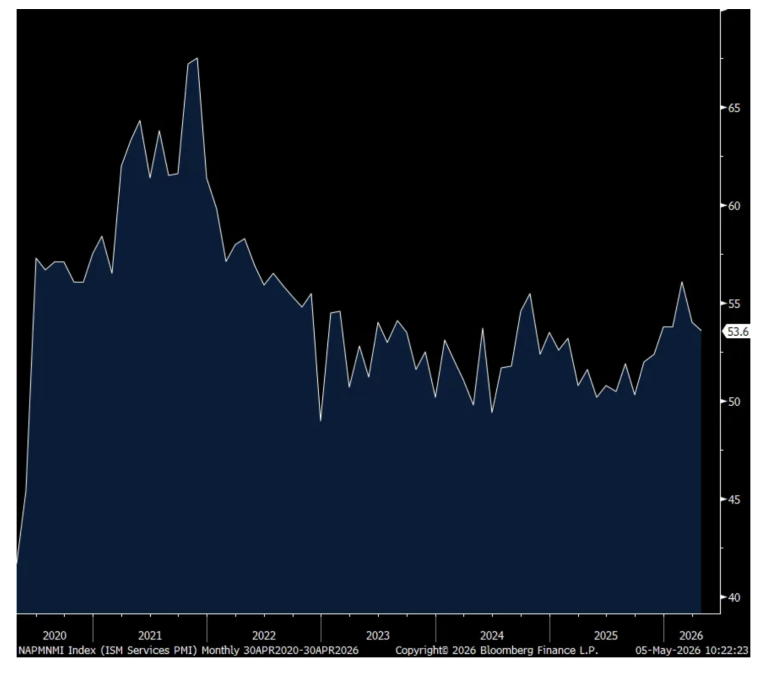

The April ISM services index fell a touch to 53.6 from 54 in March and about as expected. The Business Activity did lift by 2 pts but after falling by 6 in March and the rest of the internals were pretty mixed.

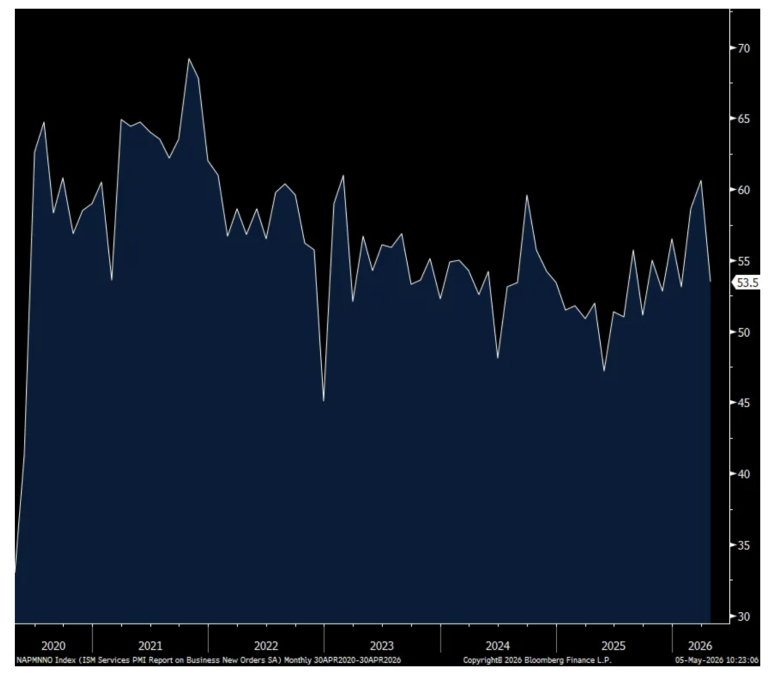

New orders dropped by 7.1 pts m/o/m to 53.5 while backlogs slipped by .6 pts at 53. Inventories remained above 50 but declined by 1.7 pts to 53.1. Said by ISM on new orders, “Everything is higher, because orders are trying to be placed before prices go higher” and “Middle East conflict is creating demand for domestic products.”

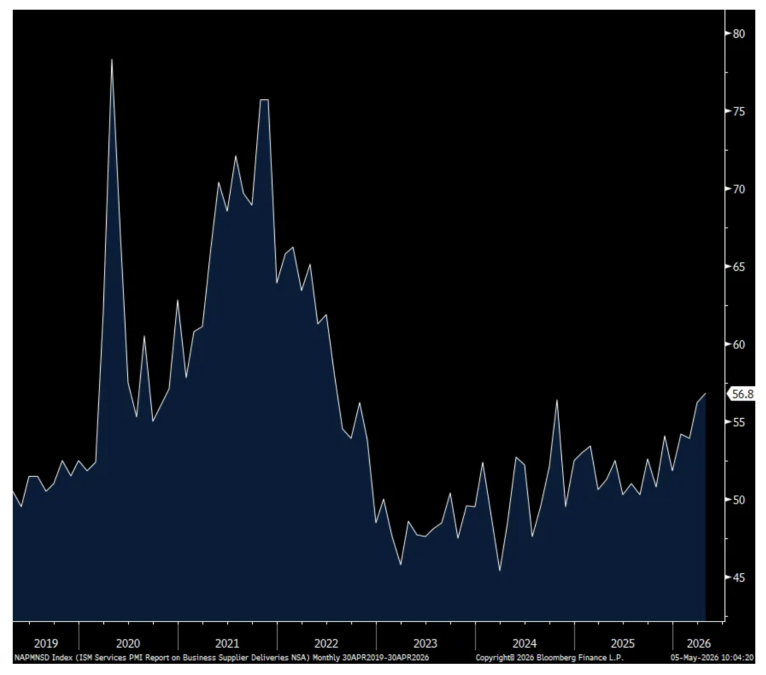

Reflecting growing supply chain issues, Supplier Deliveries rose .6 pts to 56.8 (reflecting longer lead times and slower deliveries), the highest since July 2022. ISM said, “Generally same delivery performance; however, we are expediting deliveries out of the Middle East conflict zone” and “Supplier deliveries have slowed slightly, reflecting transportation delays, longer lead times for certain materials, and ongoing supply chain adjustments.”

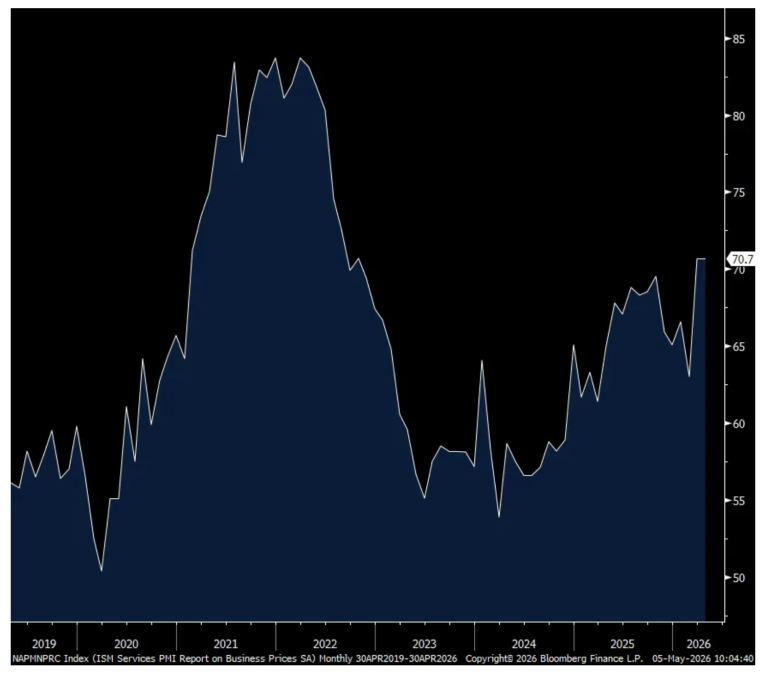

Prices paid were little changed but held at the highest since October 2022 and all 18 industries surveyed paid higher prices. The ISM said this on pricing, “For the second month in a row, there are no commodities in the report listed as down in price, with aluminum, copper, lumber, petroleum products and software licensing continuing multi-month runs of being up in price. There were several comments from respondents stating that they have yet to see petroleum price increases impacting petroleum-related products, so we expect to see continued elevated readings for the Prices Index for several months — regardless of when the conflict in Iran ends — due to these costs working their ways through global supply chains.”

Also of note, the unemployment component stayed below 50 for the 2nd month but less so at 48.2 vs 45.2 in March and vs 51.8 in February.

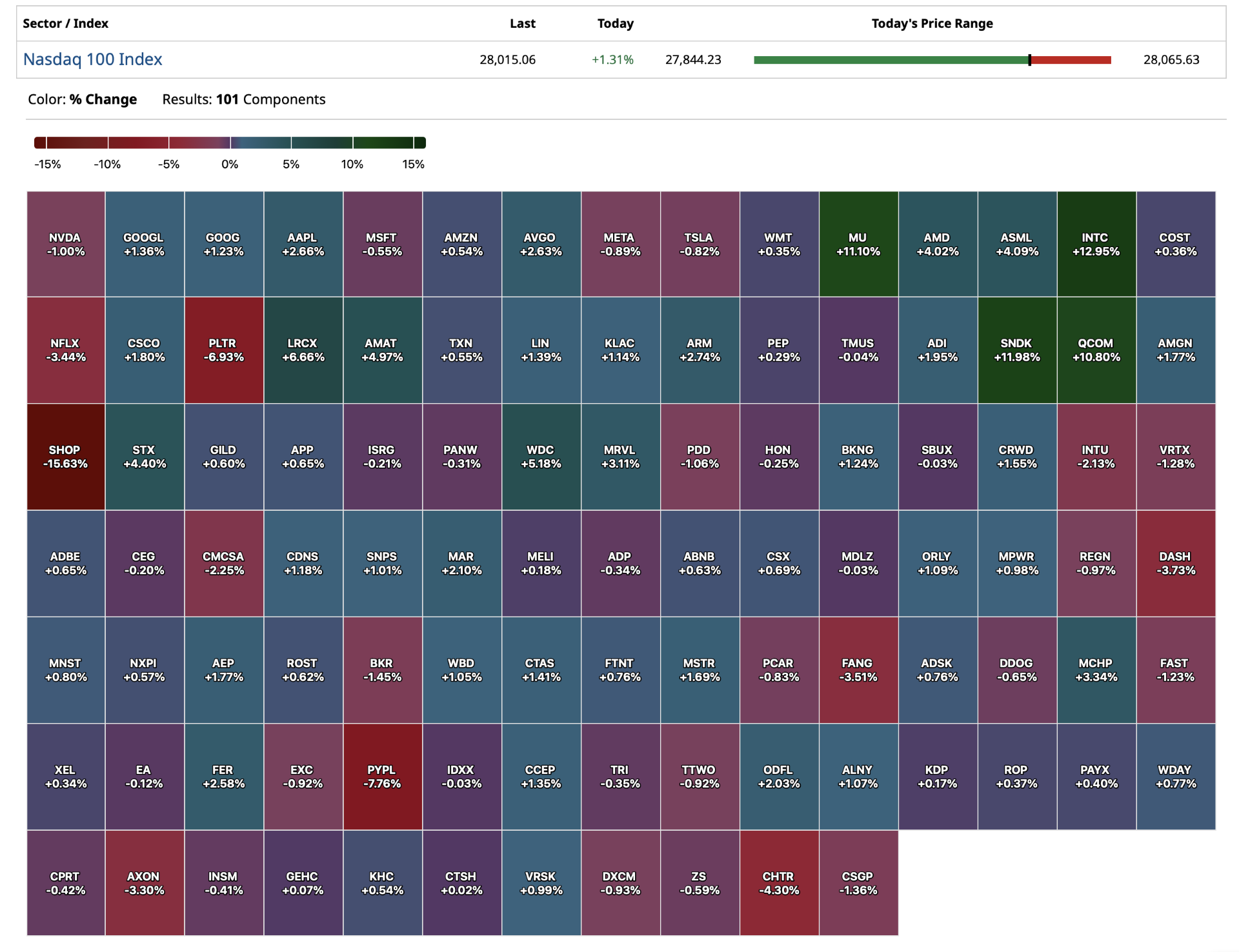

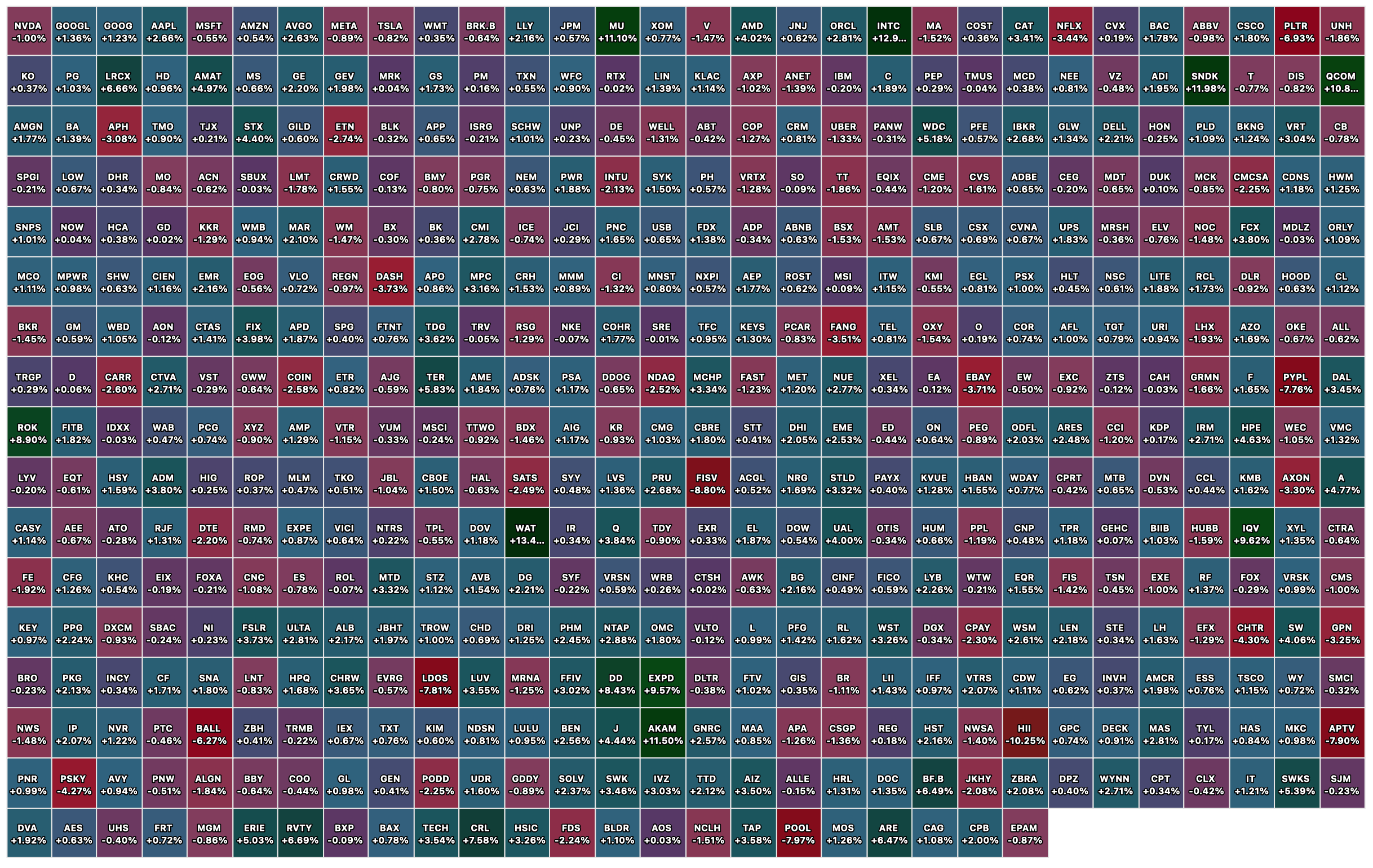

With respect to industry breadth, 14 of 18 industries reported growth and 3 are in contraction. That compares with 13 up and 3 down in March with the balance seeing no change in business.

Bottom line, I think it’s clear that there is a pull forward of ordering going on in both the manufacturing and service space ahead of higher prices and/or supply delays. To what extent will only be known after but I’m hearing more stories of this. ISM said this, “Ongoing commentary that increased ordering is related to getting ahead of future price increases seems to have been more applicable to March than April; however, the Backlog of Orders Index remained in expansion territory, well above its 12-month average of 46.4 percent.”

The respondent comments were a mixed bag as to be expected. This quote from a company in the sector of Mgmt of Companies & Support Services stood out to me, “The war has caused many banking customers to back off equipment purchases and other spending. Just as the recovery was under way, it is now turning off. Not a good thing.”

· “Spring selling season for the homebuilding construction market is here, but interest rates, inflation, and oil supply issues are keeping buyers on the fence. Discounts and rate buy-downs remain the driver of sales, as affordability continues to be the hinderance for buyers. Cost cutting and value-engineering have reduced costs to pre-coronavirus pandemic levels, but inflation and rising oil prices threaten that hard work. Fuel surcharges, previously whispers, have become requests.” [Construction]

· “First quarter 2026 finished strong for tertiary care and beat revenue expectations by 6 percent, patient volumes remain strong, and labor is holding steady. Despite macroeconomic concerns, supply chains remained resilient, yielding few significant back orders and functioning quite well compared to expectations. Geopolitical concerns remain in play for the near term, though thus far have had little if any impact on operations. Forecast is good for the next quarter.” [Health Care & Social Assistance]

· “The war has caused many banking customers to back off equipment purchases and other spending. Just as the recovery was under way, it is now turning off. Not a good thing.” [Management of Companies & Support Services]

· “For ongoing projects, we are anticipating a 7 percent to 9 percent increase in expenses, primarily driven by the current local political environment. While projects in Western Hemisphere markets remain relatively stable in the short term, the broader global geopolitical landscape is expected to exert pressure over the medium to long term. We estimate that market normalization and cost recovery will require approximately 12 to 18 months.” [Mining]

· “Our services sector continues to expand, supported by strong new orders, but softer employment and rising input costs are shaping a more cautious outlook. Clients are prioritizing efficiency, risk management and strategic advisory, driving sustained demand across our core accounting and consulting offerings.” [Professional, Scientific & Technical Services]

· “Bracing for significant impacts due to increasing fuel costs. Expenditures for city fleet have increased, and we are starting to see fuel surcharges from suppliers. Actually, we are surprised that supplier fuel surcharges have not been more robust.” [Public Administration]

· “Housing sales slowed in March, and the residential real estate market is still well below historical norms. If sales continue at the current rate for the rest of 2026, 3.98 million homes would be sold, the lowest since 1995. A prolonged conflict could maintain structural pressure on rates for 12 to 18 months.” [Real Estate, Rental & Leasing]

· “Current business conditions continue to place pressure on purchasing operations due primarily to ongoing supply chain volatility, elevated transportation costs and inflation-driven pricing from key suppliers.” [Transportation & Warehousing]

· “Business conditions in the transmission and distribution utility sector remain stable to slightly expanding, supported by ongoing grid modernization and infrastructure investment. Activity continues to be influenced by tariffs and elevated input costs, particularly in copper, aluminum, and steel, which are driving sustained pricing pressure across key materials. Supply chain conditions have improved modestly; however, lead times for critical equipment remain extended. Utilities are mitigating risk through early procurement, supplier diversification and strategic inventory positioning. The overall outlook remains positive despite cost and supply pressures.” [Utilities]

· “Activity level and project activity remains high in most verticals. Data centers are front and center and show no signs of slowing down.” [Wholesale Trade]

Global bond yields/Gold/Depreciation is still a cost/Chicken

I think more attention than is being paid should be on rising global bond yields. The Reserve Bank of Australia raised rates again by 25 bps as expected to 4.35%. That now takes back all of their cuts that they started to implement in February 2025 after the aggressive hiking seen in 2022 and 2023. Governor Bullock said “One reason to increase interest rates was to give ourselves space now to sit and see what happens. We feel we’re now in a position where we’ve got space, to be alert now to both sides of the risks to inflation - upside and downside.” After this hike, they are most likely on hold for now and Aussie yields were little changed in response. The Aussie$ is just off a 4 yr high vs the US dollar, also benefiting from being considered a commodity currency.

Also last night, Senior Deputy Governor of the Bank of Korea said “It’s time to consider stopping rate cuts, and thinking about increases.” As mentioned yesterday too, an ECB member said it’s inevitable that rates will rise in June but we’ll have to see on that.

The 10 yr UK gilt yield is jumping by 12 bps to 5.08%, a fresh 18 year high.

To the question I get often, when will stocks care about rising rates. I of course can only guess and I’d say if we got above 4.50% in the 10 yr yield, which I think is going to happen with an eventual retest of 5%.

RBA Cash Rate

Gold continues to digest the big move seen in 2025 and early 2026 but the secular trend of central bank buying remains intact as I mentioned last week with the fresh Q1 World Gold Council data. H/t too to my friend David Rosenberg for this quote seen over the past few days from the Governor of the National Bank of Poland who has been a major buyer of gold over the past few years:

“Recent market developments, driven by the instability in the Middle East, have reinforced our view that instability has become the defining feature of the global economy. I would reiterate the importance of diversifying foreign reserves and the role of gold as a strategic asset.” We remain long physical bullion and the miners.

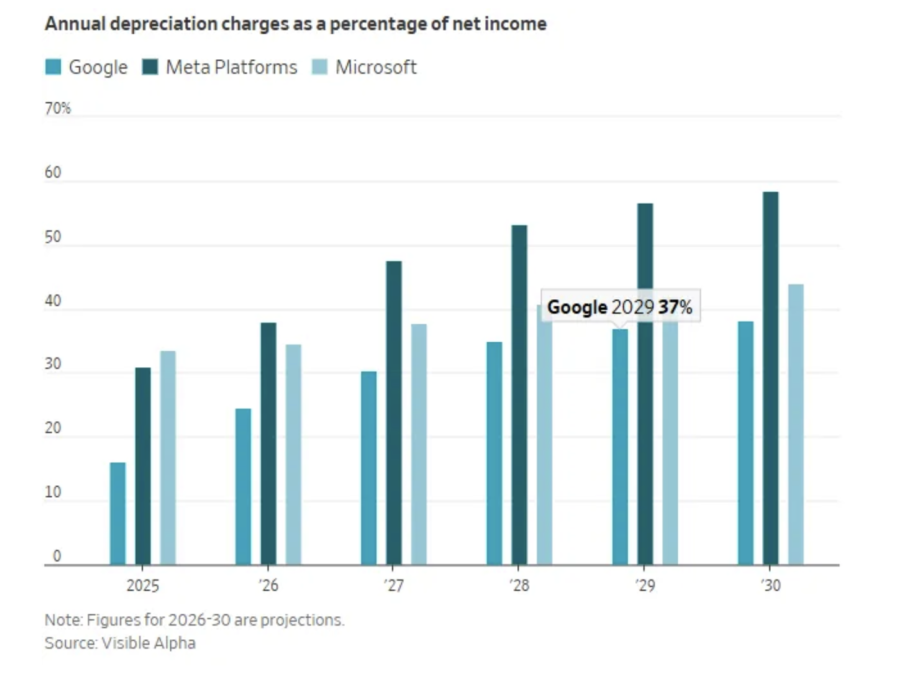

This was a great chart I saw Friday, post the earnings from the big hyperscalers, as it reflects the expense of depreciation that they will face in an increasing fashion in the years to come. The recipients of massive CapEx, especially semiconductors, are a growing cost over time for the spenders.

I forgot to mention yesterday April auto sales seen Friday that totaled 15.92mm at a seasonally adjusted annualized rate (SAAR) and that was just under the estimate of 16mm. Last April sales jumped to 17.3mm as many front ran tariffs and it is still below the 16.4mm seen pre Covid in April 2019. Affordability continues to be a growing issue as the average price of a vehicle is now around $50,000.

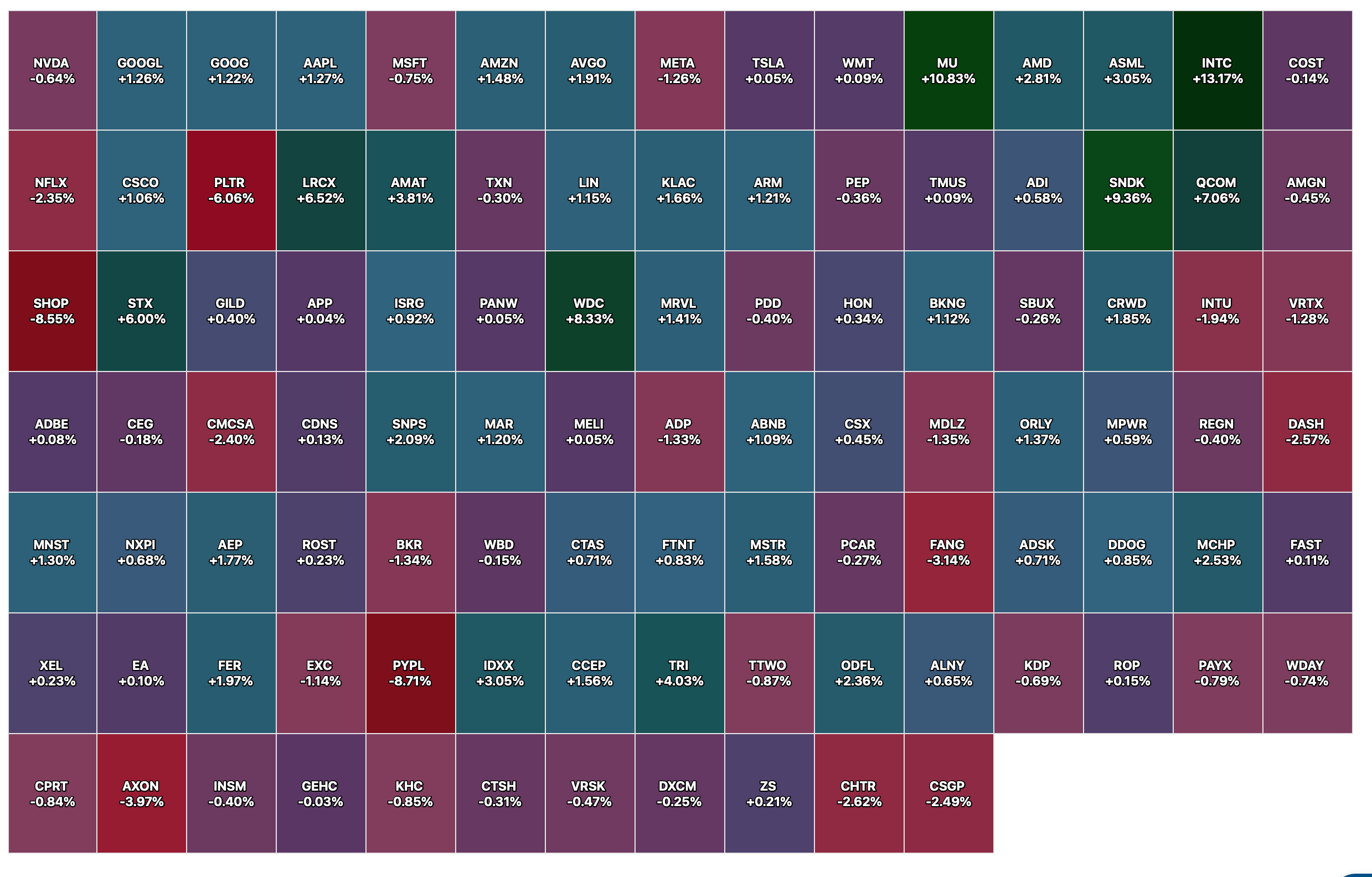

On Semiconductor is trading down pre market but was optimistic on their call:

“Turning to the demand environment, we saw a clear improvement as the quarter progressed, with strengthening order patterns and an increase in short lead time orders. Taken together, these signals give us confidence that this cycle has found its low point, and we are now on a path to recovery.”

They have more of an industrial base than others as customers but “we now expect our AI data center revenue to double y/o/y in 2026. As the only broad based US power semiconductor supplier, OnSemi continues to build a leading position in AI data centers across the full set of power capabilities required to modernize the power tree, including high voltage conversion, intelligent power stages, protection and control, and system level integration from the grid to the processor.”

In their automotive business, sales were flat q/o/q but up 5% y/o/y. “We continue to see stabilization in the automotive market and we now believe we’re shipping to natural demand. China electric vehicle programs continue to outperform other regions driven by a strong export market.” There industrial business was about in line with expectations.

From Tyson Foods:

“Animal protein remains top of mind for consumers and continues to gain momentum as a foundational part of a healthy diet. We are directly tied to and stand to benefit from this long term trend...Consumers are choosing protein, and they’re leaning into brands they trust for quality, taste and convenience.”

“Demand remains robust...Overall, y/o/y chicken volume was up 1.7% with retail and foodservice volumes growing nearly three times faster than total volume, reflecting momentum with our strategic customers. Importantly, these results were not driven by broad price increases, with base pricing being slightly lower in the quarter, but rather we saw improvements in product mix and executed well operationally.”

On their beef business and the higher costs, “We continue to expect results below historical margin levels until cattle supplies normalize.” They said their pork business, “performed well in a stable operating environment.” And, “Pork’s relative value to beef is likely to benefit revenue for the balance of the year.”

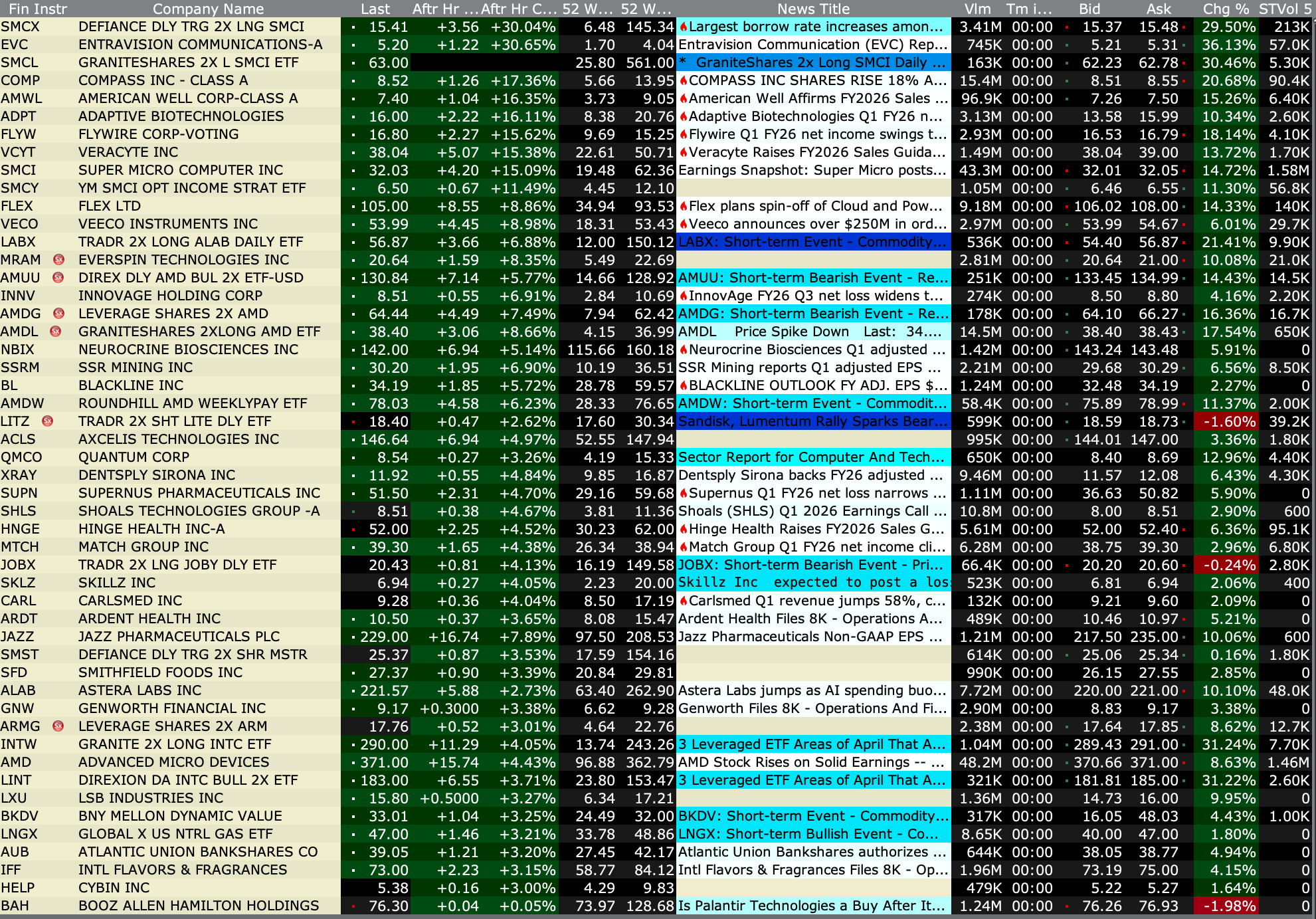

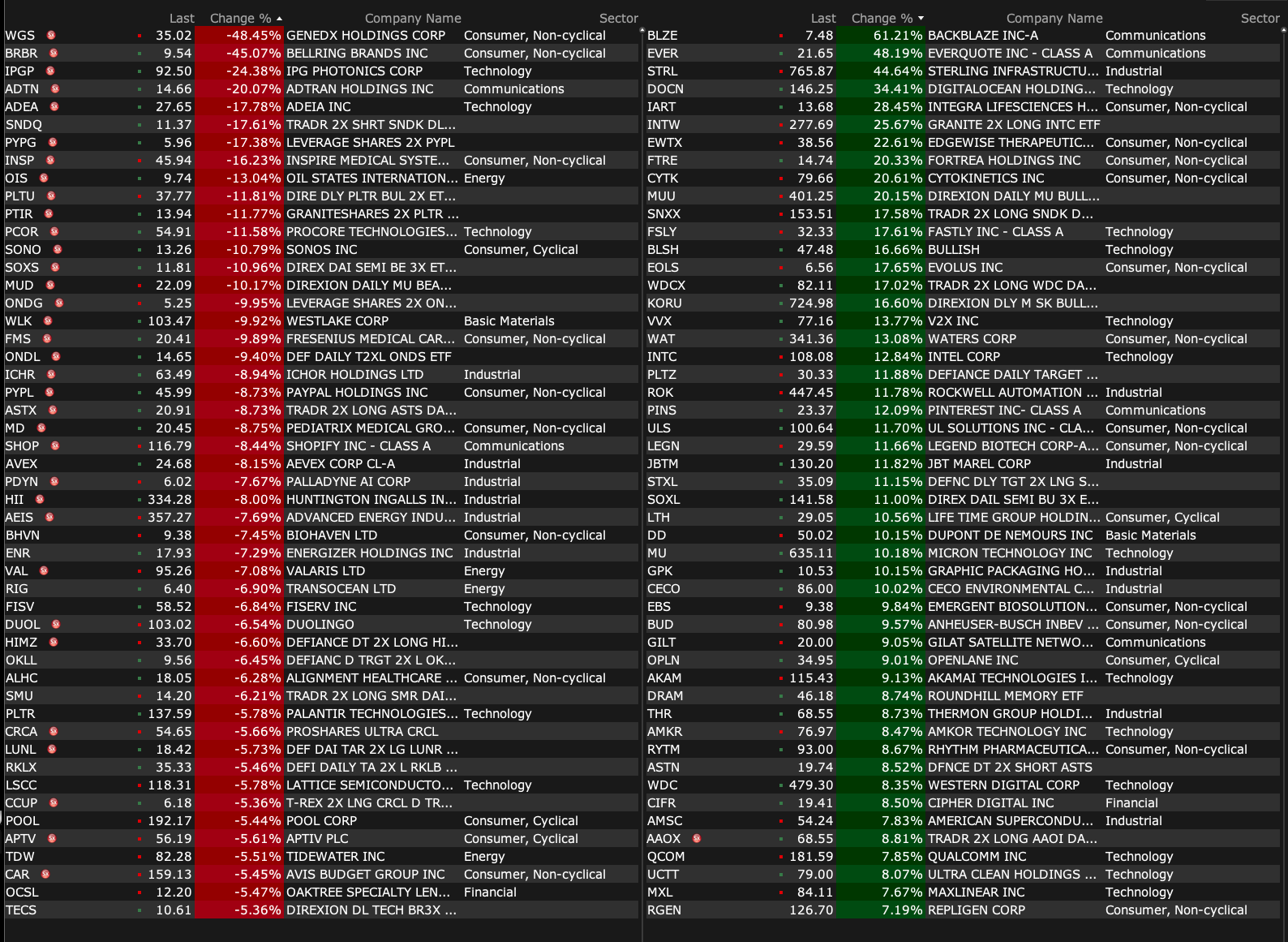

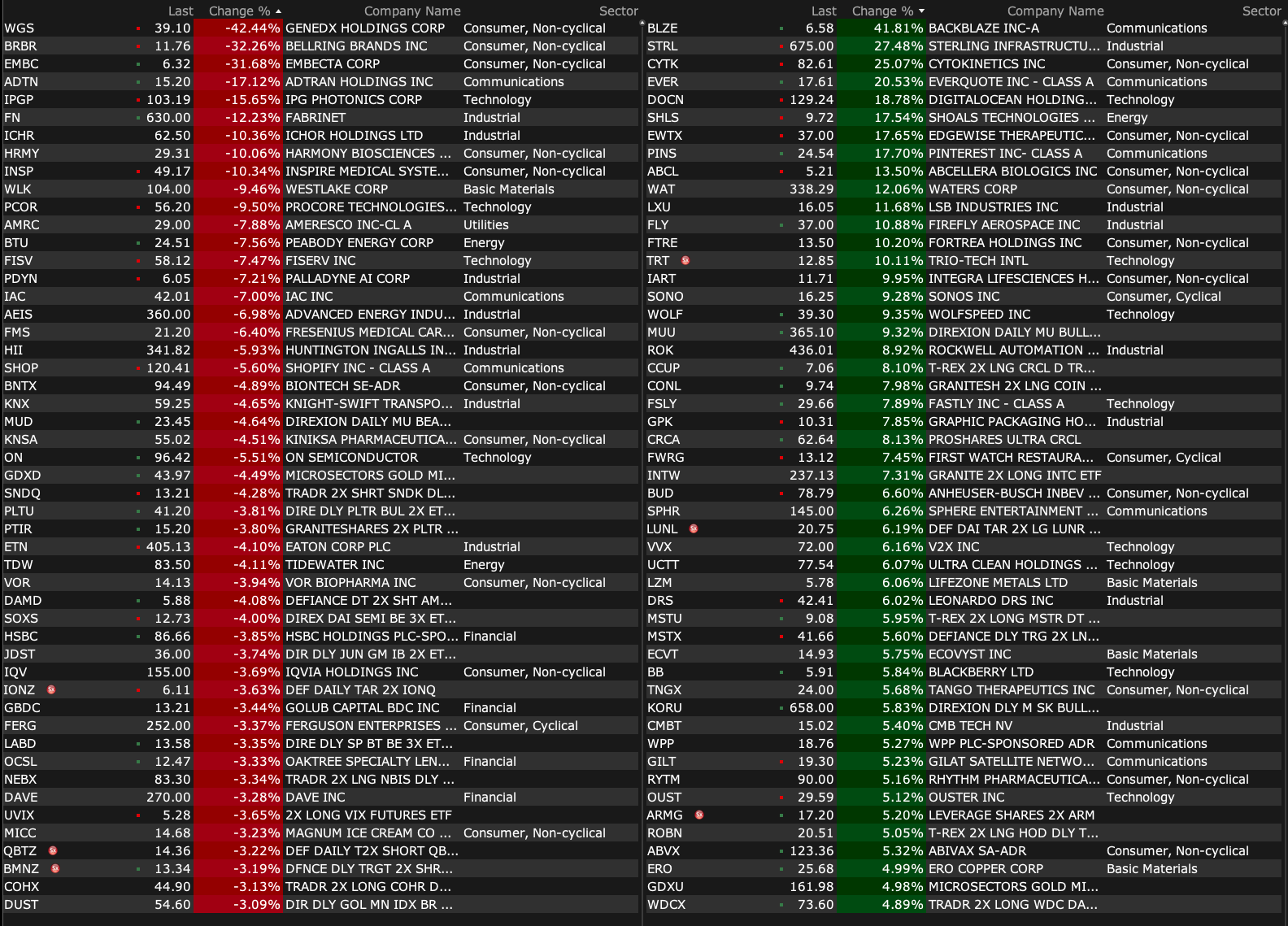

-DGXX +63% (signs AI colocation agreement with Cerebras)

-FSEA +44% (to be acquired by Cambridge Financial Group at $17.25/shr cash)

-STRL +29% (earnings, guidance)

-VRDN +24% (REVEAL-2 met primary endpoint with highly statistically significant treatment effect in Chronic Thyroid Eye Disease)

-CYTK +22% (ACACIA-HCM, Pivotal Phase 3 Clinical Trial of Aficamten in Patients with Non-Obstructive Hypertrophic Cardiomyopathy, met both dual primary endpoints and key secondary endpoints)

-DOCN +18% (earnings, guidance)

-SHLS +18% (earnings, guidance)

-FATE +11% (selected for U.S. FDA Chemistry, Manufacturing, and Controls Development and Readiness Pilot Program to Support Manufacturing Readiness of FT819 for treatment of moderate to severe systemic lupus erythematosus (SLE))

-ROK +8.9% (earnings, guidance)

-RYTM +7.5% (earnings, guidance)

-GDC +6.5% (receives prelim non-binding Going Private proposal at $10.75/shr)

-EXPD +4.5% (earnings, color)

-TDG +4.1% (earnings, guidance)

-INTC +4.0% (Apple said to be exploring using Intel and Samsung to build ‘main’ device processors)

-CMI +3.9% (earnings, guidance)

-COIN +3.9% (cutting workforce by 14%)

-IDXX +3.9% (earnings, guidance)

-ENR +3.2% (earnings, guidance)

-BLSH +3.0% (acquires Equiniti for $4.2B all-stock transaction)

-LTH +2.8% (earnings, guidance)

-TRI +2.4% (earnings, guidance)

Downside:

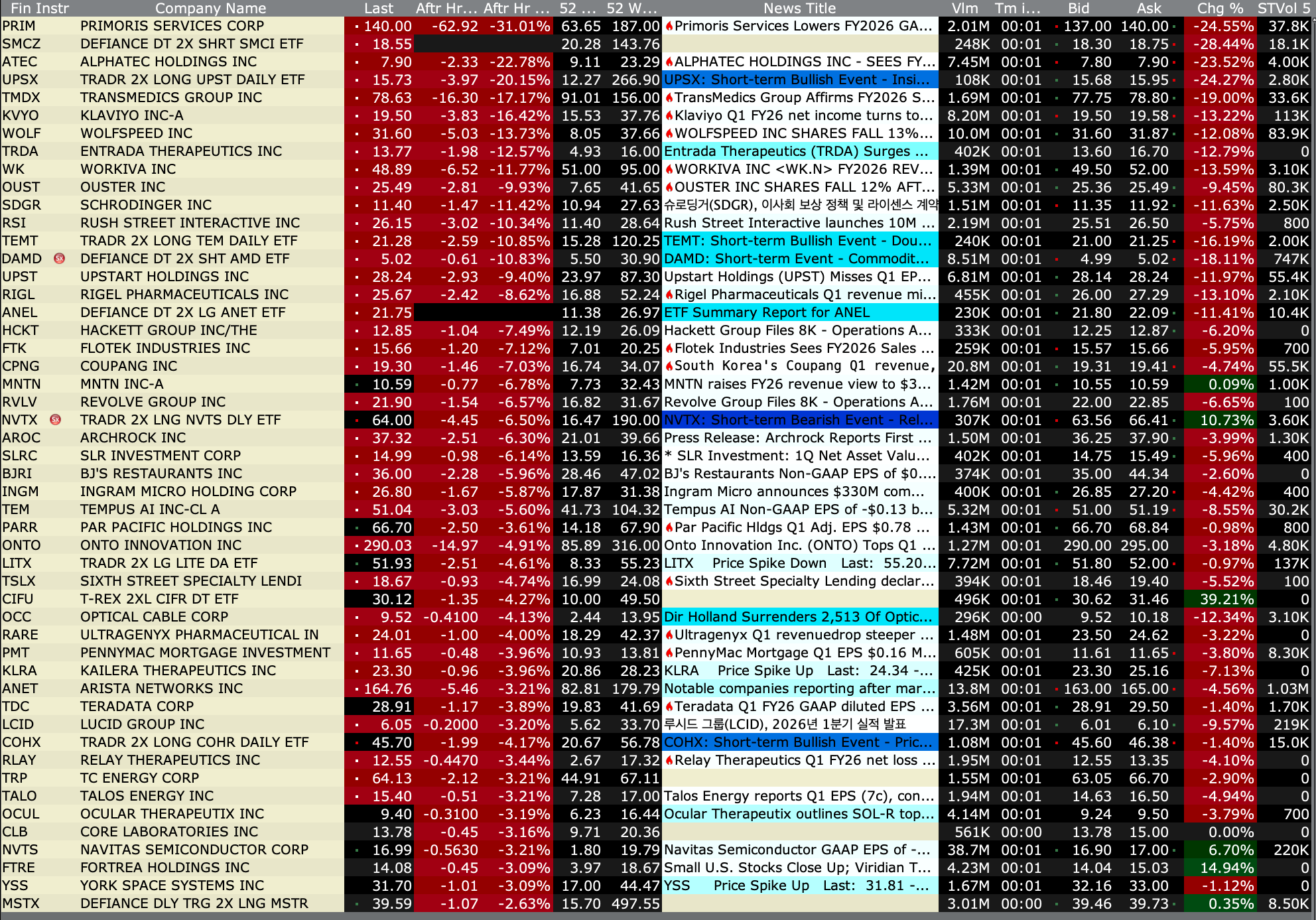

-WGS -44% (earnings, guidance)

-SKK -39% (signs agreement to purchase Rantzio drone assets valued at $259M)

-EMBC -37% (earnings, guidance)

-BRBR -34% (earnings, guidance)

-AVNW -25% (earnings, guidance)

-IPGP -17% (earnings, guidance)

-WLK -11% (earnings, color)

-PYPL -9.0% (earnings, guidance)

-FISV -8.6% (earnings, guidance)

-SHOP -7.0% (earnings, guidance)

-BTU -5.4% (earnings, guidance)

-IQV -5.3% (earnings, guidance)

-ON -5.3% (earnings, guidance)

-FERG -4.5% (earnings, guidance)

-KNX -4.3% (plans to sell $1B convertible note offering)

US: Futs are higher led by NDX / RTY as the US / Iranian truce holds including the US move to return 22 Iranian crew from a seized vessel. Iran’s FM is said to be heading to China for talks IEEPA tariff refunds to begin as early as May 12. Pre-mkt, bond yields are down 1-2bp as the curve steepens and the Dollar catching a bid. Cmdtys are seeing sales in Energy, precious metals retracing losses, and Ags mixed. Eqys are led by Semis with Mag7 mostly higher. Cyclicals (ex-Energy) are outpacing Defensives, though HC is rallying. Today shapes up to be an ‘Everything Rally’. The macro data focus will be on ISM-Srvcs and JOLTS.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVEThe biggest news yesterday and over the weekend were tests of the US / Iran ceasefire as US attempted to provide cover for stranded ships to exit SoH, a mission named ‘Project Freedom’. Iran resumed attacks, targeting UAE in addition to hitting a ship tied to South Korea with missiles; Trump says that the South Korean ship was not being escorted. The Iranian attacks drew condemnation from GCC and other countries in the region, as several initiated national security alerts. It is unclear if the Iranian moves trigger a kinetic response from the US and / or UAE; Trump has yet to express a view on whether Iran violated the ceasefire. Hegseth and Caine have a press conference scheduled for later today as the US moves additional military equipment into the region, including its first hypersonic missile, Dark Eagle.

· CRUDE PRICES – given yesterday’s kinetic moves, it is unclear the status of the ceasefire, but the expectation is for prices to move higher. The US has been ramping its exports to allied countries to offset the impact from the Middle East Conflict, part of the reason the economic damage in APAC has not been as large as expected and why the US is experiencing the second highest spike in fuel prices, behind Southeast Asia. If this conflict moves into June, expect crude prices to move to / through $150/bbl.o CVX’s CEO says that oil storage buffer are being drawn down, echoing Natasha’s view (CNBC).

· TREASURIES – bond yields were +6-7bp as the yield bear flattened and the 10Y yield closing at 4.44%. Client conversations reveal the 10Y yield moving above 4.65% as a ‘sell’ indicator.

· US CREDIT RATING – a new risk unlocked? Last week, Fitch flagged the US’s debt structure as a potential problem with elevated risks relative to other AA-rated sovereigns (Fitch). Specifically, Fitch points to the OBBBA worsening deficits with the federal government deficit of ~7.9% of GDP for FY26 and FY27 with the US debt/GDP ratio above 120% in FY27. Lastly, Fitch flags a deterioration in governance standards as problematic though that could reverse with the midterm elections.

· US MKT INTEL – Given the potential resumption of the kinetic conflict, you may consider concentrating portfolios around Tech and Energy as we may see a near-term pullback; those two sectors appear to be favored by the market to outperform in such a scenario. Further, an unwind of the +Semis / -Software trade provides an opportunity to play Software upside given the group is experiencing accelerating revenue growth and widening profit margins; stated differently, the AI-induced bear case is not materializing in micro fundamentals for Software, but we are seeing +Hardware / -Software trades being put on. Within Energy, we like playing it broadly via integrated, oil servicers, and refiners.

11:30 a.m.: Treasury hosts a $75B 6-Week Bill Auction

Fed Speakers

10 a.m.: Vice Chair for Supervision Bowman (Voter) speaks at the Women in Housing and Finance Symposium, Washington, DC)

12:30 p.m.: Fed Board Governor Barr (Voter) participates in a panel discussion titled "Out of the Deer Park and into the Frying Pan- Regulating Global Finance" at Magdalen College, Oxford

The resilience of equities (as reflected in a low VIX, yesterday's shallow decline and this morning's stock futures strength) continues to frustrate market skeptics (like myself).

While my contrarian view has been frustrating... higher interest rates, building inflationary pressures, an equity risk discount, narrowing leadership (as noted by The Divine Ms M, yesterday was another red day for the Equal Weighted S&P), uneven corporate profitability (and the disproportionate role of Mag 7/AI contributions to rising stock prices and overall profits), improvisational policy (Washington DC), a deepening political schism manifested, in part, by the ever-expanding budget and debt load coupled with still high valuations, are the anchors to my ursine market view.

Grinding

For now, my strategy is to trade dispassionately, opportunistically, small (reflecting that I have been wrong) and quickly — trying to maintain my Partnership's net asset value close to highs.

Given the absence of what I view as a reasonable "margin of safety" and an unfavorable reward vs. risk ratio, I am willing to miss the "limited" opportunity set to the upside that I see.

There will likely come a time, however, when I will be positioning (not trading) more aggressively on the short side, but now (at 6:30 AM, Tuesday morning, May 5) is obviously not yet the time.

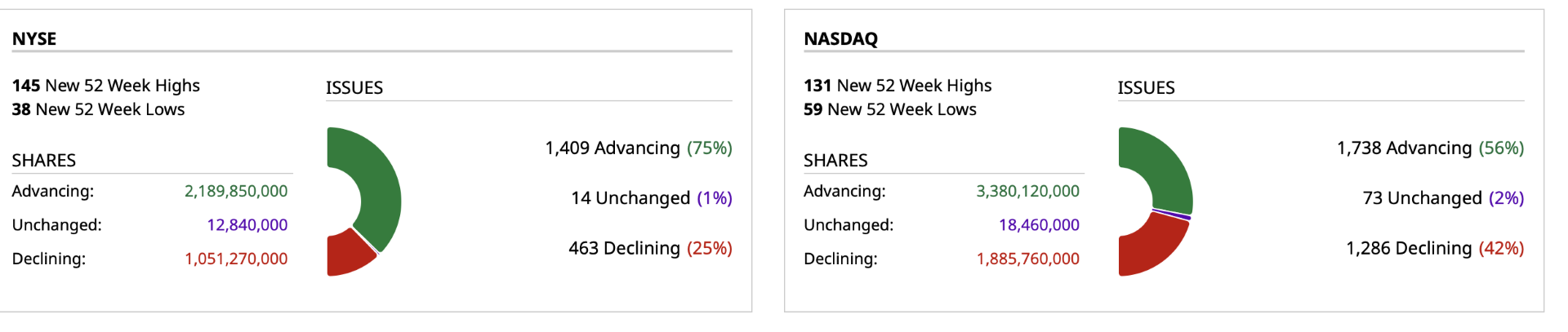

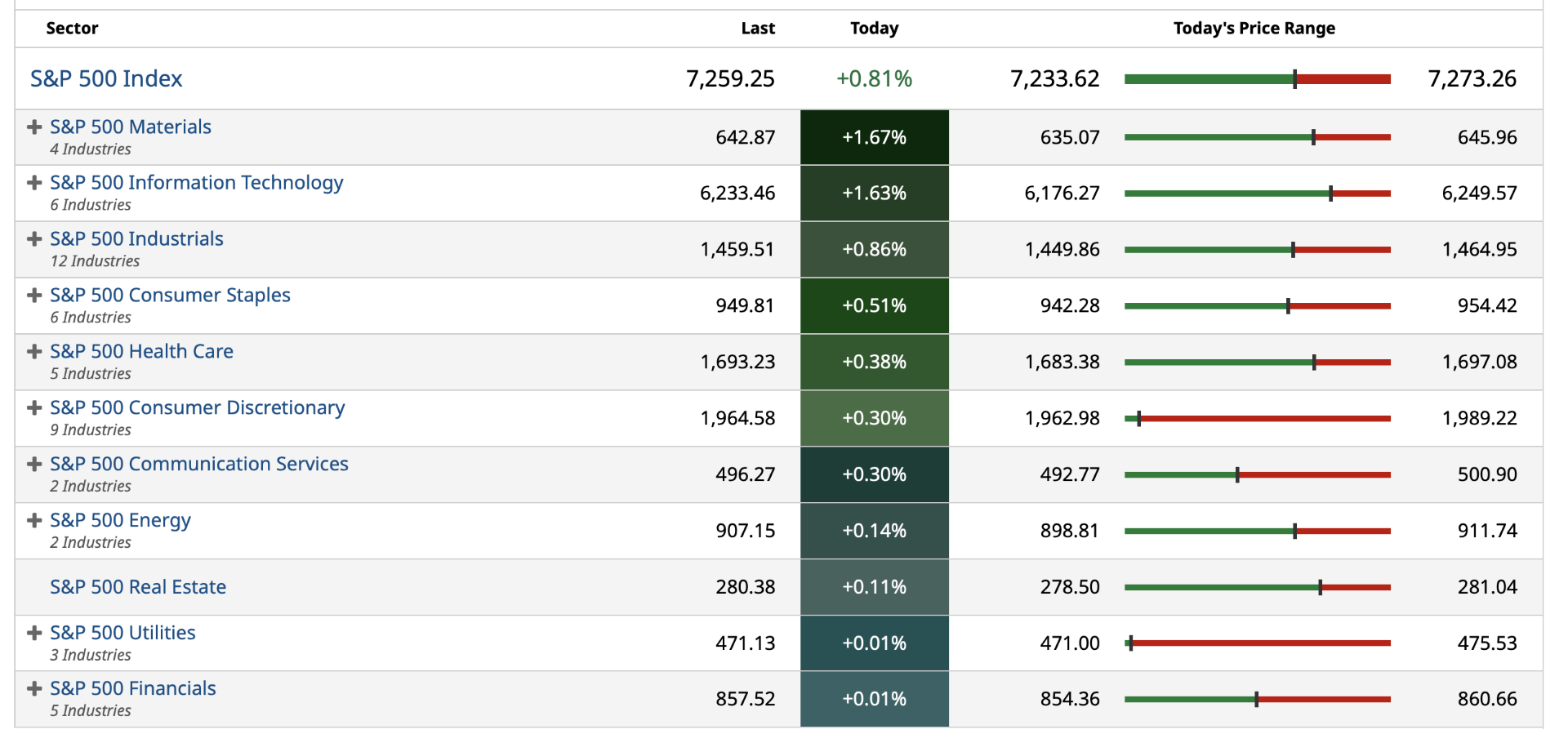

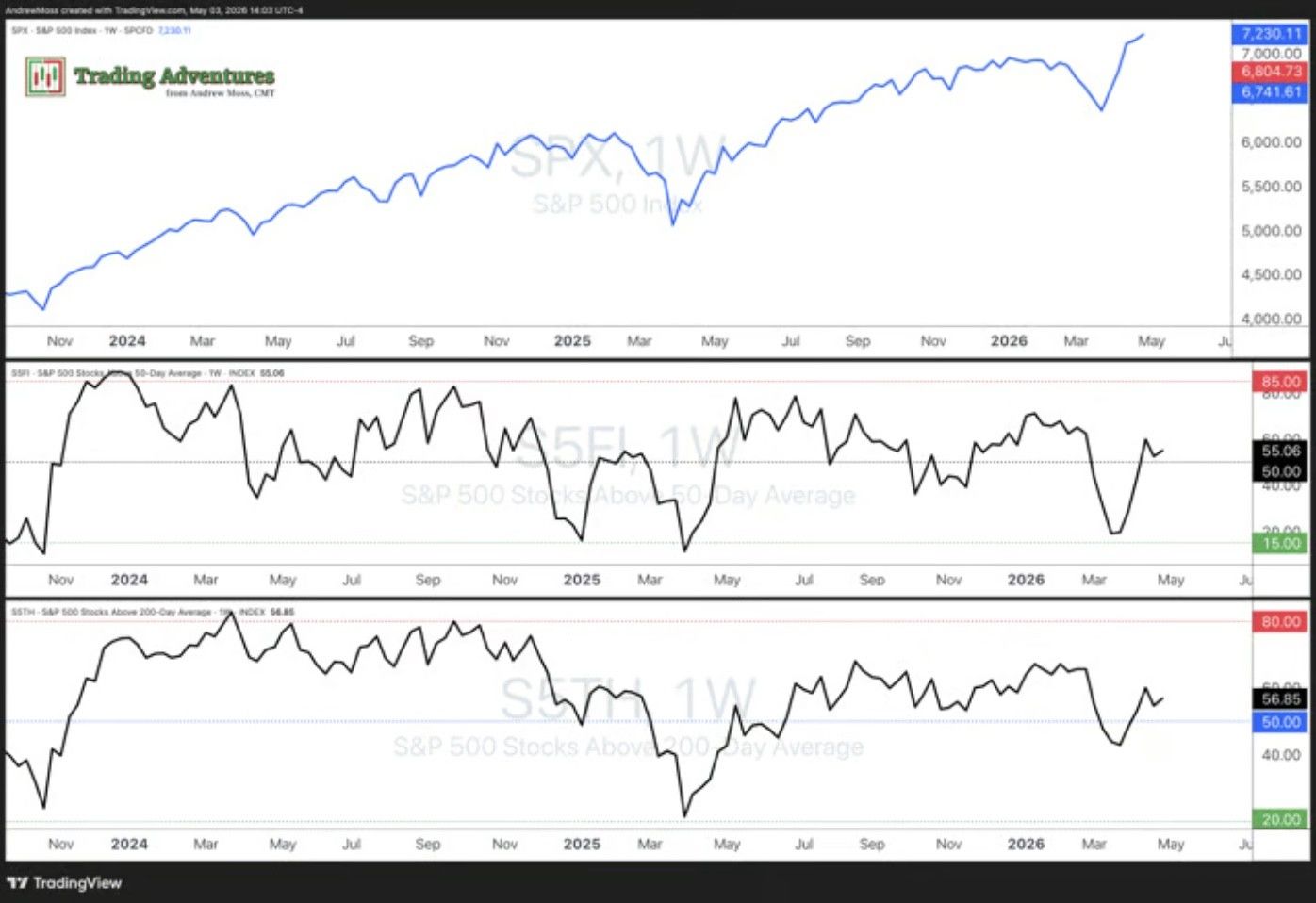

The S&P 500 ended last week at record highs, but breadth remains notably below its year-to-date peak.

Participation hasn’t been able to keep up the pace, with just over half of S&P 500 stocks holding above both their 50-day and 200-day moving averages.

When fewer names are doing the heavy lifting, it leaves the index more vulnerable if leadership starts to falter, but it also raises the possibility of a bullish breadth thrust if participation begins to expand.

The Takeaway: The market has continued to grind higher in a concentrated fashion.

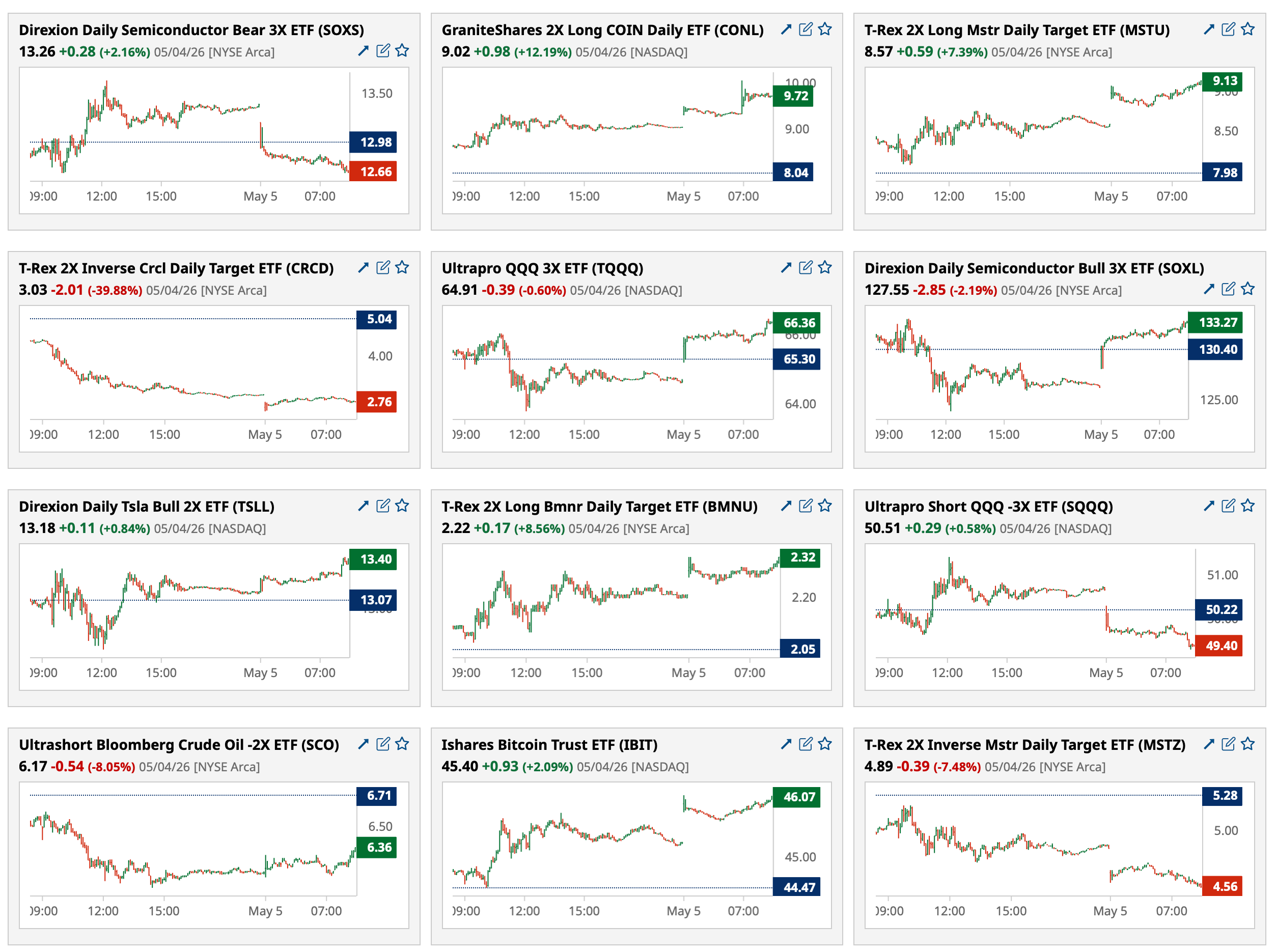

Keep an eye on Hi Yield (HYG), S&P 500 (SPY), Nasdaq 100 (QQQ and Semiconductor (SMH) ETFs. I want to see Hi Yield Bonds rise to make a higher high, confirming the SPY, QQQ, and SMH. #stockmarketpic.twitter.com/5MgYC0hzRp

— Bonnie Gortler (@Optiongirl)

Commercials are extremely net-short Bitcoin

This kind of extreme positioning historically aligned with bottoms in as seen in 2023, 2025 and today$BTCpic.twitter.com/z37ZyvcyQH

Oil up and gold down sharply, aligning with seasonal norms. We have been hedging against both in portfolios (and showing subscribers how to do so). Up by 8% to 16% in just a couple of weeks for positions that we have been using as hedges to broader equity market risks certainly… pic.twitter.com/XaAjMlJHCv

Warren Buffett's mental model that separates great investors from the rest:

Forget charts. Forget daily price movements.

Buffett explains the right way to think about owning stocks using a simple farm analogy.

Imagine you buy 160 acres of farmland. Your neighbour owns 160Show more

The US auto loan crisis is accelerating:

The average amount owed by underwater car borrowers rose to ~$7,200 in Q1 2026, the highest on record and the 4th consecutive annual increase.

Over the last 4 years, the average amount owed by negative equity car borrowers has risenShow more

US inflation expectations are surging:

The US 10-year breakeven rate is up to 2.47%, the highest since February 2025.

Excluding Q1 2025, this is the highest level since October 2023.

In turn, 1-year inflation expectations are up to 3.26%, the highest since September 2022.Show more

The 30-Year Treasury yield closed above 5% today and it not far from its highest level in more than a decade.

The stock market may be ignoring Iran and Inflation, but the bond market is not.

Video: youtube.com/watch?v=sxYJrG…Show more

Oil up and gold down sharply, aligning with seasonal norms. We have been hedging against both in portfolios (and showing subscribers how to do so). Up by 8% to 16% in just a couple of weeks for positions that we have been using as hedges to broader equity market risks certainlyShow more

Software companies are flooding the US private credit industry:

Software loans account for ~20% of all loans deployed by Business Development Companies (BDCs).

BDCs are publicly traded firms that lend to small, mid-sized, and distressed US businesses, offering retail investorsShow more

Keep an eye on Hi Yield (HYG), S&P 500 (SPY), Nasdaq 100 (QQQ and Semiconductor (SMH) ETFs. I want to see Hi Yield Bonds rise to make a higher high, confirming the SPY, QQQ, and SMH. #stockmarket