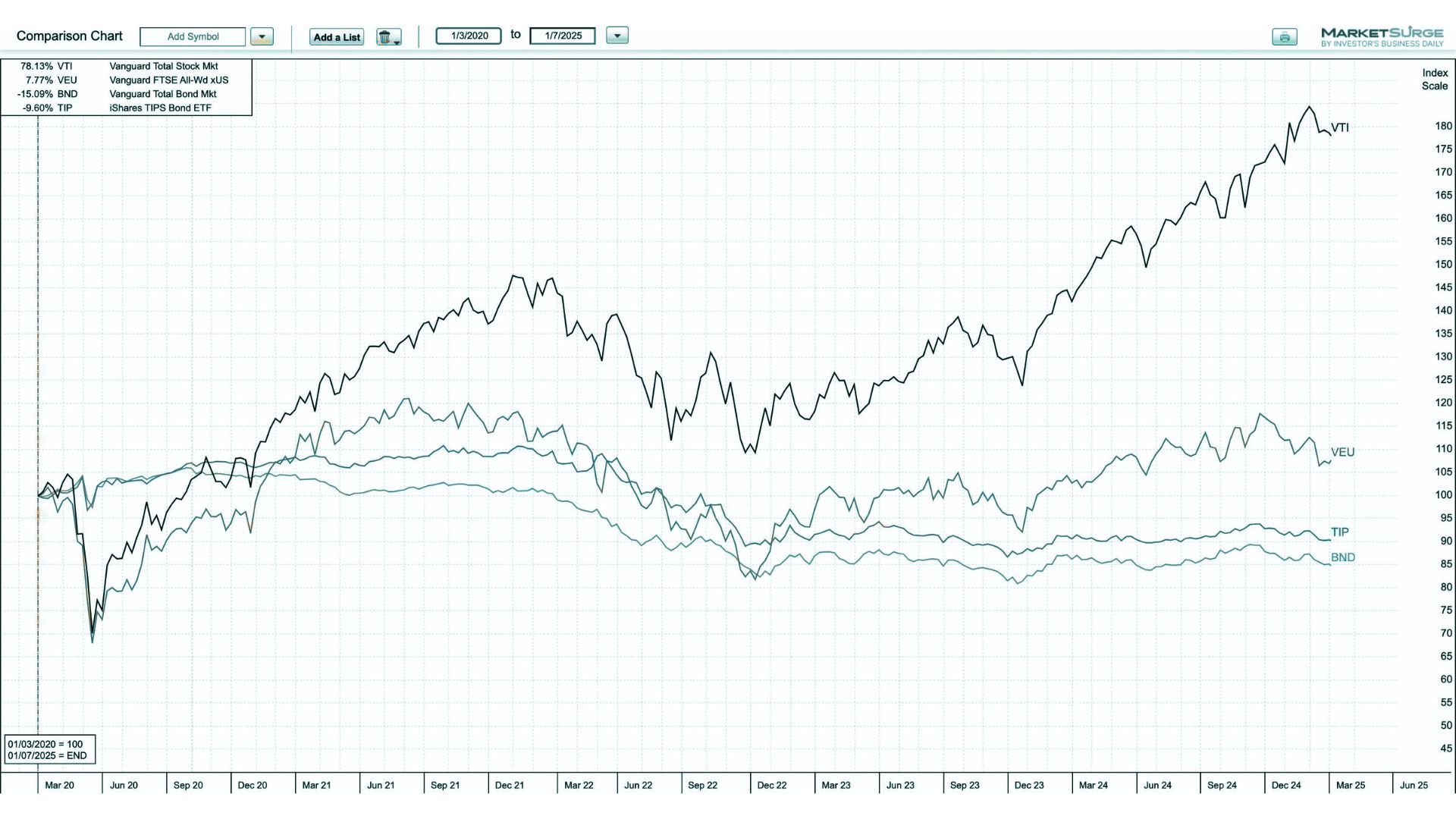

Here’s a simple, four-fund example, using low-cost ETFs.

Vanguard Total Stock Market ETF (VTI)

Allocation: 50%

Reason: Provides broad exposure to the entire U.S. stock market, including large, mid, and small-cap stocks. It's a bet on the US economy.

Vanguard FTSE All-World ex-US ETF (VEU)

Allocation: 20%

Reason: Provides exposure to international markets (excluding the U.S.), which helps diversify globally. It's a bet that when the US market isn't so strong, the rest of the world will help to improve your returns.

Vanguard Total Bond Market ETF (BND)

Allocation: 20%

Reason: Provides exposure to a wide range of U.S. investment-grade bonds, including government, corporate, and international bonds. It's a diversification bet that when stocks aren't so strong, bonds will be. It can also help provide income and not just capital gains.

iShares TIPS Bond ETF (TIP)

Allocation: 10%

Reason: Provides exposure to U.S. Treasury Inflation-Protected Securities (TIPS), which can help protect against inflation. Again, this is a bet that bonds will beat stocks when stocks are down. And preserve some of your buying power.

Here’s a look at the performance of this portfolio for the five years ending in December, 2024.

There’s nothing particularly surprising here; VTI, which reflects the total U.S. stock market, has been the better equity performer versus global stocks.

Meanwhile, bonds have served to dampen some of equities’ volatility; you don’t buy bonds with the expectation that their price appreciation will match that of stocks.

If you held a portfolio like this, or something similar, the best course of action would have been to simply rebalance at appropriate intervals, such as once or twice a year. That’s the kind of monitoring that will create the long-term return you’re looking for.

The secret sauce to portfolio success:

Monitor your portfolio to be sure it stays aligned with your long-term goals. Before you rebalance, consider factors like market conditions, asset performance and any changes to your own risk tolerance. For example, as you get closer to retirement, you probably want to allocate more money to fixed income, and less to stocks.

Shuffling holdings in a panic can disrupt strategy, incur unnecessary costs, and may result in poor timing or missed opportunities.

Certainly you’ve messed with a good recipe at times, and made it worse than it had previously been. Messing with your portfolio, just because you feel like it, can have similar results.