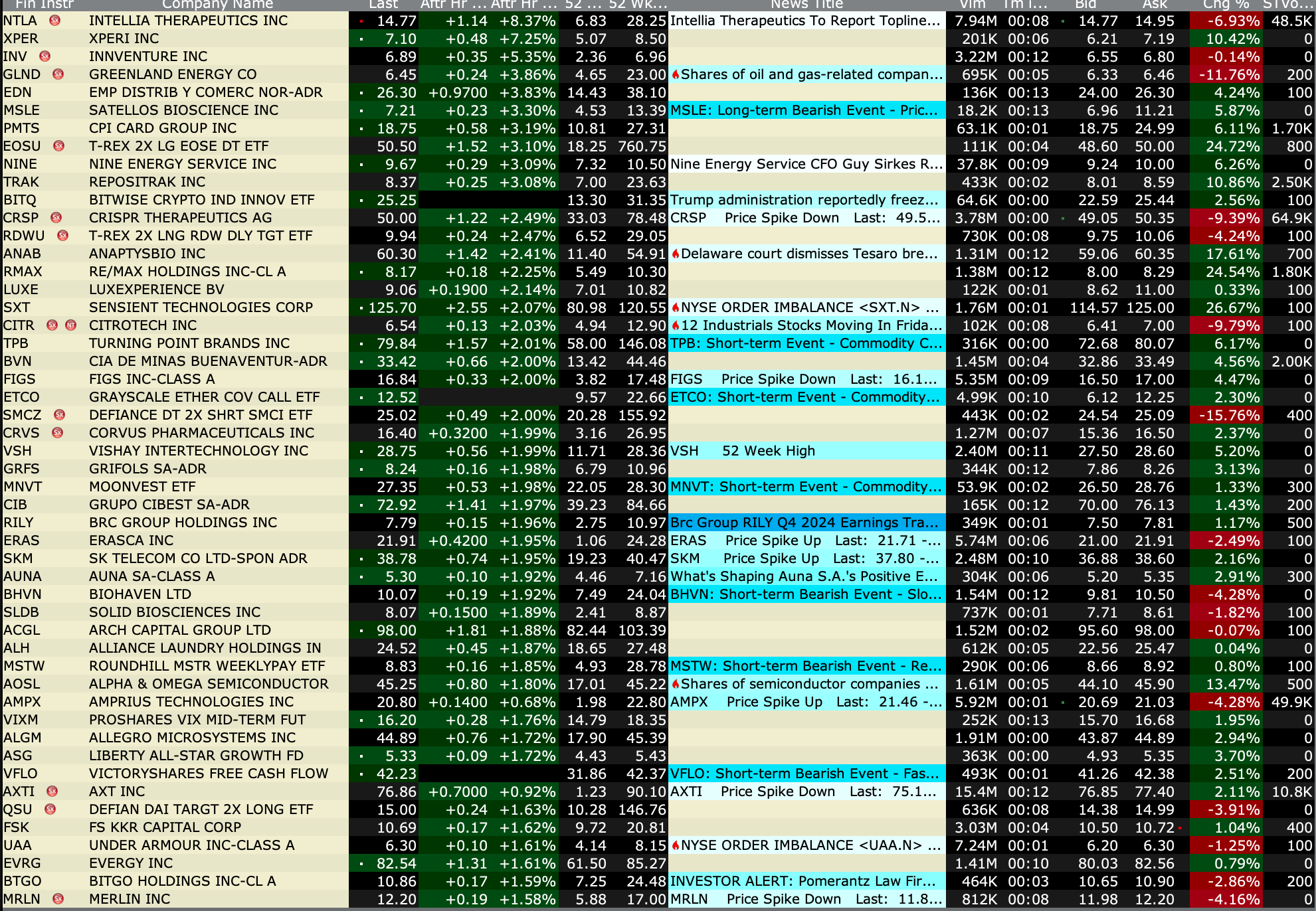

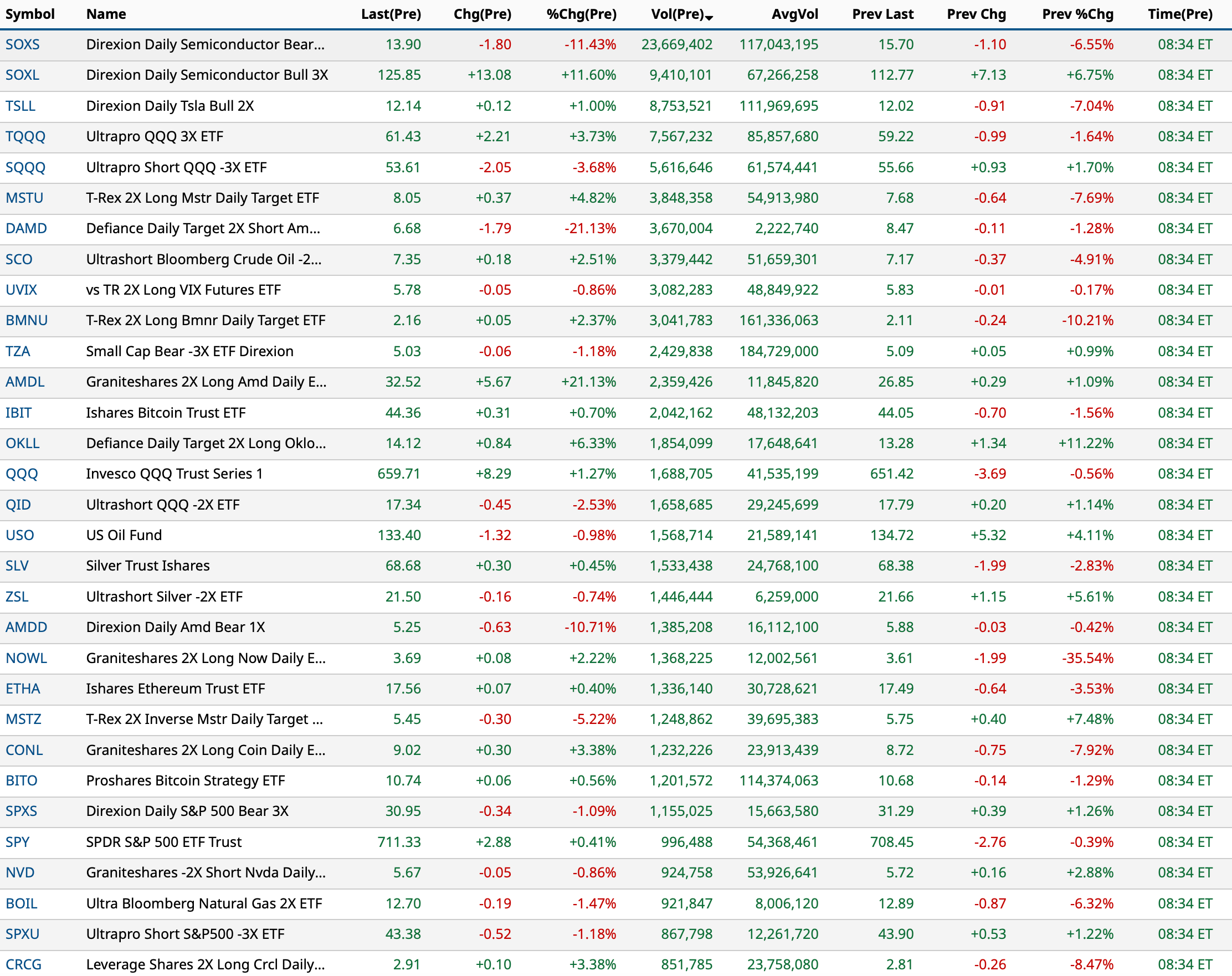

Friday's After-Hours Advancers and Decliners

After-Hours % Advancers

After Hours % Decliners

BY Doug Kass · Apr 24, 2026, 4:45 PM EDT

After-Hours % Advancers

After Hours % Decliners

BY Doug Kass · Apr 24, 2026, 4:45 PM EDT

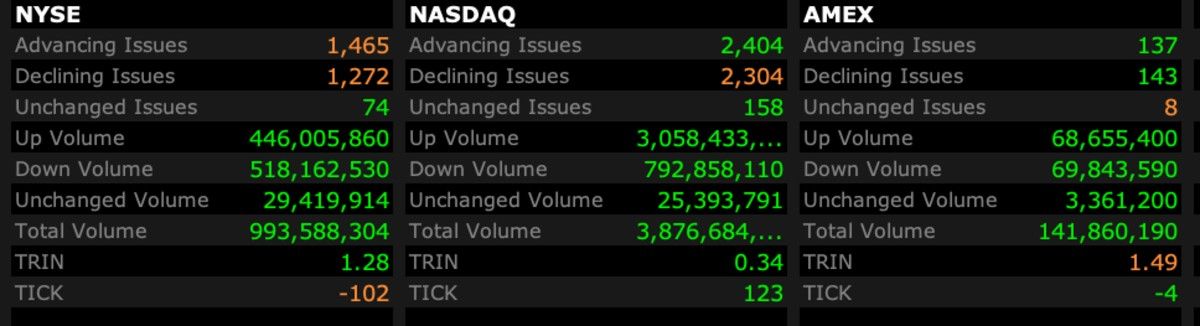

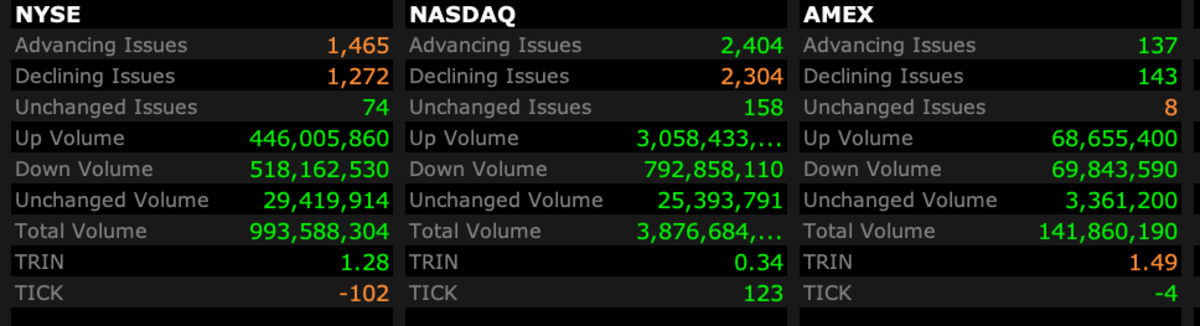

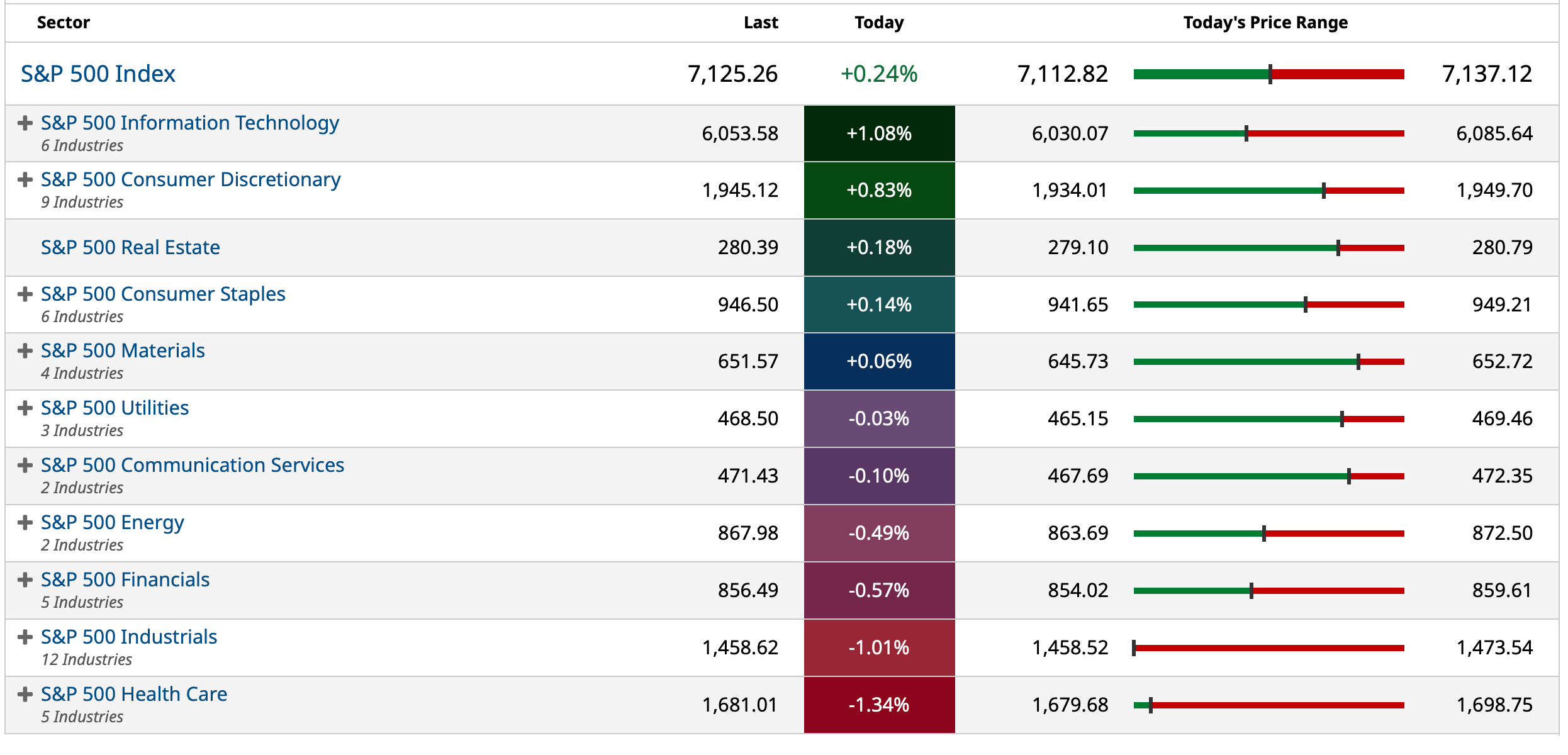

Closing Volume

- NYSE volume 14% below its one-month average

- NASDAQ volume 16% above its one-month average

- VIX index: down 3.57% to 18.62

Breadth

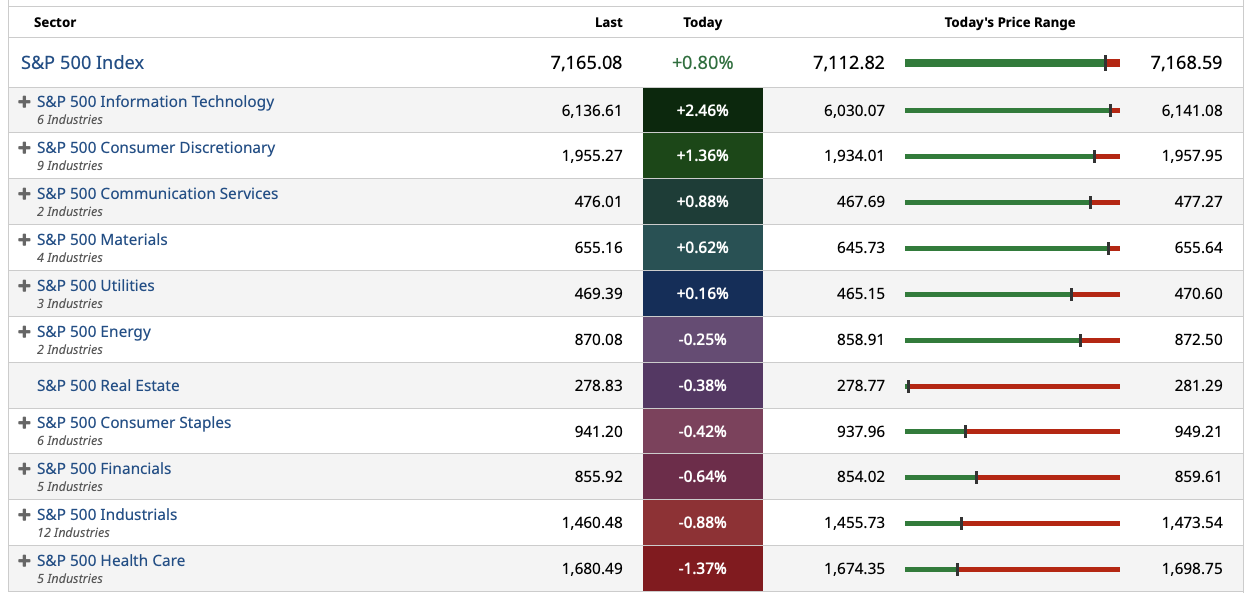

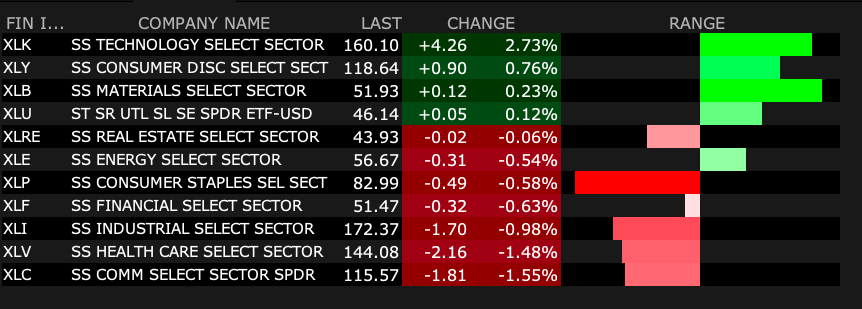

S&P 500 Sectors

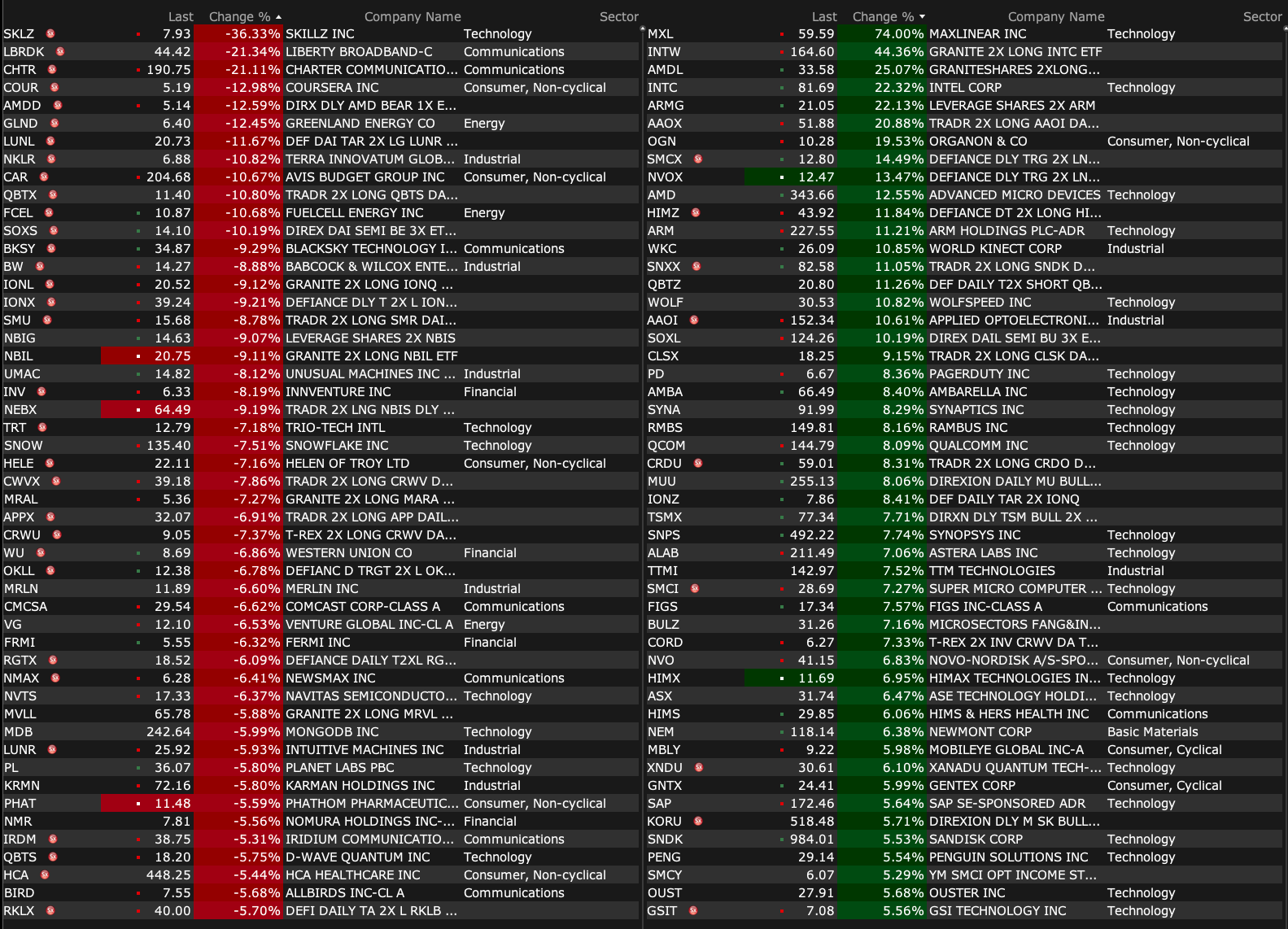

% Movers

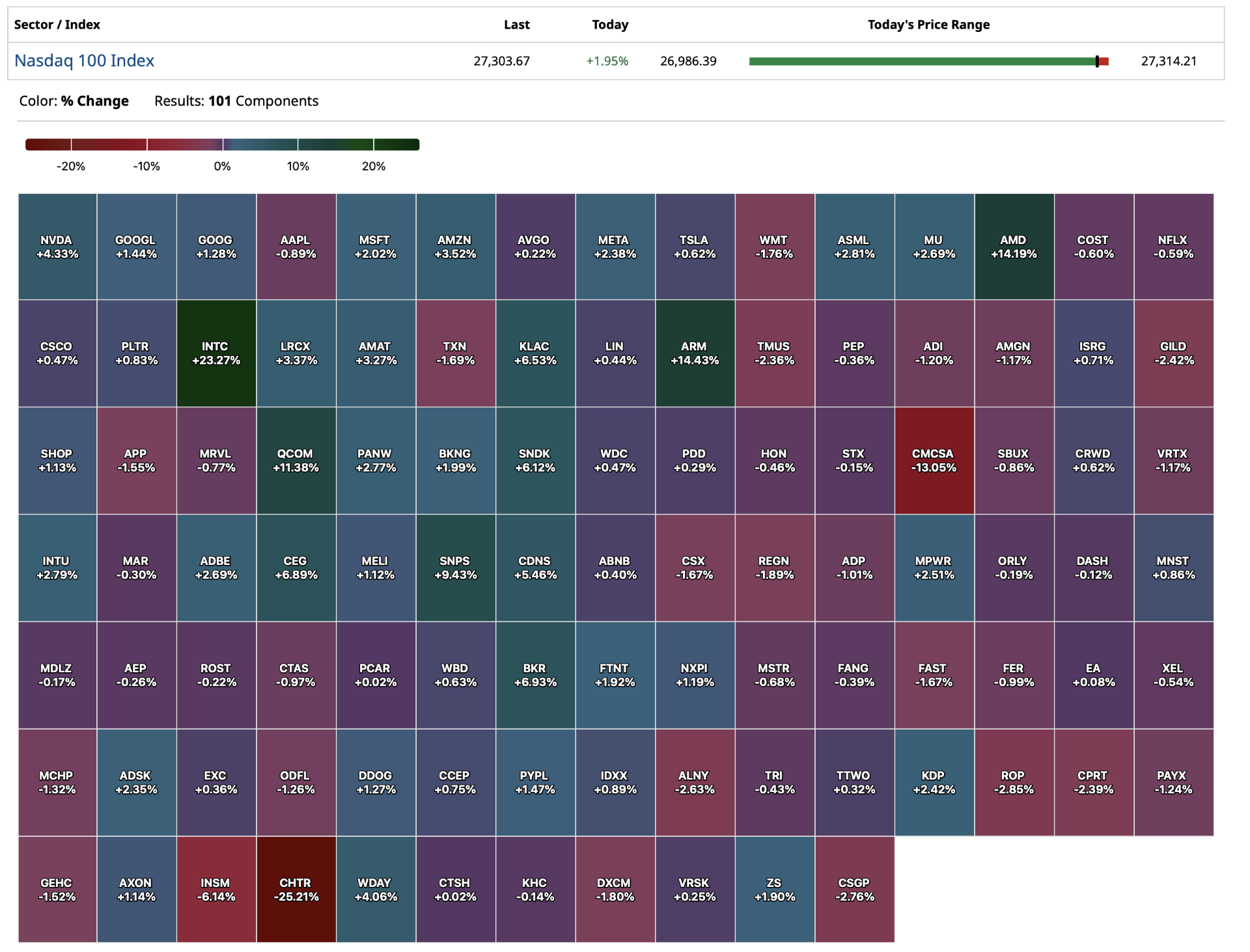

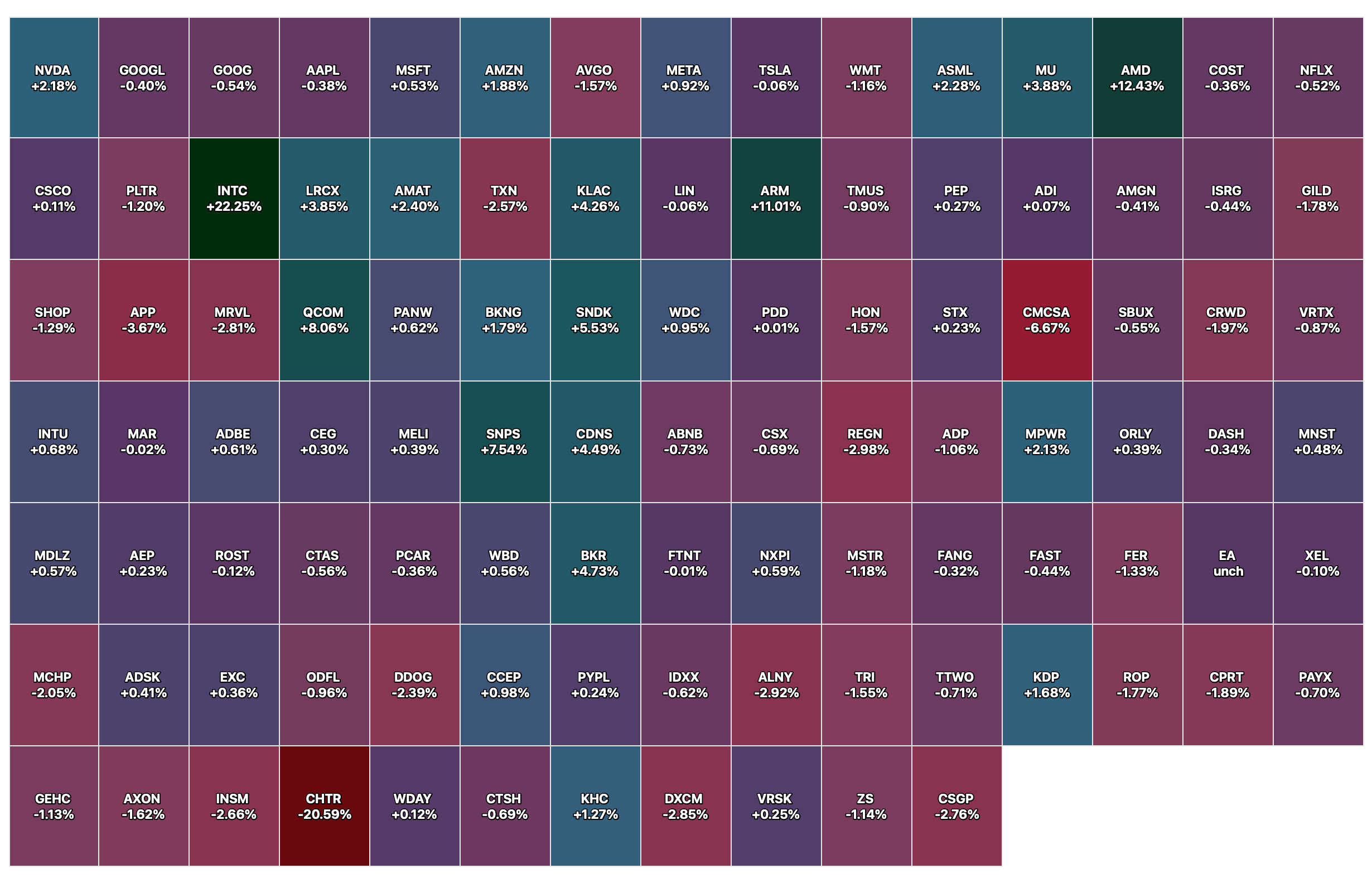

Nasdaq 100 Heat Map

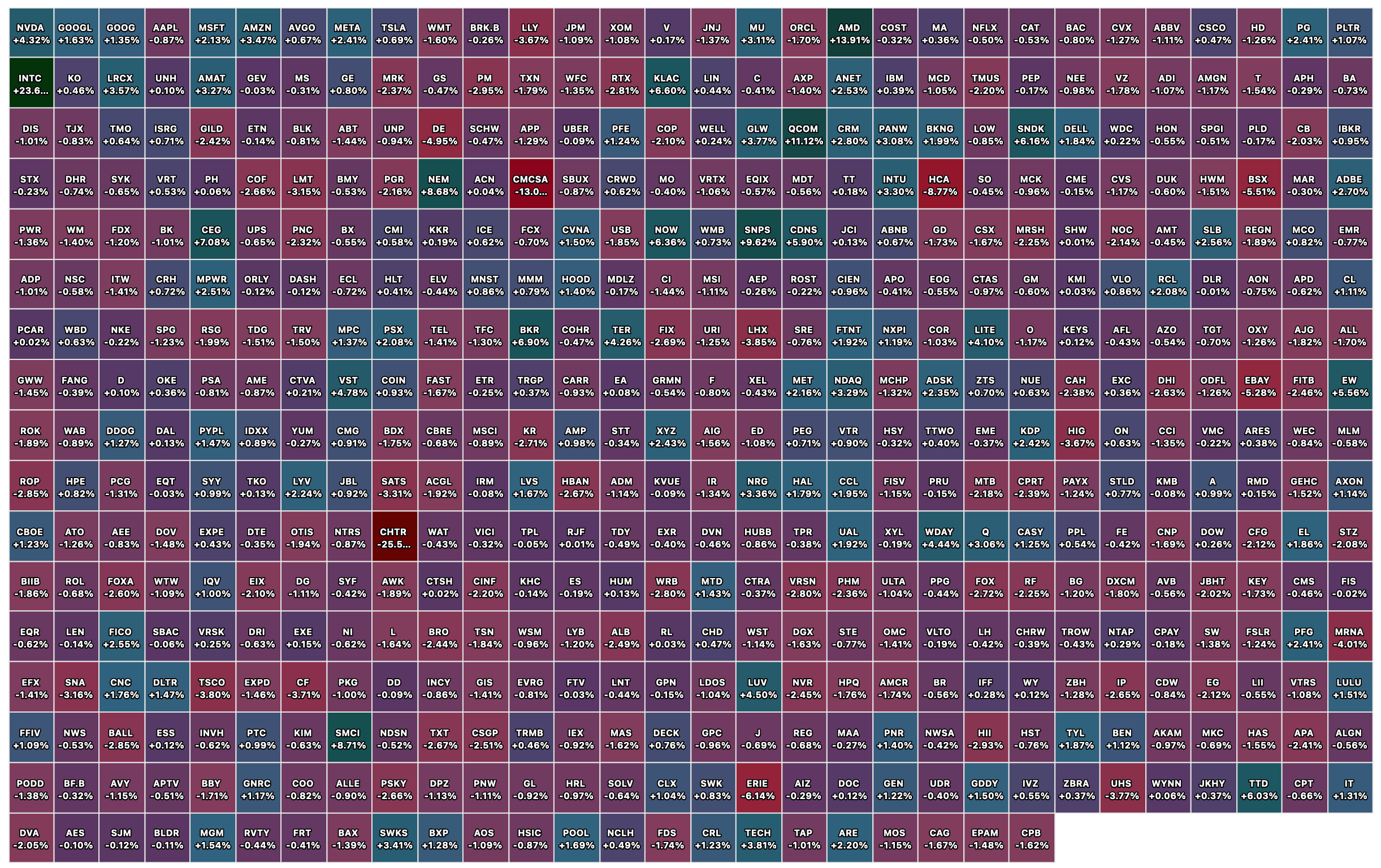

Closing S&P 500 Heat Map

BY Doug Kass · Apr 24, 2026, 4:28 PM EDT

Thanks for providing me with this platform — today, all week and for the past 28 years!

Enjoy your weekend.

Be safe.

BY Doug Kass · Apr 24, 2026, 3:45 PM EDT

With S&P cash +58 handles, I have added to my index shorts:

* (SPY) $714.25

* (QQQ) $664.01

Position: Short SPY common (VS), QQQ common (VS)

BY Doug Kass · Apr 24, 2026, 3:27 PM EDT

"Markets are strongest when they are broad and weakest when they narrow to a handful of blue-chip names."

- Bob Farrell, Ten Investing Lessons

All week long the market's leadership is narrowing into big tech.

Today, only four of 11 S&P sectors are positive:

Conspicuous is the weakness in financials. As seen below (in the intraday charts), the sector is moving deeper in the red as the day progresses. In the good old days, poor relative performance in financials was considered a signpost of concern, but this is not my father's market.

Intraday Sector Action

Position: None

BY Doug Kass · Apr 24, 2026, 3:09 PM EDT

BREAKING: Consumer sentiment in the US officially hits its lowest level on record amid the Iran War.

— The Kobeissi Letter (@KobeissiLetter)

This marks the weakest consumer sentiment since data collection began in 1978. pic.twitter.com/jwyuXlSvNl

BY Doug Kass · Apr 24, 2026, 2:40 PM EDT

Professor Scott Galloway's No Mercy No Malice: "Freedom of Navigation."

BY Doug Kass · Apr 24, 2026, 2:00 PM EDT

From Peter Boockvar:

Positives,

1) The S&P Global US manufacturing PMI rose to 54 from 52.3. S&P Global said “While manufacturing output showed a solid gain, the increase in part reflected stock building in the face of concerns over supply availability and price hikes. Input cost inflation accelerated and supply delays worsened at a pace not seen since mid-2022, contributing to the largest monthly jump in average selling prices for goods and services since July 2022.” More on this, S&P Global heard “survey respondents reporting ‘panic’ and ‘emergency’ buying ahead of price hikes and supply shortages in echoes of the problems seen during the pandemic.” Also of note, “The rise in orders was driven by domestic demand, as export sales of goods fell at an increased rate.”

2) Initial jobless claims rose to 214k from 208k and 4k above the estimate but remaining very low. The 4 week average of 211k is little changed from the 210k seen last week. Continuing claims at 1.821mm was up a touch from the 1.809mm seen in the week before but remaining below the 1.9mm range that stood as the most since November 2021.

3) With another dip in the average 30 yr mortgage rate to 6.35%, purchase applications jumped by 10% w/o/w while refi’s were up by 5.8%.

4) Pending home sales in March rose 1.5%, above the estimate of up .5% and follows a 2.5% gain in February (revised up from 1.8%) . The contributions to the gains were seen in the Northeast and South, offsetting declines in the Midwest and West. Price cuts in the South seemed to help that region. The NAR said “Contract signings rose in March despite higher mortgage rates, pointing to pent-up demand. A greater supply of inventory will help translate that demand into more home sales.” And, “Demand sensitivity to mortgage rates is greatest among first-time buyers, particularly younger buyers. As a result, boosting supply and new home construction should focus on smaller, more affordable homes.”

5) Core retail sales in March were better than expected with a .7% m/o/m gain, well better than the forecast of up .2% and February was revised up by one tenth to an increase of .6%. These are nominal figures.

6) The April KC manufacturing index at +10 was little changed from +11 in the month before.

7) From Texas Instruments: “In the first quarter, revenue came in above the top of the range, as we saw continued acceleration in industrial and data center. The overall semiconductor market recovery is continuing and we remain well positioned with inventory and capacity that allows us to support our customers with competitive lead times through the cycle.”

8) From American Express: “Card member spending grew 10% on a reported basis, and this is the highest quarterly growth in three years, driven by strong growth across both goods and services and T&E. We continue to see strong demand and engagement with our premium products across our customer base...Credit performance remains excellent with both delinquency and write-off rates still below 2019 levels.”

9) From Fifth Third Bank: “In commercial, legacy Fifth Third C&I loan balances grew 6% y/o/y. Production remained healthy, with the strongest activity in manufacturing and construction supported by restoring and infrastructure investment...“Clients are cautious but active...The consumer portfolio remains healthy, with non-accrual and over 90 delinquency rates relatively stable across all loan categories.”

10) From Southwest Airlines: “Looking deeper at the results, demand remains strong across geographies, customer segments, and both business and leisure, and the customer take rate for our enhanced product offering and seating ancillaries is strong as well.”

11) From Dow: “While January and February order books were solid, we experienced a sharp positive inflection in March with the beginning of the conflict in the Middle East. We expect this supply disruption will persist throughout 2026...an increasingly positive margin backdrop continues to unfold, and we expect the pricing momentum that began in March to continue across every business and every region in Dow’s portfolio.”

12) From Taylor Morrison: “As I shared on our last earnings call in February, early signs heading into the spring selling season were positive and the quarter played out largely as we expected with sales activity building through the quarter and March representing our strongest month. That momentum is consistent with normal seasonal patterns, albeit with slightly less acceleration than we have seen historically, reflecting continued consumer cautiousness...April started off somewhat slower, as typical, coinciding with the holiday weekend, but momentum then picked back up and we’re looking forward to a strong end to the month, even with all the headline noise.”

13) From Travel & Leisure: “Overall, our owner base remains healthy. They are prioritizing travel, and we are not seeing any meaningful shifts in their behavior. First quarter gross bookings were up y/o/y. The booking window remains steady at approximately 100 days and average length of stay is unchanged y/o/y at just over four days. The distance traveled to our resorts in Q1 was actually up slightly to last year, indicating consumers’ willingness to travel to our resorts. The data suggests that in uncertain economic times, our value proposition becomes even more relevant...As we enter our peak sales season, we are mindful of the macro backdrop and its potential to influence consumer behavior. That said, the trends we are seeing remain healthy, our value proposition continues to resonate, and the model is performing as designed, positioning us to outperform across cycles.”

14) From CSX: “One emerging positive here is that shippers are looking more to rail conversion as they weigh the impacts of higher fuel and trucking costs.”

15) From Philip Morris: “The Middle East conflict had a small impact on our business in the first quarter, which affected shipment to global travel retail and certain markets in the region for both combustible and HTUs (heated tobacco units) . While we have observed increased energy prices and some disruption in energy supply in a number of markets, this has not at this stage translated into a discernible shift in consumer behavior.”

16) From Tesla: “On the autos business, we have seen a resurgence in demand in EMEA and certain countries like France and Germany showing over 150% q/o/q growth in deliveries. In APAC, we witnessed growth in South Korea and Japan, again in terms of deliveries. Even out here in the US, we have seen slight growth in terms of q/o/q deliveries...Whilst the recent increase in gas prices has had a positive impact on the order rate, this improvement started before the uptrend in gas prices.”

17) From MMM: “We had a light start to the year on the top line with organic growth of 1.2%, driven by pockets of macro pressure, but we saw encouraging order trends that support our outlook for acceleration in the balance of the year.” Most likely due to the front running of orders I believe.

18) From Capital One: On the state of their consumer, “So the US consumer remained healthy and the overall economy remained resilient through the first quarter. The unemployment rate improved slightly in the quarter. Despite some high profile headlines about layoffs, the total volume of job losses and new jobless claims remains low and stable. Income growth continue to run ahead of inflation. Consumer spending remained robust. Because of last year’s budget bill, tax withholdings are lower than a year ago and tax refunds are higher.” On credit quality, “In our Domestic Card business, our credit metrics continue to improve on a y/o/y basis in the quarter. On a sequential quarter basis, our charge-off rate moved in line with seasonality, while our delinquencies improved relative to what we would expect from normal seasonality. Our auto credit metrics remained strong as well. Auto losses were slightly higher on a y/o/y basis in Q1, but this was consistent with a modest increase in the subprime mix of that portfolio over the past year. Our auto losses have been back near pre-pandemic levels for over a year. And our auto credit is supported by strong performance of recent originations and generally stable vehicle prices.”

19) From Zion Bancorp: To a question about the loan outlook, “the pipeline is looking healthy, actually, at this point. We’re seeing lots of activity in small business, middle market, corporate banking syndications, just general C&I. We’re just seeing lots of activity. Another thing that’s coming back is we’re seeing increased CRE activity. We’re cautious there, but we are seeing increased activity as some of the markets have reached more stabilization. So, I think we’ll continue to see growth coming from those areas.”

20) From Cleveland Cliffs: “While Q1 results could be better and they would be better, if not for a couple of one-timers, we can see the clear signs of a positive trend for me. Among these one-timers, the impact of the spiking of energy costs was the most relevant to Q1 results. Now to the good news. Our order book is full, and the automotive OEMs are booking more and more steel from Cliffs. Production schedules are tight, and lead times have moved out. Historically, pricing changes took about a month to flow through our realized numbers Today, that lag is closer to two months...In practical terms, that means the pricing strength visible in the market today will increasingly show up in results as we move through the year quarter by quarter.”

21) Japan’s March CPI and ex food and energy rose 2.4% y/o/y as expected vs 2.5% in February. Keeping the headline figure in check of up 1.5% y/o/y were government energy subsidies to cushion the blow of the spike in imported fuels.

22) Japan’s April manufacturing PMI rose to 54.9 from 51.6 while services fell to 51.2 from 53.4. In Australia, they saw improvement for both components with manufacturing at 51 vs 49.8 and services bouncing to 50.3 from 46.3. In India, manufacturing rose 2 pts m/o/m to 55.9 and services came in at 57.9 vs 57.5. Still doing well notwithstanding their imported energy exposure.

23) Capturing the war, Japanese exports in March rose by 11.7%, about in line with the estimate of up 11%. Imports grew by 10.9%, higher than the forecast of up 7%. Helping trade was China reopening after their Lunar New Year holiday and likely too a rush to get stuff with growing worries of supply chain issues.

24) In the UK, March retail sales ex auto fuel were as expected when including a downward revision to February.

25) The UK manufacturing PMI was up to 53.6 from 51 and services grew too to 52 from 50.3. Same thing here, “The improved rate of expansion is in part a reflection of a short term boost from a rush to secure purchases ahead of feared price rises and supply shortages linked to the war.“

26) Bank Indonesia left its benchmark rate unchanged at 4.75% as expected and their bias is up with rates. “Bank Indonesia is prepared to implement a further strengthening of monetary policy as needed to maintain the stability of the rupiah exchange rate and keep inflation in 2026 and 2027 within the target range.”

Negatives,

1) From the S&P Global services US services PMI, “Orders for services ranging from travel and tourism to financial products barely rose as the war caused hesitancy for spending among both households and business customers, with surging prices and the prospect of higher borrowing costs acting as a further deterrent.” On the overall labor market, S&P Global said, “Employment rose only marginally in April after falling slightly in March. The overall flat picture represents the worst back-to-back months for employment since late 2024. Manufacturing headcounts fell for the first time in nine months and only a marginal return to jobs growth was reported in the service sector. While some of the weak employment picture reflected resignations and persistent labor supply shortages, companies also reported concerns over the need to reduce staffing costs in the face of the uncertain demand environment and high input prices.”

2) The final April UoM consumer confidence index came in at 49.8 vs 53.3 in March and 56.6 in February. That remains a record low but up from 47.6 in the preliminary print. One yr inflation expectations were 4.7% vs 3.8% in March and 3.4% in February. The UoM said “ Decreases in sentiment were seen across political party, income, age, and education. Expected business conditions declined for both short and long time horizons, nearly matching year-ago readings when the reciprocal tariff regime was implemented. After the two-week cease-fire was announced and gas prices softened a touch, sentiment recovered a modest portion of its early-month losses.” Also, This month, two-thirds of consumers believe it is a bad time to buy, primarily due to already-high prices, which clearly dominates the smaller share who believe it is a good time to buy to avoid future price increases.”

3) Maersk released this saying “Given the ongoing Middle East position and the escalation in the situation - with 3 container ships attacked by Iranian forces this week - the SoH remain firmly closed. We cannot guarantee safe passage and safety of our people, assets and our customers’ cargo remains the top priority.”

4) The WCI Shanghai to LA container price rose to the highest since mid January, up 4.4% w/o/w. The price to NY though was little changed while it fell to Rotterdam from Shanghai.

5) According to the weekly figures from WorldACD Market Data, air cargo prices rose by another 3% in the week between April 6-12 and are now up 37% y/o/y and higher by 40% from the end of February.

6) The April Philly services index remained deeply negative at -16.5 vs -23.9 in March.

7) From American Express: On the airline slowdown they cited, “we saw definitely noise towards the end of March, beginning of April, and where it was the most visible is in the volume of refunds that we saw being processed. It’s always hard to know exactly what happened with these refunds. Is that people booking on a different schedule, different airline, but we definitely saw a spike in terms of customer refund. That being said, the impact is not that large.”

8) From Ally Financial: “Notwithstanding the increase in tax refunds and a dynamic macro, delinquency followed what we consider to be a typical seasonal pattern during the quarter. We’ve continued to see a resilient consumer, but given the evolving backdrop, we feel it’s appropriate to remain measured.” How they define ‘measured,’ “If you look at the data from the quarter, auto applications are up 16% y/o/y but origination volumes are at a slightly more moderate pace. And so we’re prioritizing, I call it, discipline over volume.”

9) From Southwest Airlines: “Turning to the outlook, there is significant economic and geopolitical uncertainty, and it’s impossible to know with confidence all the ways the industry could be impacted. That said, we do know two things. Fuel prices are much higher, and if that’s sustained, it will require higher ticket prices to offset that increase in fuel. Given the ongoing macroeconomic uncertainty, updating our full year adjusted EPS guide of $4 would not be productive at this time.”

10) From Alaska Air: “Air Group began the year with solid operating momentum, though first quarter 2026 results were impacted by sharply higher fuel prices and localized demand disruptions as a result of historic rainstorms in Hawaii and civil unrest in Puerto Vallarta ahead of the peak spring break travel season. These markets represent appoximately 30% of Air Group capacity.”

11) From Freeport McMoRan: On the rising cost side, “The price of diesel fuel, which we use to support our haul trucks in the Americas and for a portion of our power plant in Indonesia has been volatile with the most significant impacts in Indonesia. To date, it has been more of a cost issue than a sourcing issue, but we continue to monitor the situation carefully...For reference, the sharp rise in diesel prices in March equates to an approximate $500 million cost increase on an annualized basis. We are also monitoring the sulfuric acid situation where prices more than doubled on the spot market.”

12) From PulteGroup: “Within a demand environment impacted by domestic and global dynamics, we see a consumer with concerns about affordability and the economy, but still desirous of homeownership as demonstrated by the 3% growth in our first quarter net new orders.”

13) From DR Horton: “Affordability constraints and cautious consumer sentiment continue to impact new home demand; however, our tenured operators executed with discipline, driving an 11% y/o/y increase in net sales orders, while reducing unsold completed homes by 35% from a year ago. We expect our sales incentives to remain elevated in fiscal 2025, with incentive levels dependent on demand, mortgage interest rates and other market conditions.”

14) From United Airlines: “At the moment, our goal is to do whatever it takes to recover 100% of the increase in jet fuel prices as quickly as possible and to achieve double digit pre-tax margins next year.” And how will they do that?, “to recover 100% of fuel costs, yields need to increase by about 15% to 20% and we are assuming that fuel may remain higher for longer. Two, as yields increase, there will be an elasticity effect on demand, we’re estimating it will lead to less overall demand. While we haven’t actually seen that decline yet, ECON 101 makes us believe it’s coming. Three, less demand means that we should be supplying fewer seats to the market.”

15) From Tesla: Hopefully good over time but rising expenses in the meantime, “We’re going to be substantially increasing our investments in the future. So should expect to see a very significant increase in capital expenditures, but I think well justified for a substantially increased future revenue stream...Obviously Tesla is not alone in this. I think you’ve seen in most, if not all, certainly the major technology companies substantially increasing their capital investments, and we’re going to be doing the same. I think it’s going to pay off in a very big way. So we’re investing in and improving our core technologies, battery powertrain, AI software, AI training, chip design, manufacturing design - laying the groundwork for significantly increased manufacturing production.”

16) From Tractor Supply: “The retail environment remains cautious but stable, with spending focused on needs and small indulgences, with some evidence of trip consolidation.” Specifically, “In Pet, the category remains pressured, and while we are holding our share, our performance is below our expectations...Dog ownership, particularly in larger breeds, has come under pressure, and our mix remains heavily weighted towards dog...Cat ownership is growing and gaining share, and that’s where we under index.” And, “A good example of consumer spending is around their tax refund behavior. While refunds did come through and we captured our fair share, customers are using these dollars more cautiously. A significant portion is going towards essentials, savings and debt reduction rather than discretionary spending, consistent with the broader environment we’re seeing.”

17) Also out on the inflation front in Japan, March services producer prices rose 3.1% y/o/y, up from 2.7% in February.

18) In Japan’s manufacturing PMI specifically, “There were reports that some manufacturing firms boosted output due to concerns and uncertainty surrounding the war in the Middle East and the potential for further supply chain disruptions. The latter contributed to not only a much sharper rise in costs, but the most pronounced increase in average delivery times for manufacturers’ inputs for nearly four years.”

19) Germany’s March PPI jumped 2.5% m/o/m, well more than the estimate of up 1.4%.

20) The April German ZEW investor confidence index on their economy fell to -17.2 from -.5 and vs the estimate of -5.8. The Current Situation deteriorated too, declining to -73.7 from -62.9. ZEW said “The economic consequences of the Iran war for the German economy go far beyond price increases: Businesses are concerned about long-term shortages of energy supply, and this discourages investment and weakens the effect of government stimuli.”

21) In Germany, the April IFO business confidence index fell to 84.4, the lowest since May 2020 during you know what, from 86.3 and that was below the estimate of 85.7 with both the Current Assessment and Expectations components lower. The IFO said succinctly, “The German economy is being hit hard by the Iran crisis.” Within the index, manufacturing fell, “especially in the chemical industry” and there was “increasingly” reports of “supply bottlenecks.” The service sector index “fell considerably” and “the logistics industry in particular is under pressure. The outlook there is grim.” In trade, “Retailers are worried in particular that consumers will be more reticent due to rising inflation.” In construction, “the business climate plummeted.”

22) Business confidence in France got hit too, falling to 94 from 97 and vs the estimate of 96. Manufacturing confidence held in but hit by a drop in retail and services confidence.

23) The Eurozone April manufacturing PMI rose to 52.2 from 51.6, offset by the drop in services to 47.4 from 50.2. Combining the two puts their composite index back below 50 at 48.6 vs 50.7. Boosting manufacturing, “Manufacturers have increased their buying of inputs to a degree not witnessed since early 2022 as supply chain delays have also risen to the most widespread since the pandemic.” And this comes along with it, “Input costs and selling prices have already jumped higher not just in response to higher energy costs but in a reflection of a broader upturn in commodity prices and mismatch of demand against strained supply. If the Covid 19 pandemic is excluded, this is the biggest surge in cost pressures that we have recorded since 2000.”

24) In the UK PMI, “Prices have spiked higher at a rate not previously seen by the survey outside of the pandemic, suggesting inflation could rise more than many forecasters have been anticipating. Prices are rising not just because of surging energy costs, but also due to increases in charges levied for a wide variety of goods and services, with price hikes often stoked by supply concerns. The number of supply delays reported has jumped to the highest on record if the pandemic is excluded.“

25) The UK CBI industrials order index plunged to -65 from -19 in April.

26) In the UK, March CPI was hot, up by .7% m/o/m and by 3.3% y/o/y vs 3% in the month before. Of course higher energy costs were the main factor with motor fuel jumping by 8.7%. The core rate though was still up by 3.1% y/o/y vs 3.2% in February. Services inflation remains persistent, up by 4.5% y/o/y vs 4.3% in February. Wholesale prices were very hot, with input prices spiking by 4.4% in the month alone and by 5.4% y/o/y. Output charges were higher by .9% m/o/m and 2.6% y/o/y but I’m sure will catch up to the rise in costs.

27) In the UK, 11k jobs were lost in March and February was revised down to a fall of 6k vs the estimate of a rise of 20k. Jobless claims rose by 26.8k in March after an increase of 17.1k in February. Thru the 3 months ended February, the unemployment rate fell to 4.9% from 5.2% but was mostly due in part to a big fall in the size of the labor force looking for work. The wage gains were 3.6% y/o/y thru February vs 3.8% in January. There is obviously a mix here of March and February data, pre war, post war.

BY Doug Kass · Apr 24, 2026, 12:45 PM EDT

I have added to my shorts in (GRNY) at $26.64 and (JOET) at $43.01.

Position: Short GRNY (M), JOET (S)

BY Doug Kass · Apr 24, 2026, 12:15 PM EDT

Momentum is having an insane run right now. It's the biggest 18-day rally since June of 2000, which came after the dot com bubble's peak in March of 2000. Per BTIG's Jonathan Krinsky:

— Negligible Capital (@negligible_cap)

"The GS High Beta Momentum Long Index (GSCBHMOM) is having its second biggest 18-day run in… pic.twitter.com/TzvZflEG2p

BY Doug Kass · Apr 24, 2026, 11:55 AM EDT

BY Doug Kass · Apr 24, 2026, 11:35 AM EDT

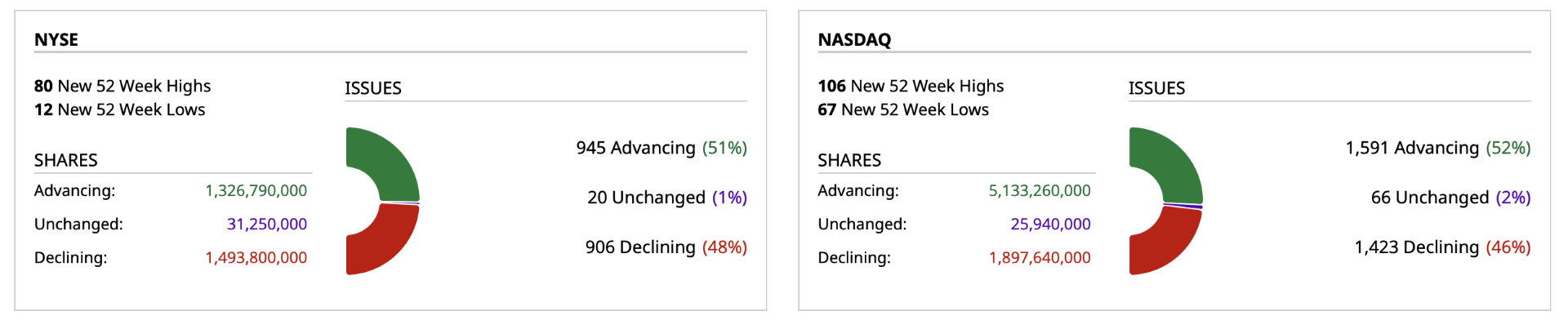

Despite the tech-led rally, breadth is nothing to write home about:

Dan Niles sees the possibility of a blow-off top in the league-leading semiconductors — let's watch closely.

I have taken small trading short rentals (with a tight stop) in:

* (AMD) $348.19

* (MU) $503.35

Position: Short AMD (VS), MU (VS)

BY Doug Kass · Apr 24, 2026, 11:25 AM EDT

- NYSE volume 12% below its one-month average;

- Nasdaq volume 24.5% above its one-month average;

- VIX index: down 2.38% to 18.85

Positions: None.

BY Doug Kass · Apr 24, 2026, 11:01 AM EDT

BY Doug Kass · Apr 24, 2026, 11:00 AM EDT

I covered my trading short rentals in the indexes (for a profit):

* (SPY) $709.27

* (QQQ) $656.97

I plan to reshort on any strength.

Positions: None.

BY Doug Kass · Apr 24, 2026, 10:05 AM EDT

Goldman Sachs says pension funds may sell roughly $25B in equities for month-end rebalancing, the largest non-quarterly rebalance on record.

— TT3 (@TradingThomas3)

Positions: None.

BY Doug Kass · Apr 24, 2026, 9:45 AM EDT

Hi Andy,

— Dan Niles (@DanielTNiles)

The 17 consecutive up days over which the Semiconductor Index (SOXX) gained 41% is unprecedented. Here are some stats to put this in perspective. The prior record is 15 days ending on June 11th, 2014 but that gain was for only 8%. The 11 day streak in 2017, the two 10…

Positions: None.

BY Doug Kass · Apr 24, 2026, 9:29 AM EDT

-INTC +30% earnings

-PG +3% earings

-MXL +30% earnings

-WKC +22%

-APPF +6% earnings

-FIX +6% earnings

-EW +4% earnings

-SLM +3% earnings

-ZM +3% Spurcepoint

-SAP +6% earnings

-SWKC +20% earnings

-PFG +6% earnings

-CHE +7% earnings

-FIX +7% earnings

-COUR -11% earnings

-BYD -6% earnings

-HIG -4% earnings

-WU -12% earnings

-CHTR -4% earnings

-HCA -8% earnings

-NSC -2% earnings

Positions: None.

BY Doug Kass · Apr 24, 2026, 9:19 AM EDT

Positions: None.

BY Doug Kass · Apr 24, 2026, 9:04 AM EDT

Positions: None.

BY Doug Kass · Apr 24, 2026, 8:59 AM EDT

Positions: None.

BY Doug Kass · Apr 24, 2026, 8:39 AM EDT

11:00 a.m.: Kansas City Fed Services Activity (April);(earnings calendar: TipRanks)

Positions: None.

BY Doug Kass · Apr 24, 2026, 8:34 AM EDT

I've moved to small-sized (up from very small) in index shorts:

* (SPY) $713.08

* (QQQ) $661.75

Position: Short SPY (S) QQQ (S)

BY Doug Kass · Apr 24, 2026, 7:45 AM EDT

This reporting by Simon Jack, the BBC's Business Editor, is rightly attracting a lot of attention this morning.#economy #markets #bbc @BBCSimonJack @bankofengland @BBC pic.twitter.com/LjIqg0DG0h

— Mohamed A. El-Erian (@elerianm)

BY Doug Kass · Apr 24, 2026, 7:40 AM EDT

Bloomberg just reported that Iran is considering returning to the negotiating table. That's causing a sharp ramp in futures now.

BY Doug Kass · Apr 24, 2026, 7:30 AM EDT

BY Doug Kass · Apr 24, 2026, 7:21 AM EDT

BY Doug Kass · Apr 24, 2026, 7:10 AM EDT

Ed Yardeni: "Apparently, the US stock market can live with $100 oil for now. Indeed, sentiment has turned more positive as can be seen in the latest readings of our two favorite Bull/Bear Ratios. They aren't high enough to give us pause about the stock market rally that started…

— David Kass (@DrDavidKass)

BY Doug Kass · Apr 24, 2026, 7:00 AM EDT

Chart of the Day: US Gasoline Fund (UGA)

The United States Gasoline Fund (UGA) broke-out of a high and tight flag to new all-time highs today.

This continuation pattern had built for weeks following the massive multi-year breakout, and suggests the path of least resistance for Gasoline is now higher.

Meanwhile, markets weakened as UGA rallied, reinforcing the negative correlation between rising energy prices and a supportive backdrop for risk assets.

The Takeaway: Upside pressure in gasoline may be an early sign that geopolitical risk is creeping back into markets.

$SPX Possible double top or just a consolidation within an ongoing uptrend?

— Rachel Dashiell, CFP, CMT (@RachelDashCS)

7050 acting as crucial near term support after Tuesday's gap fill

*Not a recommendation@SchwabTrading @SchwabNetwork pic.twitter.com/jbwowbuTh0

2026 has yet to see any major Advance or Decline moves as measured by 10:1 days. All considered, markets have remained fairly calm from a broad breadth perspective. pic.twitter.com/V1JoXj6fXz

— Andrew Thrasher, CMT (@AndrewThrasher)

For the 10th time since 2000, $SPX gained 1% with more stocks declining than advancing (-66 spread), and only the 3rd time it did so to make a new ATH: pic.twitter.com/6703Ib27lr

— Optuma (@Optuma)

11/ Over the past few years, a noticeable gap has formed between gold and the price of some key commodities.

— Bravos Research (@bravosresearch)

The primary reason for this is that there was very little concern regarding their supply.

This has helped keep their prices low despite the debasement of the US dollar. pic.twitter.com/sEUGuntk8H

— Aksel Kibar, CMT (@TechCharts)

Unlike some, we didn't sell our Energy Exposures - new Cycle Highs for us in $OIH terms pic.twitter.com/Ita9wyMzJx

— Keith McCullough (@KeithMcCullough)

Bonus — Here is a great link:

BY Doug Kass · Apr 24, 2026, 6:45 AM EDT

Wolf Street howls about natural gas supply/demand.

BY Doug Kass · Apr 24, 2026, 6:35 AM EDT

* And more than two standard deviations above historical norms...

🇺🇸 Valuations

— ISABELNET (@ISABELNET_SA)

After the recent surge, US stocks are firmly out of bargain territory. Most valuation gauges are stretched, sitting more than two standard deviations above historical norms. "Cheap" is not part of the current narrative

👉https://t.co/14i5SQVCfd

h/t @SoberLook $spx pic.twitter.com/iojTKhw7C6

BY Doug Kass · Apr 24, 2026, 6:25 AM EDT

JP Morgan on Tesla (TSLA) :

JP Morgan still looking for a 61% crash in Tesla's stock: pic.twitter.com/qKS0P54k7S

— Brian Sozzi (@BrianSozzi)

Position: Short TSLA (S)

BY Doug Kass · Apr 24, 2026, 6:15 AM EDT

"Two companies alone account for 50% of the earnings growth in the first quarter, Micron and Nvidia. Two companies. That's it. 50% of the earnings growth. And if you roll it forward to the full year of 2026, those two companies account for a third of the entirety of the earnings… pic.twitter.com/ylA35TDPZd

— Excess Returns Podcast (@excessreturnpod)

BY Doug Kass · Apr 24, 2026, 6:05 AM EDT

Reestablished index shorts

From Comments section:

Dougie Kass

Thursday night trading. 930PM

Reestablished Index shorts:

SPY $710.14 QQQ $656.38

small sized for now

And from Randorama:

Randy

Yankees sweep of the Stink Sox has ya feelin' better.

Position: Short SPY (VS), QQQ (VS)

BY Doug Kass · Apr 24, 2026, 5:55 AM EDT

The S&P Short Range Oscillator remains (albeit less) overbought at 4.52% vs. 5.36%.

Position: Short SPY (VS)

BY Doug Kass · Apr 24, 2026, 5:45 AM EDT

Momentum is having an insane run right now. It's the biggest 18-day rally since June of 2000, which came after the dot com bubble's peak in March of 2000. Per BTIG's Jonathan Krinsky: "The GS High Beta Momentum Long Index (GSCBHMOM) is having its second biggest 18-day run in Show more

Goldman Sachs says pension funds may sell roughly $25B in equities for month-end rebalancing, the largest non-quarterly rebalance on record.

Ed Yardeni: "Apparently, the US stock market can live with $100 oil for now. Indeed, sentiment has turned more positive as can be seen in the latest readings of our two favorite Bull/Bear Ratios. They aren't high enough to give us pause about the stock market rally that started Show more

BREAKING: Consumer sentiment in the US officially hits its lowest level on record amid the Iran War. This marks the weakest consumer sentiment since data collection began in 1978.

🇺🇸 Valuations After the recent surge, US stocks are firmly out of bargain territory. Most valuation gauges are stretched, sitting more than two standard deviations above historical norms. "Cheap" is not part of the current narrative 👉isabelnet.com/?s=valuation h/t @SoberLook $spx

This reporting by Simon Jack, the BBC's Business Editor, is rightly attracting a lot of attention this morning. #economy #markets #bbc @BBCSimonJack @bankofengland @BBC

"Two companies alone account for 50% of the earnings growth in the first quarter, Micron and Nvidia. Two companies. That's it. 50% of the earnings growth. And if you roll it forward to the full year of 2026, those two companies account for a third of the entirety of the earnings Show more

For the 10th time since 2000, $SPX gained 1% with more stocks declining than advancing (-66 spread), and only the 3rd time it did so to make a new ATH:

11/ Over the past few years, a noticeable gap has formed between gold and the price of some key commodities. The primary reason for this is that there was very little concern regarding their supply. This has helped keep their prices low despite the debasement of the US dollar.

$SPX Possible double top or just a consolidation within an ongoing uptrend? 7050 acting as crucial near term support after Tuesday's gap fill *Not a recommendation @SchwabTrading @SchwabNetwork

2026 has yet to see any major Advance or Decline moves as measured by 10:1 days. All considered, markets have remained fairly calm from a broad breadth perspective.

Unlike some, we didn't sell our Energy Exposures - new Cycle Highs for us in $OIH terms

#INDUSTRIAL #METALS looking good. This one is #NICKEL