Subscriber Comment of the Day

Randy

Virginia Lawmakers And Governor Meet To Discuss Marijuana Sales Legalization Compromise That Could Pass This Month

BY Doug Kass · Jun 5, 2026, 4:47 PM EDT

Randy

Virginia Lawmakers And Governor Meet To Discuss Marijuana Sales Legalization Compromise That Could Pass This Month

BY Doug Kass · Jun 5, 2026, 4:47 PM EDT

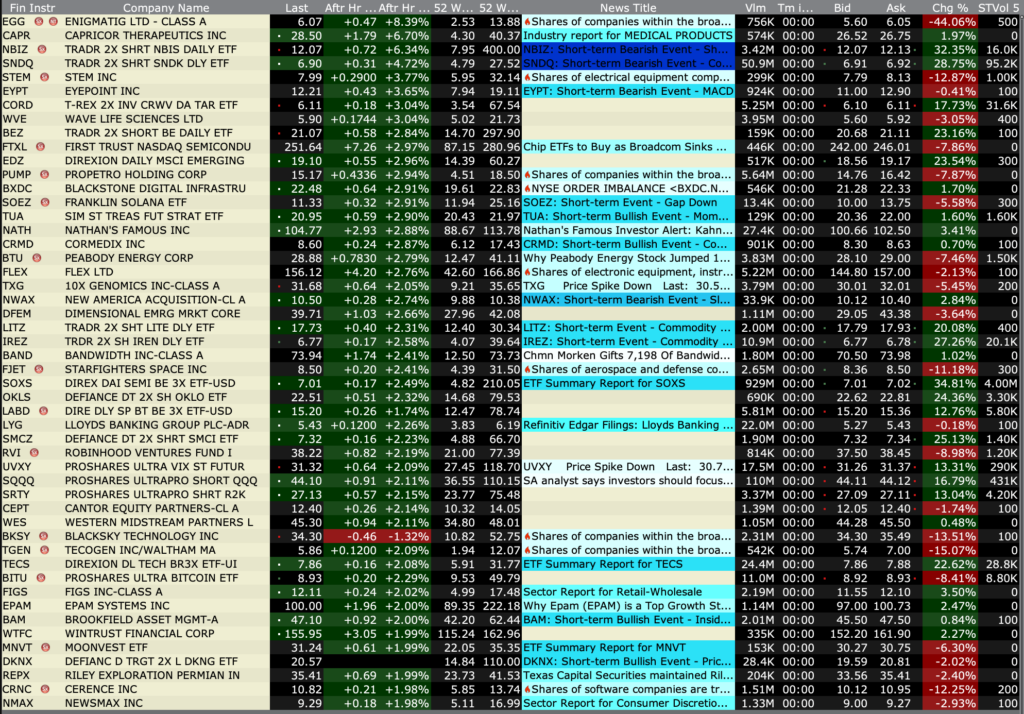

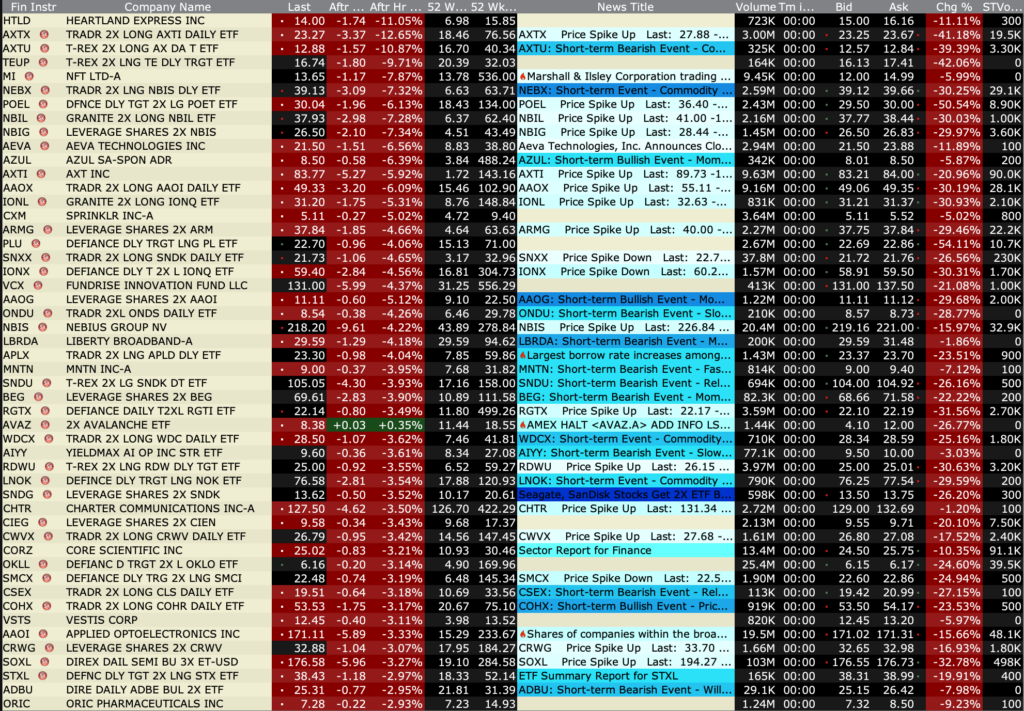

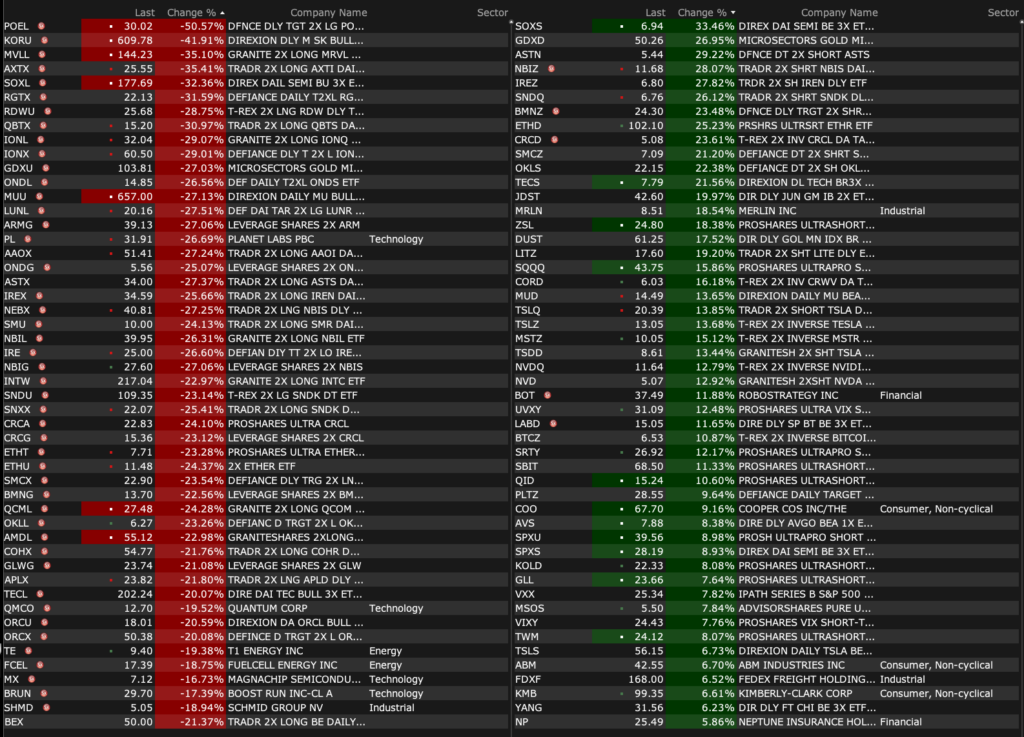

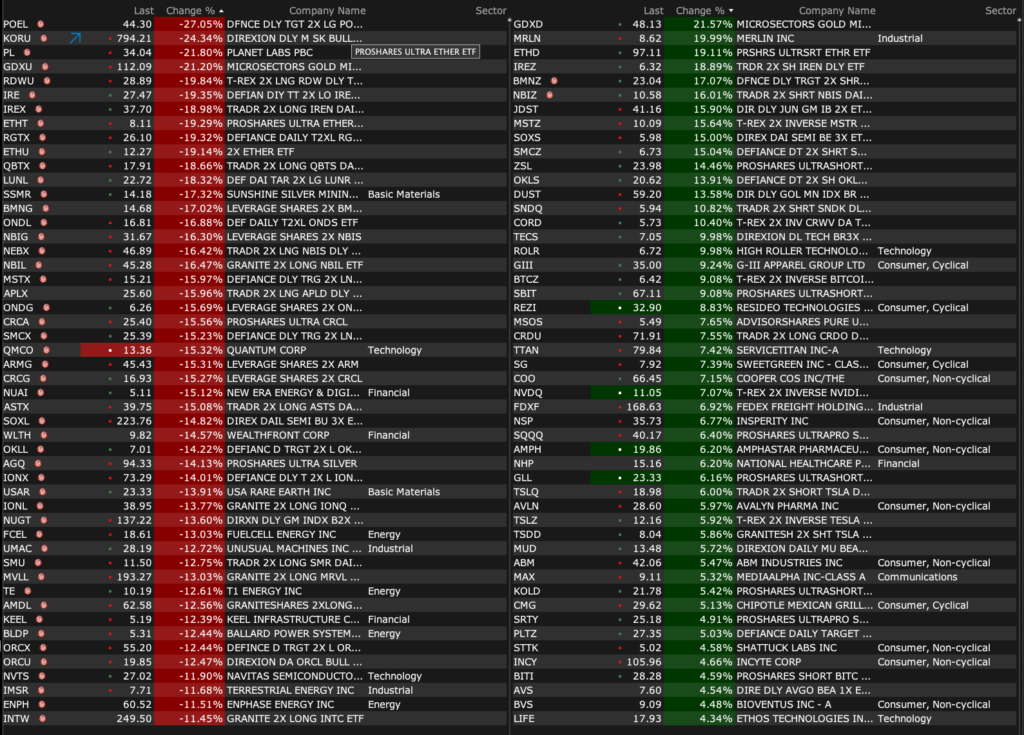

After-Hours % Advancers

After-Hours % Decliners

Position: None

BY Doug Kass · Jun 5, 2026, 4:35 PM EDT

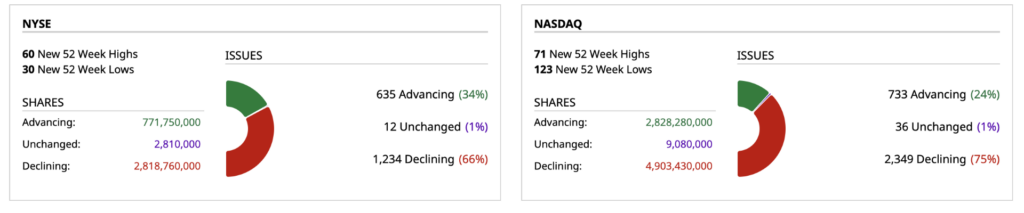

Closing Volume

– NYSE volume 1% below its one-month average

– NASDAQ volume 18% above its one-month average

– VIX index: up 36.36% to 21

Breadth

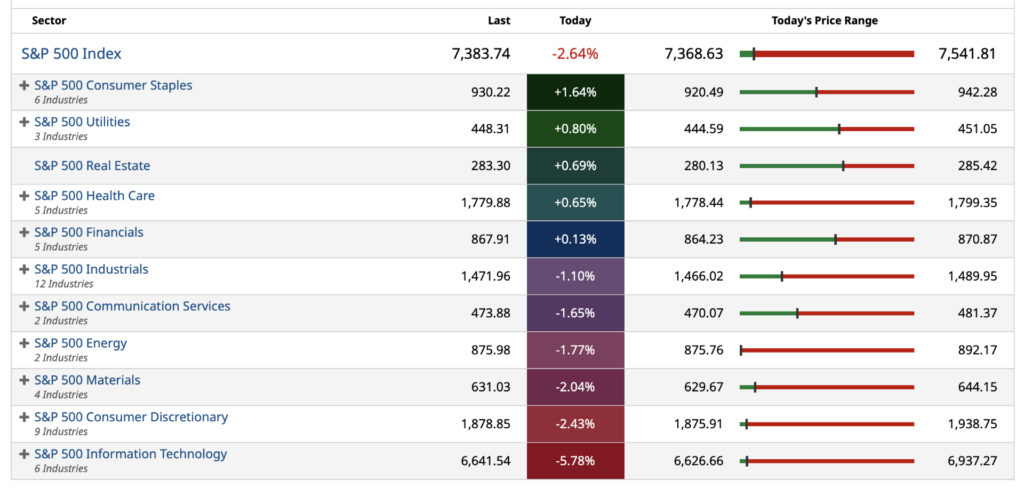

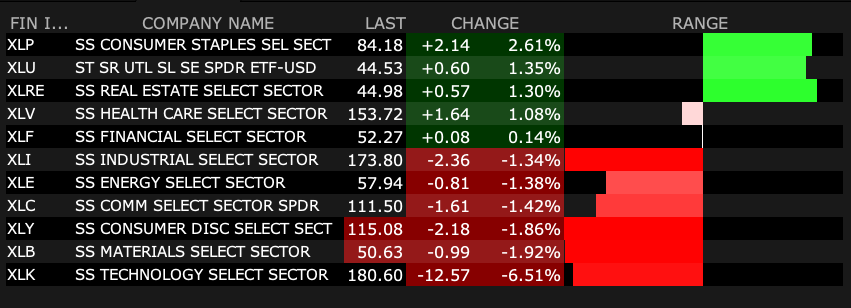

S&P 500 Sectors

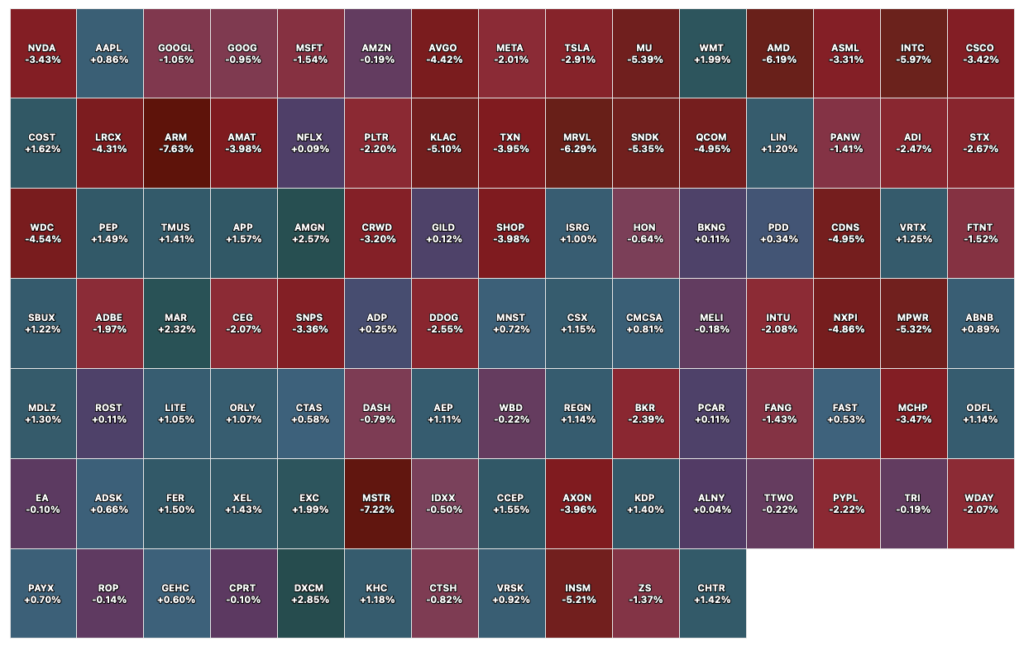

% Movers

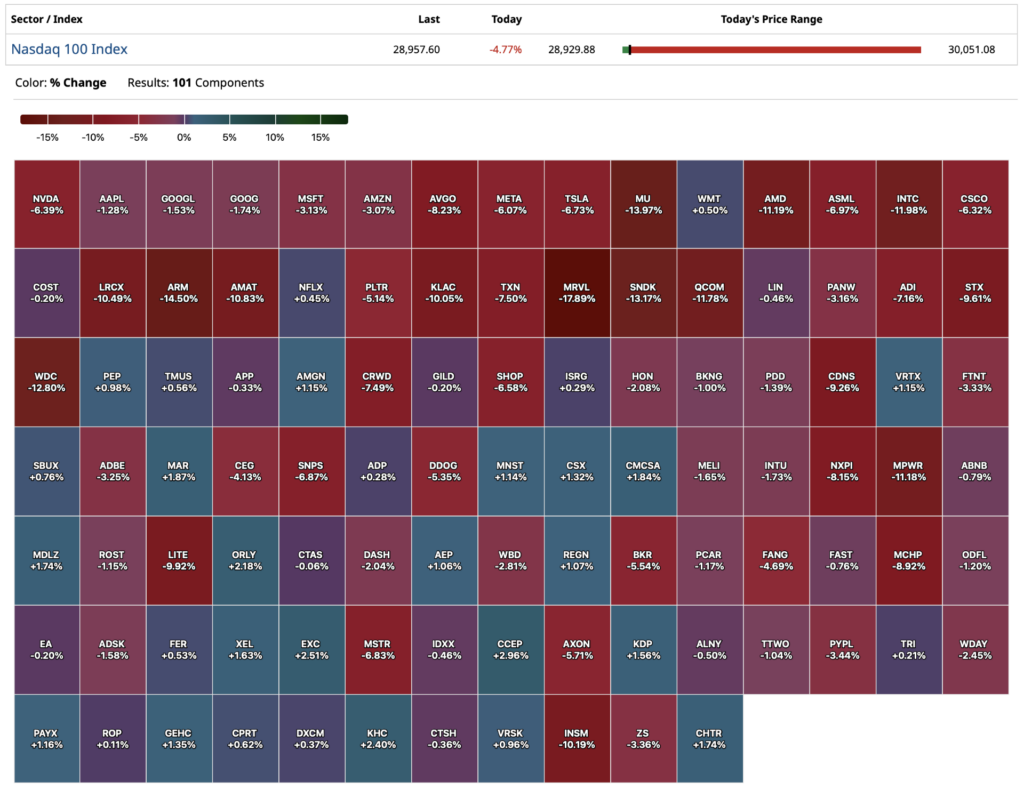

Nasdaq 100 Heat Map

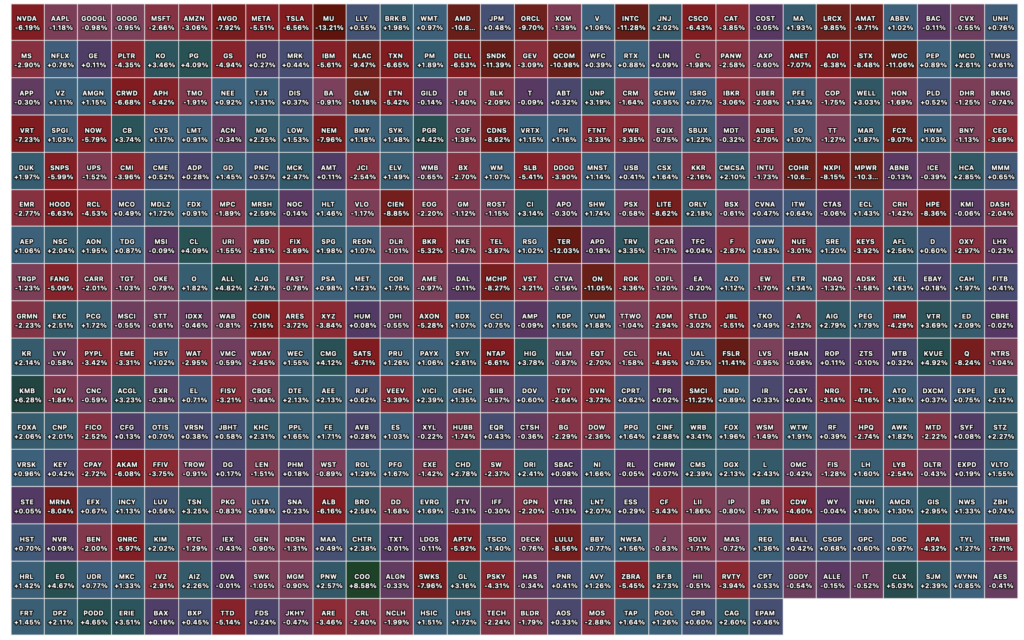

Closing S&P 500 Heat Map

Position: None

BY Doug Kass · Jun 5, 2026, 4:25 PM EDT

Position: None

BY Doug Kass · Jun 5, 2026, 4:08 PM EDT

From Peter Boockvar:

Positives,

1) Payrolls in May rose by 172k, well more than the estimate of up 88k and the two prior months were revised up by a total of 93k. A major factor at play was the 55k person increase in local government hiring. Also helping was the 70k hiring increase in leisure/hospitality, thanks in part to World Cup hiring vs the average monthly increase of 14k over the prior 12 months. Healthcare, again, the other major contributor, added 35k jobs, about in line with the average of 38k over the prior year. Elsewhere, the hiring was more mixed. The household survey said 149k jobs were new but which follows three months in a row of declines totaling 475k. The labor force grew by 83k and which combined, kept the unemployment rate unchanged at 4.3%. The all in U6 rate at 8.1% was down one tenth m/o/m. The participation rate held at 61.8%, the lowest since September 2021 but continued to be weighed down by retiring boomers. The participation rate for the 25-54 yr old group rose one tenth to 83.9%, just one tenth below from matching the highest since 2001. Hours worked remained at 34.3 while average hourly earnings grew by .3% m/o/m as expected and by 3.4% y/o/y. Combining the two saw weekly earnings higher by .3% m/o/m and 3.7% y/o/y.

2) The number of job openings in April jumped to 7.618mm, an increase of 752k from March and to the most since May 2024. Just about all of the increase in job openings came from just the ‘professional/business services’ line item which spiked by 668k.

3) The May ISM services index rose to 54.5 from 53.6 and that was above the estimate of a slight gain to 53.8. New orders rose to 57.3 from 53.5 after falling by 7 pts last month. Backlogs were above 50 for the 4th straight month at 51.3. Likely reflecting the pull forward of ordering I keep hearing about, the inventory component jumped by almost 10 pts to 62.5 matching the highest on record dating back to 1997 with this survey with May 2010 the only other time. Not confirming the jobs report, Employment remained a drag coming in at 47.9, little changed m/o/m but below 50 for the 3rd straight month. The ISM said “Respondents commented frequently that their companies had instituted hiring freezes or were not backfilling vacated positions, however, most industries reported that they were holding flat in employment month over month.” Prices paid remained high, rising by another .6 pts to 71.3 which is the most since August 2022. ISM said, “For the third month in a row, no commodities in the report listed as down in price, with multi month runs of being up in price for aluminum, copper, diesel, gasoline, software licensing and transportation.” With regards to sector breadth, 17 of 18 industries saw growth in May while just one experienced a contraction, that being in ‘real estate, rental & leasing.’ That compares with 14 industries seeing growth and 3 a downturn.

4) The May ISM manufacturing index rose to 54 from 52.7 and was 1 pt above the estimate. Strength in new orders helped again, rising by 2.7 pts m/o/m to 56.8 and backlogs were above 50 for the 5th month in a row at 52.2. Inventories got to 49.9, around the flat line but that is the highest since April 2025. Customer inventories remain well below 50 at 42.7 but that is the highest in 5 months. Employment was in contraction again at 48.6 but up 2.2 pts m/o/m. Industry breadth further improved with 16 of 18 industries seeing growth vs 13 in the two prior months. In December it was at just 2. One saw a contraction, ‘wood products’, vs 3 in April.

5) With the average 30 yr mortgage rate staying above 6.50%, at 6.57%, though down from 6.65% in the week before, purchase applications fell for the 4th week in the past 5, down another 2.9%. Refi’s were down by 2.3% w/o/w after dropping by 18% in the week before.

6) From Petco: To a question on their consumer, “I would remind you and everyone on the call for that matter that Petco serves customers across all income demographics. We have a really nice offering from both value all the way to premium brands. As we look back on the quarter, I would say there was nothing material amongst income demographics that performed differently. It was consistent across all. So in total, we didn’t see really any different change in behavior.”

7) From Macy’s: “In the first quarter, we delivered enterprise wide growth, better than expected performance across all key metrics and our best comparable sales in four years with all nameplates and channels positive.” They saw “widespread increases in new and retained customers as well as across all income cohorts.”

8) From Five Below: “The comp growth was disproportionately driven by transactions up 19% with ticket up 4%, reflecting strong traffic, customer engagement, and continued success in our value proposition across price points.”

9) From Dollar General: “We grew market share in both dollars and units in highly consumable product sales once again during the quarter, in addition to growing market share in non-consumable product sales.” Comps grew by 2% “primarily driven by customer traffic growth of 1.4%, and supported by average basket growth of .5 point. Notably, this marks the fourth consecutive quarter of growth in customer traffic as our combination of value and convenience continues to resonate with customers.” And in the search for value by everyone, “we are seeing customer penetration growth across low, middle and high-income segments, as customers across all income cohorts seek value at increasing rates. Notably, across these cohorts, the largest increase in customer count came from the highest income segment, which earns more than $100,000 annually, contributing to a significant increase in trade-in customer households during the quarter.”

10) From Signet Jewelers: “We delivered comp sales growth across every category and most brands this quarter…we continue to see strength in higher end consumer with some of our best performance at higher price points…By category, growth was low single digit for bridal and fashion with stronger growth in watches and services.”

11) From Victoria’s Secret: “We achieved our 4th consecutive quarter of positive comps with total comp sales increasing 13% and driving total sales growth of 15%. We also saw strength across channels and geographies. We were particularly encouraged by double digit gains in new customer acquisition and continued file growth across all age and income cohorts. In fact, we saw the strongest growth from customers and households earning under $50,000 annually and over $200,000, underscoring the broad resonance of our brands across the consumer landscape.”

12) From Ulta Beauty: “growth in the beauty category remains healthy, even as consumers are increasingly value focused…And while we are continuing to monitor how the macro landscape could evolve, we remain execution focused and are confident we will deliver our fiscal 2026 expectations.”

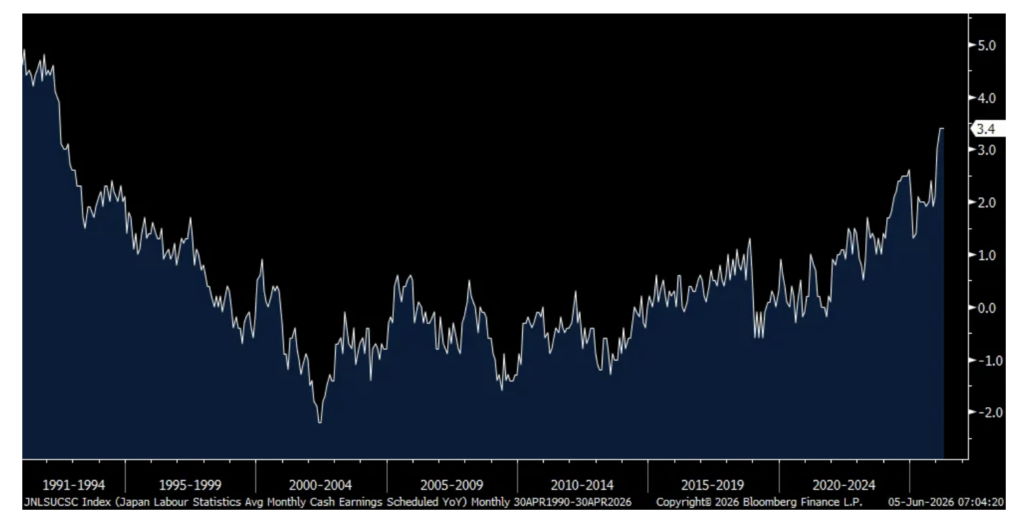

13) The Bank of Japan got another reason to hike rates after base pay in April rose 3.4% y/o/y for a 3rd straight month, staying at the highest since 1992.

14) China’s private sector weighted May services index rose to 54.4 from 52.6 and 2 pts above the estimate. RatingDog said “The faster increase in activity was accompanied by a further acceleration in the rate of growth in new business moving through the second quarter. The rate of expansion in demand for services accelerated for the fourth time in five months and was broadly in line with the long run survey averages. Increased client demand, business innovation and expansion, new client acquisitions, improved market conditions and the development of new projects were all mentioned as sources of new work.”

15) Manufacturing PMIs from overseas: Taiwan 56.1 vs 55.3 (certainly helped by TSMC) , South Korea 54.8 vs 53.6 (certainly helped by Samsung and SK Hynix) , Vietnam 52.8 vs 50.5, Japan 54.5 vs 55.1, Australia 50.7 vs 51.3, India 55 vs 54.7, Philippines 50.8 vs 48.3, the China state focused manufacturing was 50 vs 50.3 in April. The non-manufacturing PMI (including construction) was 50.1 vs 49.4. The PMI for Singapore’s service and manufacturing sector was 56.7 vs 57.9.

16) Eurozone manufacturing PMI in May was 51.6, above 50 for a 4th straight month. In the UK, it was 53.9 vs 53.7.

17) The Swiss National Bank will likely keep rates for now at zero after May CPI rose .6% y/o/y as expected with a core rate of up just .3%, also as estimated. The rise in fuel prices hasn’t had much of an impact, yet.

Negatives,

1) Initial jobless claims rose by 13k w/o/w to 225k and that was 10k more than expected. That helped to lift the 4 week average to 215k from 208k and also due to the print of 199k 5 weeks ago that dropped out. While still low, it’s the most since late February. Continuing claims totaled 1.777mm, little changed with the 1.785mm seen in the week before.

2) The NFIB yesterday released its small business May Plans to Hire in the coming 3 months figure and it fell to 9, down 4 pts m/o/m to the lowest level since May 2020 and matching the weakest since August 2014 before that. Also, job openings that could not be filled dropped 5 pts to also the lowest since May 2020 at 29%. The chief economist at the NFIB said, “Concerns about rising labor costs increased significantly to the highest reading in the survey’s history. Small business owners are facing mounting pressure to retain workers, and many firms are navigating costly new state mandates. While current conditions restrict Main Street’s already thin profit margins, compensation measures remain steady for now.”

3) In the April JOLTS data, the hiring rate though fell back to 3.2% after rising to 3.5% in March vs 3.1% in February. Outside of Covid, 3.1% was the lowest since 2011 for perspective. The quit rate fell to 1.9% which matches the smallest print since 2014, also not including Covid.

4) From the Fed’s Beige Book, “Economic activity increased at a slight to moderate pace for ten of the twelve Federal Reserve Districts, while one District reported a slight decline and one reported no change. On the biggest component of US GDP, “Consumer spending remained mixed across Districts and increasingly bifurcated across income groups amid affordability pressures. Higher-income households remained resilient and less sensitive to price increase, while middle-income households were described as “squeezing more life out of every dollar before deciding to spend it,” and low-income consumers showed greater financial strain. Overall, there were reports of increased credit card usage, fewer retail visits, and stronger demand for necessities. Auto dealers reported softer new vehicle demand tied to affordability and fuel costs, alongside substitution toward used and hybrid vehicles.”

5) Notwithstanding the strong payroll report, the Beige Book said: “Employment showed little to no change across eleven Districts, while one District experienced modest growth.” And, “Most Districts described a low-hire, low-fire environment, with workers increasingly reluctant to change jobs because of economic uncertainty. Hiring remained selective and primarily focused on critical roles or attrition replacement. Professional services occupations had mixed demand conditions, partly reflecting shifts in technological and operational changes.” Where there has been some growth, “Manufacturing hiring was the strongest sector in several Districts, supported by defense-related activity and rising data center demand.”

6) And on prices from the Beige Book: “Prices increased at a moderate to strong pace overall, with most Districts reporting higher inflation than the previous report. Districts noted that energy-related costs tied to the conflict in the Middle East were the primary driver of inflationary pressures, with spillovers into shipping, packaging, groceries, and fertilizer. Non-labor input costs continued to rise faster than selling prices, contributing to broader concerns about margin compression.”

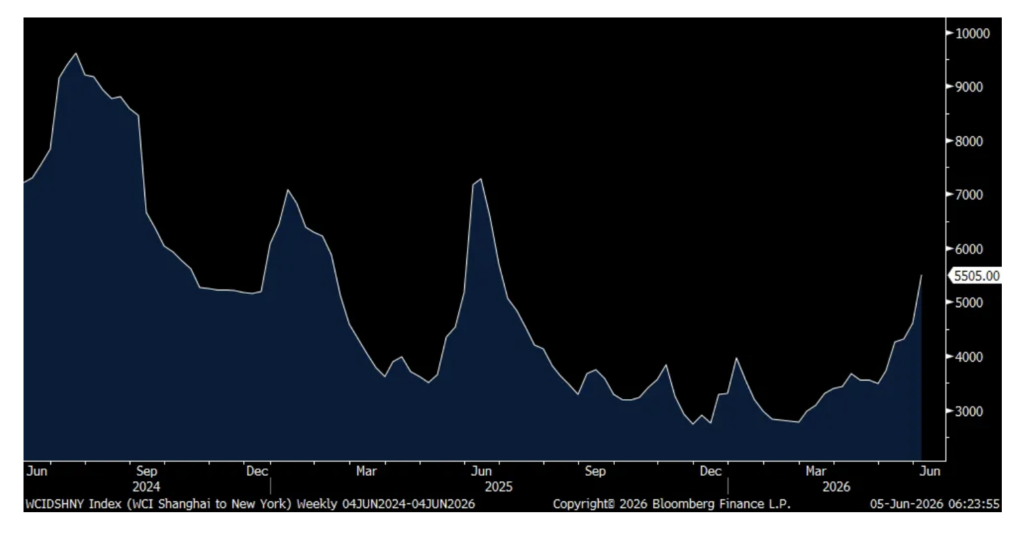

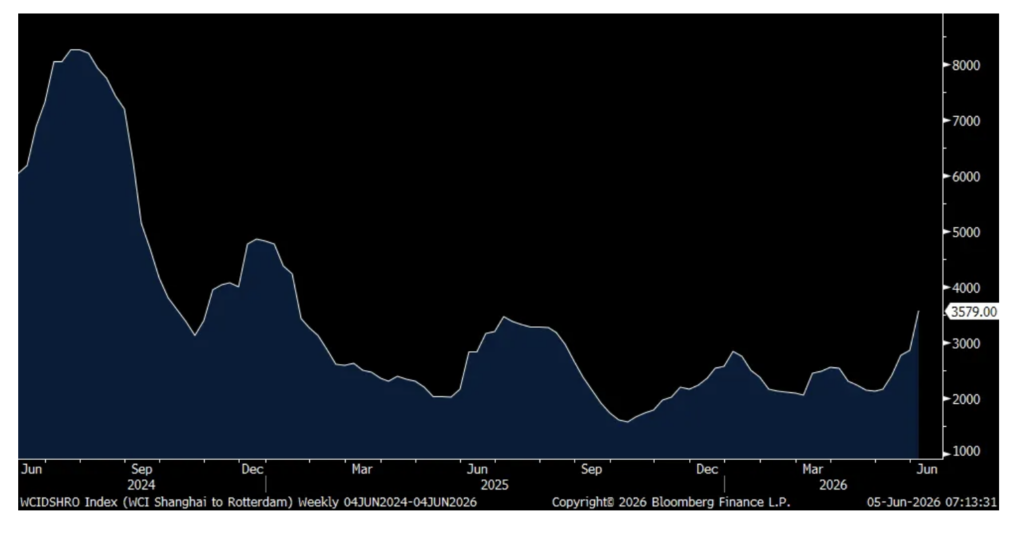

7) Container shipping prices jumped again according to the World Container Index. The Shanghai to NY route saw prices sharply higher by 20% w/o/w to $5,505, the highest in a year. The Shanghai to LA trip was 31% pricier w/o/w to $4,565, also the highest since June 2025. The price of a container from Shanghai to Rotterdam is the most since January 2025, up 25% w/o/w.

8) From the Logistics Managers Index: “Transportation Prices are up 1 pt to 96, which is the fastest rate of expansion ever recorded for any metric in the nearly ten year history of the index. Transportation Capacity continues to contract quickly at 31.7, and Transportation Utilization expansion remains elevated at 69.5. The transportation market has been tight, with prices growing at an unprecedented rate since the closure of the Strait of Hormuz. The spike in fuel has led to increases for all three of our price and cost metrics, with aggregate logistics costs reading in at 250.9, which is the highest reading since March of 2022.”

9) From S&P Global on US manufacturing: “At first glance, the manufacturing sector seems to be firing on all cylinders but lift the hood and the picture is not so clear…since the outbreak of war in the Middle East we have seen production and demand buoyed by stock building as companies worry over rising prices and supply difficulties. This stockpiling was again widely evident in May and makes it hard to take an accurate reading on the underlying health of the manufacturing economy, as growth will cool once this stock build has run its course.”

10) From Lululemon: “We saw encouraging signs in Q1 that reinforced we are moving in the right direction, but as we closed Q1 and entered Q2, we faced a few headwinds and a moderating sales trend. Based on our early analysis, there are two key factors impacting our trend. First, we experienced spikes of negative commentary in the media and on social channels with regard to our brand, which had an impact on traffic and overall top-line performance. And second, not all of our product launches have met our expectations.”

11) From Coca Cola: “we have spoken for a couple of years now, under the general headline of the consumer is resilient, that seems to pop up every quarter, that some of them are not as resilient as you think. And so segmenting populations, whether it’s in the US or whether it’s in China, is a very important capability to build, so that you have the opportunity to evolve your portfolio, to stay relevant with those segments that are under the most pressure…for people earning less than $50,000, $60,000 a year, when you take a step back and look at the cumulative impact of cost pressures on their typical basket of goods and services, the math is pretty obvious, it doesn’t work. They just don’t have the purchasing power to be able to, and so something’s got to go.”

12) From Ollie’s Bargain Outlet: “Touching on the consumer for a moment, customers are shopping closer to need more than ever before, but also remain resilient. In the first quarter, the environment shifted very quickly with surging gas prices impacting shopping patterns with a focus on trip consolidation. This primarily impacted the lower income consumer, particularly those driving longer distances to the store. We saw further strengthening of trade down, but typically in these moments of economic stress, lower income consumers trade out more quickly than upper income trade-in.”

13) From Five Below: And why the stock is likely down, “We’re very pleased with our Q1 performance and remain highly convicted in our ability to continue to generate durable, sustainable growth. At the same time, we remain cautious with respect to the macro environment, consumer sentiment, and buying behaviors. As such, we have left our half two comparable sales assumptions unchanged from our previous guidance.”

14) From Thor Industries: “At the end of our fiscal second quarter, we correctly identified the risk of geopolitical events having an adverse impact on the RV selling season. The consequences of this risk coming to fruition during our fiscal third quarter have exceeded the expectations of our industry due to the unforeseen duration of these macroeconomic influences and their impact on consumer sentiment and material costs. In particular, our North American Towable segment has confronted both suppressed volumes due to strained consumer sentiment and rising material costs brought on by tariff and inflationary pressures.”

15) From Shack Shack: “We are seeing some challenges in short to mid term on the cost side. Obviously, I think everyone is aware of the beef prices that we’re battling. They’ve continued to escalate. And we are also seeing fuel surcharge prices on some of our distribution and some of the other input costs in the middle of the P&L…there’s going to be some headwinds in the macro and we acknowledge that. And that’s part of what you see in the update and guidance today reflecting our views on the current cost structure and what our views are just given the competitive landscape and all the things that we know today.”

16) From Dollar General: “While there are a variety of puts and takes on customer budgets during Q1, our core customer continues to be financially constrained, as any benefit from tax benefits was largely offset by higher fuel prices and reductions in SNAP benefit payments. Importantly, while there has been a significant reduction in overall SNAP dollars distributed in 2026, we grew share of wallet with SNAP customers during Q1, further demonstrating the strength and relevance of our value proposition…Notably, during the quarter many of our core customers reported cutting back on other household expenses, including food purchases, due to rising gas prices. This pressure has been more pronounced on customers in rural communities as they work to minimize trip distance and make trade-offs in their search for everyday affordability and value.”

17) From Broadcom as sometimes great is not great enough: Their semiconductor business saw a sales gain of 79% y/o/y and of course, “Driving this growth was AI semiconductor revenue at a record $10.8 billion, up 143% y/o/y and above our outlook…Demand for XPUs and networking is simply insatiable.”

18) From HP Enterprises: “Demand was even stronger than revenue growth. Orders more than doubled, significantly outpacing revenue, resulting in a record company backlog. Customer investments in agentic AI and AI inferencing accelerated. We also saw broad based demand strength across the portfolio, driven by ongoing investment in compute infrastructure modernization, unstructured storage data growth, and private cloud adoption for AI.”

19) The revised service PMI’s for Germany, France, Italy and the UK all remained below 50 while Spain just got there at 50.1. The UK was close at 49.3. Not surprisingly, “Cost pressures in the service sector continued to increase, as they now have done in every month since the start of the war in the Middle East. Output charge inflation saw only a fractional uplift from April, however.”

20) The May Eurozone CPI was higher by 3.2% y/o/y and 2.5% at the core. The headline was as forecasted but the core rate was one tenth above and both compare with 3% and 2.2% in April. Of note, services inflation accelerated to a 3.5% y/o/y increase, matching the quickest since April 2025 while non-energy industrial goods prices rose .9% y/o/y, still benign but that is the fastest rate of change since Q1 2024.

21) South Korea reported May CPI that rose 3.1% headline y/o/y, two tenths more than expected and a core rate gain of 2.5% which was 3 tenths above the estimate.

Position: None

BY Doug Kass · Jun 5, 2026, 3:50 PM EDT

I have covered my shorts in GRNY at $26.88 and JOET at $44.25.

Position: None

BY Doug Kass · Jun 5, 2026, 3:39 PM EDT

BY Doug Kass · Jun 5, 2026, 3:37 PM EDT

I’m taking a small trading long rental in the indices:

* SPY $736.37

* QQQ $705.04

Position: Long SPY (VS), QQQ (VS)

BY Doug Kass · Jun 5, 2026, 3:29 PM EDT

At 2:55 PM:

Position: None

BY Doug Kass · Jun 5, 2026, 3:06 PM EDT

Dr Frankenstein: Now that brain that you gave me, was it Hans Del Brooks?

Igor: No.

Dr. Frankenstein: Would you mind telling me whose brain I did put in?

Igor: Abby someone.

Dr. Franksenstein: Abby, who?

Igor: Abby Normal – I am almost sure that was the name.

Dr. Frankenstein: Are you saying I put an abnormal brain into a 7 1/2 foot long, 54 inch wide gorilla?

– Young Frankenstein Abby normal scene

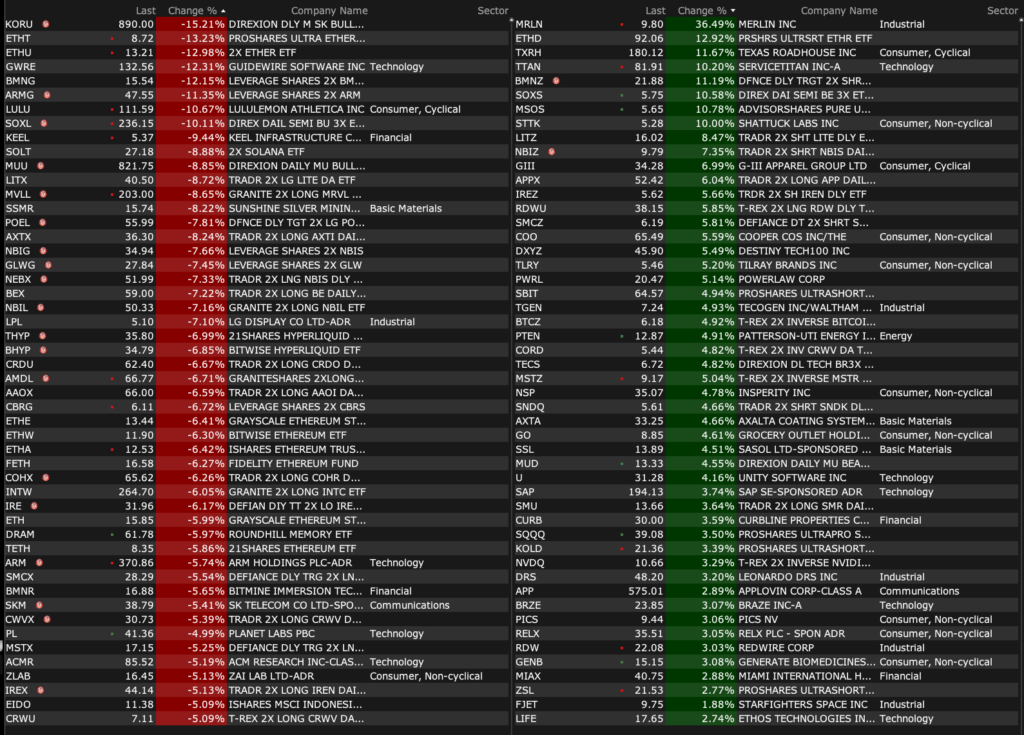

Consider the following price changes in today’s session:

* SNDK -$201

* MU -$101

* AMD -$51

* MRVL -$38

To me, this should make investors consider whether the market has been nothing more than a casino — in which the many momentum-based investors know everything about price but nothing about value.

And that, as I have observed, the concepts of risk vs. reward and “margin of safety” have been generally ignored.

Position: None

BY Doug Kass · Jun 5, 2026, 1:35 PM EDT

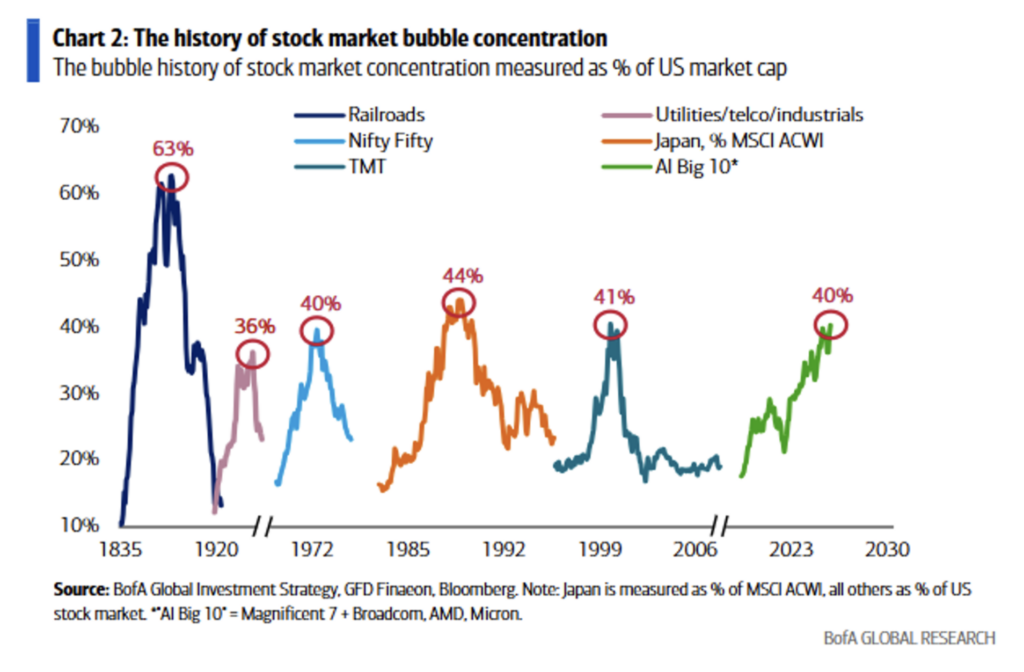

On The Death Star, Judge Wapner just refenced the chart contained in my “It Is Not Different This Time” post:

Position: None

BY Doug Kass · Jun 5, 2026, 1:05 PM EDT

Gord

HI Doug, any targets for MSOS? Thx G

Dougie Kass

i don’t do price targets. markets are dynamic and ever changing

there is a bearish view and a set of assumptions – yields price of $4

there is a base case view and a set of assumptions – yields $10-$15

there is a bullish view and a set of assumptions – yields over $20

Position: Long MSOS (M)

BY Doug Kass · Jun 5, 2026, 12:45 PM EDT

This is likely the reason for the last leg lower in equities:

Live updates: Iran war, Lebanon’s president speaks out, Hezbollah-Israel attacks | CNN

Position: None

BY Doug Kass · Jun 5, 2026, 12:31 PM EDT

For kicks and giggles, here is my negative market outlook from earlier this week:

Position: None

BY Doug Kass · Jun 5, 2026, 11:45 AM EDT

– NYSE volume 11% below its one-month average;

– Nasdaq volume 2% above its one-month average;

– VIX index: up 6.56% to 16.41

Positions: None.

BY Doug Kass · Jun 5, 2026, 11:17 AM EDT

From Peter Boockvar:

Payrolls in May rose by 172k, well more than the estimate of up 88k and the two prior months were revised up by a total of 93k. A major factor at play was the 55k person increase in local government hiring. Also helping was the 70k hiring increase in leisure/hospitality vs the average monthly increase of 14k over the prior 12 months. Healthcare, again, the other major contributor, added 35k jobs, about in line with the average of 38k over the prior year.

Elsewhere, the hiring was more mixed. Jobs were lost in retail, financial services and information. Professional/business services, the sector that saw the huge jump in job openings in April, added 6k jobs vs 22k in the month before. On the goods side, manufacturing added 7k people and construction hired a net 17k, both most likely tied to the AI buildout.

The household survey said 149k jobs were new but which follows three months in a row of declines totaling 475k. The labor force grew by 83k and which combined, kept the unemployment rate unchanged at 4.3%. The all in U6 rate at 8.1% was down one tenth m/o/m.

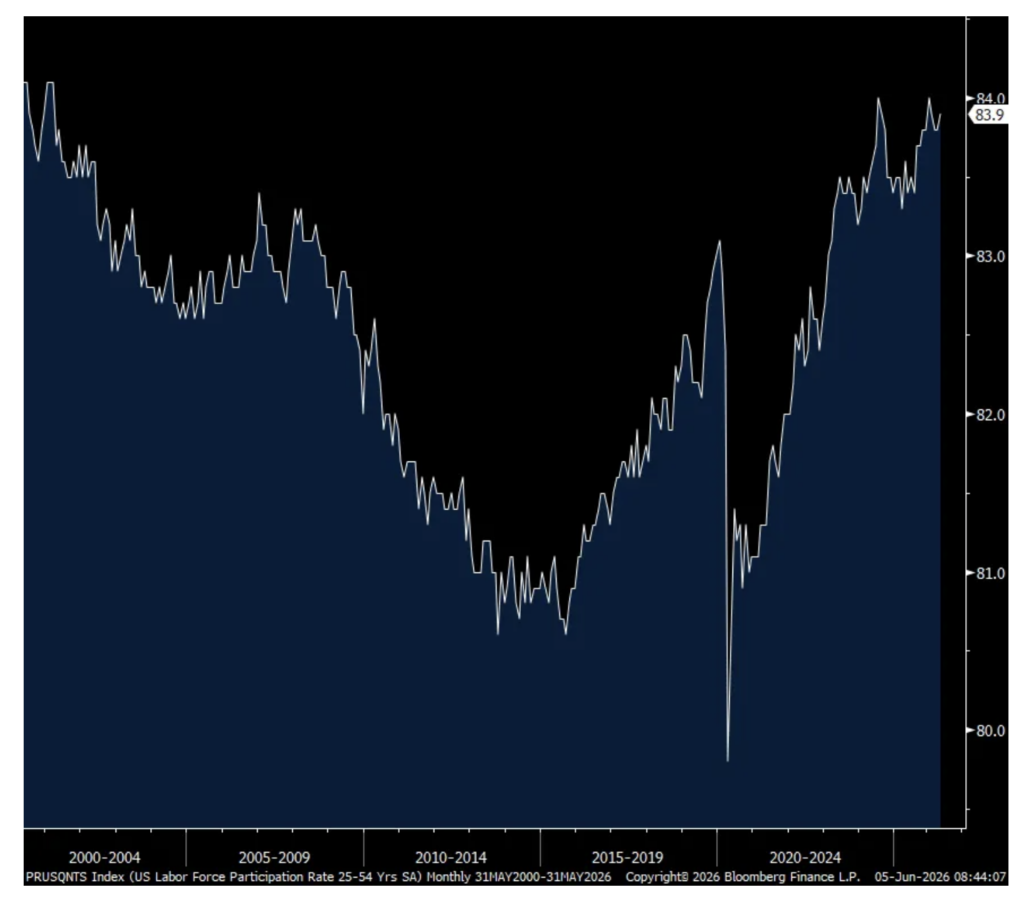

The participation rate held at 61.8%, the lowest since September 2021 but continued to be weighed down by retiring boomers. The participation rate for the 25-54 yr old group rose one tenth to 83.9%, just one tenth below from matching the highest since 2001. Hours worked remained at 34.3 while average hourly earnings grew by .3% m/o/m as expected and by 3.4% y/o/y. Combining the two saw weekly earnings higher by .3% m/o/m and 3.7% y/o/y.

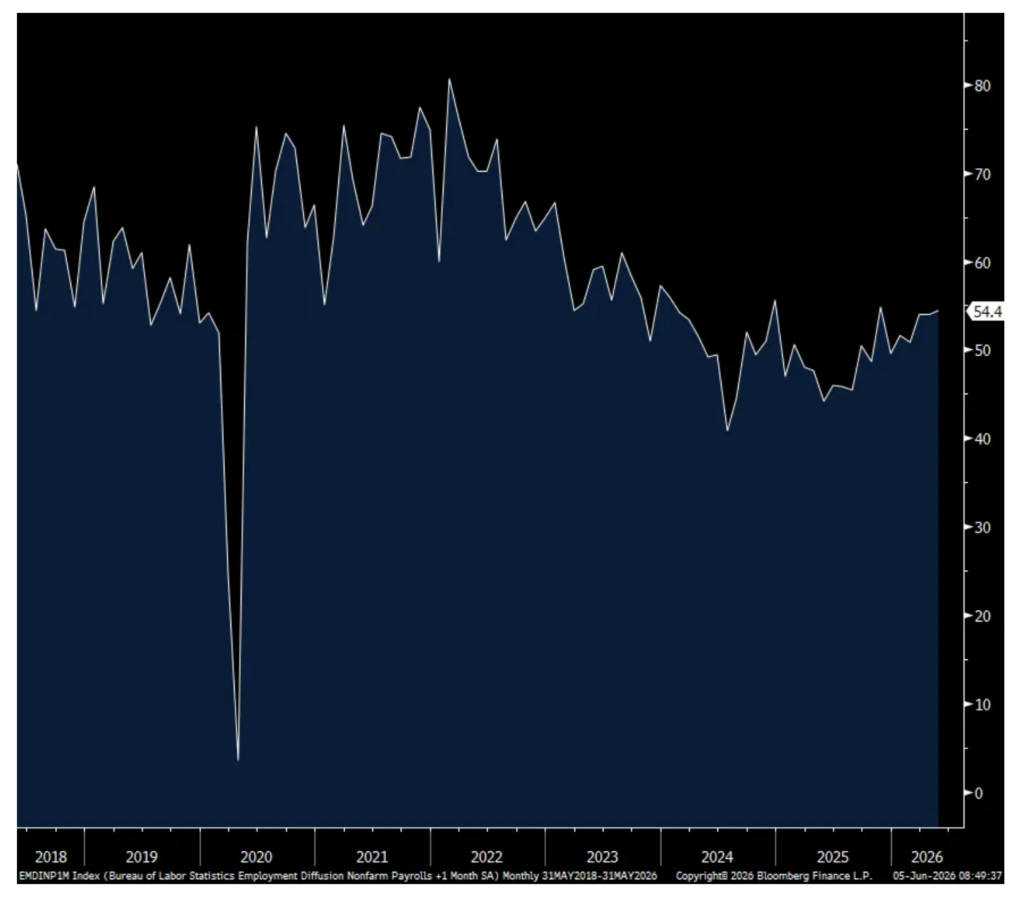

Measuring the breadth of hiring is seen in the diffusion index and it ticked up to 54.4 from 54 and which compares with 54.2 in January 2020. That’s the highest since December 2024.

Bottom line, the data center construction, along with the demand for healthcare workers and leisure/hospitality drove most of the job gains. Because of the local government hiring pop, I’ll do the monthly averages with just the private sector. The 3 month average is 166k vs the 6 month average of 87k and the 12 month average of 56k. Thus, a clear pick up over the past few months and why interest rates are jumping in response with the 10 yr yield back above 4.50% and the 30 yr above 5.00%. The 2 yr yield is having the biggest move, jumping 10 bps to 4.14%. While I don’t think the fed funds futures are that relevant in pricing in rate moves until we hear from Kevin Warsh in a few weeks, it is currently pricing in an 88% chance of one rate hike by yr end.

25-54 yr old Participation Rate

Diffusion Index

Positions: None.

BY Doug Kass · Jun 5, 2026, 10:24 AM EDT

Positions: None.

BY Doug Kass · Jun 5, 2026, 9:54 AM EDT

From Peter Boockvar:

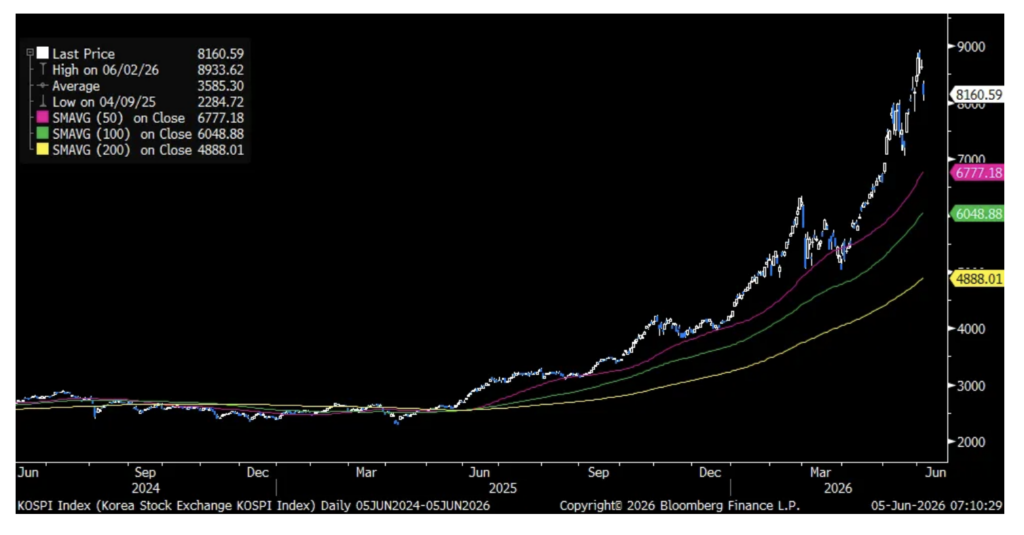

After waking up each day for a while to see first thing what JGB yields were doing overnight, it’s now watching how the South Korean Kospi traded. It fell by 5.5% after falling by 2.8% Thursday but still is up 94% year to date because of Samsung and SK Hynix which dominate the index, as we know.

Kospi

Ahead of today’s May jobs report, the NFIB yesterday released its small business May Plans to Hire in the coming 3 months figure and it unfortunately fell to 9, down 4 pts m/o/m to the lowest level since May 2020 and matching the weakest since August 2014 before that. Also, job openings that could not be filled dropped 5 pts to also the lowest since May 2020 at 29%.

The chief economist at the NFIB said, “Concerns about rising labor costs increased significantly to the highest reading in the survey’s history. Small business owners are facing mounting pressure to retain workers, and many firms are navigating costly new state mandates. While current conditions restrict Main Street’s already thin profit margins, compensation measures remain steady for now.”

Plans to Hire

Container shipping prices jumped again according to the World Container Index. The Shanghai to NY route saw prices sharply higher by 20% w/o/w to $5,505, the highest in a year. The Shanghai to LA trip was 31% pricier w/o/w to $4,565, also the highest since June 2025. The price of a container from Shanghai to Rotterdam is the most since January 2025, up 25% w/o/w.

Shanghai to NY

Shanghai to Rotterdam

I’ve expressed my positive stance many times on certain commodities/stocks and want to again mention platinum after the article in the WSJ I read yesterday titled “Sticker shock at the pump fuels a surge in hybrid sales.” The article said “Hybrid cars and trucks are now hotter than ever. Elevated gas prices…helped drive a 33% jump in hybrid sales in May compared with last year, according to data from Motor Intelligence – a bright spot in the otherwise stagnant new-car market.”

Why does this matter for platinum? A hybrid vehicle uses 10-15% more platinum than that used in an internal combustion engine auto. We are long platinum.

Platinum

Something I mentioned a few months ago that the current situation in the Persian Gulf and Hormuz Strait was going to completely alter the logistical waterway to make sure the current situation never happens again. And when done, Iran will lose all its leverage over the Strait of Hormuz. In case you didn’t see this article in the WSJ yesterday titled “The Hormuz squeeze is redrawing the oil map for good.” The piece said, “Across the Gulf, governments are pouring billions into new oil pipelines, rail corridors and energy storage hubs to bypass the waterway in what is set to become one of the most durable outcomes of the conflict. The new energy links are part of a broader redrawing of the region’s logistics map, shifting trade toward trucking, rail and new ports.”

To some company notables.

From Lululemon, trading down 13% pre-market:

“We saw encouraging signs in Q1 that reinforced we are moving in the right direction, but as we closed Q1 and entered Q2, we faced a few headwinds and a moderating sales trend. Based on our early analysis, there are two key factors impacting our trend. First, we experienced spikes of negative commentary in the media and on social channels with regard to our brand, which had an impact on traffic and overall top-line performance. And second, not all of our product launches have met our expectations.”

Coca Cola’s CFO had some interesting comments at the Deutsche Bank conference yesterday and a stock we own:

“I think the narrative on the consumer being resilient is a nuanced narrative because they’re not all the same. We have segments of our consumer base around the world that are under pressure, and we have a choice to stay relevant with them or not. Longer-term, the equation to have a more active and large consumer base, in our view, is the one that is going to create the most value longer term.”

“we have spoken for a couple of years now, under the general headline of the consumer is resilient, that seems to pop up every quarter, that some of them are not as resilient as you think. And so segmenting populations, whether it’s in the US or whether it’s in China, is a very important capability to build, so that you have the opportunity to evolve your portfolio, to stay relevant with those segments that are under the most pressure.”

“for people earning less than $50,000, $60,000 a year, when you take a step back and look at the cumulative impact of cost pressures on their typical basket of goods and services, the math is pretty obvious, it doesn’t work. They just don’t have the purchasing power to be able to, and so something’s got to go.” And a Coca Cola product they want to be the last to go.

The Bank of Japan got another reason to hike rates after base pay in April rose 3.4% y/o/y for a 3rd straight month, staying at the highest since 1992. Nothing market moving though today as JGB yields and the yen are little changed.

Base pay y/o/y

Positions: None.

BY Doug Kass · Jun 5, 2026, 9:45 AM EDT

Adding to (VRNO).

Positions: Long VRNO S

BY Doug Kass · Jun 5, 2026, 9:38 AM EDT

* Wells Fargo lowered the firm’s price target on PepsiCo to $150 from $160 and keeps an Equal Weight rating on the shares. There is much noise in the macro, likely impacting the consumer and thereby PepsiCo’s categories, the firm says. The company’s execution, namely in Food, has been good in spots, Wells acknowledges, adding that the reality is nevertheless that accelerating sales through 2026, a goal for PEP, feels tough and debate on long-term North America growth likely sustains.

* Citi lowered the firm’s price target on Winnebago to $29 from $30 and keeps a Neutral rating

Positions: Short WGO VS

BY Doug Kass · Jun 5, 2026, 9:36 AM EDT

-MRLN +32% (completes Critical Design Review for C-130J Autonomy Program with USSOCOMCDR approval)

-BCDA +21% (receives FDA minutes saying CardiAMP Heart Failure II Trial may support PMA for ischemic HFrEF)

-TTAN +14% (earnings, guidance)

-GIII +7.6% (earnings, guidance)

-COO +7.1% (earnings, guidance)

-AGX +6.0% (earnings, color)

-U +4.5% (hearing boutique firm raises rating)

-AXTA +3.9% (hearing RBC Capital raises price target)

-APP +2.7% (hearing boutique firm raises rating)

-GWRE -12% (earnings, guidance)

-KEEL -11% (announces pricing of upsized $400M convertible senior note offering)

-LULU -11% (earnings, guidance)

-BMNR -5.6% (prices upsized Series A perpetual preferred stock offering of 3.5M shares at $80/shr)

-DOCU -4.5% (earnings, guidance)

-INIO -4.1% (lower following IPO yesterday)

-INTC -3.8% (profit taking in chips)

-MRVL -3.6% (profit taking in chips)

-IOT -3.2% (earnings, guidance)

Positions: None.

BY Doug Kass · Jun 5, 2026, 9:18 AM EDT

Positions: None.

BY Doug Kass · Jun 5, 2026, 8:55 AM EDT

Positions: None.

BY Doug Kass · Jun 5, 2026, 8:40 AM EDT

Positions: None.

BY Doug Kass · Jun 5, 2026, 8:30 AM EDT

This was from late May, and I’m repeating for emphasis:

I am growing much more optimistic on the cannabis complex.

I plan to super-size my MSOS holdings and I plan to expand individual equity positions (with emphasis on GTBIF, GLASF, TSNDF and VRNO).

Verano Holdings (VRNO) remains my favorite stock in the sector with the best risk/reward proposition.

I am optimistic on the cannabis space because:

* I am extremely confident that rescheduling of both medical and adult use (recreational) will pass in the next few months.

* I am confident that uplistings will soon follow.

* More relaxed custodian rules allowing for institutional purchases of the group.

* The recent debt refinancings have eliminated the frightening debt maturity cliff that some feared.

* Industry fundamentals (volumes and pricing) have stabilized.

* Expectations are very low.

* Massive absolute and relative underperformance over the last five years has created a long runway for appreciation.

* Upside reward is probably more than 5x downside risk.

Position: Long MSOS M VRNO S TSNDF S GLASF S GTBIF S

BY Doug Kass · May 27, 2026, 4:33 PM EDT

BY Doug Kass · May 28, 2026, 6:40 AM EDT

“Welcome to “What Are We Doing” (WAWD), the Substack newsletter where Wall Street outsiders—Danny Moses, Vincent Daniel, and Porter Collins, famously portrayed in “The Big Short” pull back the curtain on markets and investing.”

– Danny, Vinnie and Porter

There are few smarter and contrarian investors than Danny Moses, Vincent Daniel and Porter Collins.

Read on:

They Look at Me Like It’s Christmas and I’m Santa Claus

Position: Long MSOS M GLASF S

BY Doug Kass · May 28, 2026, 7:15 AM EDT

BY Doug Kass · Jun 5, 2026, 8:18 AM EDT

* This is an epic and very positive industry development

In what could be the second most important development for the cannabis sector EVER (the first one being rescheduling)… Trulieve has just announced that its shares have been approved for listing on the New York Stock Exchange. Trulieve Announces Uplist to NYSE – Jun 5, 2026

This approval will likely accelerate resolution of long standing custodian issues that have plagued the sector as well as providing the foundation for institutional ownership.

I can’t overstate the importance of this development.

Not up in smoke.

Positions: Long MSOS M TCNNF S

BY Doug Kass · Jun 5, 2026, 8:05 AM EDT

* Uplistings will reprice cannabis stocks higher and likely lead the way to institutional ownership

* I am growing more bullish on the cannabis space — having repurchased MSOS on Wednesday

* MSOS and Trulieve’s shares moved higher yesterday on moves aimed by TCNNF to facilitate NYSE uplisting

* Expect other MSOS to uplist in the months ahead

* I added to VRNO yesterday (and I will do more today) — it’s my favorite risk/reward candidate (and one of the more probable other uplisting candidates)

On Wednesday I stepped up and repurchased MSOS (at around $4.75). Here is what I wrote two days ago:

I don’t think today’s decline in cannabis stocks makes much sense.

I have gotten aggressive with MSOS on a scale lower.

My average cost is about $4.76.

Position: Long MSOS (M)

BY Doug Kass · Jun 3, 2026, 3:52 PM EDT

Yesterday MSOS had an outsized move to the upside ($4.72 to $5.10), likely because of Trulieve’s (TCNNF) move (its shares rose by +14%) aimed at a NYSE listing:

Trulieve Restructures Business in Move Tied to NYSE Listing Application

and…

and…

On Tuesday I wrote an upbeat weed column that emphasized that uplistings could be a catalyst for the cannabis sector:

* The Likely Memeification of Cannabis Stocks

“I never make plans that far ahead.”

– Casablanca (Rick’s response when Ilsa asks, “Will I see you tonight?”)

The animal spirits are on overload.

Market participants are grabbing at anything AI, space, memory, semis, etc. Parabolic moves have become common place. In the extreme, Jensen Huang mentions Marvell (MRVL) favorably and the shares rally by nearly +$70.

With the likely rescheduling of weed, likely uplistings (on major U.S. exchanges), settling of custody issues and emergence of institutional buyers (unleashing an abundance of buying power), I am increasingly of the camp that cannabis stocks could be memeified with such powerful changes ahead in the reasonably near term.

I add daily to VRNO – my favorite on a risk/reward basis.

Position: Long MSOS (M), VRNO (S) TCNNF (VS)

BY Doug Kass · Jun 5, 2026, 7:00 AM EDT

This SpaceX Pump Just Keeps Getting Uglier

Position: None

BY Doug Kass · Jun 5, 2026, 6:15 AM EDT

Yesterday’s rally was a head scratcher.

Today’s reversal in stock futures (S&P futures -40, Nasdaq futures -300) seems to be a function of several factors:

* Anthropic is calling for a global pause in AI development:

* SpaceX IPO issues:

and…

* A delayed reaction to the reemergence of private equity issues:

Meanwhile, the semiconductor/memory (heavily) weighted Kospi is much lower:

Asia tech stocks drop after Broadcom rattles AI trade and drags Wall Street names lower

Position: None

BY Doug Kass · Jun 5, 2026, 5:56 AM EDT

BY Doug Kass · Jun 5, 2026, 5:44 AM EDT

Just heard during a financial television interview on equity investing: “ANY pullback is an opportunity to buy.” This echoes quite a broad market belief -- conditioned by years of policy puts and outcomes-- that has increasingly ensured market corrections are remarkably limited Show more

The US jobs report for May is out, and it includes a big upside surprise on both 1. Job Creation: A significant beat at 172,000 versus the 88,000 consensus forecast (and a "breakeven" rate of ~50,000); and 2. Revisions: The previous two months were revised up by a substantial Show more

$tcnnf validates the uplist playbook @rivers_kim stockalpha.ai/alpha-breaking…

Looks like we’re on the way haters. the exchanges weren’t waiting for full legalization they were waiting for rescheduling medical is done. adult use hearing starts in 25 days. MSOs are doing reverse splits right now for a reason billion dollar companies trading on pink Show more

Kim and Trulieve want to be first to up-list in their own self interest. Truly believe this has zero bearing on what the outcome of the ALJ will be. If you read the filings this deconsolidation can be unwound swiftly. $MSOS

Anthropic is calling for top AI labs to weigh slowing the pace of development, suggesting that AI systems are advancing so rapidly that they may soon be able to improve themselves without human intervention in ways that could pose societal risks. on.wsj.com/4ulkmFh

JUST IN 🚨: S&P Dow Jones will not change rules to make it easier for SpaceX $SPCX to get fast track entry into the S&P 500 $SPX 🤯👀 Show more

Wow, the S&P Dow Jones Indices has just officially announced that they will NOT be changing their inclusion rules to make it easier for “MegaCap” companies (such as @SpaceX) to be fast-tracked into the S&P 500. Their reasoning: "S&P DJI determined that exceptions to the