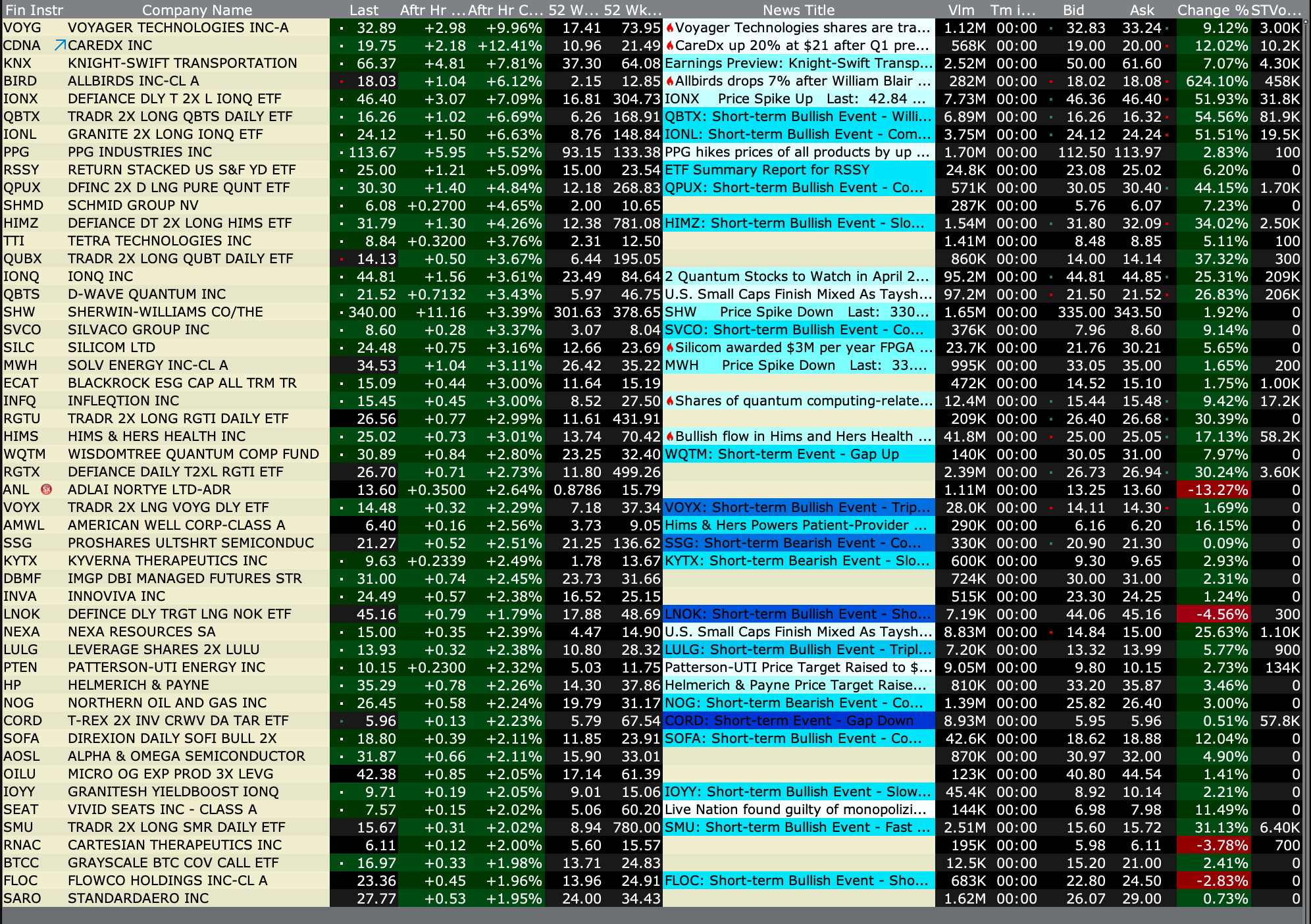

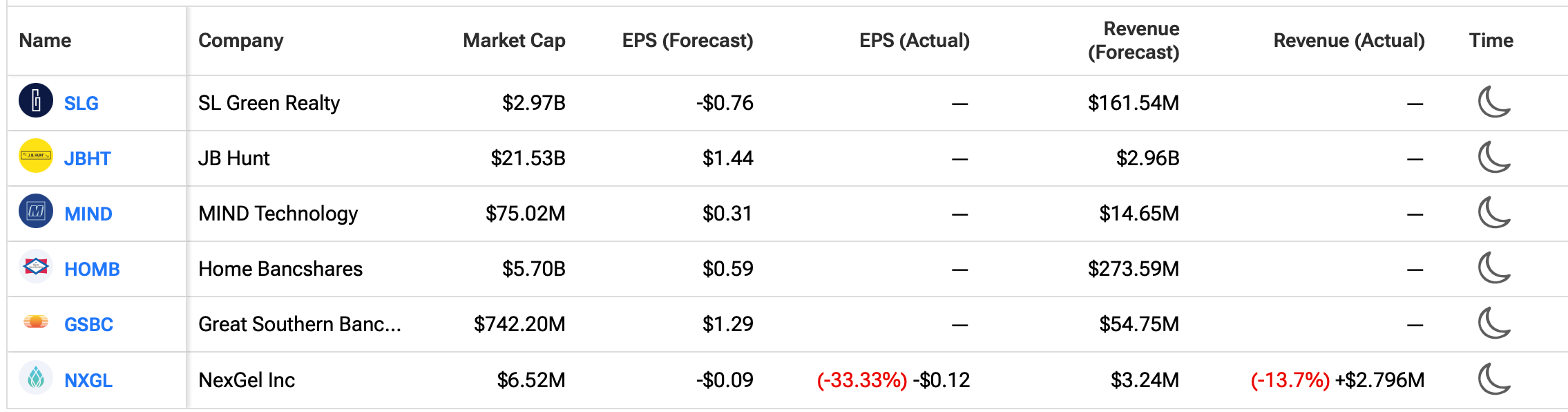

Wednesday's After-Hours Advancers and Decliners

After-Hours % Advancers

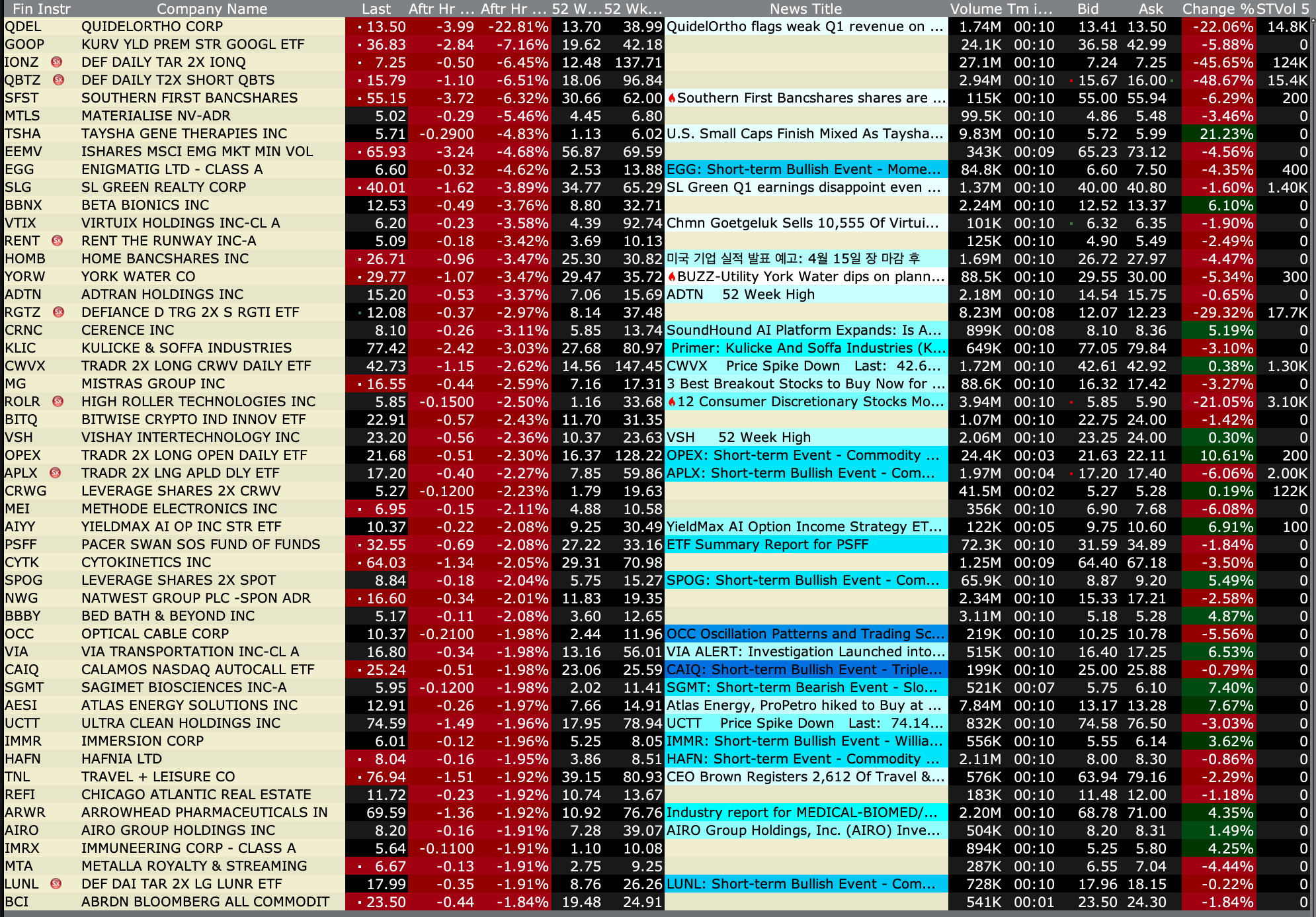

After-Hours % Decliners

BY Doug Kass · Apr 15, 2026, 5:00 PM EDT

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Apr 15, 2026, 5:00 PM EDT

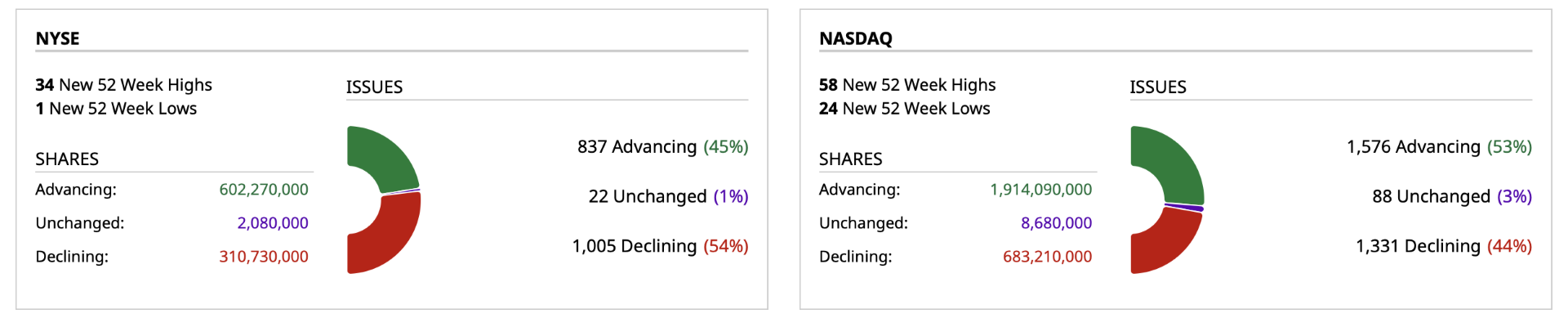

Closing Volume

- NYSE volume 10% below its one-month average

- NASDAQ volume 18% above its one-month average

- VIX index: 18.17 down 0.19%

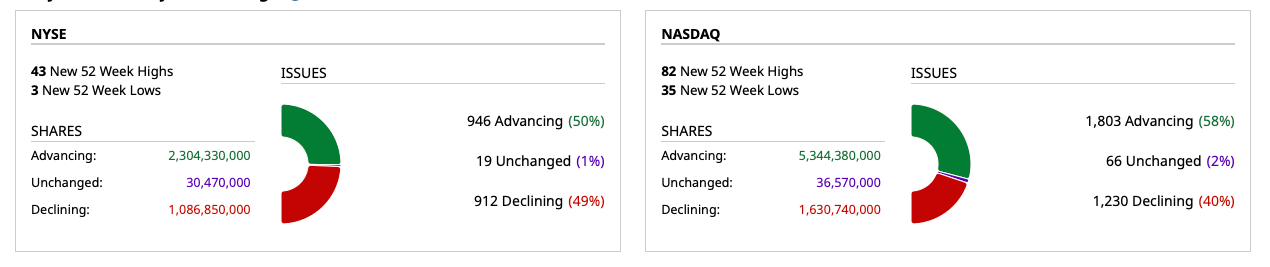

Breadth

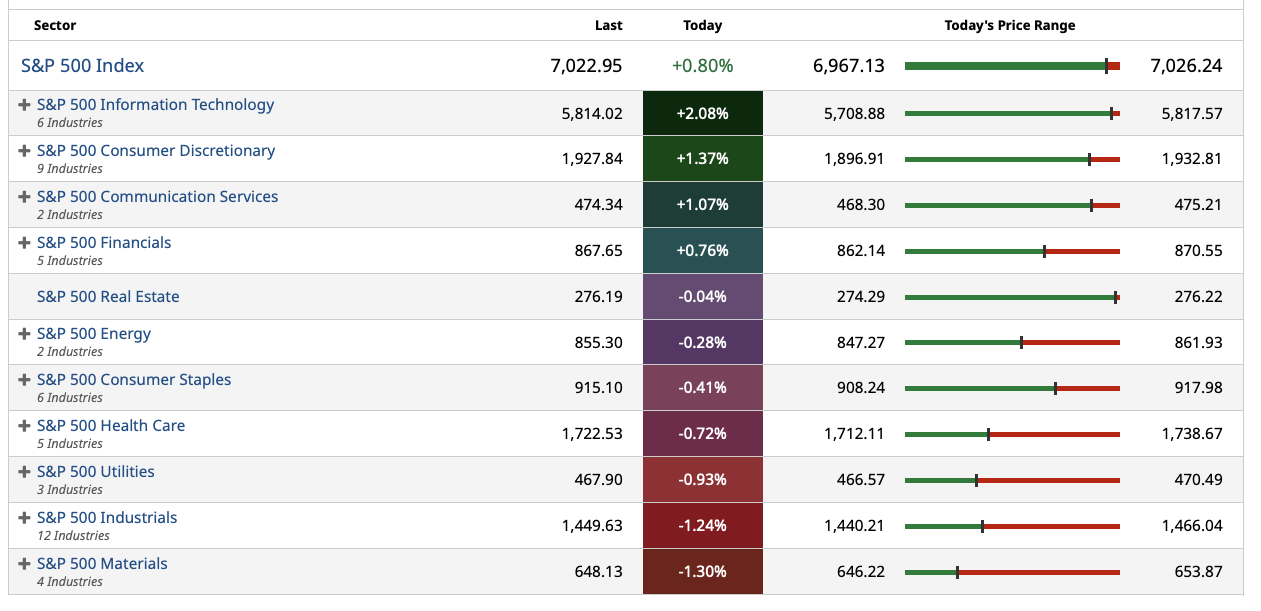

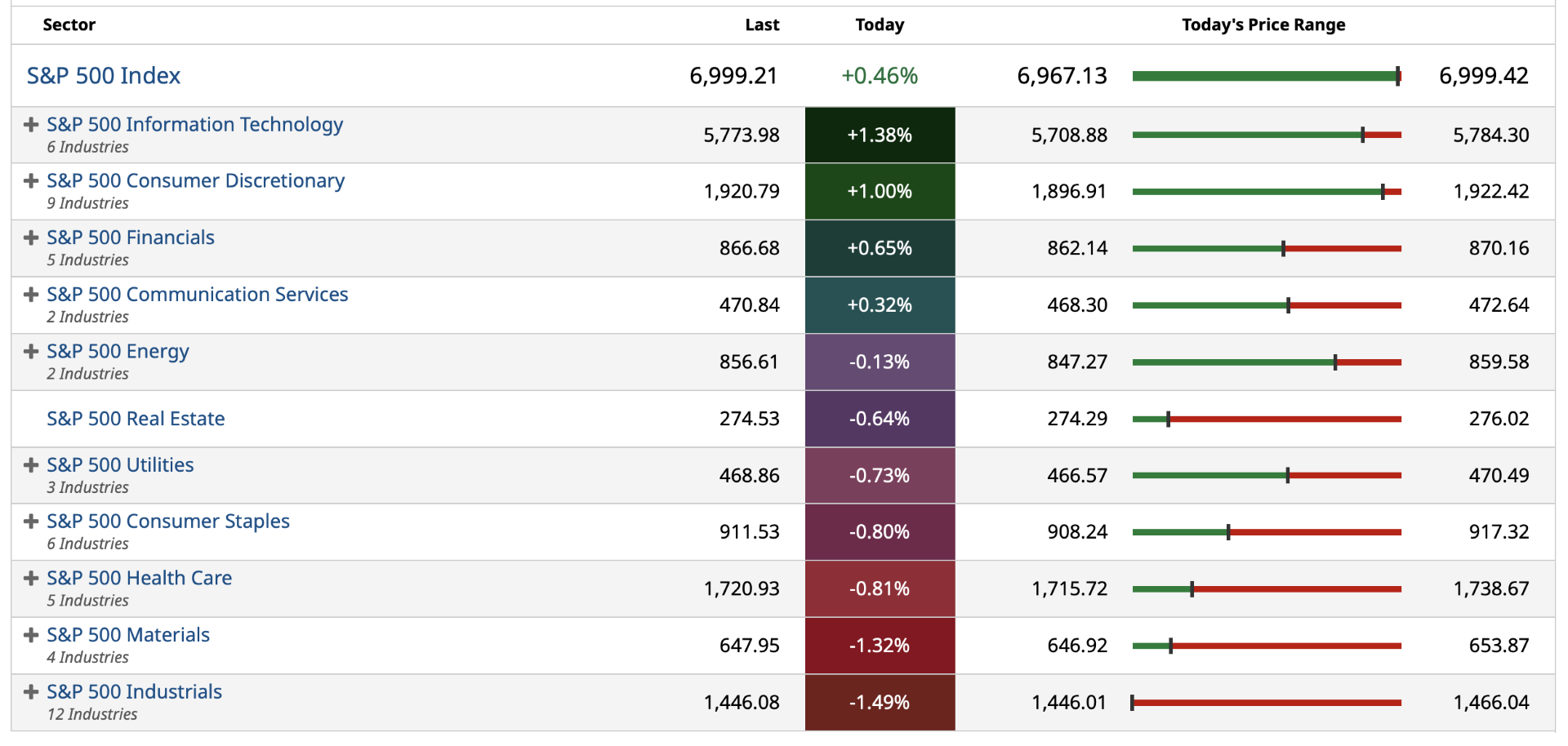

S&P 500 Sectors

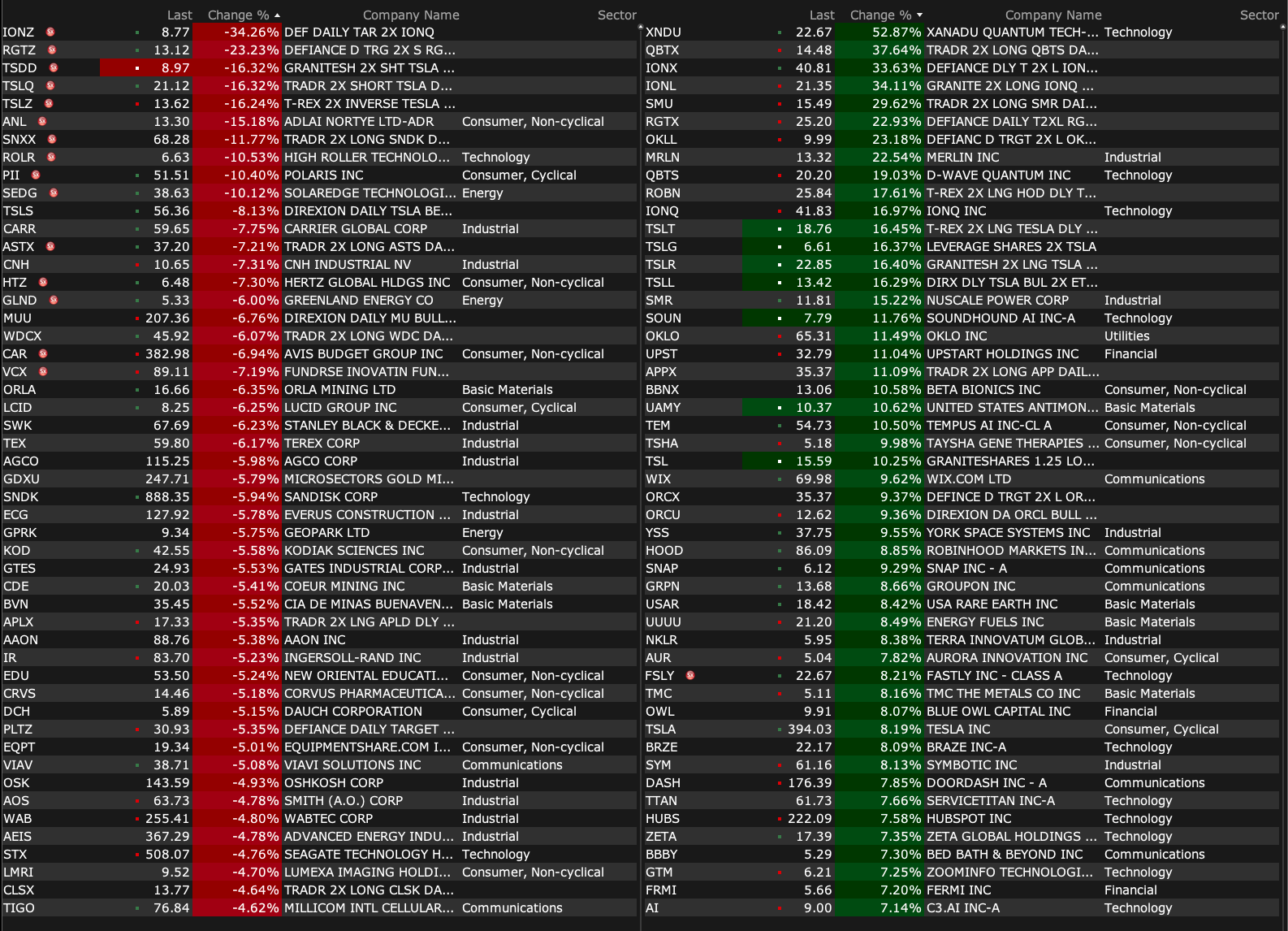

% Movers

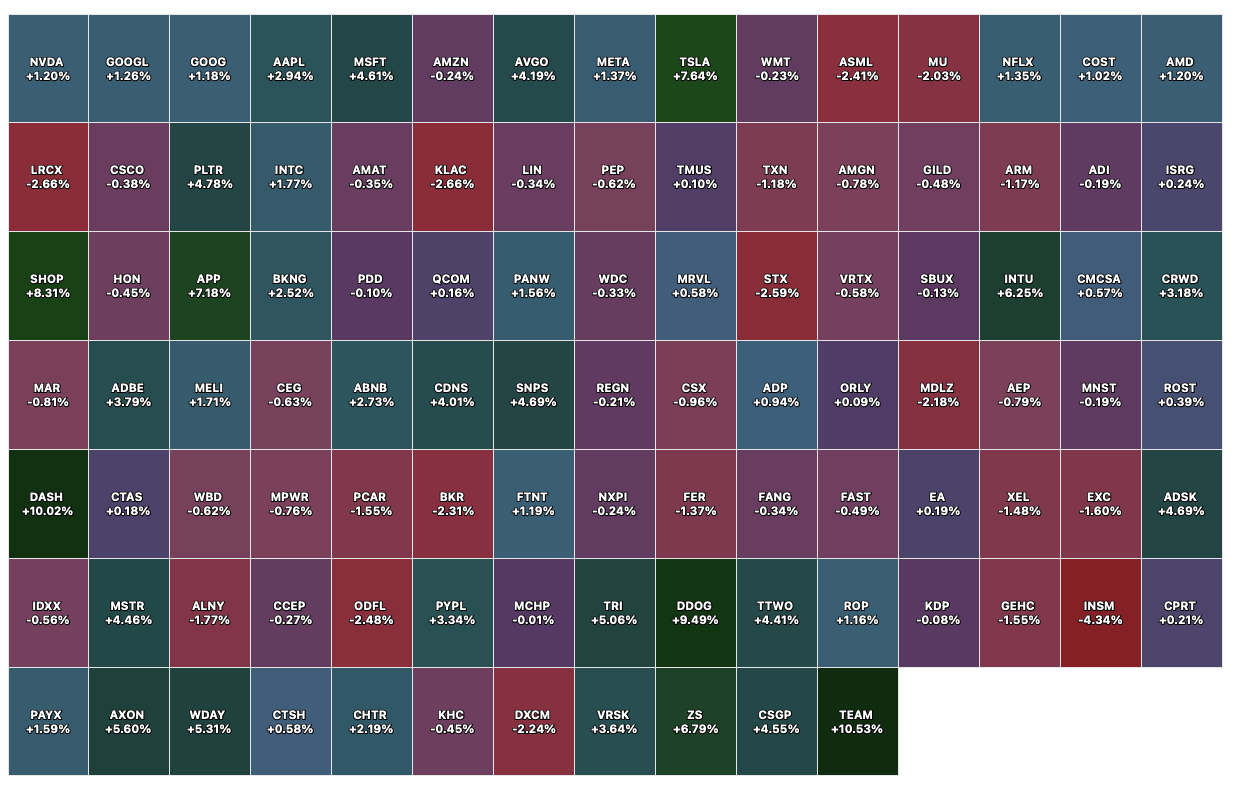

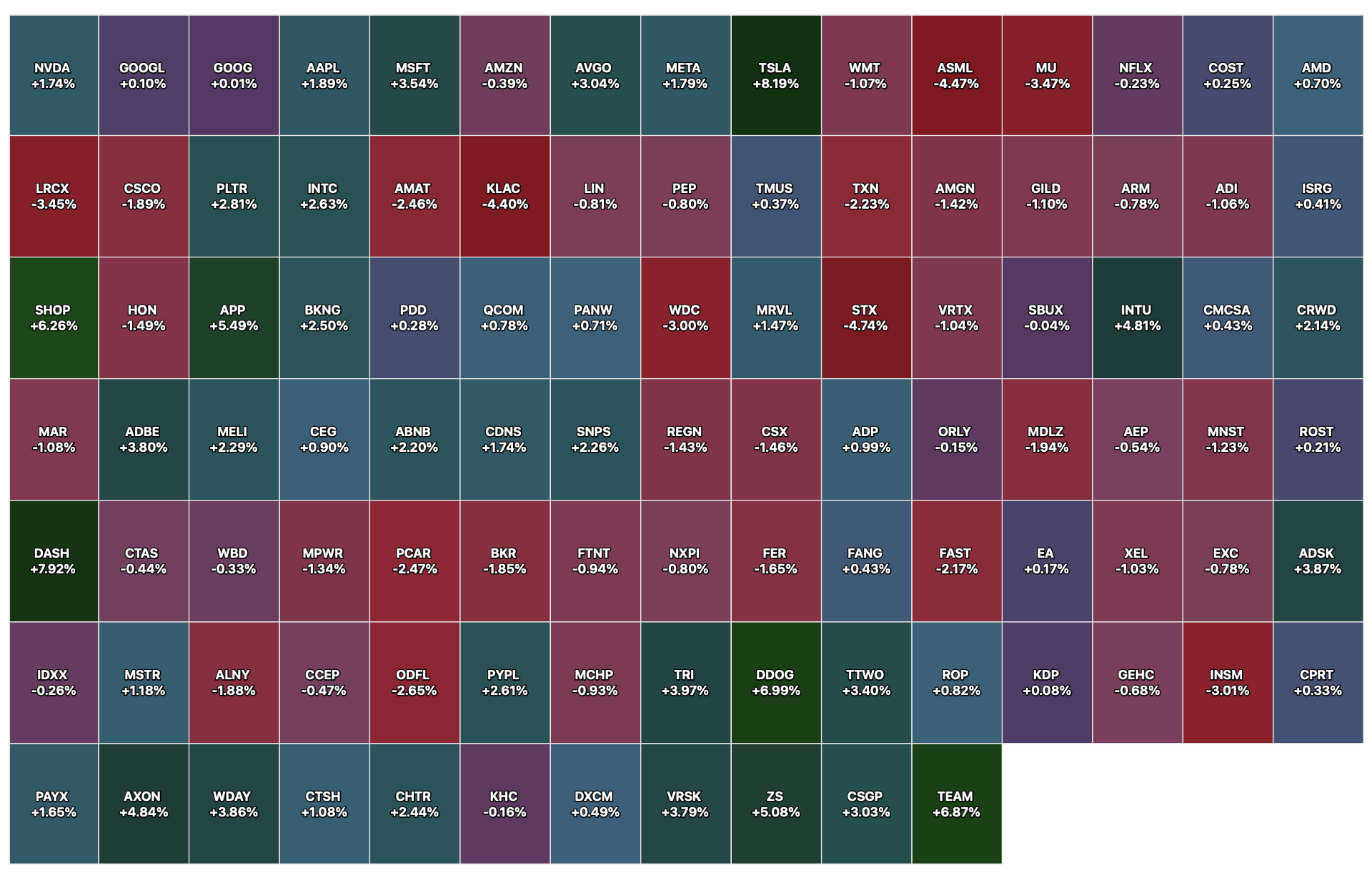

Nasdaq 100 Heat Map

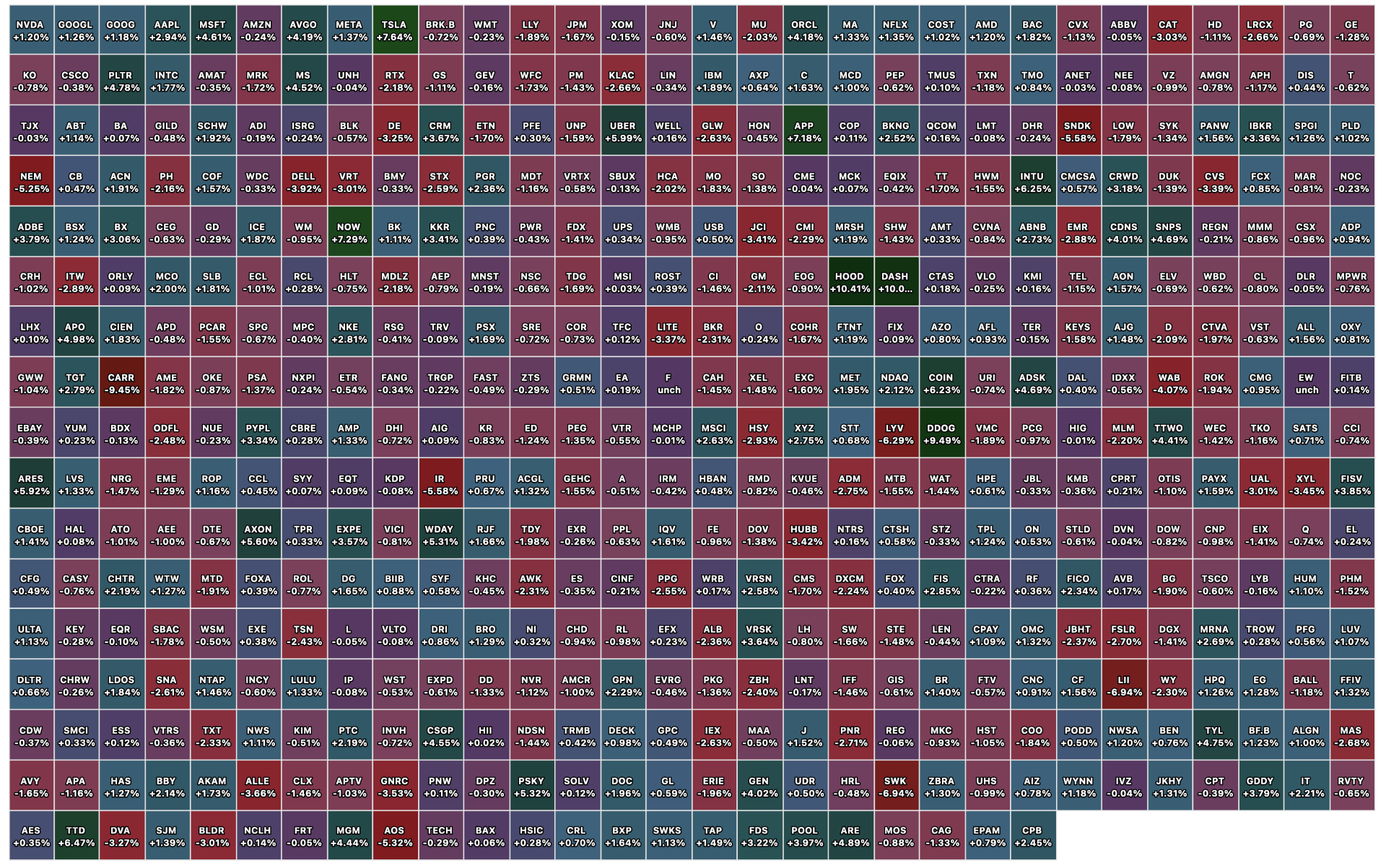

Closing S&P 500 Heat Map

BY Doug Kass · Apr 15, 2026, 4:44 PM EDT

After the Close Wednesday, April 15

Before the Open Thursday, April 16

BY Doug Kass · Apr 15, 2026, 3:25 PM EDT

I wish the Allbirds people luck in their attempt to pivot to GPUs. Maybe they can do it. But i regard this as the first definitive sign that things have gone too far. What a bunch of jokers and mountebanks they are..

— Jim Cramer (@jimcramer)

BY Doug Kass · Apr 15, 2026, 2:30 PM EDT

BY Doug Kass · Apr 15, 2026, 2:20 PM EDT

As mentioned yesterday, I have root canal work being done at 315 PM today.

So I will be signing off early.

BY Doug Kass · Apr 15, 2026, 2:10 PM EDT

I have sold the balance of my tech longs:

* (AMZN) $248.18 (-$0.86)

* (GOOGL) $334.44 (+$1.51)

* (META) $674.18 (+$11.60)

* (MSFT) $408.27 (+$15.15)

Position: None

BY Doug Kass · Apr 15, 2026, 1:25 PM EDT

I previously observed the non participation in the Russell (IWM) and Equal Weight S&P Index (RSP) .

What was flat performance in IWM and RSP is now an outright decline.

Coupled with the mediocre market breadth... we are perhaps seeing some signposts of exhaustion at/near an all-time S&P high.

Position: Short SPY common (S)

BY Doug Kass · Apr 15, 2026, 1:04 PM EDT

Allbirds (BIRD), a busted sneaker company, turns into CoreWeave (CRWV) today.

The company's AI pivot sends the stock +665%.

This takes the cake!

And we have seen this movie before.

Position: None

BY Doug Kass · Apr 15, 2026, 12:40 PM EDT

The last 10-days have been unlike any 10-day period in the market since 1950.

— Warren Pies (@WarrenPies)

First, the S&P 500 is up 9.8% in 10-days, which is in the 99.7th percentile of all 10 day returns. pic.twitter.com/fQLDhjfX1j

BY Doug Kass · Apr 15, 2026, 12:30 PM EDT

Breadth

Sectors

% Movers

Nasdaq 100 Heat Map

BY Doug Kass · Apr 15, 2026, 12:15 PM EDT

Amazingly, (RSP) (equal weighted S&P), and (IWM) are essentially flat today.

Machines and algos (not affected by where stocks have been or how stocks are valued) — geared towards momentum — rule the market landscape.

This is not my father's market.

Position: None

BY Doug Kass · Apr 15, 2026, 11:43 AM EDT

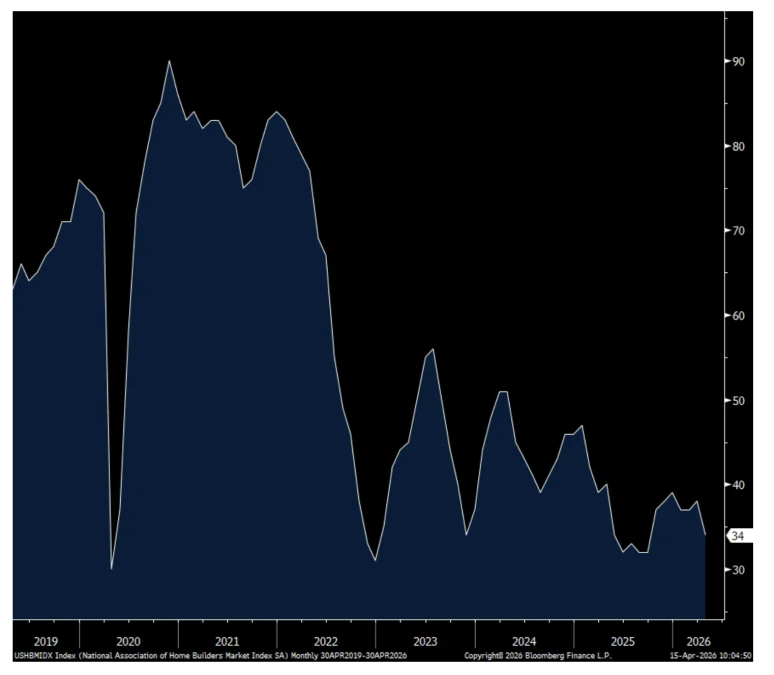

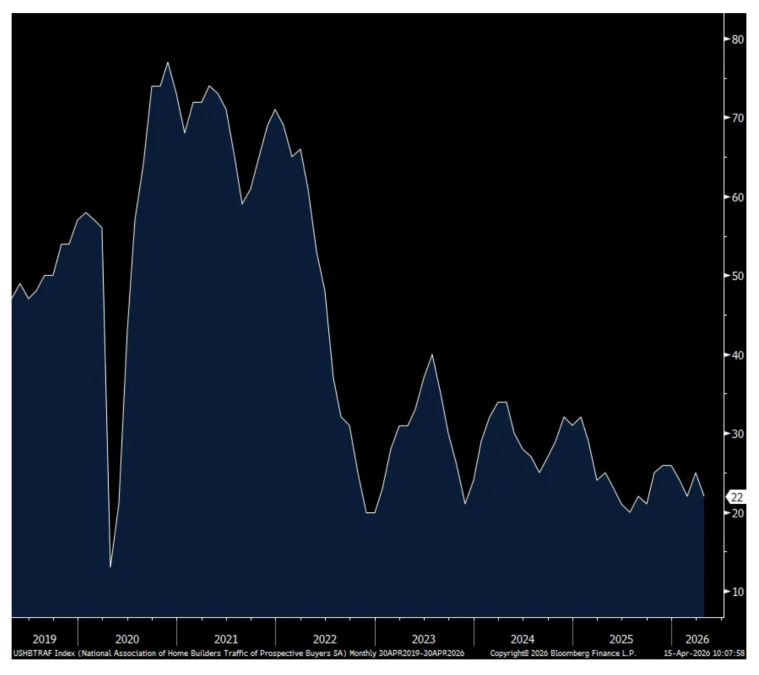

From Peter Boockvar:

The April mood of homebuilders softened further to 34 from 38 in March. The estimate was 37. The Present Situation fell 4 pts m/o/m to 37 while the Future look was down by 7 pts to 42. Prospective Buyers Traffic is not helping with it down 3 pts to just 22 after rising by 3 pts in March.

Higher energy prices have had an immediate impact from a construction perspective. The NAHB said “With oil prices higher in the US, 62% of builders reported suppliers have increased building material costs due to higher fuel prices, including gas and diesel. With near-term economic risks elevated, 70% of builders reported challenges pricing homes given uncertainty about material costs.”

As for the demand side and that depressed level of interested buyers, “buyers face ongoing elevated interest rates and growing economic uncertainty. The year started with hopes for housing momentum growth, but risks with respect to the Iran war, energy costs, and declines for consumer confidence have slowed the market.”

What to do to drive transactions? “The latest HMI survey also revealed that 36% of builders cut prices in April, down slightly from 37% in March. The average price reduction was 5%, down from the 6% figure in March. The use of sales incentives was 60% in April, down from 64% in March, and marking the 13th consecutive month this share has reached 60% or higher.”

Bottom line, so not only does the housing industry have subdued buyer traffic, builders are now thrown a whole new set of raw material and procurement challenges.

NAHB

Prospective Buyers Traffic

None.

BY Doug Kass · Apr 15, 2026, 11:35 AM EDT

As I have been offisdes I am doing little.

In fact, I have not made a trade today - which is unusual for me.

None

BY Doug Kass · Apr 15, 2026, 11:22 AM EDT

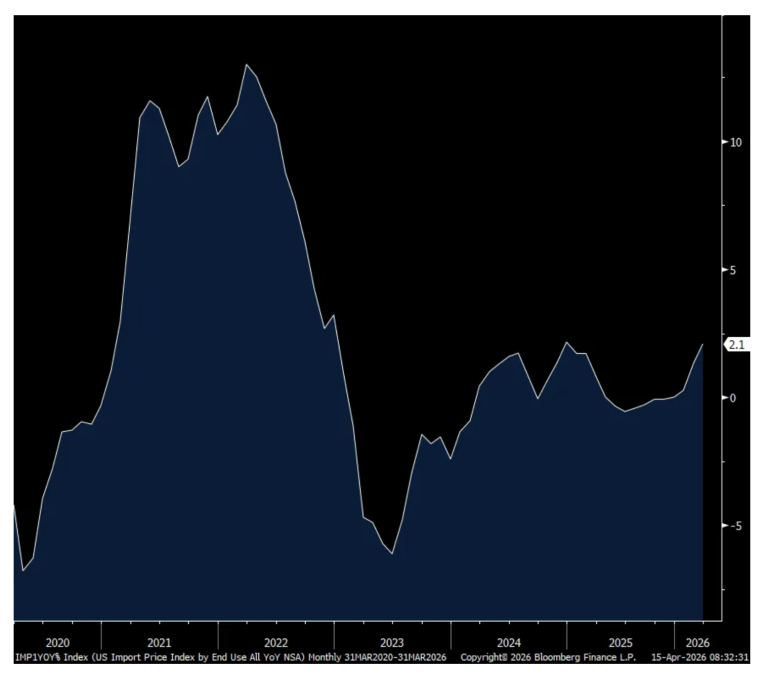

From Peter Boockvar:

After a big jump seen in February of .9% m/o/m (revised down from 1.3%), March import prices rose another .8%, though that was well below the estimate of 2.3%. The y/o/y gain went to 2.1% from 1.3% and that is the most since December 2024. Import prices ex petro rose just one tenth m/o/m but was up .9% in February, .8% in January and .4% in December and still up 2.6% y/o/y. Taking out both fuels and food saw an import price jump of .6% m/o/m vs .9% in February, .7% in January and .3% in December and higher by 3.5% y/o/y.

Higher prices for industrial supplies (up 2% m/o/m and led by fuels), capital goods (up .5% m/o/m), consumer goods (up .4%), and food/beverages (up .5% m/o/m) drove the gains. The only pace where it’s been more muted is in autos/parts where prices were unchanged m/o/m and down .8% y/o/y.

Bottom line, higher import prices started before the war and now with the higher commodity prices, cost pressures are spreading with the only question being how companies manage it, either via prices or margin.

Import Prices y/o/y

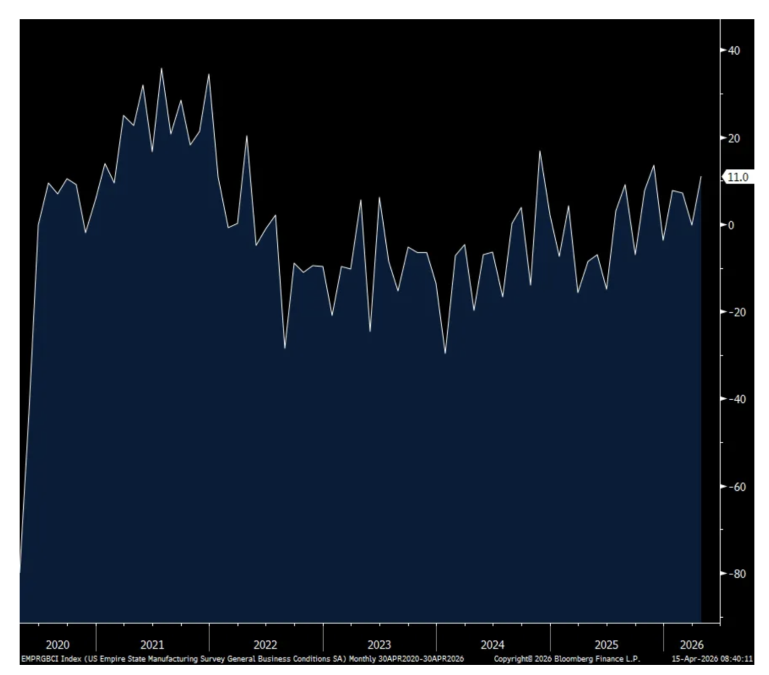

The volatile NY manufacturing index for April rebounded to +11 from essentially zero at -.2 in March and +7.1 in February. What stood out was the 14.4 pt jump in prices paid to 51, the highest since last October but those received were little changed, for now, up .4 pts to 21.8. New orders jumped to 19.3 from 6.4 and I really believe this is mostly due to companies wanting to front load ordering because of the war and fears of shortages. Backlogs and inventories fell slightly.

Employment got better, rising to 9.8 from 5.8 and more than twice the six month average. The workweek also improved.

A drag in the data was the drop in the 6 month business outlook to 19.6 from 31 and that is a 5 month low. Expectations for both prices paid and received were higher. Similar to what was seen in the NFIB Small Business Optimism index, capital spending plans declined to just under the six month average.

Bottom line, I think front running any supply issues helped to lift the headline number and the one for new orders but higher cost pressures is muting the outlook for the coming six months. And that big jump in prices paid in April shows that the March inflation data will likely worsen from here.

NY Mfr’g Index

None.

BY Doug Kass · Apr 15, 2026, 10:00 AM EDT

From Peter Boockvar:

I’m going to start with some earnings calls yesterday with still the consumer bifurcation an issue. Talk about higher gasoline prices and the impact along with what’s going on in the Middle East is now being discussed. Make sure to also read what Lending Tree had to say about the results of their Buy Now, Pay Later survey.

From JP Morgan:

Revenue growth of 10% y/o/y was “primarily driven by higher markets revenue, higher asset management and investment banking fees, and higher NII driven by the impact of balance sheet growth, predominantly offset by the impact of lower rates.”

“Notwithstanding the recent volatility in market and gas prices, based on our data, consumers and small businesses remain resilient, with consumer spend growth continuing above last year’s pace.” The CFO is talking in nominal terms.

In their investment banking and M&A business, “Looking ahead, client engagement and pipelines remain healthy, but of course, developments in the Middle East could have an impact on deal execution and timing.”

On a question about private credit, Jamie Dimon said “I think there’s been some weakening in underwriting, and that’s not just by private credit elsewhere. And there will be a credit cycle one day, and I think when there’s a credit cycle, losses will be worse than people expect relative to the scenario. I don’t think it’s systemic. It almost can’t be systemic at that size ($1.7 trillion) relative to anything else, but when recessions happen, and values go down and people refi at higher rates, there’ll be stress and strain in the system. And are people prepared for that? I can’t speak for other banks, but you’d have to have very large losses in private credit before, at least it looks like banks are going to get hit or something like that. So, it doesn’t mean you won’t feel some stress and strain, and you might have to do something about it, but I’m not particularly worried about it. I’d be more worried about when there’s a credit cycle, how’s that going to filter through the whole system. That to me is a bigger issue.”

What are they seeing on the US consumer? “There really is not anything new or interesting to say this quarter. We’ve looked at it through every angle, early roll rates, delinquency rates, cash buffer, spend, discretionary spend, non-discretionary spend, it all looks consistent with prior trends and fundamentally healthy…So think gas or energy costs is something like 3% of the typical consumer’s expense – spend expenditure, at least in our portfolio. So, it’s not nothing, but it’s not overwhelming. We’ve looked to see if there’s kind of evidence in there of people trading, decreasing other discretionary spending to adjust for higher gas prices, but it’s just kind of not enough yet to be visible.”

Further, “I would caution though, I think it remains fundamentally the case that the biggest single reason that the consumer credit performance is healthy is that the labor market is strong. And if you get bad outcomes in the Middle East, much higher energy prices or other problems that sort of do eventually crack what has been, I think, from many people’s perspective, a surprisingly resilient American economy and a very resilient US consumer, and that winds up having knock-on effects on the labor market then you will see that come through clearly. But right now, in the end, the story remains the same, which is resilient consumer that’s doing fine despite higher gas prices.”

From Citigroup and Jane Fraser’s brief macro commentary:

After a rundown on their numbers, among other comments, “Switching gears, the global macroeconomy to date has weathered shock after shock. However, the impact of the Middle East conflict is hitting Asia and Europe harder than countries such as the US and Brazil, which are more insulated from energy shocks. Clearly, the longer this goes on, the more pronounced the second and third order impacts are going to be around the world. And inflation is now a greater risk to growth that will likely cause central banks to lean towards more restrictive monetary policies.”

With respect to their exposure to private credit, “You can see it’s not a significant exposure for us, right at $22 billion of loans, 98% investment grade. And that’s because we have ample subordination in terms of the position that we take and all the protections…We also have additional protections in terms of our collateral. We have fraud control. We utilize third parties where appropriate so that we just don’t rely on attestations and warranties. And so we feel very good and comfortable that we are able to navigate a range of environment with a portfolio, and it’s all anchored in the strength of our risk capital that we built over time.”

From Wells Fargo:

“Despite slowing employment momentum, US economic growth has held up. The US consumer remains resilient in the aggregate, but increasingly bifurcated beneath the surface. Spending has held up into early 2026, despite slower job growth, supported by higher income households, steady wage growth for incumbent workers and continued access to credit. However, confidence indicators and underlying balance sheet trends point to rising stress for less affluent consumers. Upper income consumers continue to benefit from elevated equity prices, home equity and cash buffers accumulated earlier in the cycle, allowing discretionary spending to remain firm. By contrast, lower income households are more exposed to higher interest rates and energy prices.”

“Consumers are spending more than a year ago, which includes spending more on gas, but they haven’t slowed spending on everything else. Gas represented 6% of our total debit card spend and 4% of our total credit card spend before the rise in oil prices. They now represent 7% and 5% of debit and credit card spend. Note that these numbers are higher for low-income households. We have seen historically that it often takes consumers several months to reduce their spend levels on other categories to adjust for higher oil prices. And while we don’t know the exact timing, we would expect to see the same in the second half of the year. We also expect that higher energy prices will impact other goods and services. The duration and severity will be driven by the level and duration of higher oil prices. Middle-market and large corporate clients are in a similar position. They have been resilient and balance sheets are strong, but they tell us they’re approaching the remainder of the year cautiously.”

“While the markets have reacted to macroeconomic uncertainty, our actual credit performance in the first quarter remains strong. Our net loan charge-off ratio was stable from a year ago and increased 2 bps from the fourth quarter. Commercial credit continues to perform well, and we are not seeing signs of systemic weakness.”

With their consumer loan book, “We continue to closely monitor our portfolios for signs of weakness, but have not observed recent deterioration or meaningful shifts in trends.”

“Client sentiment is cautious but engaged as macro and geopolitical uncertainty has increased and clients have largely shifted to a more selective and defensive posture.”

Carmax stock got whacked by 15% yesterday and said this of note:

“Our EPS during the quarter was impacted by restructuring costs as well as by a non-cash goodwill impairment, while our margins decreased from the prior year quarter as we continue our focus on targeted price reductions and driving sales.”

And more on the strategy of lower prices to improve affordability that would increase sales, “we felt like lower the prices, get sales moving in the right direction, and then pay for it by taking costs out of the business. And I think that’ll be a theme for this team going forward as well, which is figuring out how to grow the company.”

“Average selling price was $26,019, a y/o/y decrease of $114 per unit. Wholesale unit sales are up 3% vs the fourth quarter last year. Average wholesale selling price declined by $268 per unit to $7,776.”

On their auto finance business, “Consistent with the third quarter, credit losses in the fourth quarter were in line with our expectations.” But, “With regard to roll rates and delinquencies, I think across the auto lending industry, lenders would say, customers, maybe absent exception of the highest credit quality, the 800 plus FICO, they certainly are feeling the stress of affordability, inflation, etc...So, those customers from mid-Tier 1 all the way down to deep subprime are feeling the stress, delinquencies are higher, roll rates are higher, and for us as a lender, our job is to support them, help to service them, and then set the reserve accordingly in preparation for that...But there is a stressed customer out there, and we are thoughtful on that.”

More on the consumer from Albertson’s and whose stock fell 3% yesterday:

“In grocery, units and ID sales in Q4 remained pressured in our lowest income cohorts. Egg deflation also created a meaningful sales headwind as we cycled the significant egg shortages from a year ago, a dynamic that we expect persist into the first quarter of 2026.”

“So we’re still expecting industry inflation, food inflation to run around that 2% range. That said, you should know that we have not been passing through that inflation at the 2% rate. We’ve been working on that to help bolster our price position surgically across the company.”

“And as we look forward from a fuel perspective, what I would say is maybe this, and just thinking about the consumer for a second. We do see units remaining pressured across the industry. And that pressure certainly is unevenly distributed. What we’re seeing is increasing pressure on the lower income cohorts. It’s reflected in ongoing affordability changes. We’re seeing further pressure from SNAP regulation, and so forth...and by the way, the middle and upper income customers remain more stable in terms of the pressures that we’re seeing there. But that said, we do recognize our customers are focused on value, our lower income household are most elastic and that’s why we continue to describe our value actions as very surgical. We’re trying to improve the value perception where it changes behavior, again, while protecting long-term returns through productivity funding.”

Kering, the owner of Gucci, YSL, Bottega Veneta, Balenciaga, and others, is trading down 10% in Paris today after releasing numbers yesterday. They said this:

Group revenue fell 6%, “impacted by the strengthening of the euro, and stable y/o/y on a comparable basis. This stabilization represents an important first milestone and a further sequential improvement. It was delivered in a challenging and uncertain environment, with low visibility and continued pressure on consumer confidence. Geopolitical tensions, notably in the Middle East, also weighed on traffic and performance during the quarter.”

“Regional trends remained uneven. Western Europe continued to face headwinds, while North America delivered an excellent quarter, with growth across all brands, clearly standing out as the Group’s strongest region...Asia Pacific declined 4% comparable, an improvement of 2 points compared with Q4...Strong performances in South Korea, Hong Kong, and to a lesser extent Taiwan, were not sufficient to offset the decline in mainland China.” Japan comps fell 3% but “a marked improvement versus previous quarters.”

One more thing on the US consumer. On Monday Lending Tree released an updated analysis on Buy Now, Pay Later and they said this, “A growing percentage of buy now, pay later (BNPL) users say they’ve paid late on one of these loans in the past year. Now, 47% of BNPL users have done so, up six percentage points from 2025 and 13 percentage points from two years ago.”

“That’s just one of the troubling findings...We asked consumers about their behaviors and perspectives regarding these popular loans. Along with increased late payments, we found that more users are buying groceries with these loans and carrying three or more BNPL loans at once, and that more than half of BNPL users say they wouldn’t be able to make ends meet without them.”

https://www.lendingtree.com/personal/buy-now-pay-later-loan-statistics/

The average 30 yr mortgage rate fell 9 bps w/o/w to 6.42% and that helped refi’s rebound by 5.1% after big declines in the prior four weeks. Purchases were little changed though, down 1% after rising by a like amount last week. Nothing new here, affordability remains the big challenge for mostly the first time buyer.

None.

BY Doug Kass · Apr 15, 2026, 9:30 AM EDT

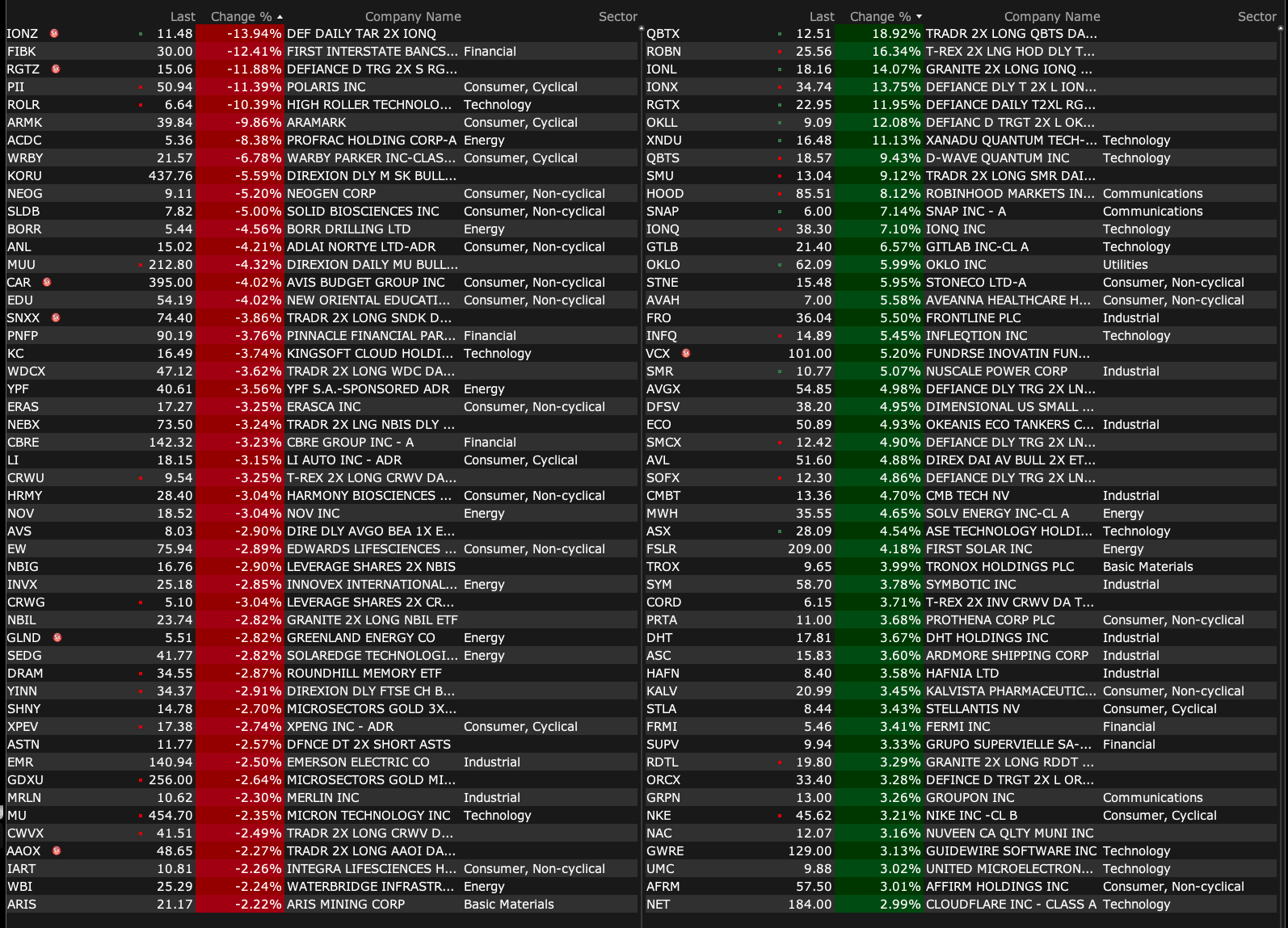

-GLOO +15% (earnings, guidance)

-LAES +11% (autonomous quantum lab demonstrated with EeroQ, Conductor Quantum and NVIDIA)

-QBTS +9.5% (NVDA unveils suite of new open source AI models with goal of accelerating progress in quantum computing)

-BULL +9.3% (momentum following SEC approval of changes to PDT rule)

-IONQ +7.8% (NVDA unveils suite of new open source AI models with goal of accelerating progress in quantum computing)

-HOOD +7.4% (SEC gives go-ahead for major changes to restriction on day trading by small investors)

-MAMA +7.1% (earnings, color)

-SNAP +6.4% (cuts workforce, raises guidance)

-GTLB +6.3% (collaborates with Google Cloud to Bring Agentic DevSecOps to Enterprise Teams Using Vertex AI)

-AEO +5.5% (launches summer jean shorts campaign with Sydney Sweeney)

-ADNT +3.8% (hearing upgraded by Citi to Buy)

-NET +3.3% (Piper/Sandler Raised NET to Overweight from Neutral, price target: $222)

-STLA +3.3% (reports prelim Q1 metrics)

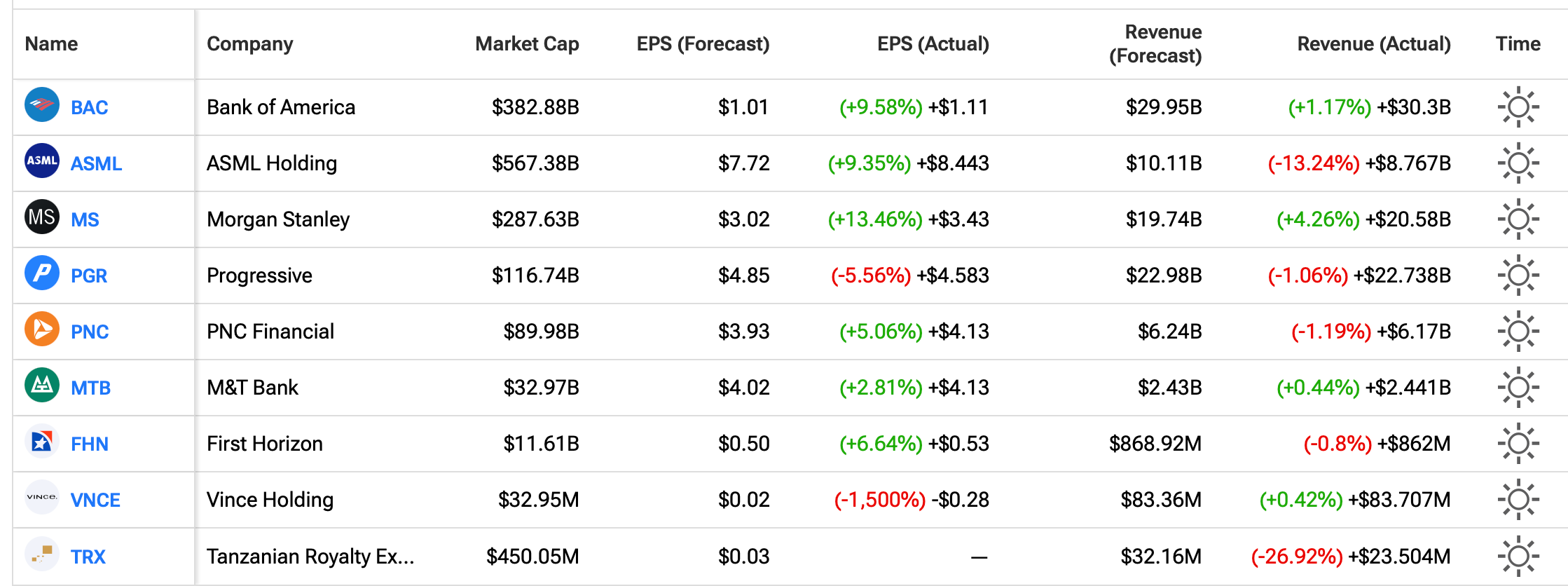

-MS +3.0% (earnings, color)

-AESI +2.5% (hearing upgraded at Citi from Neutral to Buy)

-NKE +2.5% (CEO Hill discloses purchase of 23.7K shares at $42.27/shr on 4/13; Director Tim Cook also buys 25K shares at $42.43/shr on 4/10)

-PUMP +2.5% (hearing Citi upgrades on power contracts)

-AVGO +2.1% (announces Extended Partnership with Meta to Deploy Technology to Support Multi-Gigawatts of Meta’s Custom Silicon)

-DOO -24% (withdraws financial outlook for FY27 due to tariff concerns)

-PII -13% (lower in sympathy with DOO)

-ACHV -8.9% (informed third-party manufacturing facility received OAI classification from FDA inspection)

-WULF -6.7% (prices 47.4M shares at $19.00/share)

-ASML -4.3% (earnings, guidance)

-SEDG -3.0% (Goldman Sachs Cuts SEDG to Sell from Neutral, price target: $31)

-NOV -2.9% (reports prelim Q1)

None.

BY Doug Kass · Apr 15, 2026, 9:20 AM EDT

None.

BY Doug Kass · Apr 15, 2026, 9:00 AM EDT

Source: TipRanks

None.

BY Doug Kass · Apr 15, 2026, 8:40 AM EDT

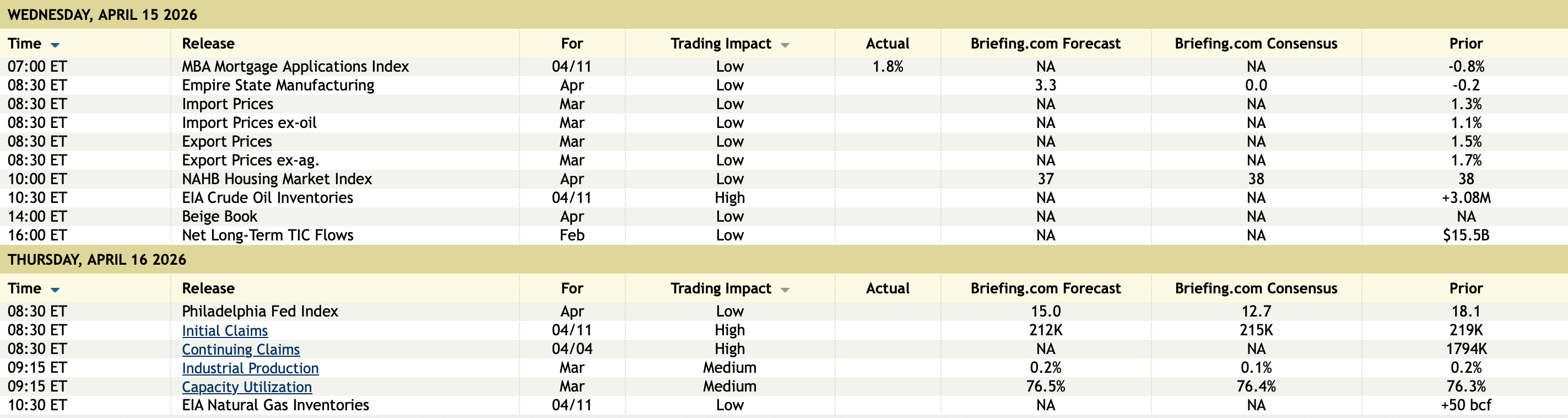

11:00 a.m.: Treasury buyback announcement (cash mgmt);

11:30 a.m.: Treasury hosts a $69B 17-Week Bill Auction;

2:00 p.m.: Fed Beige Book;

2:00 p.m.: Treasury buyback (liq support);

4:00 p.m.: Treasury International cap flows;

4:00 p.m.: Total Net TIC Flows; Net Long-Term TIC Flows (February)

8:30 a.m.: Fed Board Governor Barr (Voter) participates in discussion on "Consumer Compliance Supervision and Regulation" before the National Community Reinvestment Coalition (NCRC) Just Economy Conference, Washington, DC (No text. Q&A from moderator. Webcast available,details forthcoming);

8:30 a.m.: Fed Bank of Cleveland President Hammack (Voter) appears on CNBC's "Squawk Box,";

1:45 p.m.: Fed Vice Chair Bowman (Voter) participates in conversation on "Banking Regulation" before the Institute of International Finance Global Outlook Forum: "Deciphering Risks, Defining Opportunities," Washington, DC (No text. Q&A from moderator. No webcast)

None.

BY Doug Kass · Apr 15, 2026, 8:32 AM EDT

None.

BY Doug Kass · Apr 15, 2026, 8:13 AM EDT

* Bulls cite about +17% growth in S&P 2026 EPS. However, taking out Micron (MU) and Nvidia (NVDA) , brings aggregate EPS growth to only a high-single-digit increase. Good, but not great and likely not suggestive of a broadening in the recent market advance.

* Since the start of the Iran War the prices of "stuff" have materially risen (while the S&P Index is +1%). As seen in the recent PPI release, pipeline inflation remains robust:

Sulfur: +67%

Jet Fuel: +66%

Urea: +51%

Diesel: +50%

Heating Oil: +40%

WTI Crude Oil: +37%

European Natural Gas: +34%

Gasoline: +32%

Fertilizer: +31%

Brent Crude Oil: +31%

Coal: +14%

Palm Oil: +10%

Iron Ore: +7%

Rice: +4%

* The Federal Reserve's hands are tied. The Fed is not in a position to do much about either inflationary or recessionary pressures. As inflation will likely be higher for longer, the Fed cannot be restrictive (in order to dampen those higher costs/prices). Not only is the Administration putting pressure on the Fed to lower interest rates (and would be vocally resistant to implementation of rate increases) but the staggering U.S. debtload and out-of-control deficit limit the ability to tighten. Meanwhile, if the economy weakens — given the cost of war, lower consumer and business confidence and the likely reemergence of inflation — the Fed is not in a position to loosen in order to stimulate economic growth.

* Improvisational foreign and domestic policy may be destabilizing to confidence and economic growth. Iran took us to a worrisome precipice — will there be more Irans... with more dire consequences?

* The AI malinvestment, the secular threat to software and private credit issues have not yet been resolved.

BY Doug Kass · Apr 15, 2026, 7:30 AM EDT

Dougie Kass

630PM

Added to Index shorts:

SPY $694.54

Position: Short SPY common (S), QQQ common (S)

BY Doug Kass · Apr 15, 2026, 6:40 AM EDT

Chart of the Day:

After another V-shaped recovery reminiscent of last year, the S&P 500 has surged roughly +10% in just 10 trading days and now sits less than 0.25% below new all-time highs.

This advance has occurred without leadership from the market’s largest stocks, and if those names begin to outperform the broader market, its likely to act as a powerful tailwind due to the weighting of the indexes.

At the same time, Consumer Discretionary is pushing to new two-month highs relative to Consumer Staples, with the ratio attempting to reclaim the neckline of its former breakdown level.

The Takeaway: The S&P 500 is within striking distance of new highs after a sharp rebound, with outperformance from the Magnificent Seven set to support the next leg higher.

Semiconductor stocks are ripping like never before.$SOX is now up for 10 straight days, gaining over 28%. The strongest 10 day positive streak on record.

— Bluekurtic Market Insights (@Bluekurtic)

There are only 4 such cases, but they show a 100% positivity rate across multiple timeframes, with strong forward returns. pic.twitter.com/cucBT30E4B

BofA: most bearish Fund Manager Survey (FMS) since Jun'25 pic.twitter.com/hdsO9mcJuC

— Mike Zaccardi, CFA, CMT 🍖 (@MikeZaccardi)

Trump Presidency Seasonal Cycle Spring Bottom — S&P 500's low close was March 30, right on cue with the seasonal pattern. During Trump Presidency Years, the market tends to carve out a spring bottom in late March to early April before advancing into year-end. Ceasefire is… pic.twitter.com/LXZsJ8gxiV

— Jeffrey A. Hirsch (@AlmanacTrader)

If micro caps are hitting new highs first... the bull is back! $IWC pic.twitter.com/tQb61ZW2v9

— Against All Odds Research (@JasonP138)

Latin America vs. S&P 500$ILF vs. $SPX pic.twitter.com/D20NnVjn49

— Ian McMillan, CMT (@the_chart_life)

Oil has dropped back down to the anchor from the beginning of the war. All of the prior tests have held as support#levelofinterest$CL_F $USO pic.twitter.com/vMEdvmitlz

— Brian Shannon, CMT (@alphatrends)

Bonus — Here are some great links:

BY Doug Kass · Apr 15, 2026, 6:25 AM EDT

Wolf Street on rising new and used car prices.

BY Doug Kass · Apr 15, 2026, 6:05 AM EDT

“PIK magic”: borrower cannot make interest payment. It defaults.

— Jeffrey Gundlach (@TruthGundlach)

Lenders don’t want to admit defaults.

They book interest as paid that wasn’t.

They increase loan principal by the interest defaulted on.

They keep the loan value at par.

NAV goes up the more loans default.

Voila!

BY Doug Kass · Apr 15, 2026, 5:58 AM EDT

The S&P Short Range Oscillator is at 8.39% vs. 7.17% — that is a deep overbought.

Here is a further explanation of the swiftness from oversold to overbought from MarketEdge:

It has been one month since the Oscillator first hit -7 on March 12th, and since then the S&P 500 has climbed from 6,673 to 6,967, a gain of +4.4%. But that one month number doesn't tell the real story.

On March 30th the Oscillator was still oversold at -4.59 with the S&P 500 at 6,344. It took just 8 trading days to swing from below -4 to above +4, and in 10 trading days the Oscillator has run all the way to +8.39 with the S&P 500 jumping to 6,954, a gain of nearly +9.8%.

This swing is a quick one.

Position: Short SPY common (S), QQQ common (S)

BY Doug Kass · Apr 15, 2026, 5:54 AM EDT

The embedded tweet could not be found…

Semiconductor stocks are ripping like never before. $SOX is now up for 10 straight days, gaining over 28%. The strongest 10 day positive streak on record. There are only 4 such cases, but they show a 100% positivity rate across multiple timeframes, with strong forward returns.

Oil has dropped back down to the anchor from the beginning of the war. All of the prior tests have held as support #levelofinterest $CL_F $USO

If micro caps are hitting new highs first... the bull is back! $IWC

“PIK magic”: borrower cannot make interest payment. It defaults. Lenders don’t want to admit defaults. They book interest as paid that wasn’t. They increase loan principal by the interest defaulted on. They keep the loan value at par. NAV goes up the more loans default. Voila!

Trump Presidency Seasonal Cycle Spring Bottom — S&P 500's low close was March 30, right on cue with the seasonal pattern. During Trump Presidency Years, the market tends to carve out a spring bottom in late March to early April before advancing into year-end. Ceasefire is Show more

The last 10-days have been unlike any 10-day period in the market since 1950. First, the S&P 500 is up 9.8% in 10-days, which is in the 99.7th percentile of all 10 day returns.

I wish the Allbirds people luck in their attempt to pivot to GPUs. Maybe they can do it. But i regard this as the first definitive sign that things have gone too far. What a bunch of jokers and mountebanks they are..