From Peter Boockvar:

Dramamine now/Some good macro takes from MMM, TSCO, COF and UAL

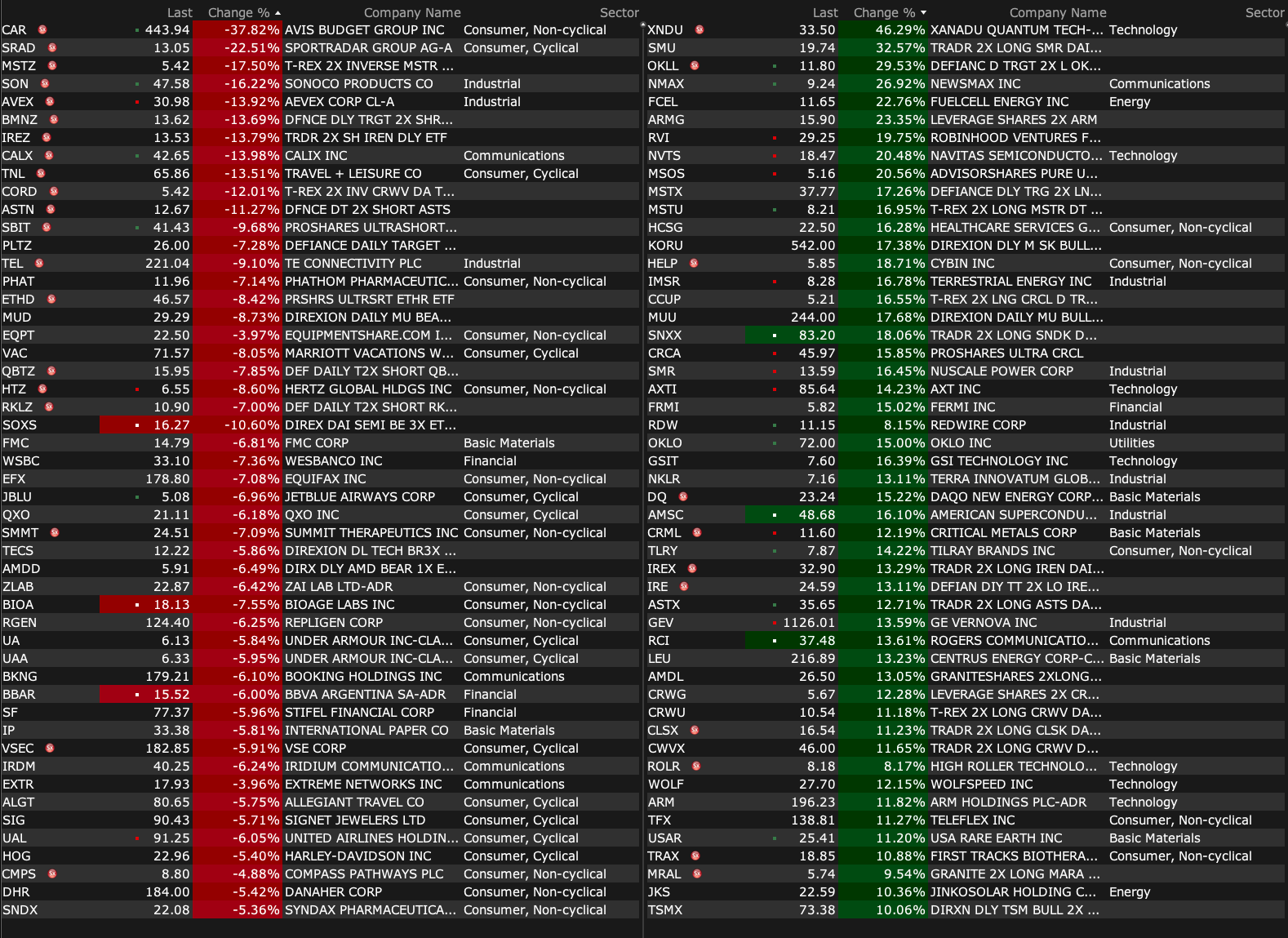

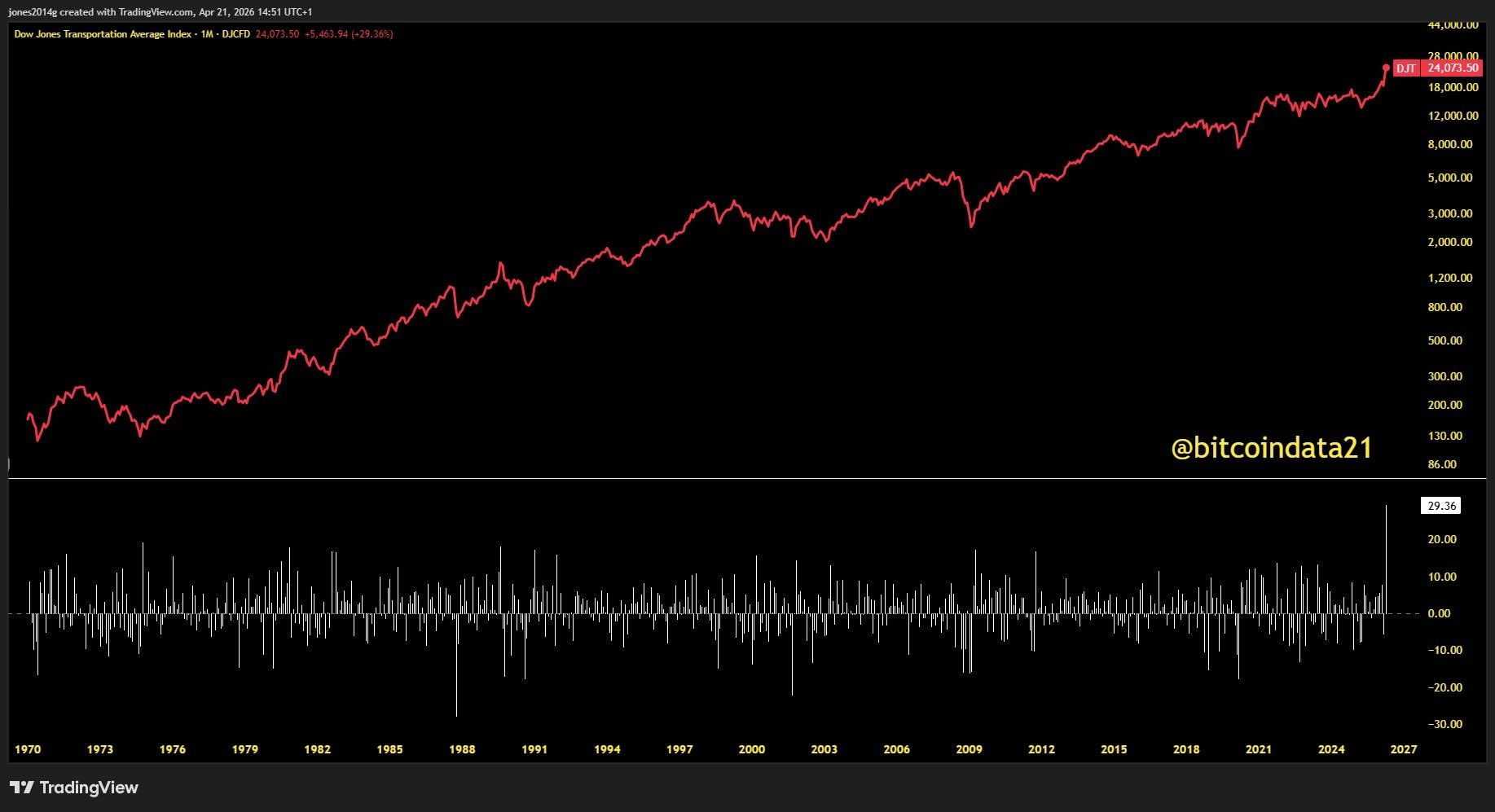

Dramamine now, and I’m not just talking about the daily volatility around every news clip related to Iran and the Strait, watching the move higher in Avis (CAR) is quite extraordinary. It now makes up almost 20% of the DJIA Transportation Index and this index is more than 35% above its 200 day moving average, the widest since 1989 according to my old colleague Jonathan Krinksy, currently at BTIG.

From MMM and whose stock fell 2% yesterday:

“We had a light start to the year on the top line with organic growth of 1.2%, driven by pockets of macro pressure, but we saw encouraging order trends that support our outlook for acceleration in the balance of the year.”

“When you look across our portfolio, roughly 60% of our businesses showed relative strength in Q1, including General Industrial and Safety...At the same time, we experienced macro and industry driven softness in about 40% of the portfolio that we’ve been highlighting as watch areas.”

“Our performance in semiconductor and data centers was very strong, while consumer electronics was soft due to industry wide memory chip issues, which is impacting demand.”

“In automotive, the market was soft as expected in the first quarter. Global build rates were down 3% overall and 10% in China, which pressured volumes. And in Consumer, we continue to see soft US consumer discretionary spending with a few pockets of strength in categories with recent new product introductions.”

They are seeing rising costs in raw materials as to be expected. “So it’s ethlenes, propylenes, esters, acrylates, all those various things. And we are seeing some upward cost pressure on that. What we’ve seen so far and expect is about $125 million of cost increases there, which are offsetting into pricing...that we expect about a 50 basis point uplift on price coming from that oil based exposure.”

Tractor Supply traded down 12% yesterday and they said this:

“The retail environment remains cautious but stable, with spending focused on needs and small indulgences, with some evidence of trip consolidation.”

Specifically, “In Pet, the category remains pressured, and while we are holding our share, our performance is below our expectations...Dog ownership, particularly in larger breeds, has come under pressure, and our mix remains heavily weighted towards dog...Cat ownership is growing and gaining share, and that’s where we under index.”

“A good example of consumer spending is around their tax refund behavior. While refunds did come through and we captured our fair share, customers are using these dollars more cautiously. A significant portion is going towards essentials, savings and debt reduction rather than discretionary spending, consistent with the broader environment we’re seeing.”

About all of their comp gain was price, “average ticket increased 1.6%, reflecting a combination of inflation and category mix. Retail price inflation was the primary driver to the average ticket increase at approximately 150 bps contribution, along with a category mix benefit, principally from big ticket sales growth. This was partially offset by a modest decline in units per transaction.”

From Capital One that is trading down pre-market because of a rise in credit loss provisions:

“In our Domestic Card segment, the allowance balance was flat at $18.8 billion. Favorable observed credit in the quarter was offset by greater consideration to downside economic scenarios related to heightened geopolitical uncertainty.” Their card delinquency rate did slip by 29 bps q/o/q and by 55 bps y/o/y.

In their consumer banking area, “The allowance build was primarily driven by strong growth in the auto business, a slightly higher subprime mix in that growth, and a modestly lower outlook for vehicle values.” Auto delinquency rates fell too, lower by 72 bps y/o/y.

They also raised their allowance in commercial banking “primarily driven by a very small number of specific reserves in our real estate portfolio, as well as a modest increase in our criticized rate.”

On the state of their consumer, “So the US consumer remained healthy and the overall economy remained resilient through the first quarter. The unemployment rate improved slightly in the quarter. Despite some high profile headlines about layoffs, the total volume of job losses and new jobless claims remains low and stable. Income growth continue to run ahead of inflation. Consumer spending remained robust. Because of last year’s budget bill, tax withholdings are lower than a year ago and tax refunds are higher.”

“In our Domestic Card business, our credit metrics continue to improve on a y/o/y basis in the quarter. On a sequential quarter basis, our charge-off rate moved in line with seasonality, while our delinquencies improved relative to what we would expect from normal seasonality. Our auto credit metrics remained strong as well. Auto losses were slightly higher on a y/o/y basis in Q1, but this was consistent with a modest increase in the subprime mix of that portfolio over the past year. Our auto losses have been back near pre-pandemic levels for over a year. And our auto credit is supported by strong performance of recent originations and generally stable vehicle prices.”

“Of course, the new conflict in the Persian Gulf represents a significant cloud on the horizon. We’ve already seen energy prices spike sharply over the past six weeks. Inflation moved higher in March, largely because of the higher gas prices. So if energy prices remained elevated for an extended period of time, that would be a real headwind for consumers and probably a drag on the overall macroeconomy. But so far, we’ve not seen any adverse effects on our portfolio, either in our credit or in our spend metrics. We’ve judgmentally incorporated elevated macroeconomic risk into our allowance through qualitative factors. But we continue to really feel very good about not only our portfolio performance, but good for the credit outlook of consumers and good for the opportunity to continue to lean in to origination and credit line growth in our business.”

While lowering their full year guidance because of higher fuel costs, United Airlines is trading up after reporting and they said this in their earnings release ahead of their call today:

Their fuel bill went up by $340 million but “United’s capacity and revenue initiatives are intended to recapture this increase over the long term.”

“United’s diverse revenue streams remained resilient, including premium revenue up 14% compared to the first quarter of 2025, loyalty revenue up 13%, and revenue from basic economy up 75. Business revenue also remained strong at up 14% for the first quarter.”

To some economic data. With another dip in the average 30 yr mortgage rate to 6.35%, purchase applications jumped by 10% w/o/w while refi’s were up by 5.8%. We need to see a run of higher wage growth relative to home price growth to help on the affordability front.

Capturing the war, Japanese exports in March rose by 11.7%, about in line with the estimate of up 11%. Imports grew by 10.9%, higher than the forecast of up 7%. Helping trade was China reopening after their Lunar New Year holiday and likely too a rush to get stuff with growing worries of supply chain issues.

In the UK, March CPI was hot, up by .7% m/o/m and by 3.3% y/o/y vs 3% in the month before. Of course higher energy costs were the main factor with motor fuel jumping by 8.7%. The core rate though was still up by 3.1% y/o/y vs 3.2% in February. Services inflation remains persistent, up by 4.5% y/o/y vs 4.3% in February. All these stats were about as expected though and why the 10 yr UK inflation breakeven is unchanged at 3.41%. The 2 yr and 10 yr gilt yields are little changed too.

Wholesale prices were very hot, with input prices spiking by 4.4% in the month alone and by 5.4% y/o/y. Output charges were higher by .9% m/o/m and 2.6% y/o/y but I’m sure will catch up to the rise in costs.

Finally, Bank Indonesia left its benchmark rate unchanged at 4.75% as expected and their bias is up with rates. “Bank Indonesia is prepared to implement a further strengthening of monetary policy as needed to maintain the stability of the rupiah exchange rate and keep inflation in 2026 and 2027 within the target range.”