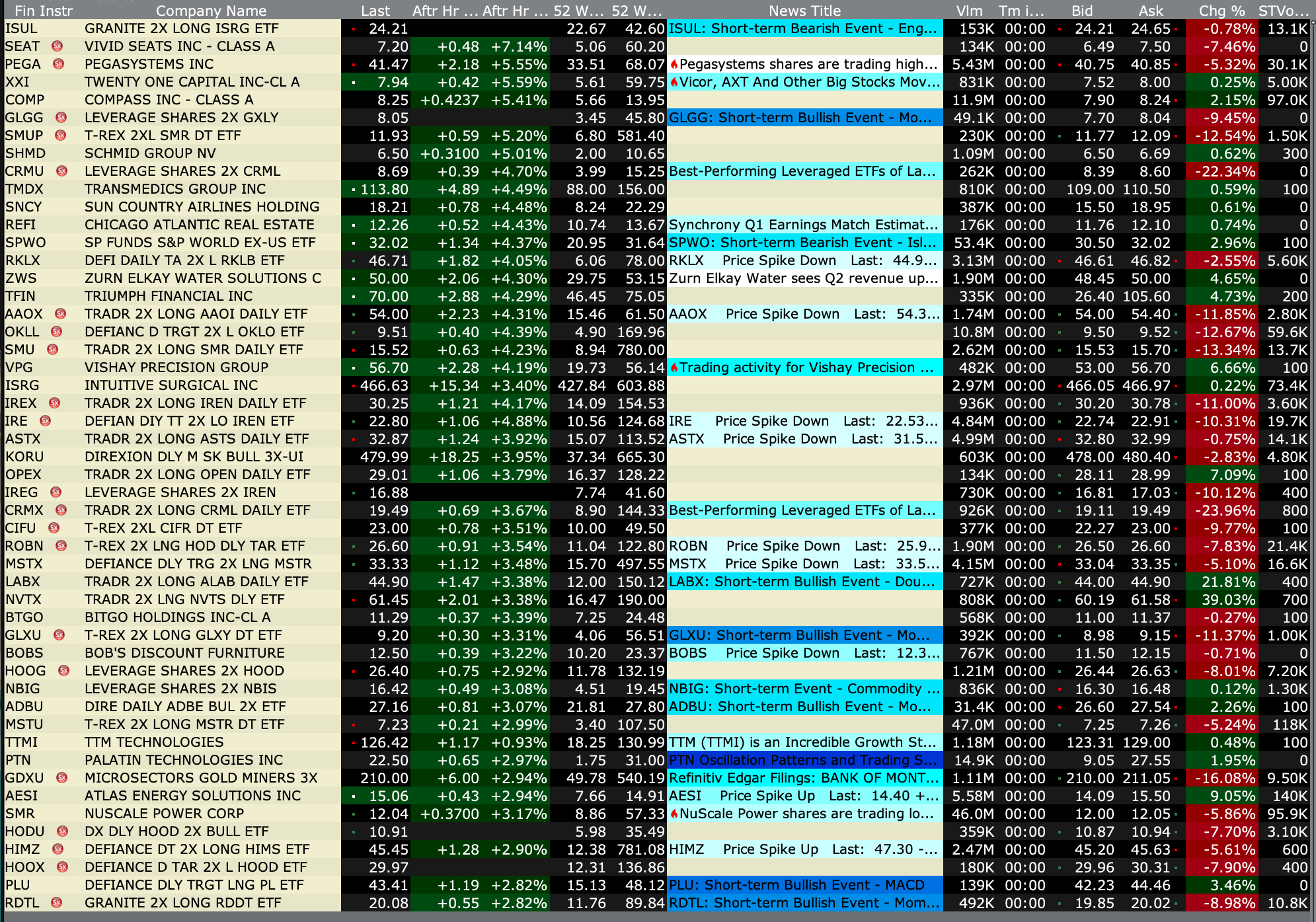

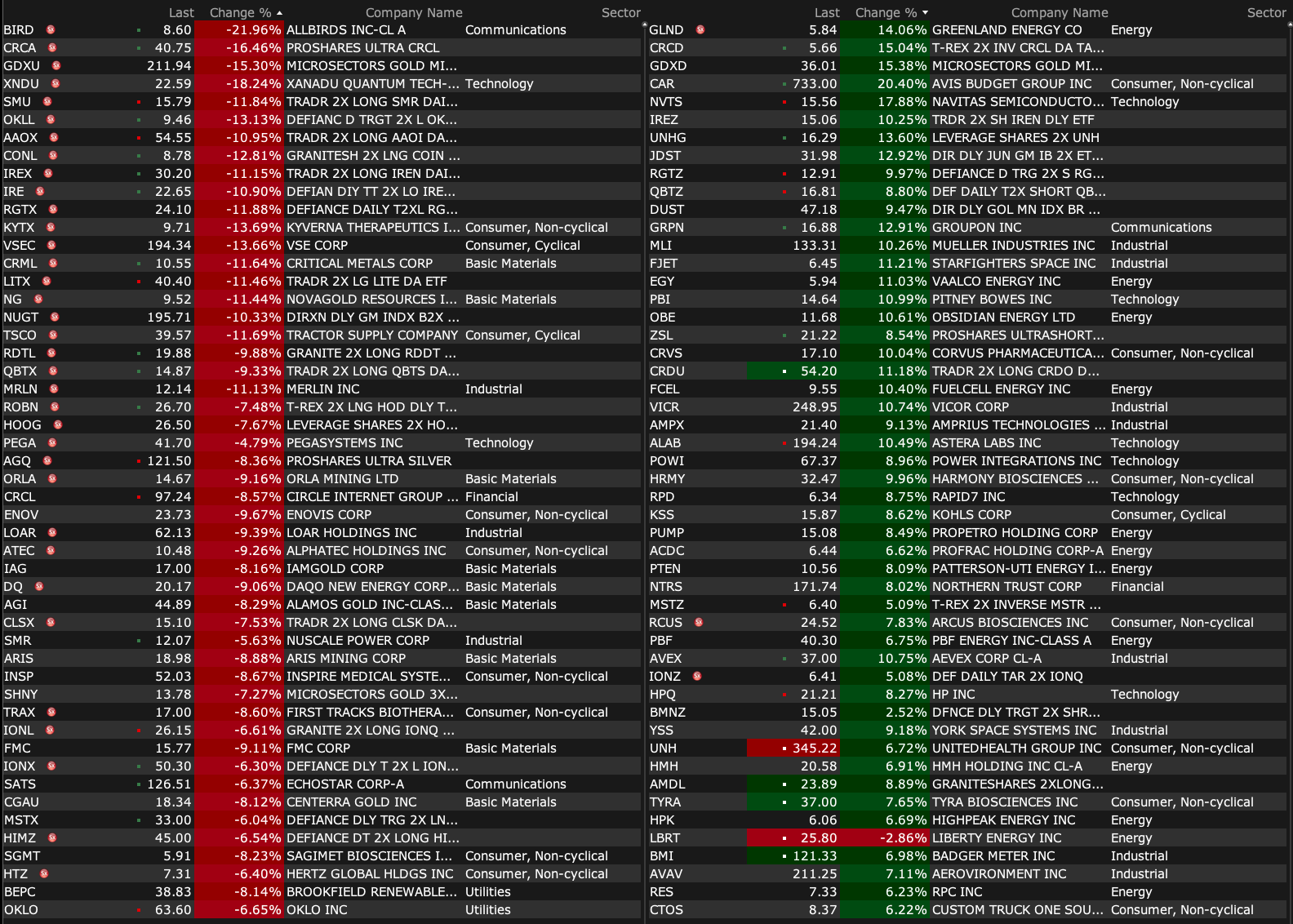

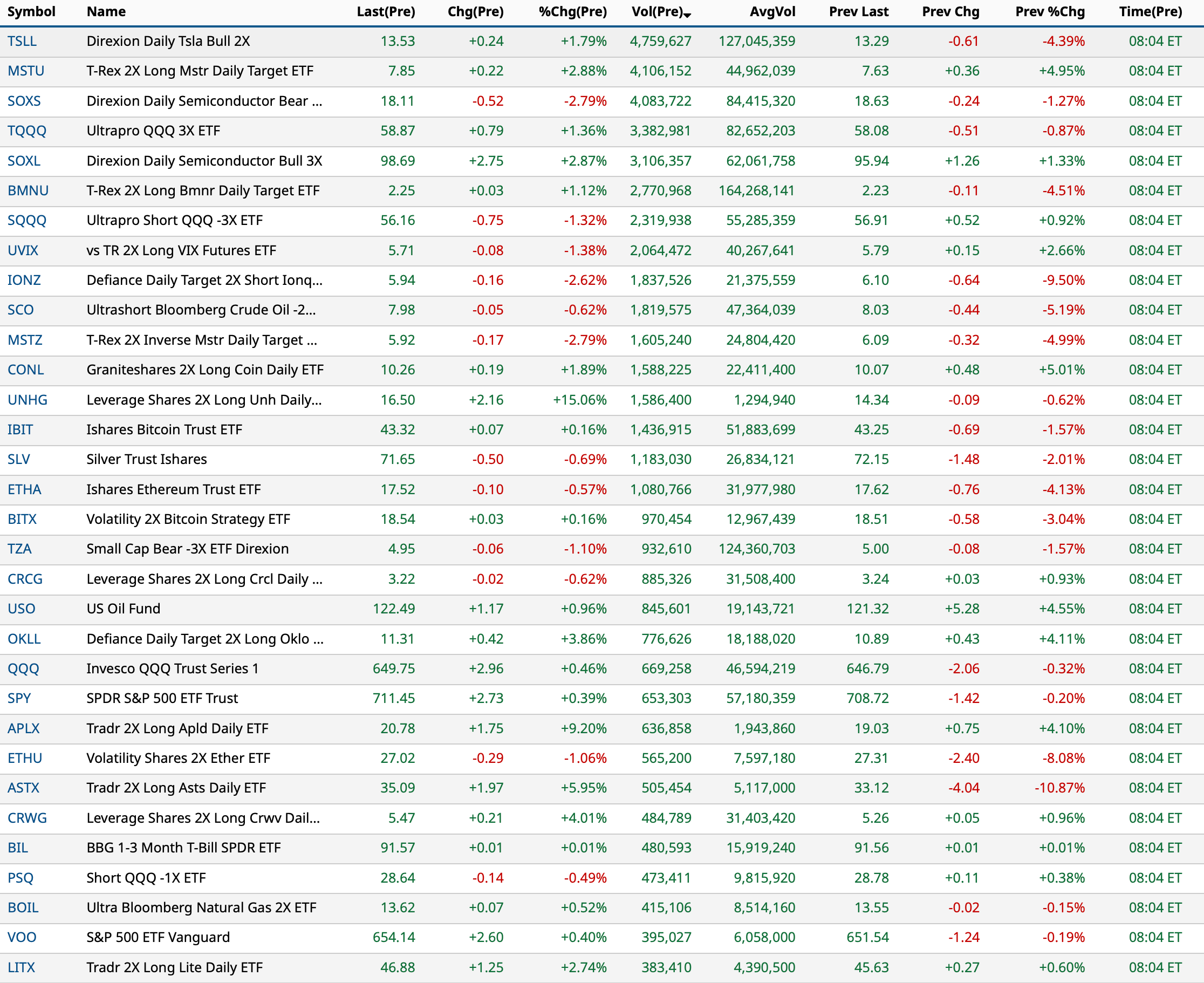

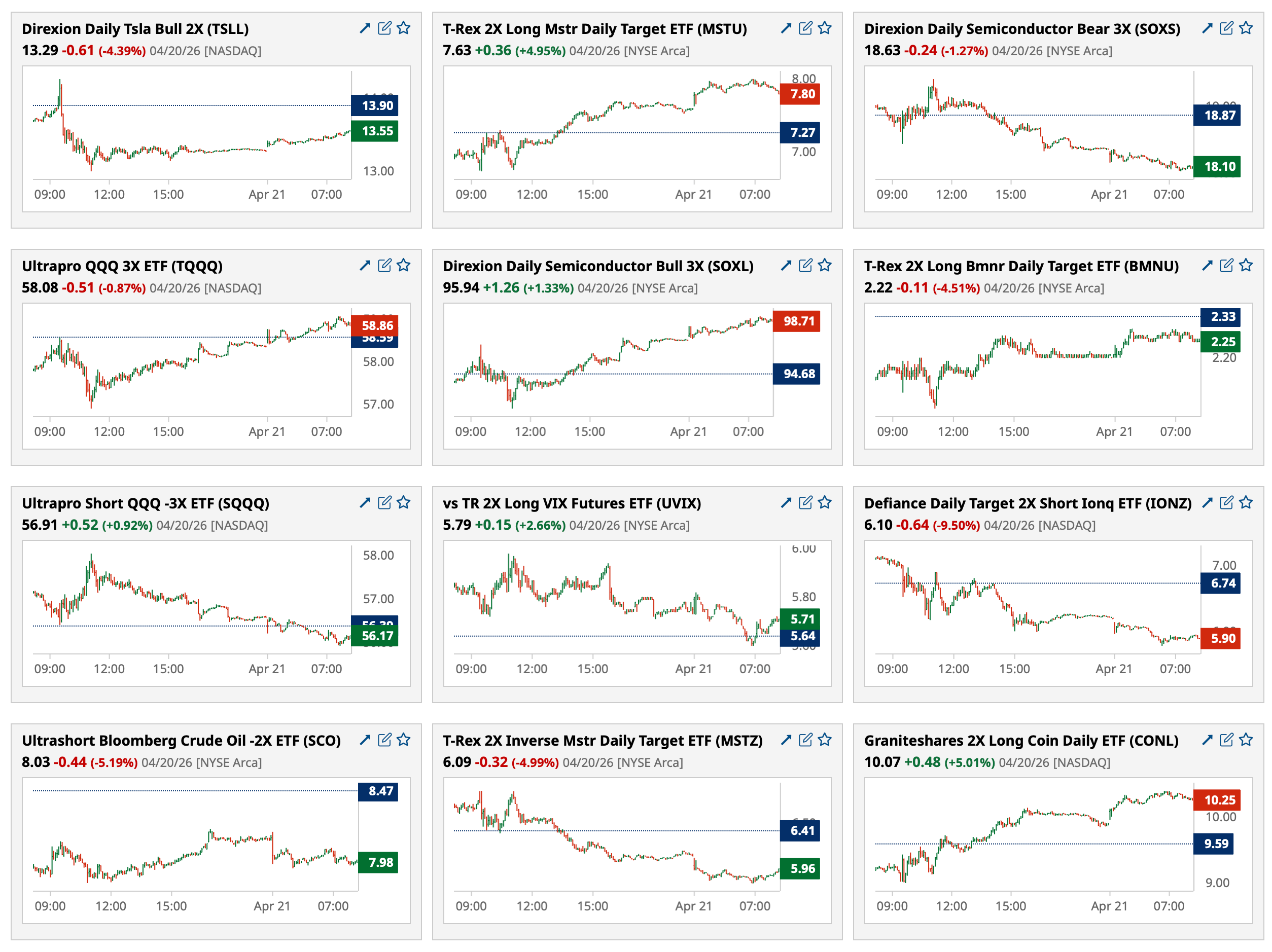

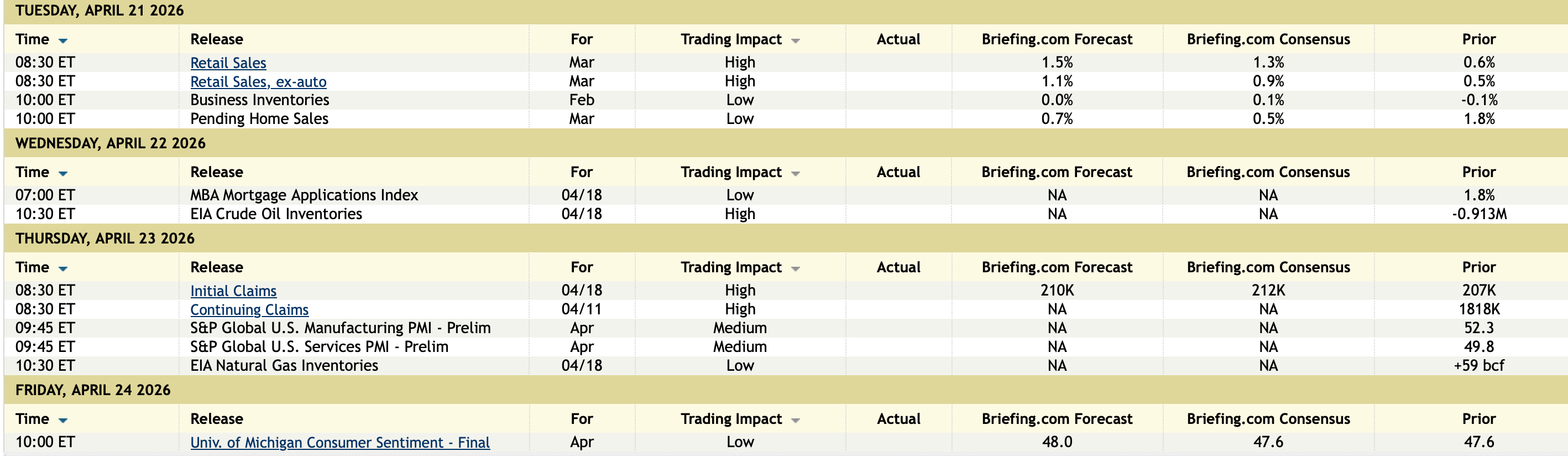

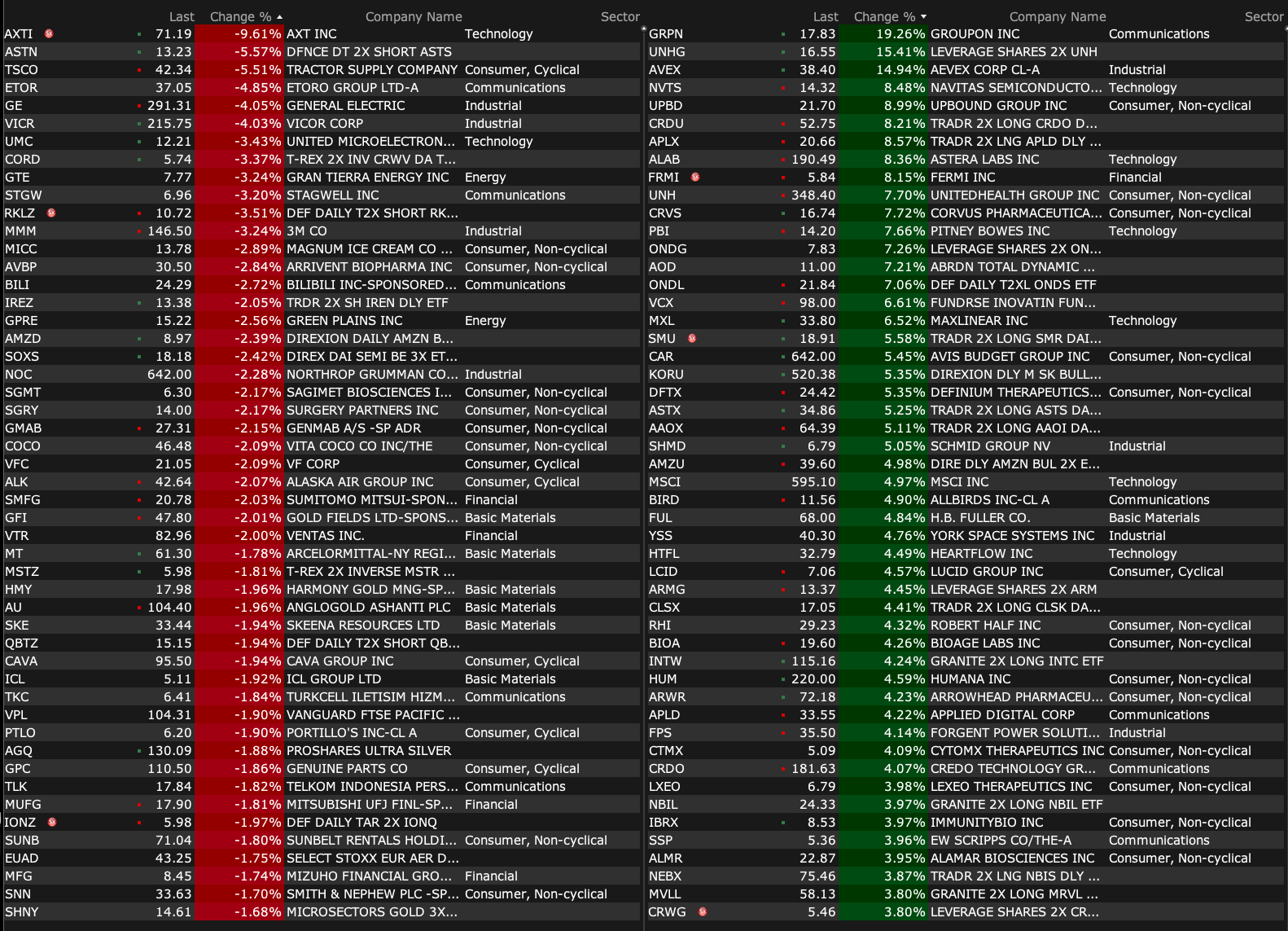

Tuesday's After-Hours Advancers and Decliners

After-Hours % Advancers

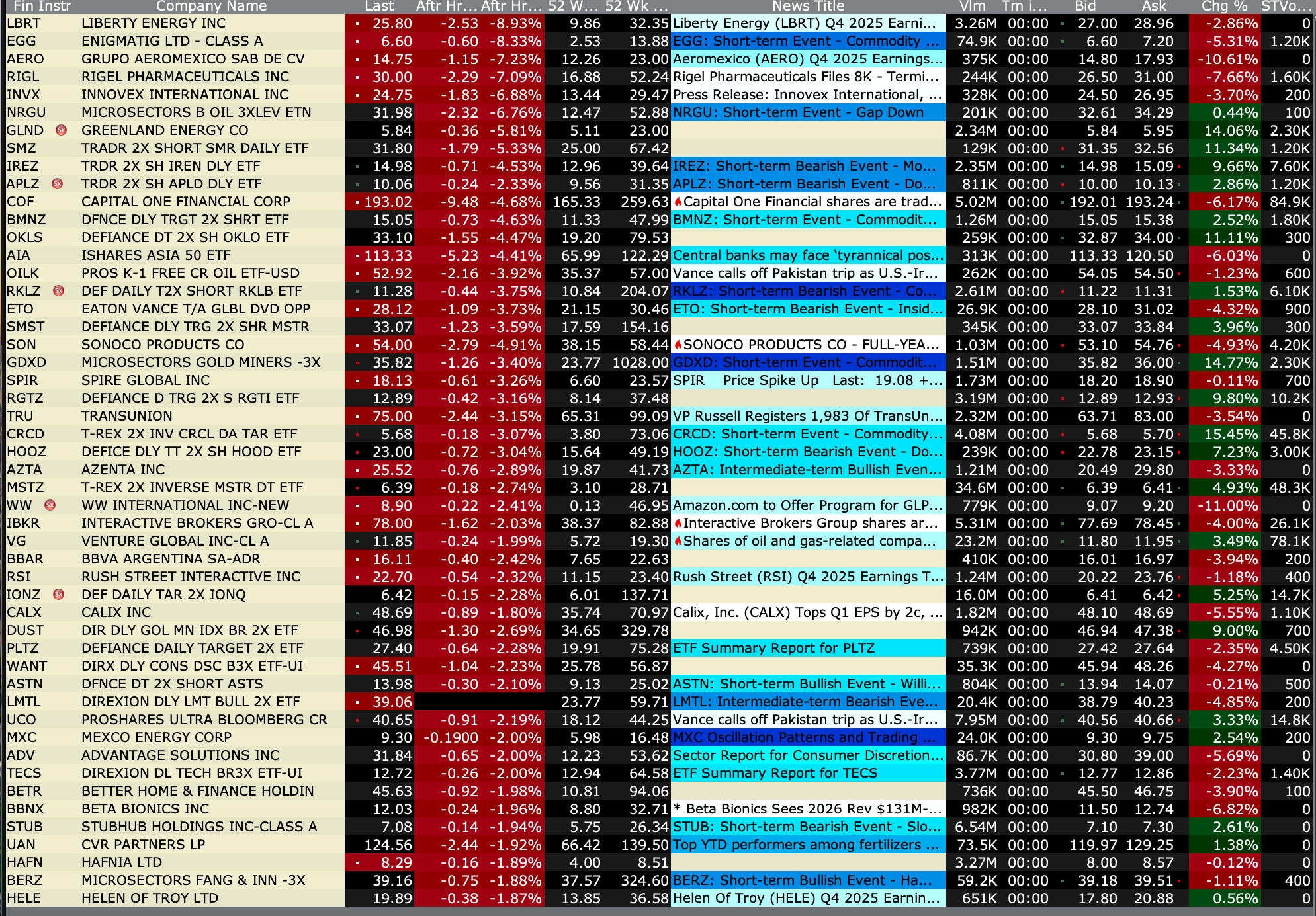

After-Hours % Decliners

BY Doug Kass · Apr 21, 2026, 4:50 PM EDT

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Apr 21, 2026, 4:50 PM EDT

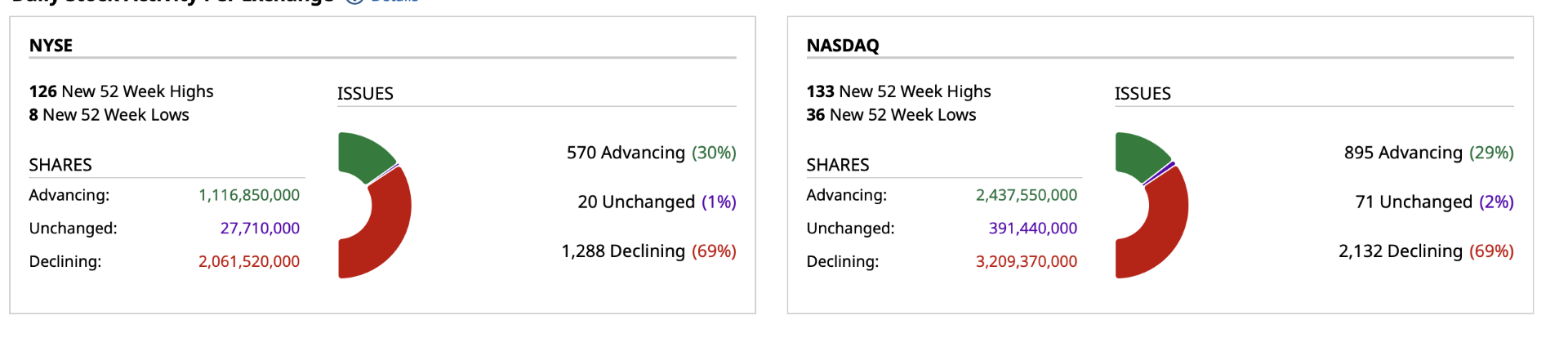

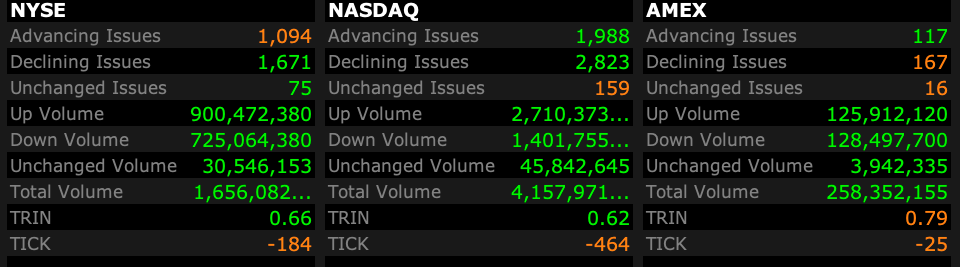

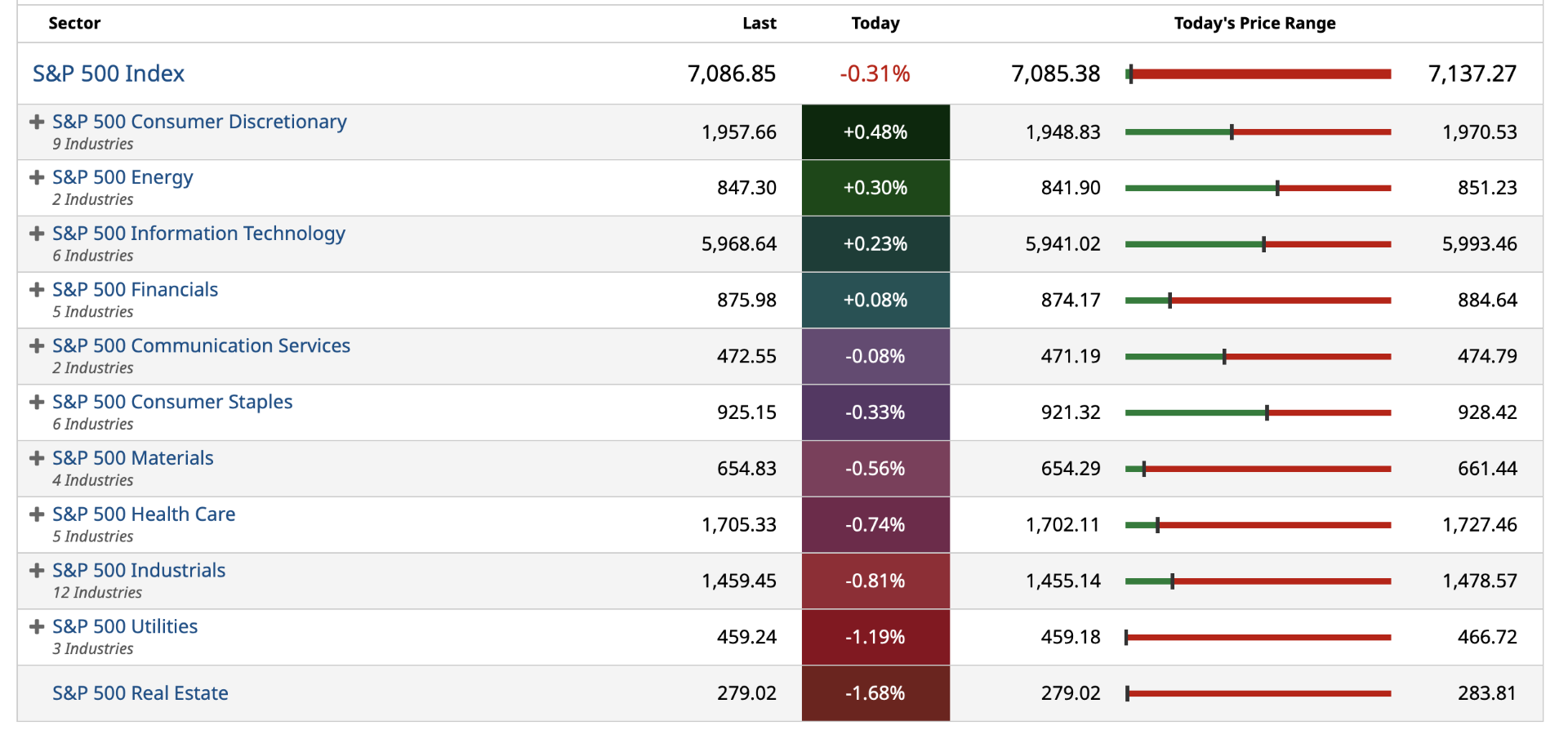

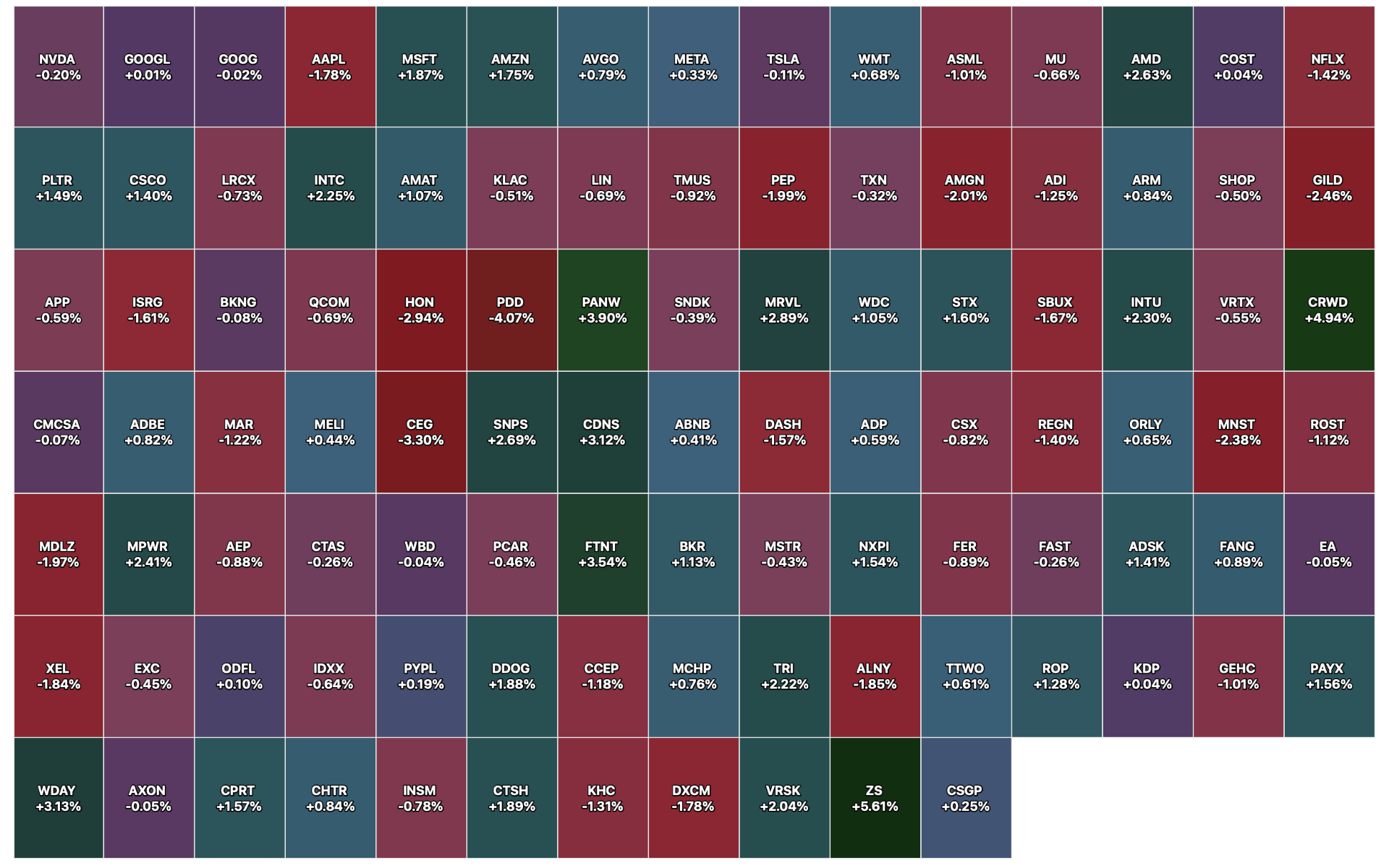

Closing Breadth

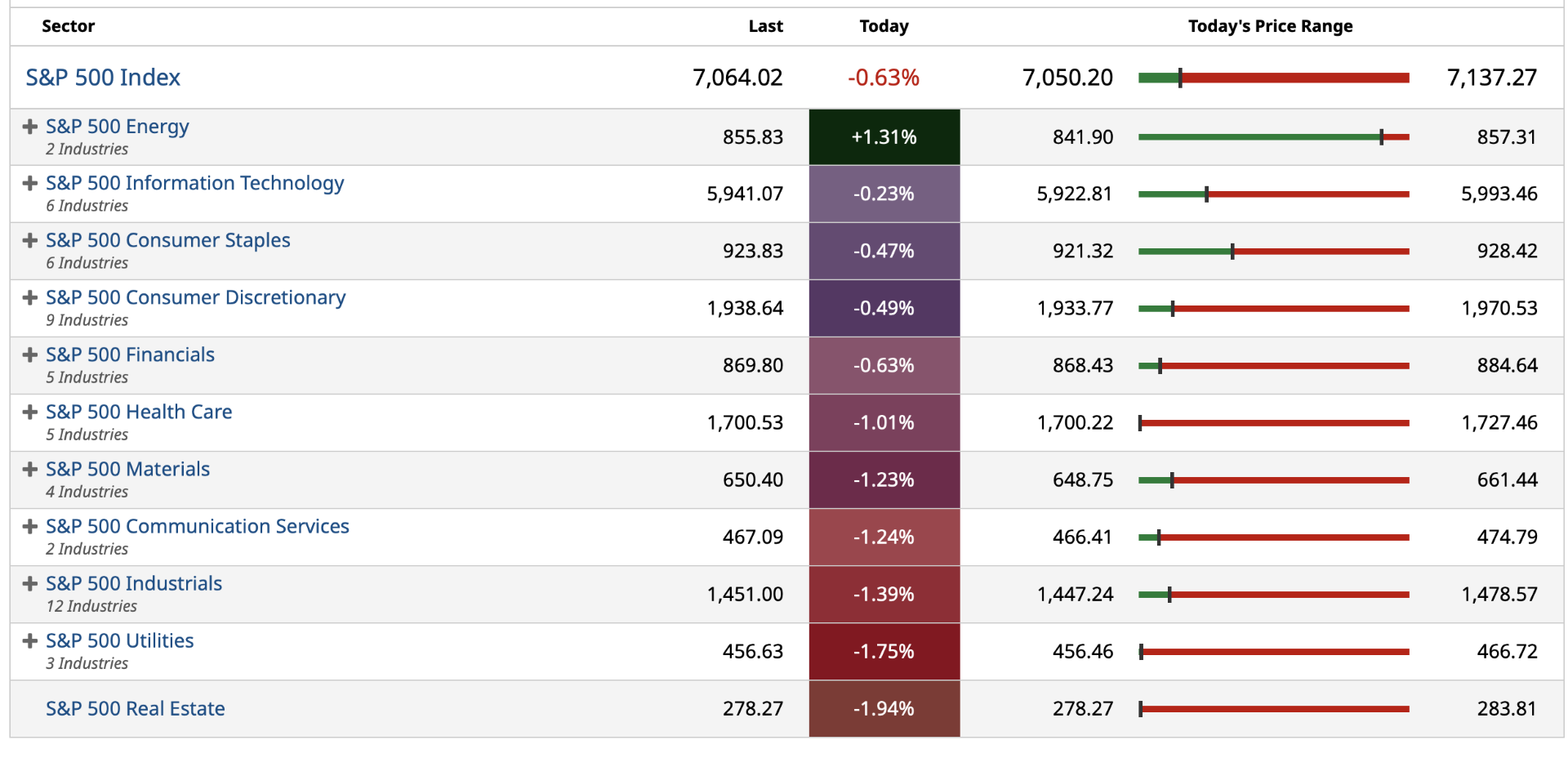

S&P 500 Sectors

% Movers

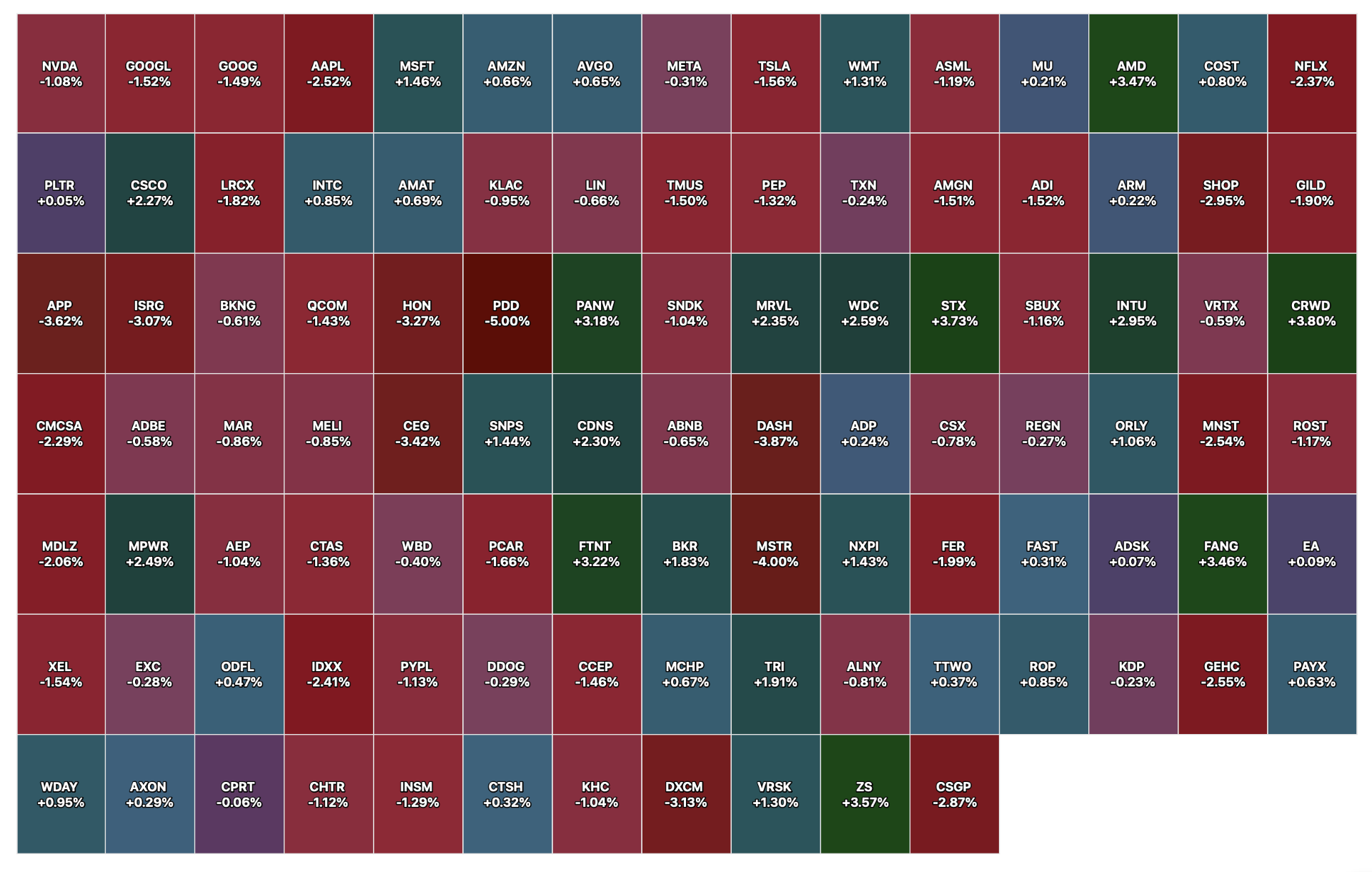

Nasdaq 100 Heat Map

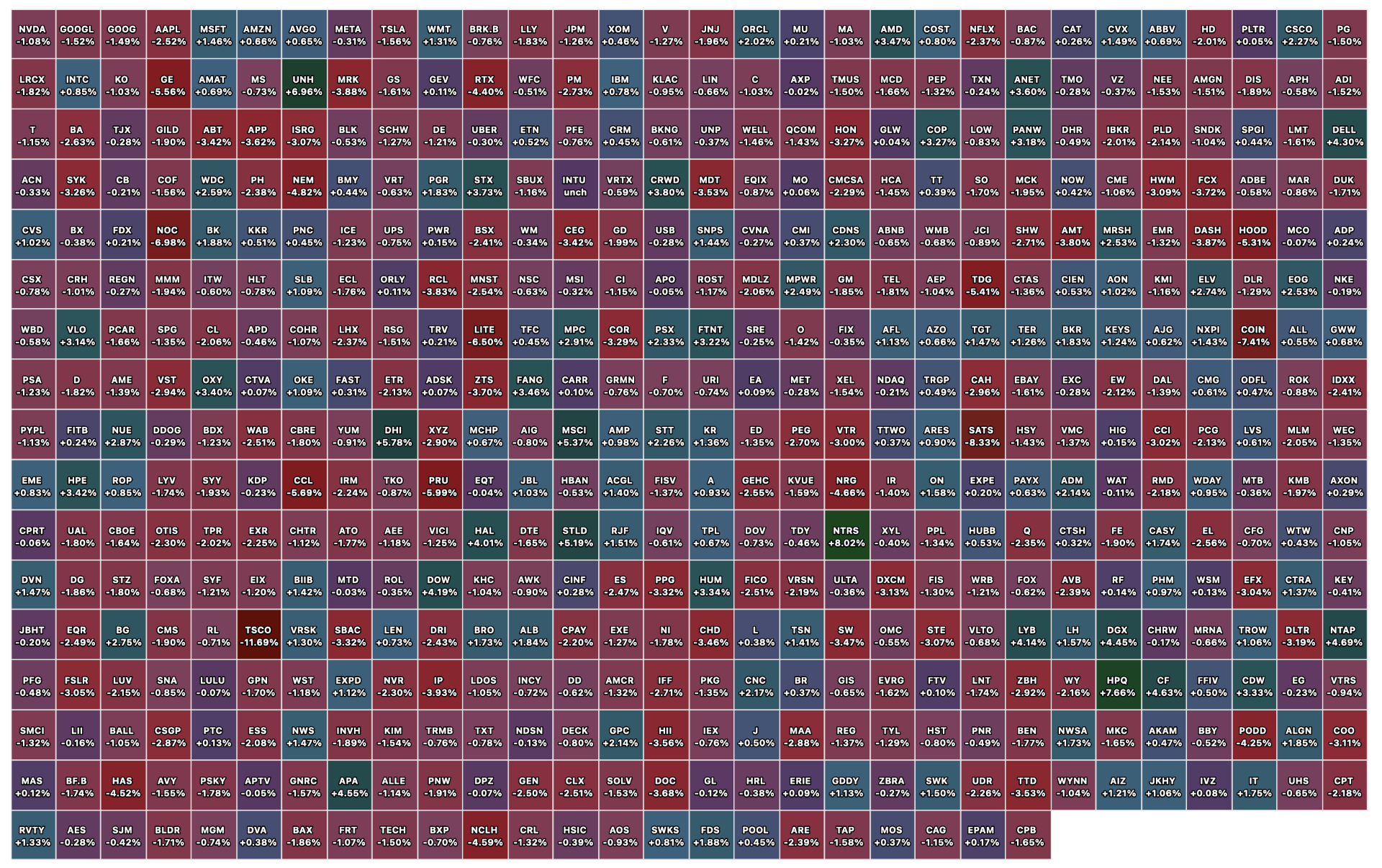

Closing S&P 500 Heat Map

BY Doug Kass · Apr 21, 2026, 4:37 PM EDT

BREAKING: Vice President JD Vance has called off his trip to Pakistan, per AP.

— The Kobeissi Letter (@KobeissiLetter)

Oil prices are surging and stocks are falling on the news.

BY Doug Kass · Apr 21, 2026, 3:59 PM EDT

I have oral surgery tomorrow morning at 7:30 AM.

I will be back in the office before the open.

BY Doug Kass · Apr 21, 2026, 3:36 PM EDT

I'm adding to index shorts:

* (SPY) $707.14

* (QQQ) $647.28

Position: Short SPY common (S), QQQ common (S)

BY Doug Kass · Apr 21, 2026, 3:17 PM EDT

Here are today's things:

* I added to (GRNY) short at $26.17.

* I shorted the indices:

(SPY) $710.32

(QQQ) $647.50

Position: Short GRNY (M), SPY common (S), QQQ common (S)

BY Doug Kass · Apr 21, 2026, 3:12 PM EDT

Wolf Street howls about the deepfreeze in pending home sales.

BY Doug Kass · Apr 21, 2026, 1:30 PM EDT

I added to my (GRNY) short at $26.17.

Position: Short GRNY (M)

BY Doug Kass · Apr 21, 2026, 1:20 PM EDT

My only trades were the short on the indices earlier in the day.

Position: Short SPY common (S), QQQ common (S)

BY Doug Kass · Apr 21, 2026, 1:00 PM EDT

Breadth

S&P 500 Sectors

% Movers

Nasdaq 100 Heat Map

BY Doug Kass · Apr 21, 2026, 11:50 AM EDT

From Peter Boockvar:

Pending home sales in March rose 1.5%, above the estimate of up .5% and follows a 2.5% gain in February (revised up from 1.8%). The contributions to the gains were seen in the Northeast and South, offsetting declines in the Midwest and West. Price cuts in the South seemed to help that region, as seen below.

Context for the data, in March the average 30 yr mortgage rate was 6.26% according to Bankrate vs 6.20% in February and vs 6.39% as of yesterday. What a ride though that the month saw as the rate was at 6.12% at the beginning of March and ended the month at 6.48%. This too might have gotten people off the fence from a rate perspective.

The NAR said “Contract signings rose in March despite higher mortgage rates, pointing to pent-up demand. A greater supply of inventory will help translate that demand into more home sales.”

And, “Demand sensitivity to mortgage rates is greatest among first-time buyers, particularly younger buyers. As a result, boosting supply and new home construction should focus on smaller, more affordable homes.”

Helping the South in particular, as mentioned above, “A good number of markets in the South experienced price cuts over the past year, but recorded the strongest job growth. That combination should lead to stronger housing market activity in the South this year.”

Bottom line, I still believe we need lower home prices to enhance the affordability situation for first time buyers as lower mortgage rates is just not enough and can do the exact opposite without a coincident increase in supply.

For further perspective, the lift in sales over the past two months is off the lowest level since at least 2001 in this index.

Positions: None.

BY Doug Kass · Apr 21, 2026, 11:20 AM EDT

I have an early business lunch at 11:45 a.m. and an eye doctor appointment at 1:45 p.m.

Positions: None.

BY Doug Kass · Apr 21, 2026, 10:49 AM EDT

Chart from 10:12 a.m. ET

Positions: None.

BY Doug Kass · Apr 21, 2026, 10:37 AM EDT

With S&P cash +17 handles I am adding to index shorts:

* (SPY) $710.32

* (QQQ) $647.50

Positions: Short SPY common S QQQ common S

BY Doug Kass · Apr 21, 2026, 9:53 AM EDT

From Peter Boockvar:

Core retail sales in March were better than expected with a .7% m/o/m gain, well better than the forecast of up .2% and February was revised up by one tenth to an increase of .6%. Keep in mind, these are nominal figures.

Above the core line saw gasoline station sales up 15.5%, with obviously price the main reason. Auto sales grew by .5% m/o/m, though down 2.3% y/o/y. Building materials continue to recover, up by .7% m/o/m and 5.3% y/o/y.

Sales bounced with furniture by 2.2% m/o/m, though little changed y/o/y. Electronic products saw a sales gain of .9% m/o/m and 6.1% y/o/y. Also boosting sales in the month was the 1% m/o/m rise at online retailers. Gains were too seen at supermarkets and also in health/personal care. General merchandise sales were up by 1% m/o/m. Sales were flat with clothing, after a strong 2.8% lift in February, and with sporting goods, and at restaurants/bars too.

Bottom line, notwithstanding the spike in gasoline prices, retail sales in the aggregate were good, again understanding that pricing is a factor too. The question of course is sustainability with higher gasoline prices and as the higher price of all fuels more broadly works its way into the economy in the months to come.

Positions: None.

BY Doug Kass · Apr 21, 2026, 9:29 AM EDT

-BYND +22% (momentum)

-GRPN +21% (momentum)

-PLYX +9.0% (US FDA fast track designations for all four indications to be evaluated in SOTERIA trial)

-BULL +8.8% (authorizes $100M share buyback over 12 months)

-ALAB +8.3% (strength in AMZN suppliers following Amazon investment in Anthropic)

-PBI +7.9% (earnings, guidance)

-UNH +7.7% (earnings, guidance)

-CAR +5.1% (suspected meaningful short squeeze)

-HUM +5.0% (higher in sympathy with UNH)

-CRDO +4.7% (strength in AMZN suppliers following Amazon investment in Anthropic)

-LCID +4.7% (Uber disclosed 11.5% passive stake)

-VMI +4.6% (earnings, guidance)

-ELV +4.3% (higher in sympathy with UNH)

-DHI +3.6% (earnings, guidance)

-DGX +3.5% (earnings, guidance)

-CVS +2.9% (higher in sympathy with UNH)

-AMZN +2.5% (to invest $5B in Anthropic and another $20B over time, secure up to 5 GW of capacity for training and deploying Claude)

-EFX +2.4% (earnings, guidance)

-MRVL +2.2% (strength in AMZN suppliers following Amazon investment in Anthropic)

-INTC +2.0% (HSBC Raised INTC to Buy from Hold, price target: $95)

-SPRB -21% (prices 1.15M shares at $50.00/share)

-AXTI -9.9% (files to sell 8.56M shares at $64.25/shr in $550M underwritten public offering)

-VICR -5.7% (earnings)

-TSCO -5.2% (earnings, guidance)

-CRML -3.7% (places 6.0M shares at $10.00/shr in $60M private placement)

-MMM -3.1% (earnings, guidance)

-ALK -2.4% (earnings, guidance)

Positions: None.

BY Doug Kass · Apr 21, 2026, 9:13 AM EDT

From Peter Boockvar:

We await the President’s appearance on CNBC this morning at 8:30am est. Is he bringing good news that a deal is about to be struck and/or will it be just a preview of the talks on Wednesday? I’m still optimistic a deal is about to be had as the economic pain points and growing shortages are on the cusp of becoming acute. And, I believe the Chinese are taking a larger role behind the scenes to help make this happen.

Kevin Warsh will be the other focus and I’m optimistic he’ll be a good Fed Chair. Of course there will be a big focus today on Fed independence and its ability to conduct policy without interference. Odds for a rate cut by December currently stands at 44%.

Nothing better I believe than hearing directly from companies on the state of things and here were some notable comments from the earnings releases/calls:

From Cleveland Cliffs and the colorful CEO Lourenco Goncalves:

“While Q1 results could be better and they would be better, if not for a couple of one-timers, we can see the clear signs of a positive trend for me. Among these one-timers, the impact of the spiking of energy costs was the most relevant to Q1 results. Now to the good news. Our order book is full, and the automotive OEMs are booking more and more steel from Cliffs. Production schedules are tight, and lead times have moved out. Historically, pricing changes took about a month to flow through our realized numbers Today, that lag is closer to two months.”

“In practical terms, that means the pricing strength visible in the market today will increasingly show up in results as we move through the year quarter by quarter.”

“This market strength is driven by what is happening on the trade front. The steel imports into the United States are at their lowest levels since 2009. By now, it’s clear that Section 232 works. The melted and poured mandate works, and the enforcement works. Along those lines, we are very encouraged by the recent changes in how derivative product tariffs are being enforced. Distribution transformers were added, which is exactly the right outcome.”

“Imported steel is now not only subject to tariffs. It is structurally more expensive due to transportation costs, energy volatility, and geopolitical risk. And while this global uncertainty is exposing weaknesses elsewhere, it is strenghtening the position of domestic steel producers like Cleveland Cliffs.”

He’s also optimistic that steel will take market share from aluminum to the automotive end market. I’ll add, what is good for steel companies in terms of pricing is a higher cost for those who use it and that is the balance when it comes to figuring out the net result and impact from tariffs.

From the Alaska Air earnings release:

“Air Group began the year with solid operating momentum, though first quarter 2026 results were impacted by sharply higher fuel prices and localized demand disruptions as a result of historic rainstorms in Hawaii and civil unrest in Puerto Vallarta ahead of the peak spring break travel season. These markets represent appoximately 30% of Air Group capacity.”

“Premium demand continued to outperform as fleet retrofits and Starlink installations progressed.”

“For full year 2026, our visibility to earnings is limited due primarily to ongoing fuel price volatility. Until conditions stabilize and we have better sight to earnings beyond the current quarter, we have suspended full-year guidance.”

From Zion Bancorp:

To a question about the loan outlook, “the pipeline is looking healthy, actually, at this point. We’re seeing lots of activity in small business, middle market, corporate banking syndications, just general C&I. We’re just seeing lots of activity. Another thing that’s coming back is we’re seeing increased CRE activity. We’re cautious there, but we are seeing increased activity as some of the markets have reached more stabilization. So, I think we’ll continue to see growth coming from those areas.”

On private credit, “I think investors increasingly really need to peel back the onion on the type of loan growth that banks are producing. The NDFI kind of issue that has sprung up has just, I mean, there are massive differences in banks’ reliance on NDFI growth. It should be a good asset class for many, many reasons. Managed responsibly, as you know for us, as we report, it’s about $2 billion of our portfolio outstanding and has not grown in five years. And you can see that our peers and banks, smaller and larger, pretty much gulping down these loans, just as there has been a difference in CRE growth.”

“And so I think what investors, if they’ll really peel back the onion, will find that if they’re worried about NDFI, if they’re worried about rapid CRE growth, if they’re worried about personal unsecured lending, that’s not us. So, I again think it just requires a little more investigation of the topic.”

And on the C&I pricing environment, “”it certainly is a competitive market out there today. So, we’re seeing some price competition. But it’s not significant, but it’s something that we’re definitely very aware of.”

From the DR Horton earnings release:

“Affordability constraints and cautious consumer sentiment continue to impact new home demand; however, our tenured operators executed with discipline, driving an 11% y/o/y increase in net sales orders, while reducing unsold completed homes by 35% from a year ago. We expect our sales incentives to remain elevated in fiscal 2025, with incentive levels dependent on demand, mortgage interest rates and other market conditions.”

To some overseas data of significance. The April German ZEW investor confidence index on their economy fell to -17.2 from -.5 and vs the estimate of -5.8. The Current Situation deteriorated too, declining to -73.7 from -62.9. ZEW said “The economic consequences of the Iran war for the German economy go far beyond price increases: Businesses are concerned about long-term shortages of energy supply, and this discourages investment and weakens the effect of government stimuli.”

Nothing market moving with the ZEW though.

In the UK, 11k jobs were lost in March and February was revised down to a fall of 6k vs the estimate of a rise of 20k. Jobless claims rose by 26.8k in March after an increase of 17.1k in February. Thru the 3 months ended February, the unemployment rate fell to 4.9% from 5.2% but was mostly due in part to a big fall in the size of the labor force looking for work. The wage gains were 3.6% y/o/y thru February vs 3.8% in January. There is obviously a mix here of March and February data, pre war, post war and only the latter matters now and the jobs picture weakened in the UK.

Both the euro and pound are lower vs the US dollar, though bond yields are little changed in response. Stocks are bouncing with the dip in crude oil prices with hopes of an imminent end to the war and reopening of the Strait.

In Japan, ahead of next week’s BoJ meeting, Bloomberg News is reporting that “The BoJ is leaning toward keeping its policy rate unchanged next week given uncertainties stemming from the war in Iran, with officials still committed to raising borrowing costs sooner or later, according to people familliar with the matter. Officials see little need to rush to hike the benchmark interest rate when the economic outlook can still shift considerably because of the highly fluid situation in the Middle East, the people said.”

Bottom line, the BoJ dragging their feet for years in raising rates has left them so unprepared for the current macro. Rates are too low relative to inflation and they are too low to matter if they need to cut in response to an economic downturn. The yen is lower just below 160 but JGB yields are little changed while the Nikkei continued its big run year to date, higher by 18%.

Positions: None.

BY Doug Kass · Apr 21, 2026, 8:59 AM EDT

Positions: None.

BY Doug Kass · Apr 21, 2026, 8:51 AM EDT

11:00 a.m.: Treasury Announces a 4, 8 and 17 Week Bill Auction;

11:00 a.m.: Treasury buyback announcement (cash mgmt);

11:00 a.m.: Treasury hosts a $70B 6-Week Bill Auction

2:30 p.m.: Fed Board Governor Waller (Voter) speaks on "Modernizing Reserve Bank Operations" before the Brookings Institution, Washington, DC (Text available. Q&A from moderator and audience. Webcast at www.brookings.edu/events)

Positions: None.

BY Doug Kass · Apr 21, 2026, 8:39 AM EDT

Positions: None.

BY Doug Kass · Apr 21, 2026, 8:25 AM EDT

From JPMorgan:

US: Futs are higher. Pre-market, Mag 7 are mixed: (AMZN) +2.8%, (META) +0.6%, (AAPL) -0.4%. Apple announced its new CEO after yesterday’s close (John Ternus will become the CEO effective September 1st); AMZN announced it will invest another $25bn in Anthropic with Anthropic committing to spending more than $100bn over the next 10yr on AWS. 2Y yield added 1.7%, while 30Y -41bp. Commodities are mostly lower: Oil -1.8%, Copper -0.5%, Silver -1.0% this morning.

and...

Yesterday, while SPX finished in the red at the index level, underlying price action was better: 53%, or 6 out of 11 sectors, actually finished in the red. The selloff was more notable in the Mag 7 group: META -2.6%, (TSLA) -1.7%, (GOOG) /L -1.3%. Considering the weekend escalation and a 5.8% jump in oil prices, stocks showed resilience against macro headline volatility. We see macro growth and fundamentals continuing to support equities this earnings season, but the upcoming ceasefire deadline remains a key risk (Trump signaled that another extension of the deadline is unlikely today).

Overall, outside the weekend headlines, macro and earnings news were relatively quiet yesterday and overnight. Today, we will receive Retail Sales at 8:30am ET. See Feroli’s preview below.

· RETAIL SALES PREVIEW (FEROLI) – Rising gasoline prices should have caused a sizable increase in March retail sales, which we forecast rose 1.6%. But we also expect that non-gas sales were also quite strong. Unit auto sales rose 3.7% m/m, supported by a 4.3% m/m uptick in incentive spending by automakers coupled with continued normalization in temperatures, as noted by our auto equities team. They mention that demand for automobiles has not reflected a hit from the Middle East conflict, although there are some downside risks to the category from rising pass-through of tariff costs. We also look for a 13% m/m spike in sales at gasoline stations, as retail gasoline prices rose 25% m/m amid the surge in global energy prices arising from the Middle East conflict.

o Even outside of autos and gasoline, we look for a firm 0.6% m/m uptick in sales. That includes a solid 1.0% m/m increase in food services, as informed by our Chase card data 1. We look for slower growth in building material store sales, as earlier growth was possibly buoyed by demand for snow clearing and heating equipment amid unusually cold weather.

o The control group (excluding food services, autos, gas, and building material stores) is expected to rise 0.5% m/m, with that forecast based on our Chase card data. We recently discussed the implications for the boost from OBBBA tax cuts amid rising energy prices, noting that total benefits could be concentrated in lower April payments, which should keep consumer spending on a strong trajectory in the coming months. The Chicago Fed CARTS indicator, which incorporates high-frequency data on retail transactions, foot traffic, gasoline sales, and consumer sentiment, points to a 1.3% m/m rise in retail and food services sales ex. autos for March.

DUBRAVKO RAISES SPX PT FROM 7,200 to 7,600 – his full note is here

· Markets broke out to new highs last week, led by geopolitical de-escalation and strong momentum in the AI theme, with Mag-7 and AI upstream names outperforming in unison — this level of investor interest in AI stocks has not been seen since 1H25. The ~10% market correction was a clearing event for the breakout as Corporates absorbed supply via buybacks during the sell-off with many investors now having to chase (i.e., L/S Funds unwinding hedges, Systematic Strategies increasing equity exposure, Retail ramping up their buying). Other than the geopolitical de-escalation, we believe the Anthropic Mythos headline was the key catalyst, with 66% of S&P 500 AI names outperforming since April 7th — evidence of rapidly improving models and AI services, as Anthropic’s revenue run rate has tripled YTD and the upcoming OpenAI’s Spud release is expected to demonstrate significant improvement as well. Even the risk of AI induced job displacement in some of the most sensitive areas (i.e., software engineering) is being put to rest for now as hiring is resuming.

· Looking ahead, we expect a more favorable 1Q reporting season than last quarter, when investors were AI-fatigued and weary of higher Capex and R&D spending. In our view, S&P 500 consensus earnings growth has some room for further upside, given that recent positive revisions have been largely driven by a handful of Tech companies as well as Energy, see Figure 21. We are revising up our S&P 500 EPS estimates of $315 (2026) and $355 (2027), which were significantly above consensus at the time of initiation, to $330 +22% y/y (vs. consensus of $325) and $385 +17% y/y (vs. consensus of $379) for 2026 and 2027, respectively. Accordingly, we are also revising our 2026 S&P 500 year-end Price Target (PT) to 7,600, implying an unchanged NTM multiple of ~22x from our prior downgraded PT. Given the sharp rally from recent lows (10-day RSI >95th %ile) and a geopolitical backdrop that, while significantly de-escalated, remains in flux, there is a meaningful risk that the market enters a short-term consolidation phase before resuming its upward trajectory. While a full resolution might take time, with oil prices lingering in the ~$90/bbl range, this view assumes that it is unlikely there will be significant new escalation (i.e., with China likely acting as a guardrail).

· Implied multiple unchanged — PT upgrade driven entirely by higher earnings. Our PT downgrade to 7,200 last month was driven by elevated geopolitical risk rather than a deterioration in earnings fundamentals. Thus, we kept our EPS estimateunchanged, which effectively implied a compression in the forward multiple (from 23x to 22x). Our new PT of 7,600 is supported by an upward revision to our EPS forecast (now $330) largely reflecting stronger expectations in Tech / AI, rather than a removal of the geopolitical overhang. As such, our NTM multiple remains at 22x. Should geopolitical tensions move toward a swift resolution ("Blue Sky" scenario), we would expect the multiple to re-expand back toward 23x, which would imply an S&P 500 level of ~8,000.

Disclosures: None.

BY Doug Kass · Apr 21, 2026, 8:10 AM EDT

None.

BY Doug Kass · Apr 21, 2026, 8:02 AM EDT

Warren Buffett said anything above 200% means "you are playing with fire."

— Felix Prehn 🐶 (@felixprehn)

It just hit 232%.

Highest reading in the history of the American stock market.

The metric is called the Buffett Indicator. He called it "probably the best single measure of where valuations stand at any…

BY Doug Kass · Apr 21, 2026, 7:00 AM EDT

Chart of the Day: Micro-Caps

Micro-Caps (IWC) closed at new all-time highs today and new multi-year highs relative to Mega-Caps (MGC).

The ratio has reclaimed a confluence of key levels, including the 200-week moving average and 2020 pivot lows, highlighting the strengthening long-term relative trend.

Leadership from the most speculative segment of the market points to a clear risk-on environment and supportive conditions for equities broadly.

The Takeaway: Outperformance in the riskiest stocks reinforces the bullish expansion of risk appetite.

- (2) Drew Wells, CMT (@DrewTheCharts) / X

The S&P 500 is up 3% for 3 weeks in a row for just the third time since 1950.

— Phil Rosen (@philrosenn)

The last 2 times this happened stocks were up 33% a year later on average.

Hard to bet against this momentum. pic.twitter.com/ZWeXBugiry

The S&P 500 is at an all-time high while Consumer Sentiment is at an all-time low.

— Charlie Bilello (@charliebilello)

We've never seen a gap this wide between Wall Street and Main Street. pic.twitter.com/BPu6ncbG9F

— Nautilus Research (@NautilusCap)

On Friday, 10% of the S&P 500 (49 stocks) made new 52-week highs, while no stocks made 52-week lows. Net new highs have picked up quite a bit, with Tech and Consumer Discretionary driving the move late last week. pic.twitter.com/Q4pqZyjUAg

— Bespoke (@bespokeinvest)

Biotech $XBI continues to be one of the strongest groups in the market.

— Ricardo Sarraf (@nullcharts)

Among the best signals in this space is when earlier-stage companies, the ones still in clinical trials $BBC, outperform those with products already on the market $BBP.

It’s a clean way to gauge the… pic.twitter.com/xMHkjwh8qb

Far Out Man: The Psychedelics ETF $PSIL has destroyed its daily volume record in first 30min of trading.. Trump just signed ex order expediting research/access to psyche drugs to cure depression. The sector has been in dog house, waiting for catalyst, up 10% today. Watch this… pic.twitter.com/Lii1QuUBnV

— Eric Balchunas (@EricBalchunas)

$WEED (same sector as $MSOS)

— Stockspy (@Stockspy1)

nice breakout! pic.twitter.com/e2YcioWwmZ

BY Doug Kass · Apr 21, 2026, 6:45 AM EDT

🇺🇸 Recession

— ISABELNET (@ISABELNET_SA)

The market is pricing in just a 13% chance of a US recession over the next year, while Goldman Sachs sees it closer to 30%. Is the market too complacent?

👉 https://t.co/m11iBkSWhc

h/t @GoldmanSachs $spx #spx #recession #stocks #equity pic.twitter.com/Kc42FZqTvn

BY Doug Kass · Apr 21, 2026, 6:35 AM EDT

Wolf Street howls about falling condo prices nationwide.

BY Doug Kass · Apr 21, 2026, 6:15 AM EDT

Tom Lee with one of the most bullish statements today I have ever seen, well, Tom Lee say…

— Heisenberg (@Mr_Derivatives)

👀👀 pic.twitter.com/Xf1fQO9GXz

BY Doug Kass · Apr 21, 2026, 6:05 AM EDT

The S&P Short Range Oscillator remains deeply overbought at 7.61% vs. 7.89%.

Neither overboughts/oversolds nor sentiment/surveys are good clocks... but they are (especially in the extreme) a good weather forecast ..

— Dougie Kass (@DougKass)

S&P Short Range Oscillator at close stands at 7.61% - very overbought. @SquawkCNBC @andrewrsorkin @BeckyQuick @CNBCFastMoney @HalftimeReport…

Position: Short SPY common (S)

BY Doug Kass · Apr 21, 2026, 5:55 AM EDT

A massive capex boom wherein the sellers recognize revenues and profits while the buyers capitalize the costs, will do that. Look at mid-1998 to mid-2000, when S&P 500 profits rose 30%. Then look at the next twelve months when order books collapsed. https://t.co/dv3R7oqOks pic.twitter.com/BSx1CklqDK

— James Chanos (@RealJimChanos)

BY Doug Kass · Apr 21, 2026, 5:45 AM EDT

Warren Buffett said anything above 200% means "you are playing with fire." It just hit 232%. Highest reading in the history of the American stock market. The metric is called the Buffett Indicator. He called it "probably the best single measure of where valuations stand at any Show more

The S&P 500 is up 3% for 3 weeks in a row for just the third time since 1950. The last 2 times this happened stocks were up 33% a year later on average. Hard to bet against this momentum.

Tom Lee with one of the most bullish statements today I have ever seen, well, Tom Lee say… 👀👀

BREAKING: Vice President JD Vance has called off his trip to Pakistan, per AP. Oil prices are surging and stocks are falling on the news.

The S&P 500 is at an all-time high while Consumer Sentiment is at an all-time low. We've never seen a gap this wide between Wall Street and Main Street.

Neither overboughts/oversolds nor sentiment/surveys are good clocks... but they are (especially in the extreme) a good weather forecast .. S&P Short Range Oscillator at close stands at 7.61% - very overbought. @SquawkCNBC @andrewrsorkin @BeckyQuick @CNBCFastMoney @HalftimeReport Show more

🇺🇸 Recession The market is pricing in just a 13% chance of a US recession over the next year, while Goldman Sachs sees it closer to 30%. Is the market too complacent? 👉 isabelnet.com/?s=recession h/t @GoldmanSachs $spx #spx #recession #stocks #equity

On Friday, 10% of the S&P 500 (49 stocks) made new 52-week highs, while no stocks made 52-week lows. Net new highs have picked up quite a bit, with Tech and Consumer Discretionary driving the move late last week.

Earnings expectations for American stocks are now rising faster than after the 2017 tax cuts. They're rising at a pace you usually only see during recovery from recessions. The profit machine will not stop.