From Peter Boockvar:

Sentiment/"SoH remain firmly closed"/Earnings/Mfr'g up overseas but all front running

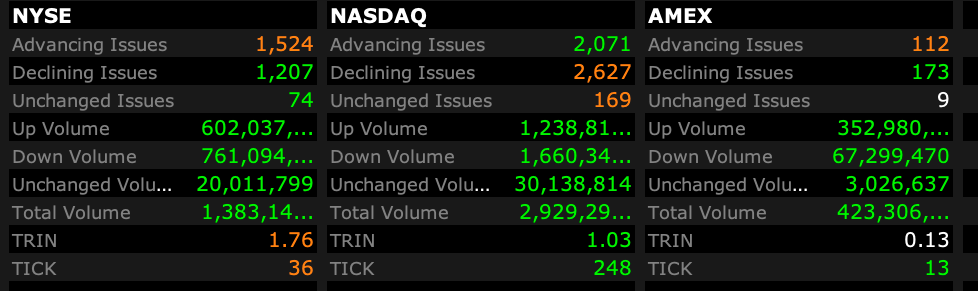

Nothing like a stock market rally to lift sentiment as mood always follows price. In the most fickle and volatile sentiment survey, the AAII retail one today saw Bulls jump by 14.3 pts to 46, the highest since mid January. Bears fell by 8.4 pts to 34.4, the least since February 5th. The Investors Intelligence survey saw Bulls jump to 48.1 from 39.6 while Bears fell 1.6 pts w/o/w to just 21.1. The CNN Fear/Greed index yesterday closed at 69 vs 10 at the end of March.

Bottom line, nothing here is extreme but quite the mood shift in only a few weeks.

Meanwhile, Maersk released this today saying “Given the ongoing Middle East position and the escalation in the situation - with 3 container ships attacked by Iranian forces this week - the SoH remain firmly closed. We cannot guarantee safe passage and safety of our people, assets and our customers’ cargo remains the top priority.”

Source: maersk.com.

I bolded for emphasis.

On to a bunch of earnings call/earnings release comments with everyone manuevering through a challenged and changed situation.

Taylor Morrison rallied 5% yesterday and said this of note:

“As I shared on our last earnings call in February, early signs heading into the spring selling season were positive and the quarter played out largely as we expected with sales activity building through the quarter and March representing our strongest month. That momentum is consistent with normal seasonal patterns, albeit with slightly less acceleration than we have seen historically, reflecting continued consumer cautiousness.”

“April started off somewhat slower, as typical, coinciding with the holiday weekend, but momentum then picked back up and we’re looking forward to a strong end to the month, even with all the headline noise.”

“Since we last spoke, the market has been faced with another round of geopolitical turmoil, intensified macro uncertainty, and a shift higher in mortgage rates. As we would expect, consumer confidence has been impacted by these developments, exasperating affordability constraints and AI related employment concerns. However, we believe the underlying desire for the homes and communities we build remain strong, even as the broader macro environment has given consumers reason to be more deliberate in their decision making.”

PulteGroup today said “Within a demand environment impacted by domestic and global dynamics, we see a consumer with concerns about affordability and the economy, but still desirous of homeownership as demonstrated by the 3% growth in our first quarter net new orders.” Their sales fell 12% y/o/y with 7 points of that due to volume and 5 percentage points caused by a lower average sales price.

In the same industry, Masco sells faucets, kitchen and bath cabinets, paint coatings, among other things and whose stock rose 11% yesterday. They said this:

“Net sales increased 6% or 4% in local currency, primarily driven by favorable pricing.”

To their expectations for pricing this year, “our plumbing expectation is mid single digit.” In terms of higher costs in their paint business, it’s “mid to high single digits.” And, “I think from an overall company perspective, we would expect mid single digit inflation.”

“DIY paint sales decreased low single digits while PRO paint sales grew mid single-digits.”

“While uncertainty remains in the near term, we are focused on positioning ourselves for ongoing sales and profit growth over the mid to long term. The structural factors for repair and remodel activity are strong, including record high home equity levels, the age of the housing stock, and increasing pent-up demand for renovation projects.”

“While we are pleased with our strong results in the first quarter, there remains a high degree of uncertainty in the macroeconomic and geopolitical environment. As a result, we are largely maintaining our full year outlook.”

To their raw materials used, “Copper prices remain elevated and oil, which impacts a wide range of material, as well as logistics costs, also remain elevated and volatile. We continue to monitor these dynamics and will work diligently to mitigate the impacts as we have demonstrated in the past.”

From UAL that got hit by 6% yesterday:

“At the moment, our goal is to do whatever it takes to recover 100% of the increase in jet fuel prices as quickly as possible and to achieve double digit pre-tax margins next year.”

And how will they do that?, “to recover 100% of fuel costs, yields need to increase by about 15% to 20% and we are assuming that fuel may remain higher for longer. Two, as yields increase, there will be an elasticity effect on demand, we’re estimating it will lead to less overall demand. While we haven’t actually seen that decline yet, ECON 101 makes us believe it’s coming. Three, less demand means that we should be supplying fewer seats to the market.”

Speaking of travel, Travel & Leisure, the owner of vacation ownership, got slammed by 14% yesterday, though they were optimistic about the travel sector on their call:

“Overall, our owner base remains healthy. They are prioritizing travel, and we are not seeing any meaningful shifts in their behavior. First quarter gross bookings were up y/o/y. The booking window remains steady at approximately 100 days and average length of stay is unchanged y/o/y at just over four days. The distance traveled to our resorts in Q1 was actually up slightly to last year, indicating consumers’ willingness to travel to our resorts. The data suggests that in uncertain economic times, our value proposition becomes even more relevant.”

“As we enter our peak sales season, we are mindful of the macro backdrop and its potential to influence consumer behavior. That said, the trends we are seeing remain healthy, our value proposition continues to resonate, and the model is performing as designed, positioning us to outperform across cycles.”

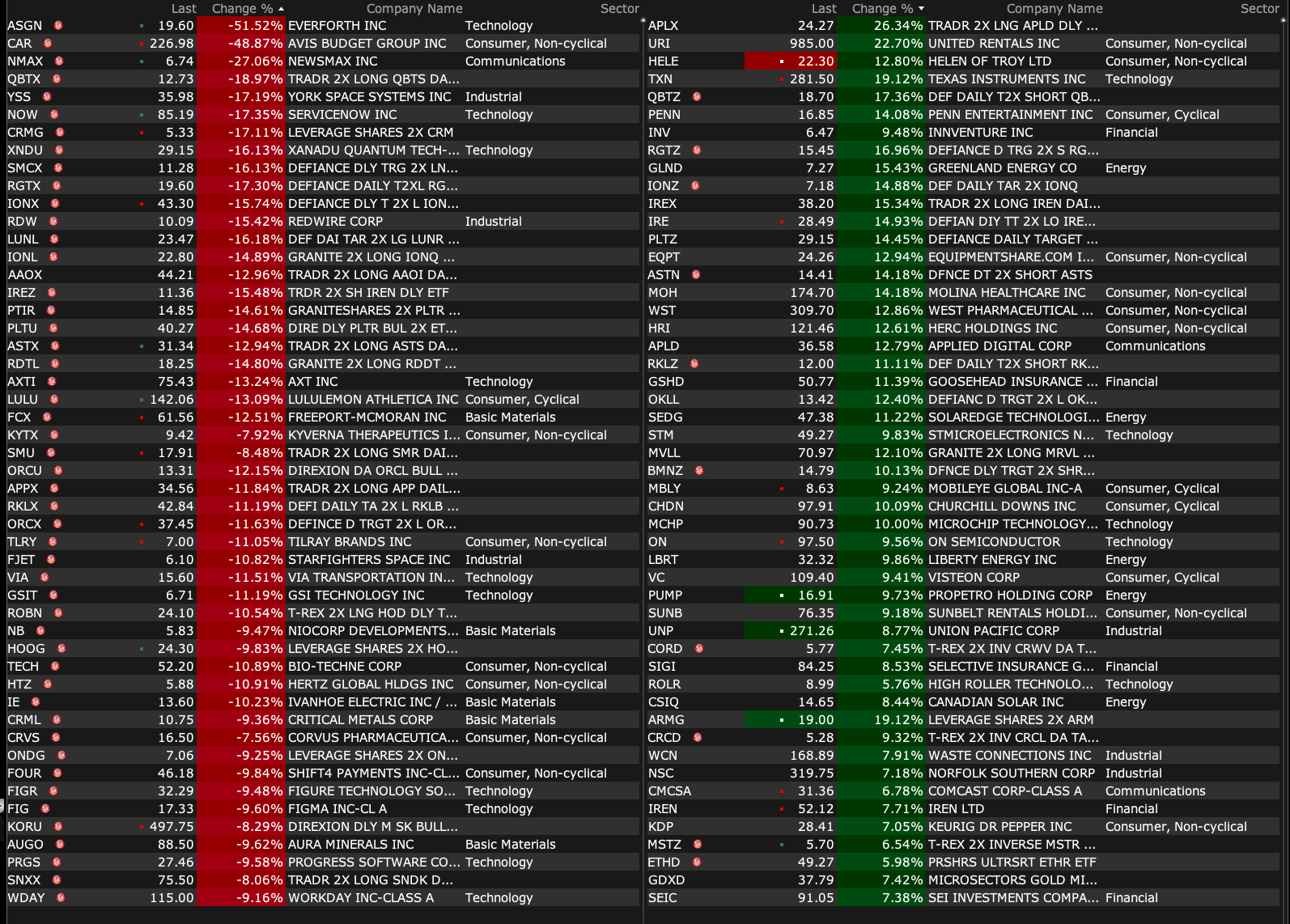

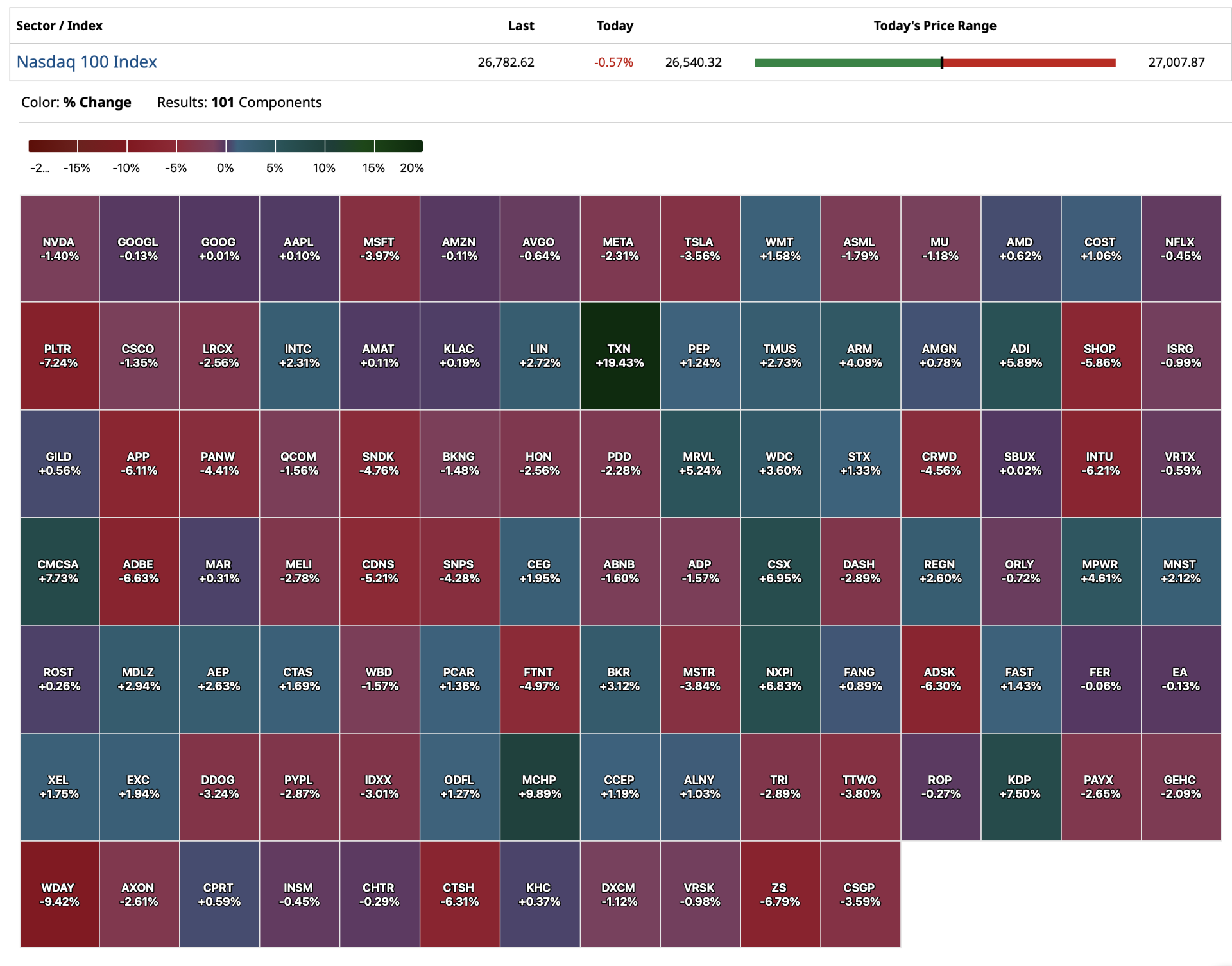

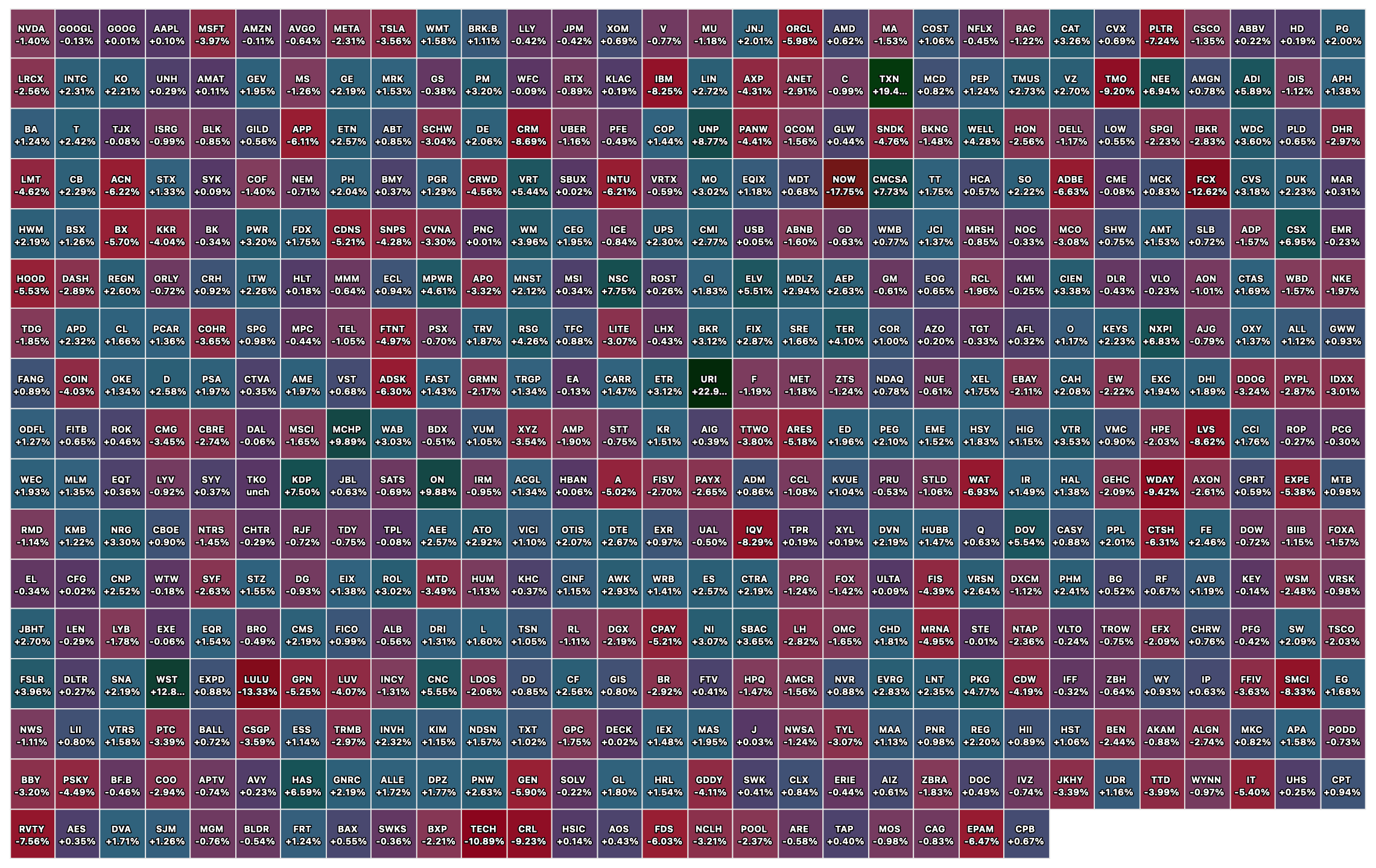

From Texas Instruments, whose stock is roaring higher pre market and said this of note:

“In the first quarter, revenue came in above the top of the range, as we saw continued acceleration in industrial and data center. The overall semiconductor market recovery is continuing and we remain well positioned with inventory and capacity that allows us to support our customers with competitive lead times through the cycle.”

“Industrial increased more than 30% y/o/y, and was up more than 20% sequentially, growing broadly across all sectors and regions.” Included here is energy infrastructure, power delivery and aerospace and defense.

“Automotive increased mid single digits y/o/y, and was about flat sequentially.”

“Data center grew about 90% y/o/y, and grew more than 25% sequentially.”

“Personal electronics was flat y/o/y, and grew low single digits sequentially. And lastly, communications equipment grew about 25% y/o/y and grew more than 30% sequentially.”

CSX is also jumping pre market and said this:

“One emerging positive here is that shippers are looking more to rail conversion as they weigh the impacts of higher fuel and trucking costs.”

From Philip Morris, a stock we own and benefiting from the shift away from combustible cigarettes and its fast growing Zyn nicotine pouch business:

“The Middle East conflict had a small impact on our business in the first quarter, which affected shipment to global travel retail and certain markets in the region for both combustible and HTUs (heated tobacco units). While we have observed increased energy prices and some disruption in energy supply in a number of markets, this has not at this stage translated into a discernibel shift in consumer behavior.”

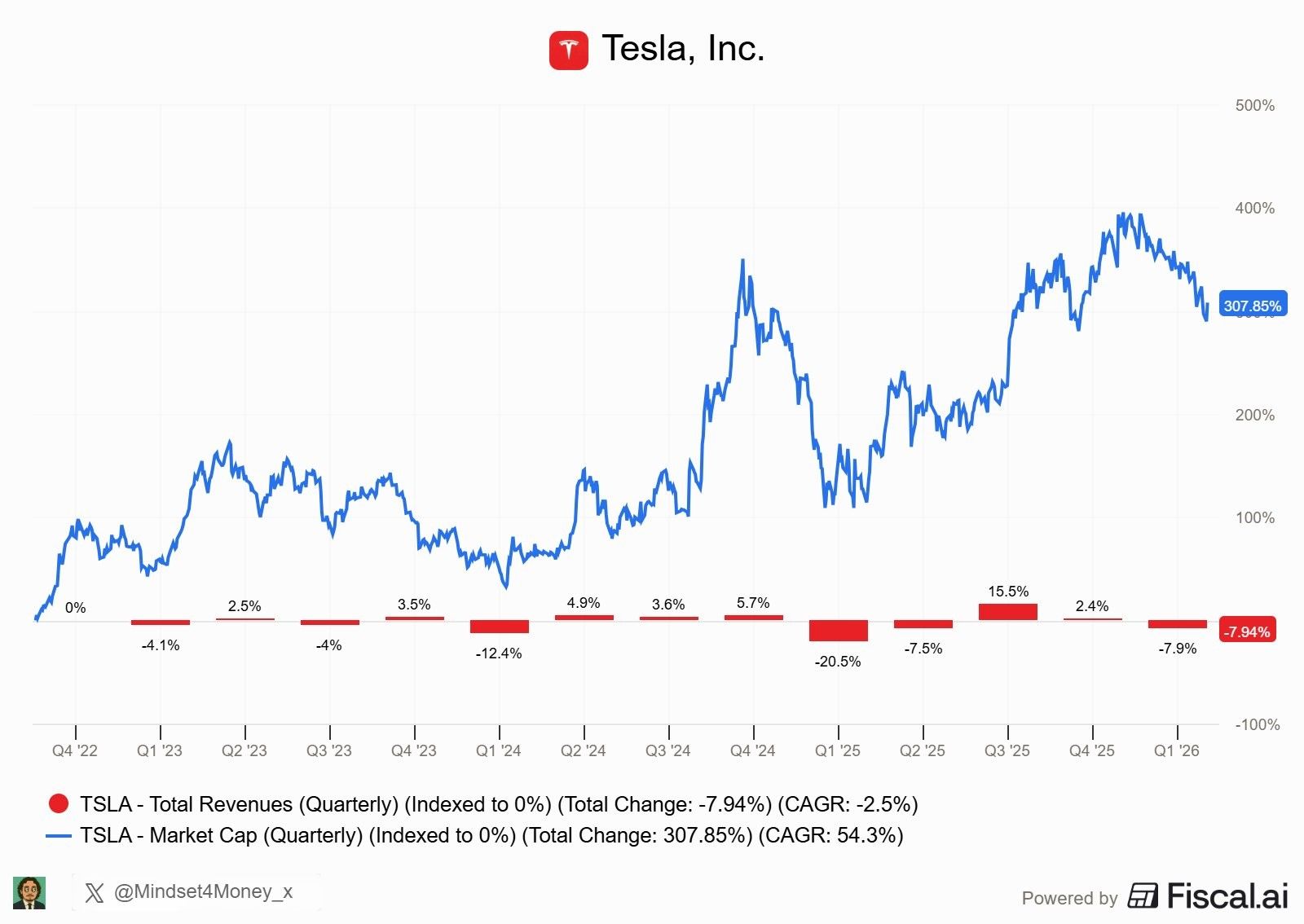

From Tesla and Elon Musk and whose stock is down about 3% pre-market because of the ramp up in spending:

“We’re going to be substantially increasing our investments in the future. So should expect to see a very significant increase in capital expenditures, but I think well justified for a substantially increased future revenue stream.”

“Obviously Tesla is not alone in this. I think you’ve seen in most, if not all, certainly the major technology companies substantially increasing their capital investments, and we’re going to be doing the same. I think it’s going to pay off in a very big way. So we’re investing in and improving our core technologies, battery powertrain, AI software, AI training, chip design, manufacturing design - laying the groundwork for significantly increased manufacturing production.”

“On the autos business, we have seen a resurgence in demand in EMEA and certain countries like France and Germany showing over 150% q/o/q growth in deliveries. In APAC, we witnessed growth in South Korea and Japan, again in terms of deliveries. Even out here in the US, we have seen slight growth in terms of q/o/q deliveries.”

“Whilst the recent increase in gas prices has had a positive impact on the order rate, this improvement started before the uptrend in gas prices.”

PMI’s for April have started to flow out today and the manufacturing side around the world continues to improve, in part I’ve argued due to front running of orders on supply chain concerns.

Japan’s April manufacturing PMI rose to 54.9 from 51.6 while services fell to 51.2 from 53.4. In Australia, they saw improvement for both components with manufacturing at 51 vs 49.8 and services bouncing to 50.3 from 46.3. In India, manufacturing rose 2 pts m/o/m to 55.9 and services came in at 57.9 vs 57.5. Still doing well notwithstanding their imported energy exposure.

With manufacturing in Japan and to what I’ve been believing, “There were reports that some manufacturing firms boosted output due to concerns and uncertainty surrounding the war in the Middle East and the potential for further supply chain disruptions. The latter contributed to not only a much sharper rise in costs, but the most pronounced increase in average delivery times for manufacturers’ inputs for nearly four years.” I bolded to highlight.

The drag, “The latest survey also point to weaker expectations regarding future output. In fact, business confidence fell to the lowest level since August 2020, amid the depths of the Covid 19 pandemic.”

The same manufacturing lift was seen in the Eurozone and UK. The Eurozone April manufacturing PMI rose to 52.2 from 51.6, offset by the drop in services to 47.4 from 50.2. Combining the two puts their composite index back below 50 at 48.6 vs 50.7.

Boosting manufacturing, “Manufacturers have increased their buying of inputs to a degree not witnessed since early 2022 as supply chain delays have also risen to the most widespread since the pandemic.”

And this comes along with it, “Input costs and selling prices have already jumped higher not just in response to higher energy costs but in a reflection of a broader upturn in commodity prices and mismatch of demand against strained supply. If the Covid 19 pandemic is excluded, this is the biggest surge in cost pressures that we have recorded since 2000.”

Lastly, “Not surprisingly, businesses are taking an increasingly gloomy view of the outlook, with sentiment now down to its lowest since late 2022.”

In the UK, manufacturing was up to 53.6 from 51 and services grew too to 52 from 50.3. Same thing here, “The improved rate of expansion is in part a reflection of a short term boost from a rush to secure purchases ahead of feared price rises and supply shortages linked to the war.“

And this, “Prices have spiked higher at a rate not previously seen by the survey outside of the pandemic, suggesting inflation could rise more than many forecasters have been anticipating. Prices are rising not just because of surging energy costs, but also due to increases in charges levied for a wide variety of goods and services, with price hikes often stoked by supply concerns. The number of supply delays reported has jumped to the highest on record if the pandemic is excluded.“

The UK CBI industrials order index plunged to -65 from -19 in April.

Business confidence in France got hit too, falling to 94 from 97 and vs the estimate of 96. Manufacturing confidence held in but hit by a drop in retail and services confidence.

Positions: None.