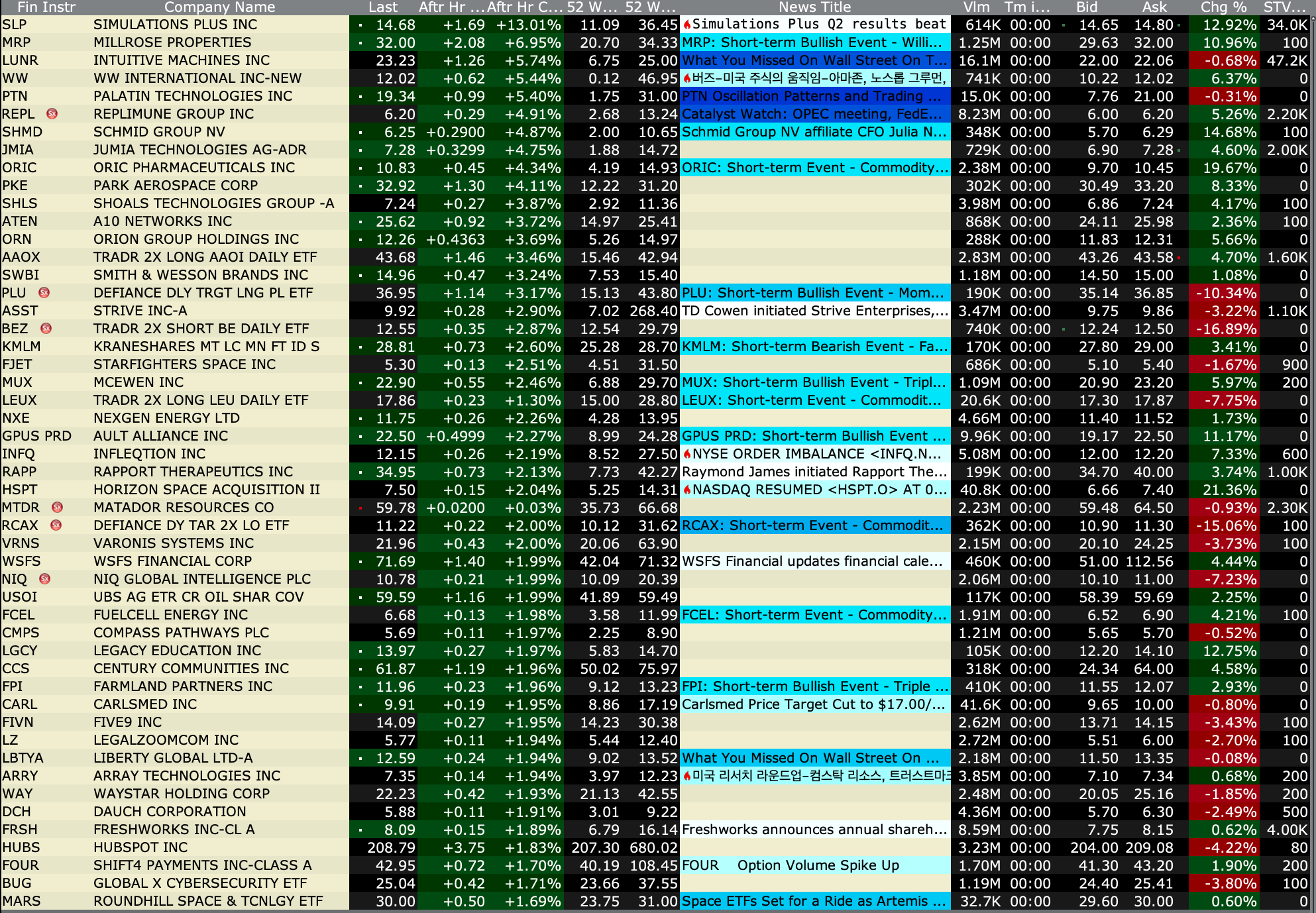

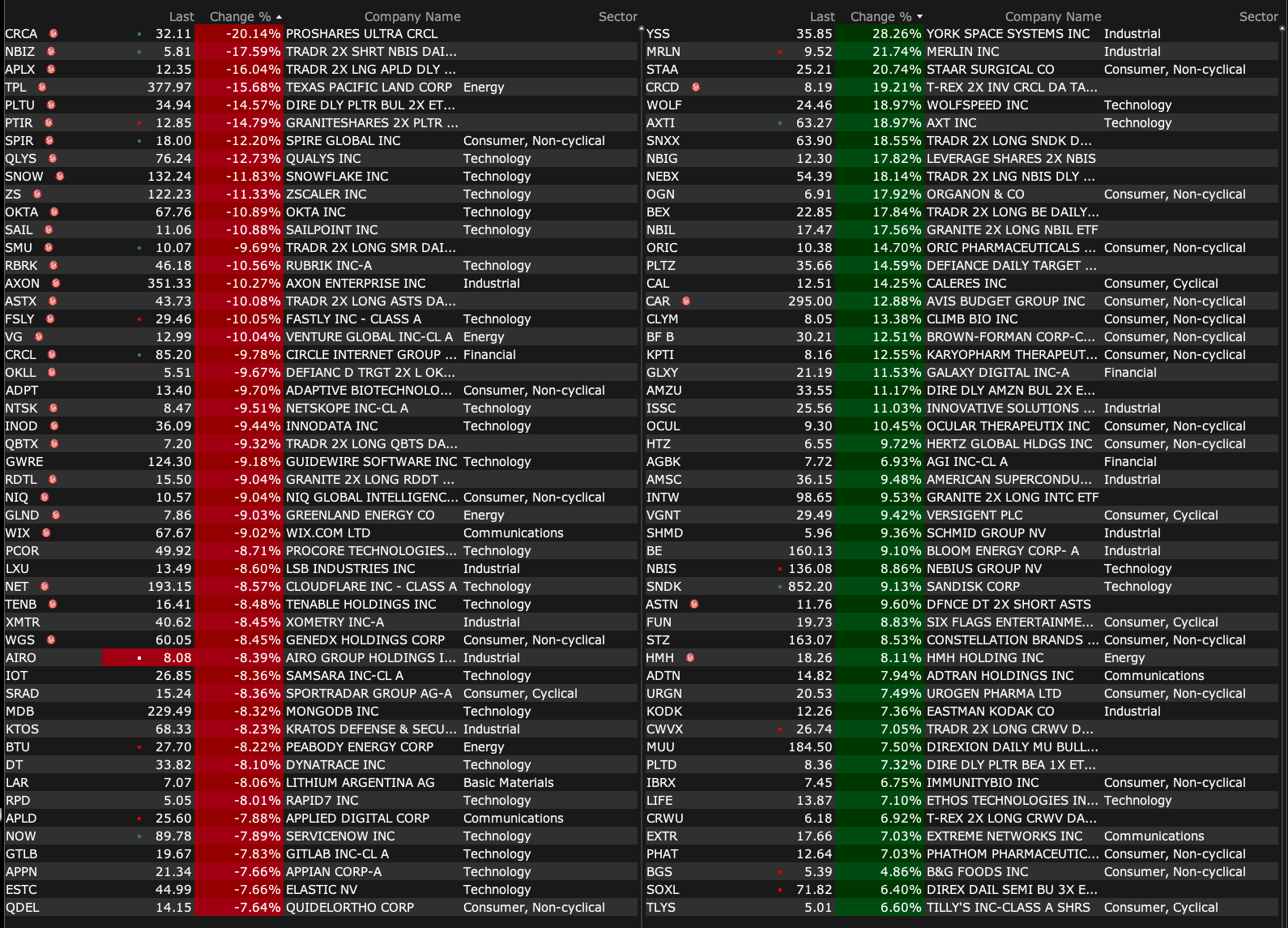

Thursday's After-Hours Advancers and Decliners

After-Hours % Advancers

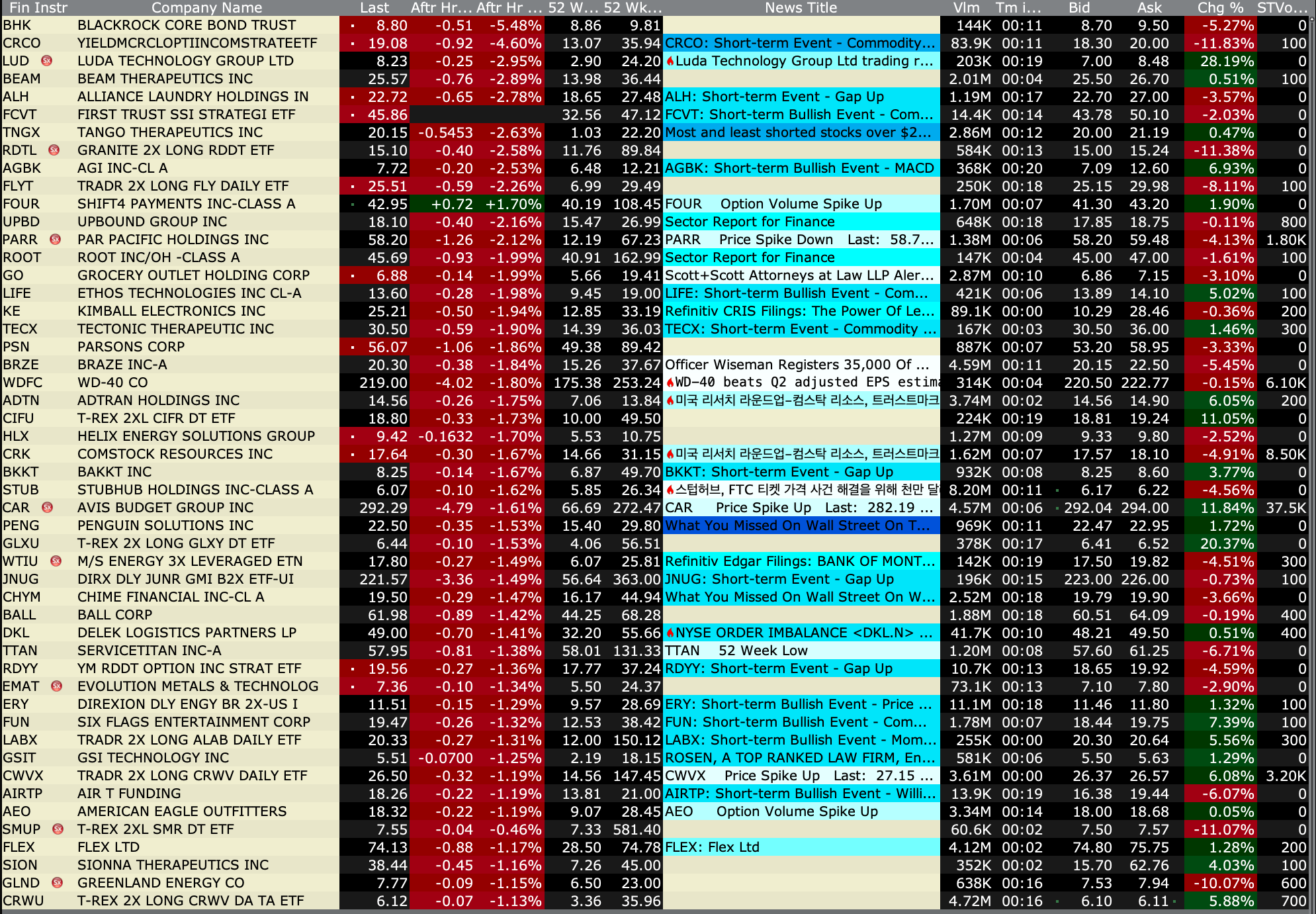

After-Hours % Decliners

BY Doug Kass · Apr 9, 2026, 4:45 PM EDT

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Apr 9, 2026, 4:45 PM EDT

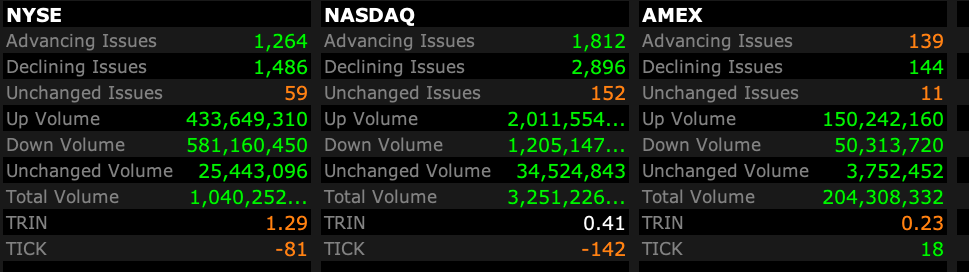

Closing Volume

- NYSE volume 14% below its one-month average

- NASDAQ volume flat to its one-month average;

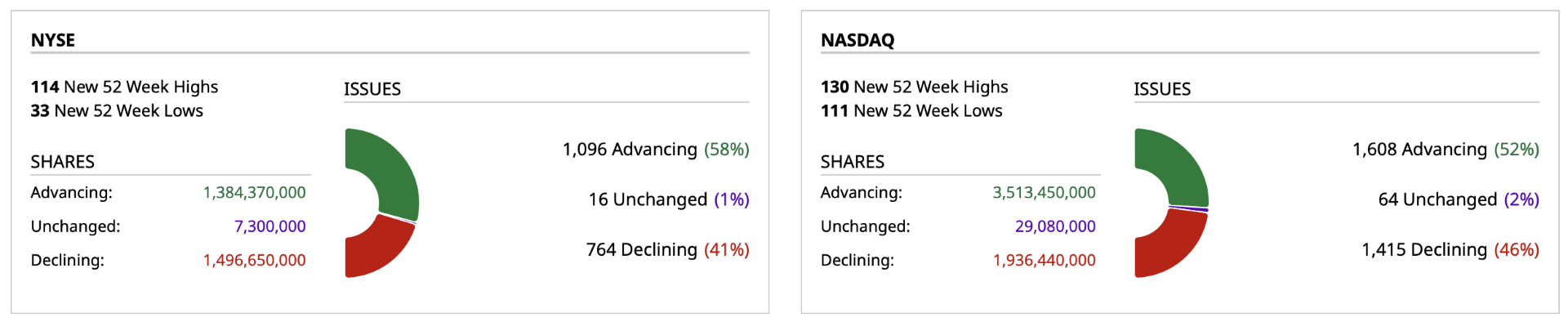

Breadth

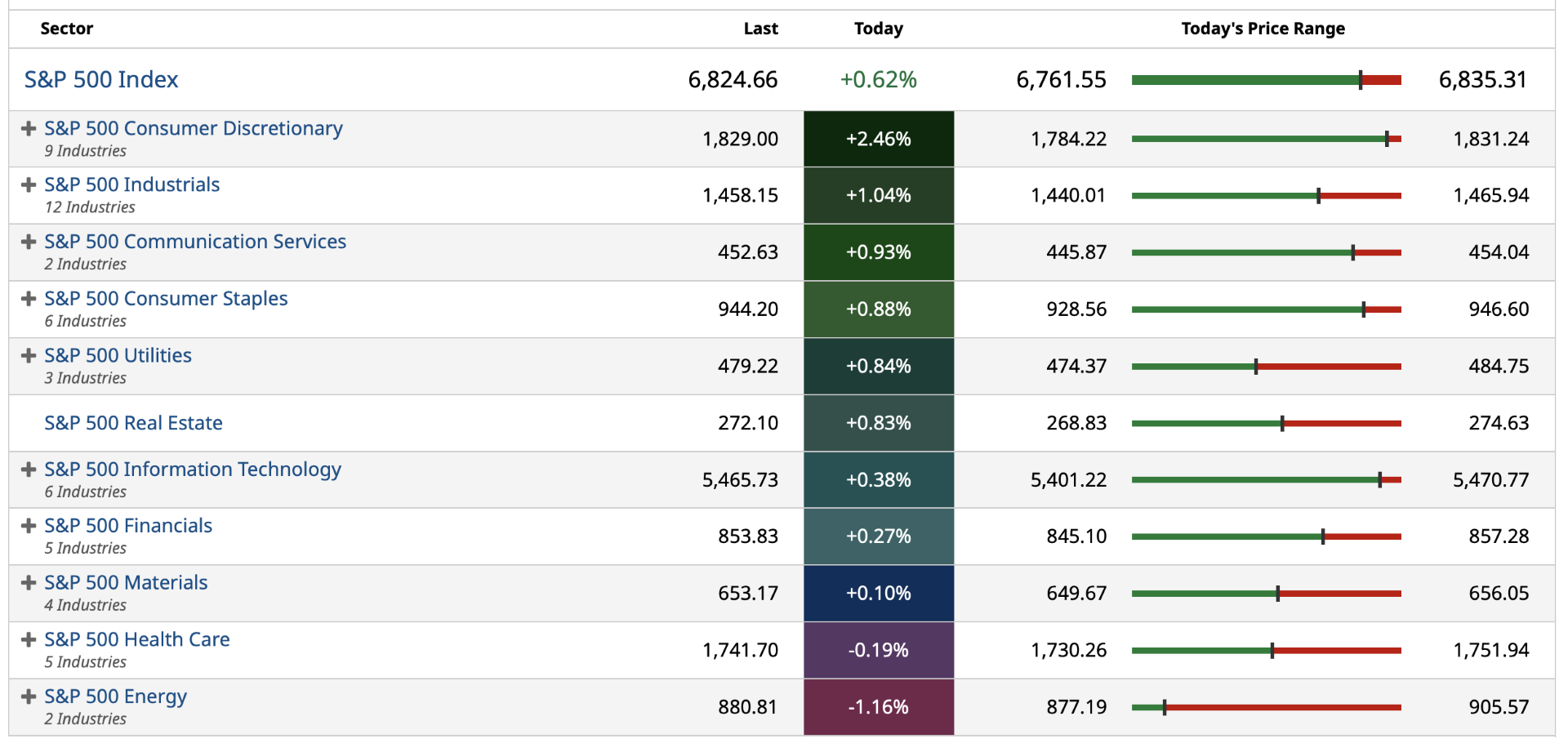

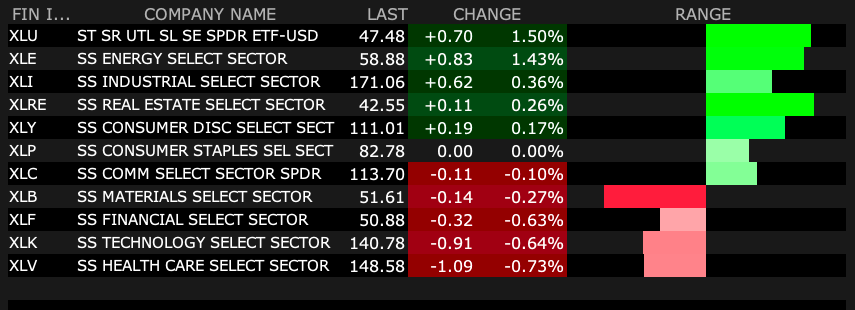

S&P 500 Sectors

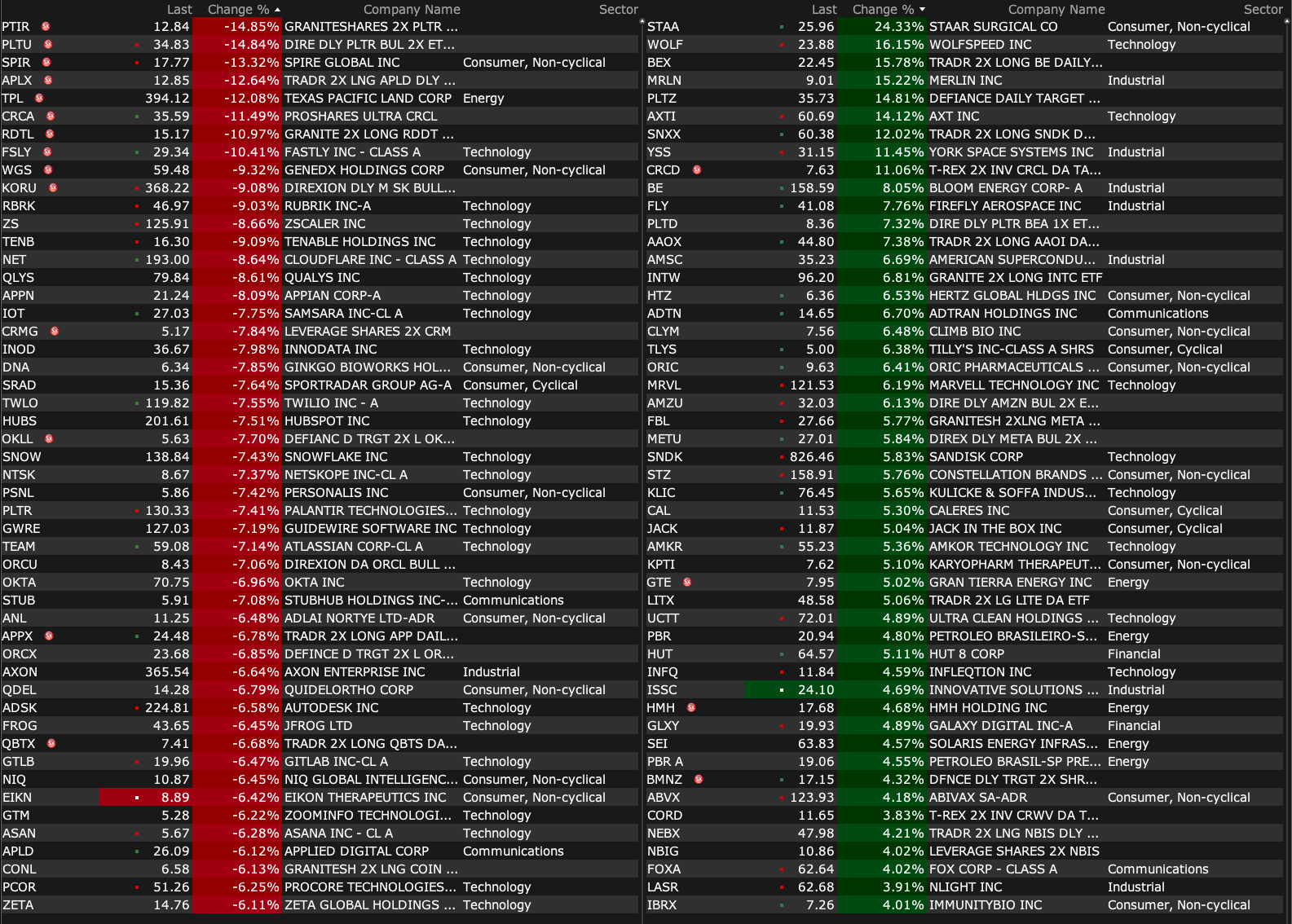

% Movers

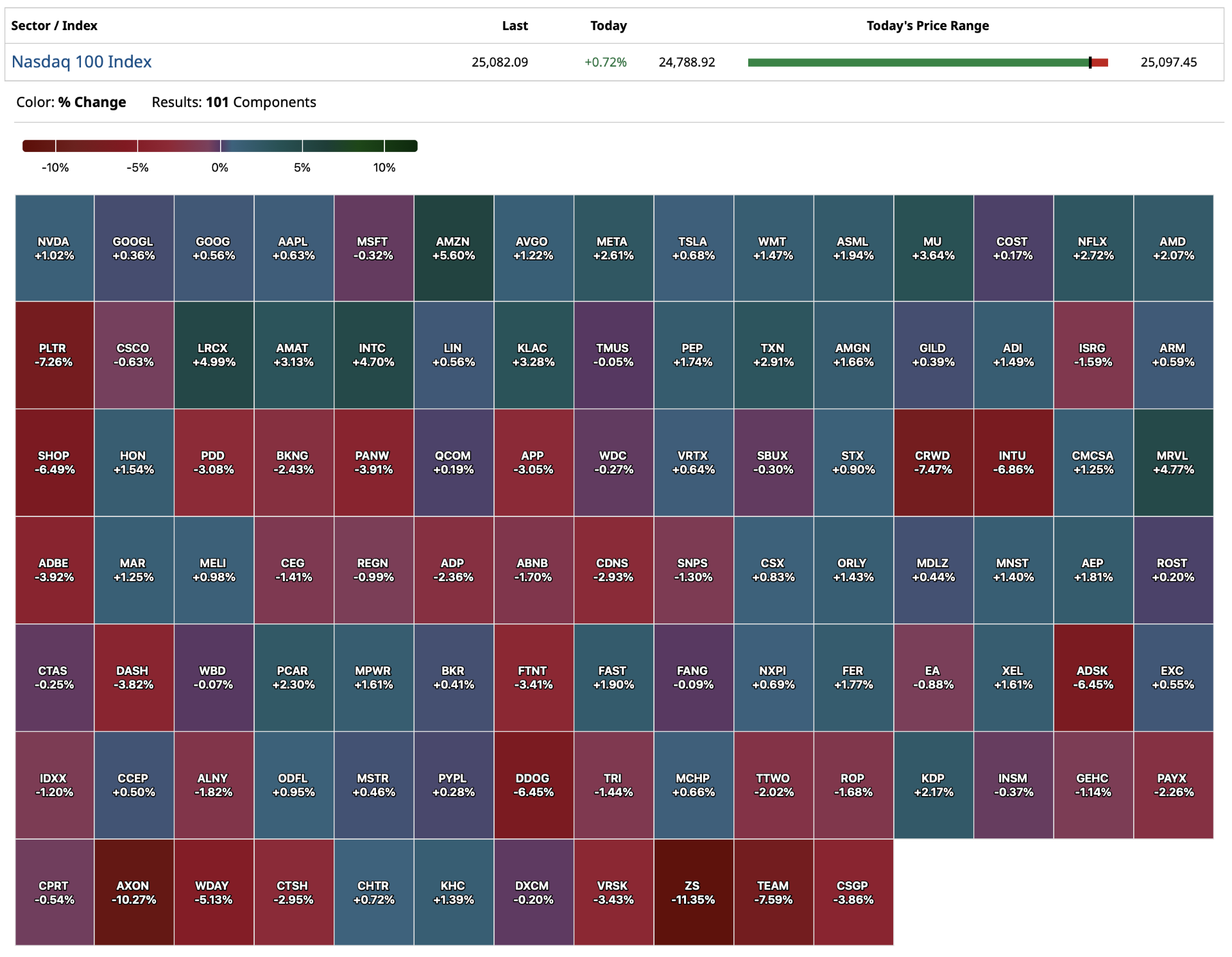

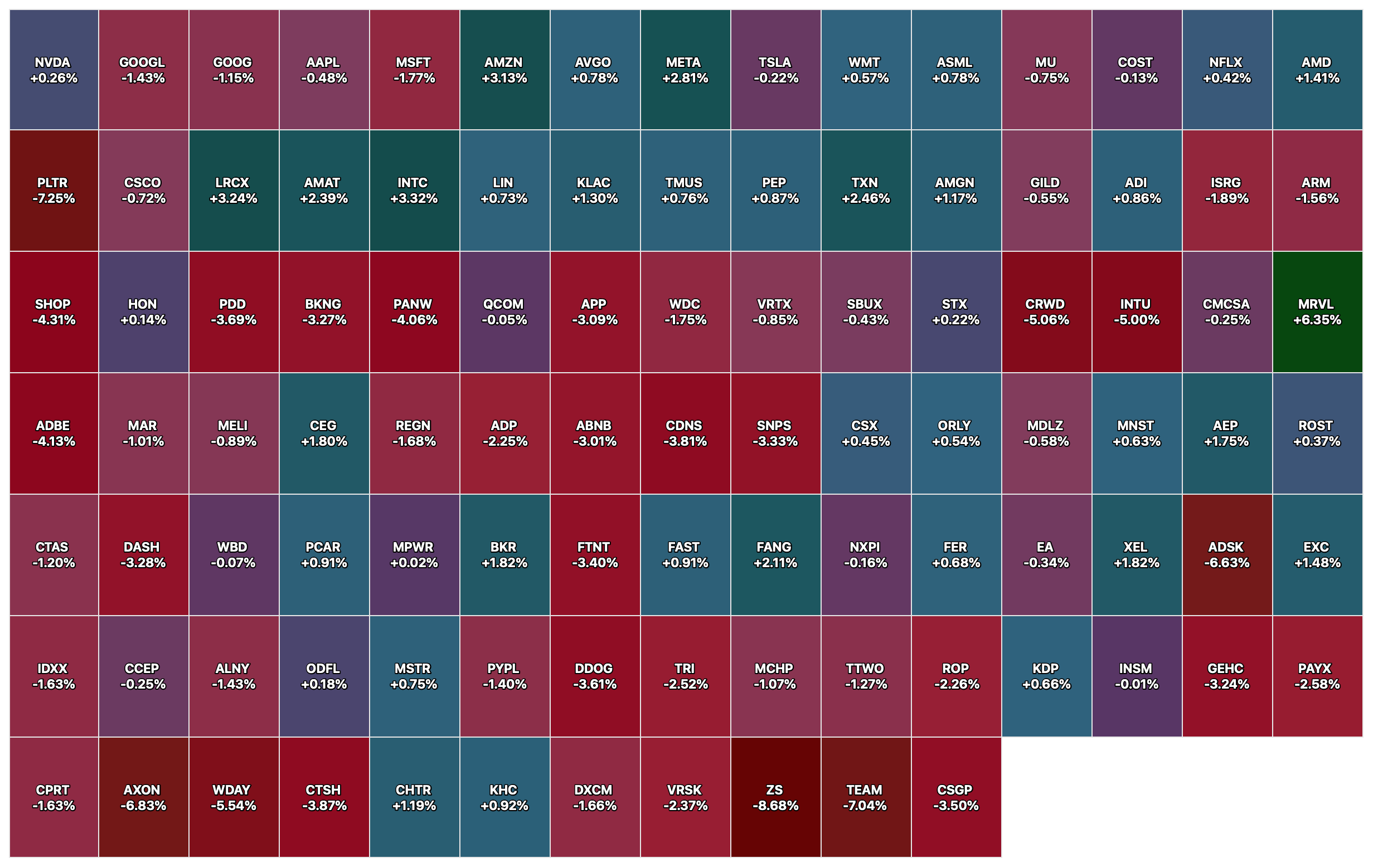

Nasdaq 100 Heat Map

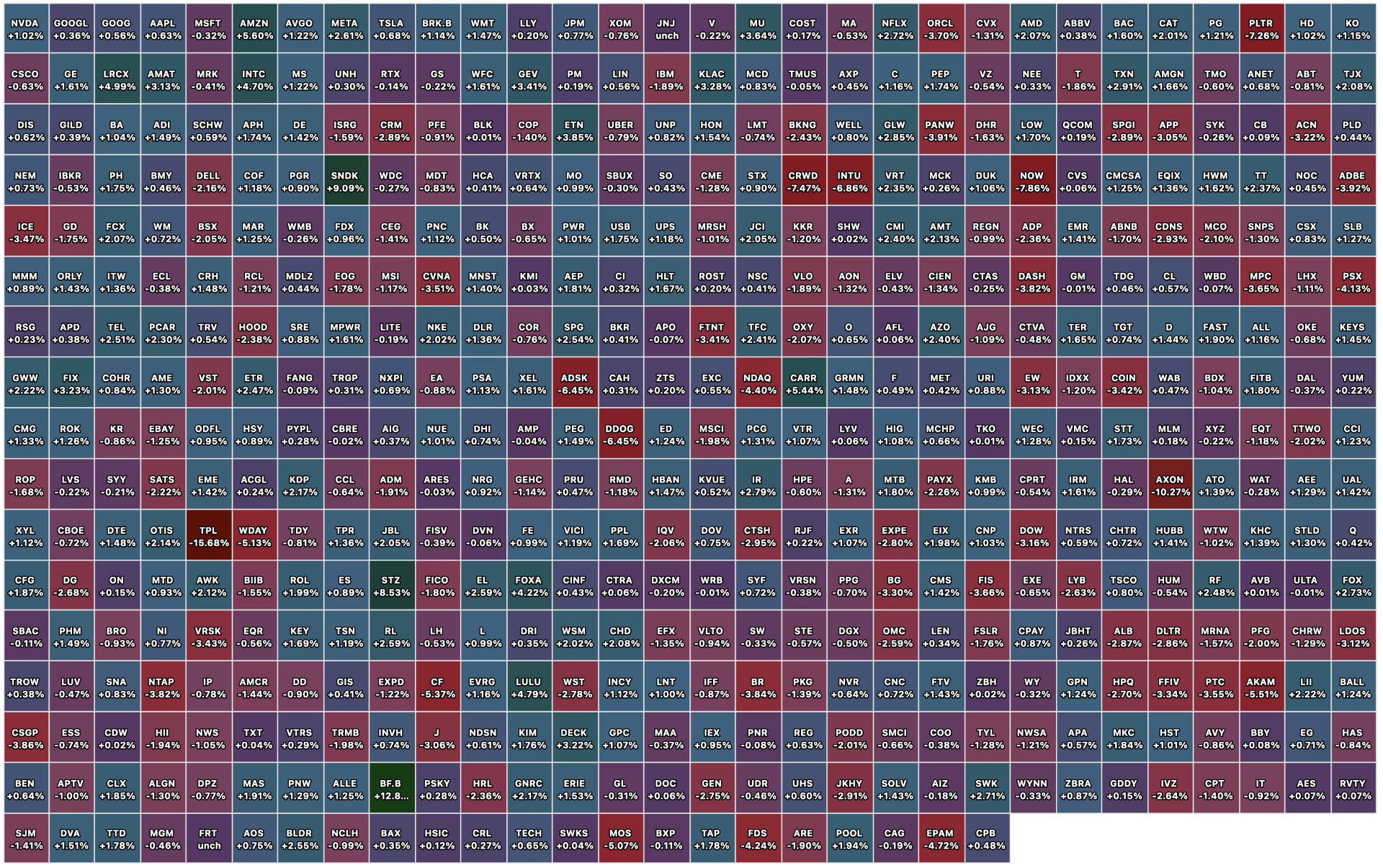

Closing S&P 500 Heat Map

BY Doug Kass · Apr 9, 2026, 4:27 PM EDT

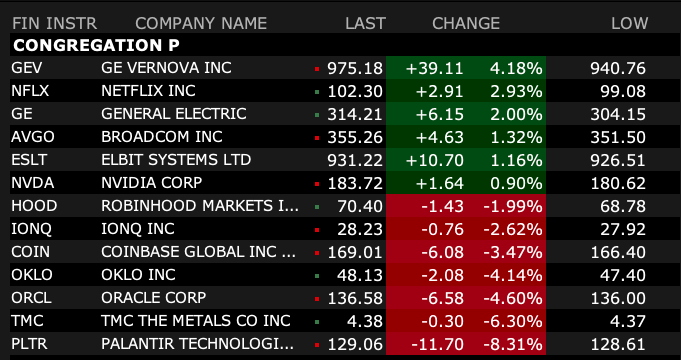

Sorted by % change on the day at 3:05 PM:

BY Doug Kass · Apr 9, 2026, 3:10 PM EDT

Programming Note:

I will be running out to the dentist about 10 minutes before the close.

BY Doug Kass · Apr 9, 2026, 2:55 PM EDT

I covered most of my index shorts for a small loss:

* (SPY) $679.09

* QQQ $608.17

I think I will regret this move.

Position: Short SPY common (VVS), QQQ common (VVS)

BY Doug Kass · Apr 9, 2026, 2:28 PM EDT

Howard Marks' latest commentary.

BY Doug Kass · Apr 9, 2026, 1:22 PM EDT

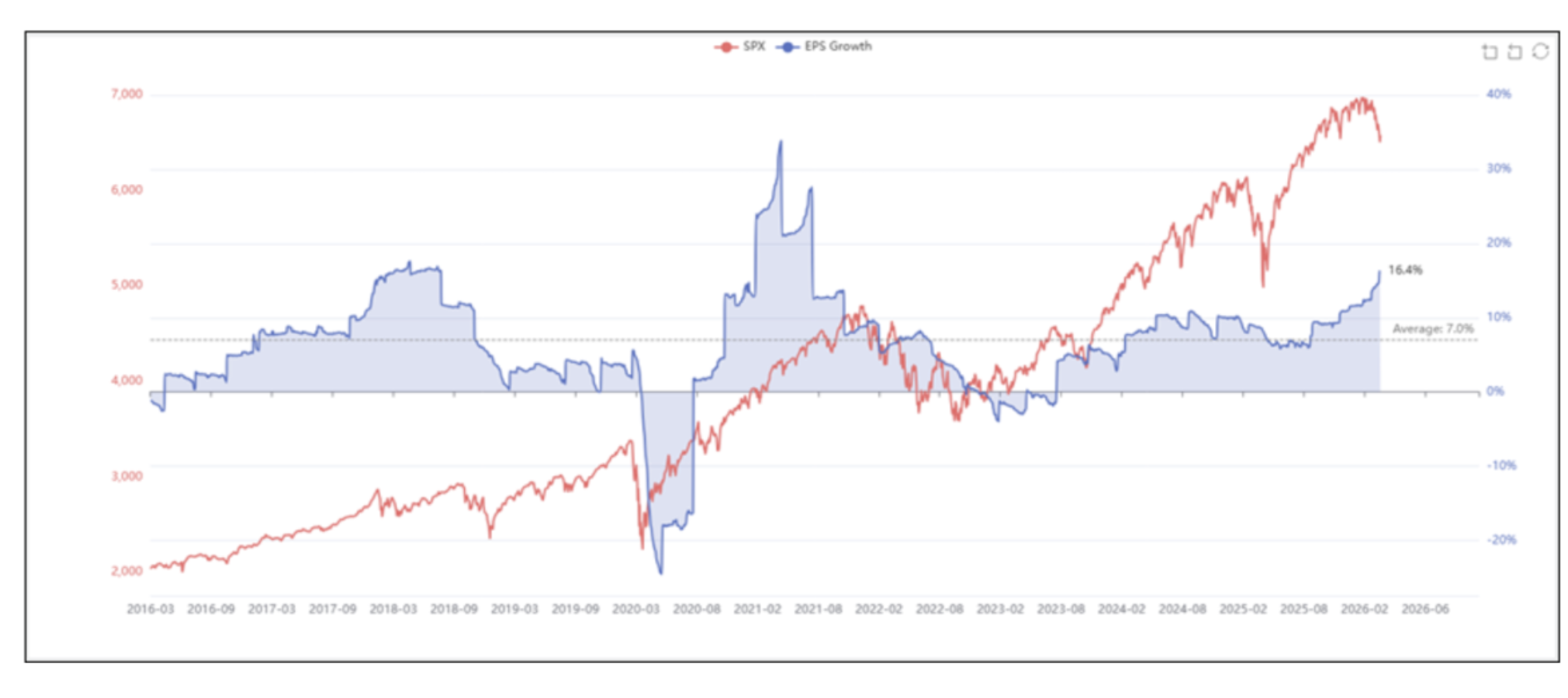

Fin TV is remarkably simplistic as they (day in and day out) solely, simply and confidentally look at the markets in a linear way.

— Dougie Kass (@DougKass)

Nearly every discussion in projecting stock prices is the observation of S and P (and sector) estimated EPS change (year over year).

I used to…

BY Doug Kass · Apr 9, 2026, 1:00 PM EDT

Programming Note:

I have a research call at 12:30 PM and another one at 3 PM today.

BY Doug Kass · Apr 9, 2026, 12:37 PM EDT

- NYSE volume 21% below its one-month average;

- Nasdaq volume 2% above its one-month average;

- VIX index: down 1.14% to 20.80

None.

BY Doug Kass · Apr 9, 2026, 11:50 AM EDT

I added further to my index shorts on the rally over the last few minutes:

* (SPY) $677.44

* (QQQ) $606.95

Position: Short SPY common (VS), QQQ common (VS)

BY Doug Kass · Apr 9, 2026, 11:43 AM EDT

I've added to my index shorts:

* (SPY) $676.07

* (QQQ) $606.12

Position: Short SPY common (S), QQQ common (S)

BY Doug Kass · Apr 9, 2026, 11:32 AM EDT

Dougie Kass

Shorted more GRNY $24.85 and reinitiated short in QQQ $605.46.

ReplyShare

Dougie Kass

5m ago

shorted more qqq $606.44

ReplyShare

i also added to spy short at $675.42

Short GRNY S QQQ S SPY S

BY Doug Kass · Apr 9, 2026, 11:20 AM EDT

From Peter Boockvar:

Capturing consumer inflation situation pre war/Claims, uptick in hiring or expiring benefits?

Capturing what the consumer inflationary world looked like pre war, the February PCE headline rate was up .4% m/o/m and the same with the core rate with both as expected. The y/o/y increases were 2.8% and 3% respectively for each for 2.8% and 3.1% in January.

Goods disinflation is over and prices in this category rose 1.8% y/o/y, the highest since 2023. Services inflation remains, up 3.3% y/o/y, though we know rental price growth will continue to decelerate, for now.

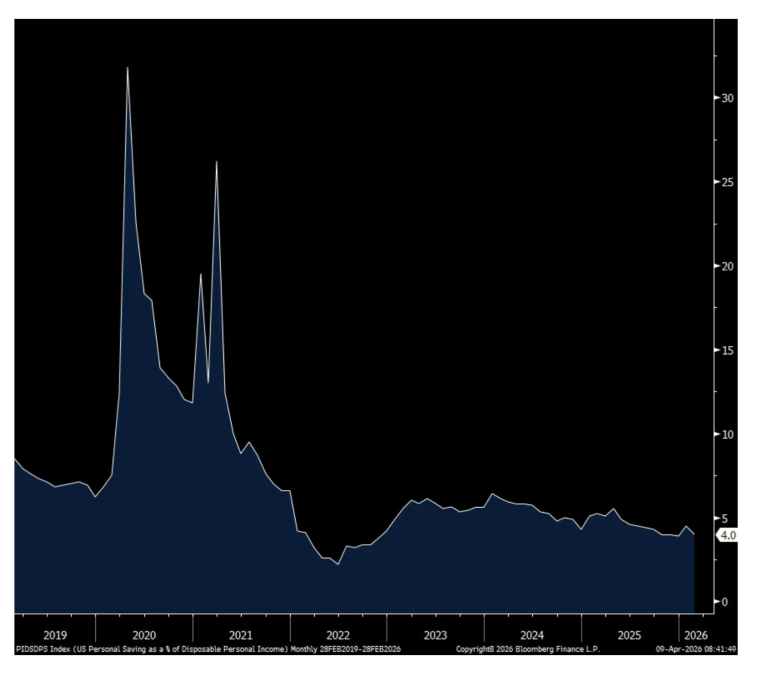

Income growth disappointed, down .1% vs the estimate of up .3% and when combined with the .5% increase in spending (est was up .6% and January was revised down by one tenth which could trim Q1 GDP estimates), the savings rate fell to 4% from 4.5% and that is one tenth from the lowest since 2022.

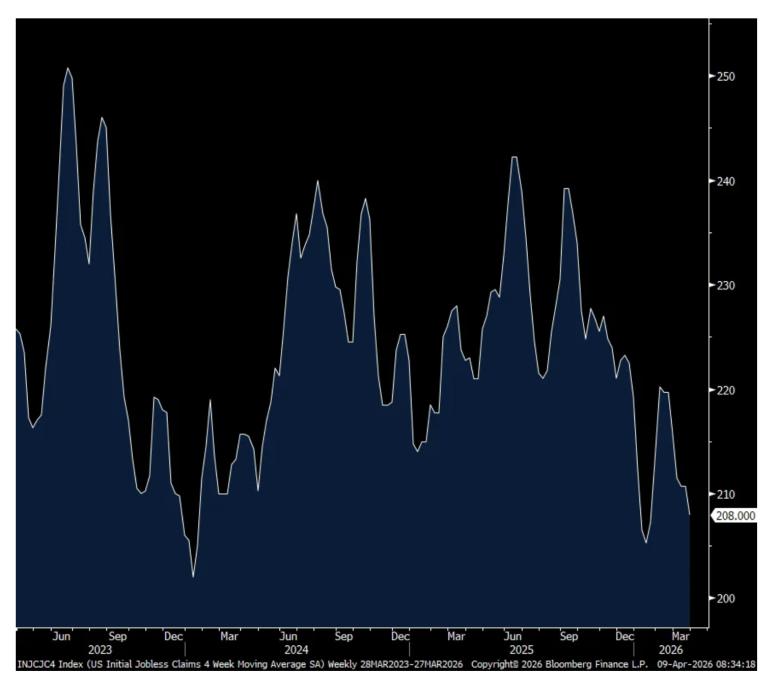

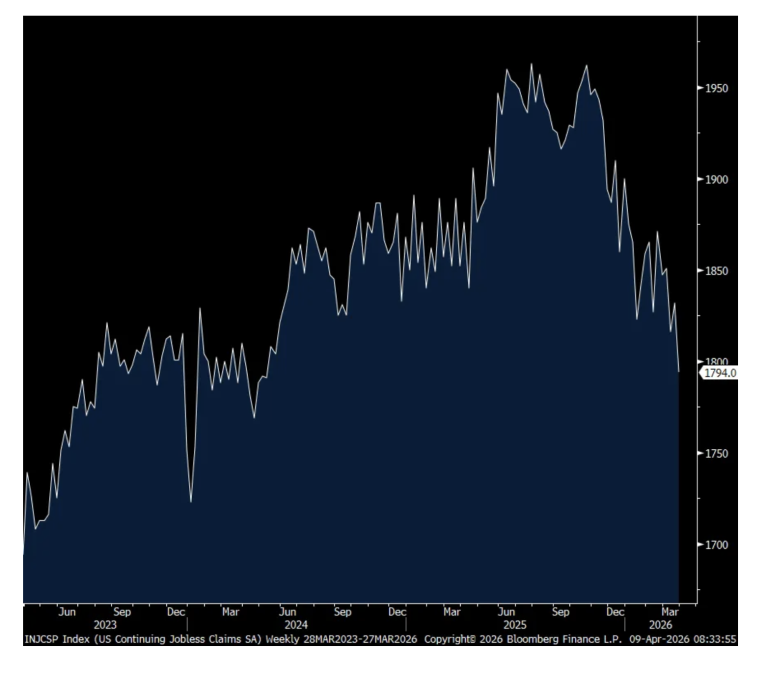

Initial jobless claims rose to 219k from 203k and that was 9k above the estimate. The 4 week average increased by 1.5k w/o/w to 210k. Delayed by a week in its reporting, continuing claims fell below 1.8mm to 1.794mm, the lowest since May 2024 from 1.832mm. The big question here, I’ll ask again, is whether people are finding new jobs or benefits are expiring. As seen with the recent hiring stats (including smoothing out the March upside surprise from the BLS in their establishment survey), I’m afraid it could be more of the latter than the former.

Savings Rate

Initial Claims 4 week avg

Continuing Claims

None.

BY Doug Kass · Apr 9, 2026, 11:08 AM EDT

Well, they tell me of a pie up in the sky

Waiting for me when I die

But between the day you're born and when you die

They never seem to hear even your cry

So as sure as the sun will shine

I'm gonna get my share now, what's mine

And then the harder they come

The harder they fall, one and all

Ooh, the harder they come

The harder they fall, one and all,,,

- Jimmy Cliff - The Harder They Come

Palantir (PLTR) and Salesforce (CRM) .

None

BY Doug Kass · Apr 9, 2026, 10:50 AM EDT

From Peter Boockvar:

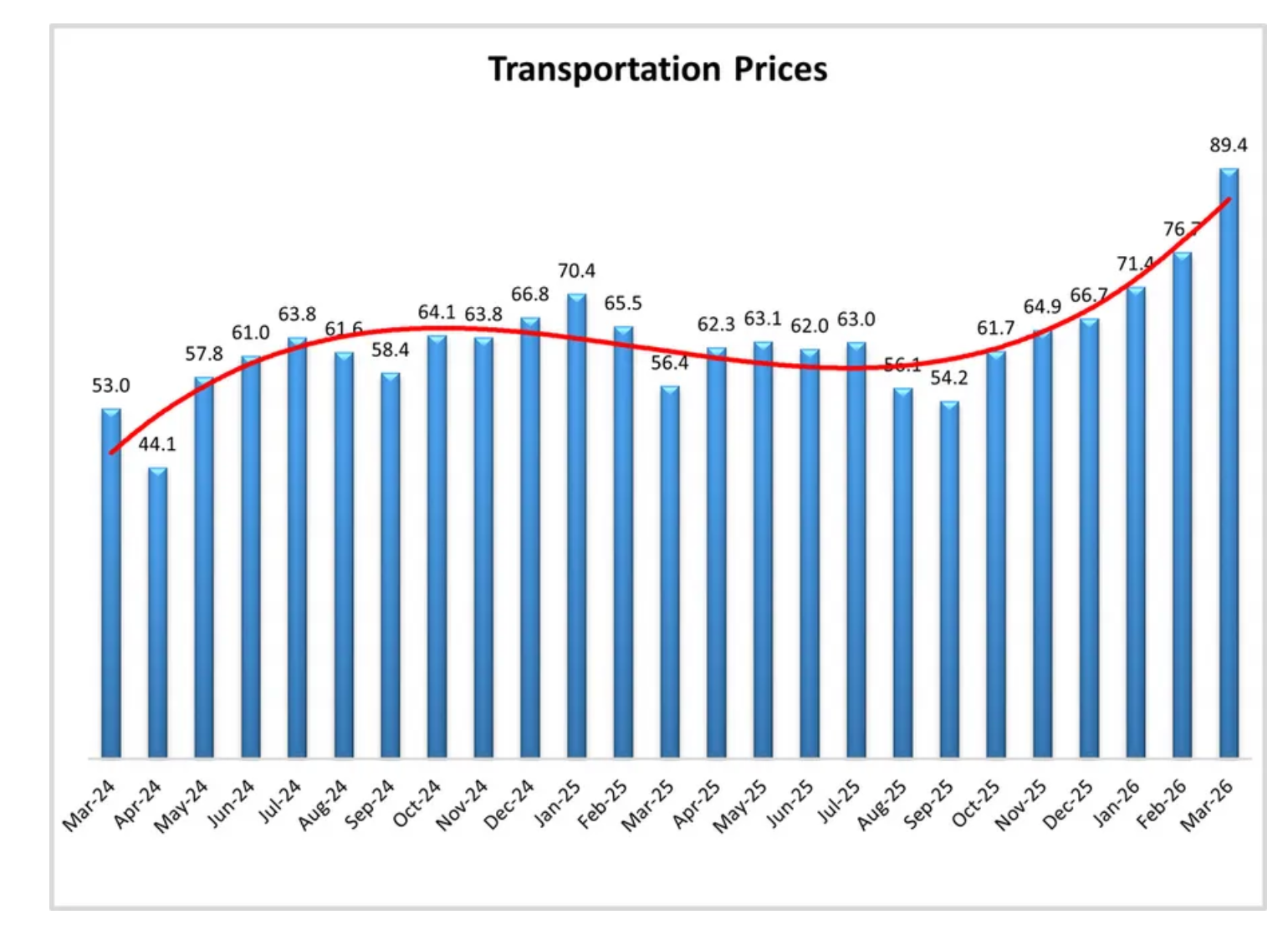

I’ll start with transportation today after going through the March Logistics Managers’ Index that came out Tuesday because I want to highlight the pricing situation and something I’ve touched upon after going through the trucking earnings calls over the last few months. Also, talk about inventories. Pricing continues to firm up because of the growing implications of excess capacity leaving the market. “Transportation prices skyrocketed (+12.7) in March to 89.4, which is the highest level since March 2022” when it got to 89.7. “Much like the spike four years ago, the rapid increase this month is at least partially attributable to the start of an armed conflict with Iran – and subsequent closure of the Strait of Hormuz – has taken approximately 20% of oil off the board in 2026. In 2022, this caused significant supply driven inflation which slowed consumer demand and ultimately led to a long lasting freight recession.”

“While there are some clear similarities in the logistics situations in 2026 and 2022, there are some differences as well…The biggest difference between now and four years ago is the inventory situation. Inventory levels were expanding quickly at 75.7 in early 2022, standing in contrast to 2026’s leaner, faster turning inventory levels which are expanding only marginally at 54.8…With the current leanness of inventories, firms will not have large stores of goods and components to draw on, which may necessitate some continued movement in freight. The leanness extends to fleet sizes as well, which have right sized considerably since 2022, meaning there will be less excess capacity this time around.” I bolded for emphasis.

We know the spike in diesel prices are a major factor here too. And on the pass through of the diesel price spike, “For the first time in its history the USPS announced a temporary price increase – with prices up by 8% - to cover increased fuel costs. These increases have spread to private carriers as well, with FedEx and UPS increasing their ground transportation prices by 26.5% and 27% respectively.”

I’ll add this thought, with leaner inventories, there maybe isn’t enough cushion if Strait closure induced supply chain shortages start to pick up in the US.

With respect to air travel, this is what Delta said of note on their call:

“Demand was broad based across corporate and leisure, with continued momentum in high margin, diverse revenue streams…Looking at the current environment, demand remains strong. The acceleration we saw in March is carrying forward into the June quarter. Over the last month, cash sales, which are the clearest indicator of demand, are up double digits, with strength across the booking curve, geographies, and products. Our consumers are continuing to prioritize experiences, with travel among the top spending categories.”

In response to the jet fuel price spike, “we are meaningfully reducing capacity in the current quarter, with a downward bias until we see the fuel situation improve. At the same time, we’re moving quickly to recapture higher fuel prices.”

Premium continues to drive most of their revenue growth but “Importantly, we saw an inflection in main cabin, with the first full quarter of positive unit revenue growth since the end of 2024.”

As for the new quarter, “we see actually really good demand right now across all entities. We’re going into peak summer for transatlantic, and that looks very good right now. Transatlantic was a bright spot for the first quarter…across all the booking curves and across all the booking periods, we’re seeing strong demand.”

Where is there softness? “A couple of places that we’ve talked about before is point-of-sale Europe has been a little bit weaker. We’ve seen a little bit of weakness in Mexico leisure, just with the incidents that occurred in Puerto Vallarta, and we’ve taken capacity actions there. So, a couple of hotspots around our network, but overall, very broad strength in what we’re seeing.”

The business of Levi Strauss seems to be good and from their Tuesday call of note:

“We saw the growth broad based across segments, channels, genders and categories…We are very cognizant of the environment around us, but our consumer is responding to innovation, newness, and Levi’s is a great value.”

Shifting gears to central bank policy. It’s clear for now that many central bankers right now are just spectators, waiting to see how things play out. After the RBNZ did so yesterday, the Reserve Bank of India stood on its hands too leaving its benchmark repo rate at 5.25%. Governor Malhotra said “We in the RBI stand committed to this policy and would judiciously continue to contain excessive or disruptive volatility to ensure that self fulfilling expectations do not exacerbate currency movements beyond what is warranted by fundamentals.” We know India is a major importer of its energy needs and is definitely being economically hurt but I still believe it’s one of the most exciting economic growth stories for years to come and we remain long stocks there.

None.

BY Doug Kass · Apr 9, 2026, 10:45 AM EDT

Here are some relevant moves from the sellside:

American Express price target lowered to $325 from $375 at JPMorgan JPMorgan analyst Richard Shane lowered the firm's price target on American Express (AXP) to $325 from $375 and keeps a Neutral rating on the shares. The firm adjusted targets in the consumer finance group as part of a Q1 earnings preview. The macroeconomic environment "remains volatile and unpredictable," the analyst tells investors in a research note. JPMorgan says "selectivity remains paramount" in this environment.

Procter & Gamble price target lowered to $167 from $172 at RBC Capital RBC Capital lowered the firm's price target on Procter & Gamble (PG) to $167 from $172 and keeps an Outperform rating on the shares as part of a broader research note previewing Q1 results in Home and Personal Care, Beverages, and Packaged Food categories, The March quarter should be fine, characterized by a still sluggish top-line environment, though much of the emphasis will be on forward commentary due to Middle East conflict, which has created top-line and inflationary risks, the analyst tells investors in a research note. This ceasefire announcement is a positive but the firm still expects lingering impacts and elevated commodity prices relative to prior to the conflict, RBC added.

PepsiCo price target lowered to $163 from $165 at RBC Capital RBC Capital lowered the firm's price target on PepsiCo (PEP) to $163 from $165 and keeps a Sector Perform rating on the shares as part of a broader research note previewing Q1 results in Home and Personal Care, Beverages, and Packaged Food categories, The March quarter should be fine, characterized by a still sluggish top-line environment, though much of the emphasis will be on forward commentary due to Middle East conflict, which has created top-line and inflationary risks, the analyst tells investors in a research note. This ceasefire announcement is a positive but the firm still expects lingering impacts and elevated commodity prices relative to prior to the conflict, RBC added.

Winnebago price target lowered to $43 from $47 at Truist Truist lowered the firm's price target on Winnebago (WGO) to $43 from $47 and keeps a Buy rating on the shares as part of a broader research note on recreational vehicles. For the industry, despite expectations for weather-related weakness in February, the North American retail revenues were down low 20%, which was even weaker than expected, the analyst tells investors in a research note. This is a sizable deceleration from January's decline of 10.8%, the firm added.

KKR price target lowered to $102 from $112 at TD Cowen TD Cowen lowered the firm's price target on (KKR) to $102 from $112 and keeps a Hold rating on the shares. The firm adjusted targets in the asset manager, broker dealers and exchanges group as part of a Q1 preview.

Blackstone price target lowered to $141 from $164 at TD Cowen TD Cowen analyst Bill Katz lowered the firm's price target on Blackstone (BX) to $141 from $164 and keeps a Buy rating on the shares. The firm adjusted targets in the asset manager, broker dealers and exchanges group as part of a Q1 preview.

Apollo Global price target lowered to $126 from $146 at TD Cowen TD Cowen lowered the firm's price target on Apollo Global (APO) to $126 from $146 and keeps a Buy rating on the shares. The firm adjusted targets in the asset manager, broker dealers and exchanges group as part of a Q1 preview.

Meta launch of Muse Spark should increase sentiment, says JPMorgan JPMorgan believes Meta Platforms' (META) launch of Muse Spark should provide increased confidence in its scaling trajectory and improve investor sentiment. Expectations for Meta's "path to the frontier became quite low" following the Q4 earnings report and press reports suggesting further model delays, the analyst tells investors in a research note. JPMorgan says the initial Meta Superintelligence Labs model represents the first step in what Meta believes is a predictable and efficient scaling trajectory. The firm keeps an Overweight rating on the shares with a $825 price target.

Long META VS AXP VS PG VS PEP VS

Short WGO VS

BY Doug Kass · Apr 9, 2026, 10:05 AM EDT

Pressing gaming shorts.

Short WYNN S CZR S MGM S

BY Doug Kass · Apr 9, 2026, 9:52 AM EDT

BY Doug Kass · Apr 9, 2026, 9:47 AM EDT

* We unemotionally bought ahead of the ceasefire (at the sound of cannons) and dispassionately sold into the rally yesterday (at the sound of trumpets)

* We believe the stock rally will now stall in the face of multiple concerns — disappointing (relative to consensus) S&P 2026-7 EPS, slowing economic growth and persistent inflation, still elevated P/E multiples, etc. — and that we are likely in a broad trading range with a negative bias over the near term

What follows is a recollection and recap of my tactical approach to the markets leading up to Wednesday's sharp move higher in the averages.

But let's not bury the lede and start with some of the reasons why I sold into Wednesday's rally:

The S&P and Nasdaq indices achieved one of the largest daily price gains on Wednesday.

Why did this happen and how did I respond?

A key feature contributing to the strength of the market was that active managers were defensive/short going into the uncertainty of President Trump's Tuesday night deadline. Offsides (and emotional) investors were forced to scramble in what was the largest short-covering session since "Liberation Day." This likely exaggerated the magnitude of Wednesday's gap higher.

As well (and as I noted earlier this morning in my Daily Diary), equities — which were in a deep oversold throughout the last several weeks — have quickly moved into a deeper overbought at Wednesday's close.

I was laser focused, as noted, on the action of the VIX throughout the afternoon — which failed to penetrate support at around 19.15 — and, instead, throughout the afternoon, rallied from a low of 19.99 to over 21 at the close (it's up to 21.50 in the premarket (h/t Hedgeye).

Despite the cheerleading in the business media and the general view on Fin TV that the worst (of the year's market decline) is over, I sold down my longs (I had concentrated my previous buys in technology and financials — both areas led the Wednesday melt up) and reinitiated a short in the indices during the afternoon.

Over the last 1-2 weeks I bought (unemotionally) at the sound of cannons.

From two days ago:

BY DOUG KASS · Apr 7, 2026, 8:30 AM EDT

My dispassionate approach to President Trump's ultimatum to Iran is that either way the situation will be shortly resolved.

* If Iran doesn't acquiesce, the military move will be devastating to Iran, decisive and likely short-lived.

* If Iran does acquiesce to the president's conditions, the conflict will be over (for now).

Either way I suspect we get a market rally.

However, I would sell into the rally for the reasons I mention in today's opening missive (coming up shortly).

From two weeks ago:

BY DOUG KASS · Mar 27, 2026, 7:15 AM EDT

* I remain of the view that the Iranian conflict is "at the beginning of the end" ... and I am expanding my small net long exposure

It is my core belief that both the U.S. and Iran are aggressively looking for an off ramp to their conflict.

That said, there remains a lot of skepticism, as illustrated by the partial Administration's "TACO" after the close of trading Thursday in which President Trump instituted a lengthier 10-day pause for negotiations — yet stocks only briefly rallied (and, based on stock futures are now modestly lower than Thursday's close).

Despite the market's skepticism, the news yesterday continues to underscore my more constructive comments made earlier this week (excerpted from below):

Both parties, for different reasons, need to come to an agreement.

"Iran has been devastated and is likely defenseless going forward. They will continue to use aggressive rhetoric because that is what regimes that are about to be defeated do.

The Trump Administration doesn't want the conflict to linger. There is an upcoming election in November, oil prices are a regressive tax (hurting those least able to tolerate the increase) and the stock market will likely be imperiled by any further escalation in the conflict. Meanwhile, interest rates and inflationary expectations are rising."

My complete column from Wednesday:

* We are now likely "at the beginning of the end" of the conflict in Iran...

… One can have a broken heart

living in misery.

Two can really ease the pain

like a perfect remedy.

One can be alone in a bar,

like an island he's all alone.

Two can make just any place

seem just like bein' at home.

- Marvin Gaye and Kim Weston, It Takes Two Baby Frankie Gaye And Kim Weston - It Takes Two

Both parties, for different reasons, need to come to an agreement.

Iran has been devastated and is likely defenseless going forward. They will continue to use aggressive rhetoric because that is what regimes that are about to be defeated do.

The Trump Administration doesn't want the conflict to linger. There is an upcoming election in November, oil prices are a regressive tax (hurting those least able to tolerate the increase) and the stock market will likely be imperiled by any further escalation in the conflict. Meanwhile, interest rates and inflationary expectations are rising.

I remain short-term bullish and intermediate-term bearish.

Note: The use of lyrics and the double entendre ("It takes two baby") is not to meant to minimize the horrors of the Iran/U.S. conflict.

BY Doug Kass Mar 25, 2026, 2:25 PM EDT

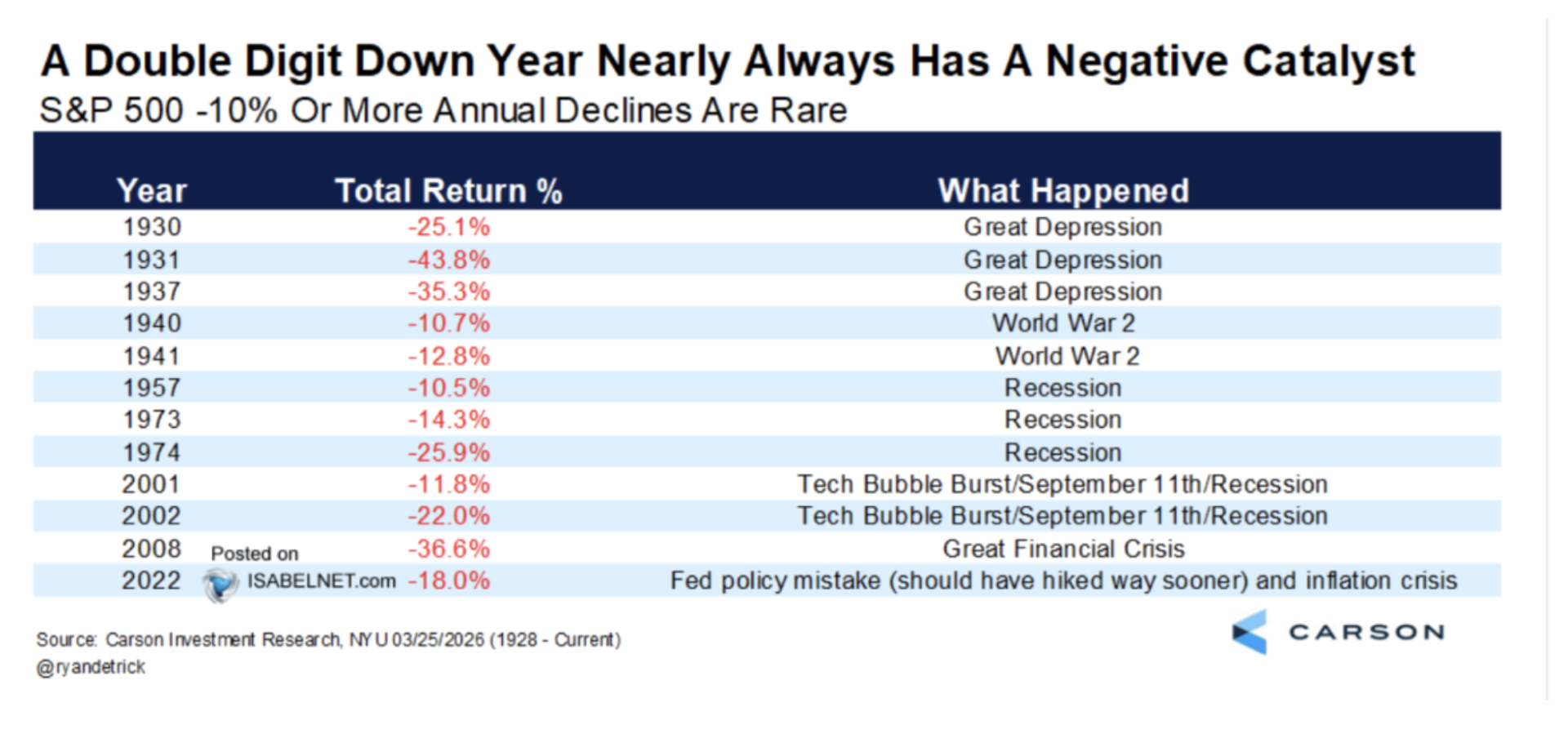

In support of my buying from my column from yesterday "Disasters Have a Way of Not Happening":

Disasters have a way of not happening. (h/t Byron Wien)

There have been only 12 data points in which the S&P Index fell by 10% or more:

For the reasons mentioned in "Growing Less Bearish " I have begun to accumulate equities — after being net short for some time.

Here are some more reasons I have begun to buy:

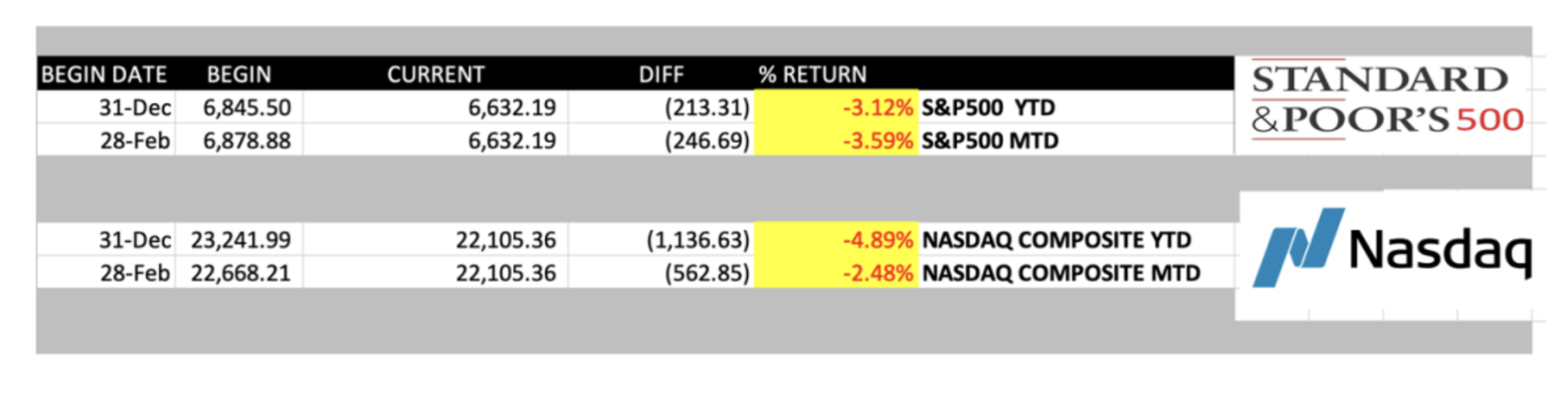

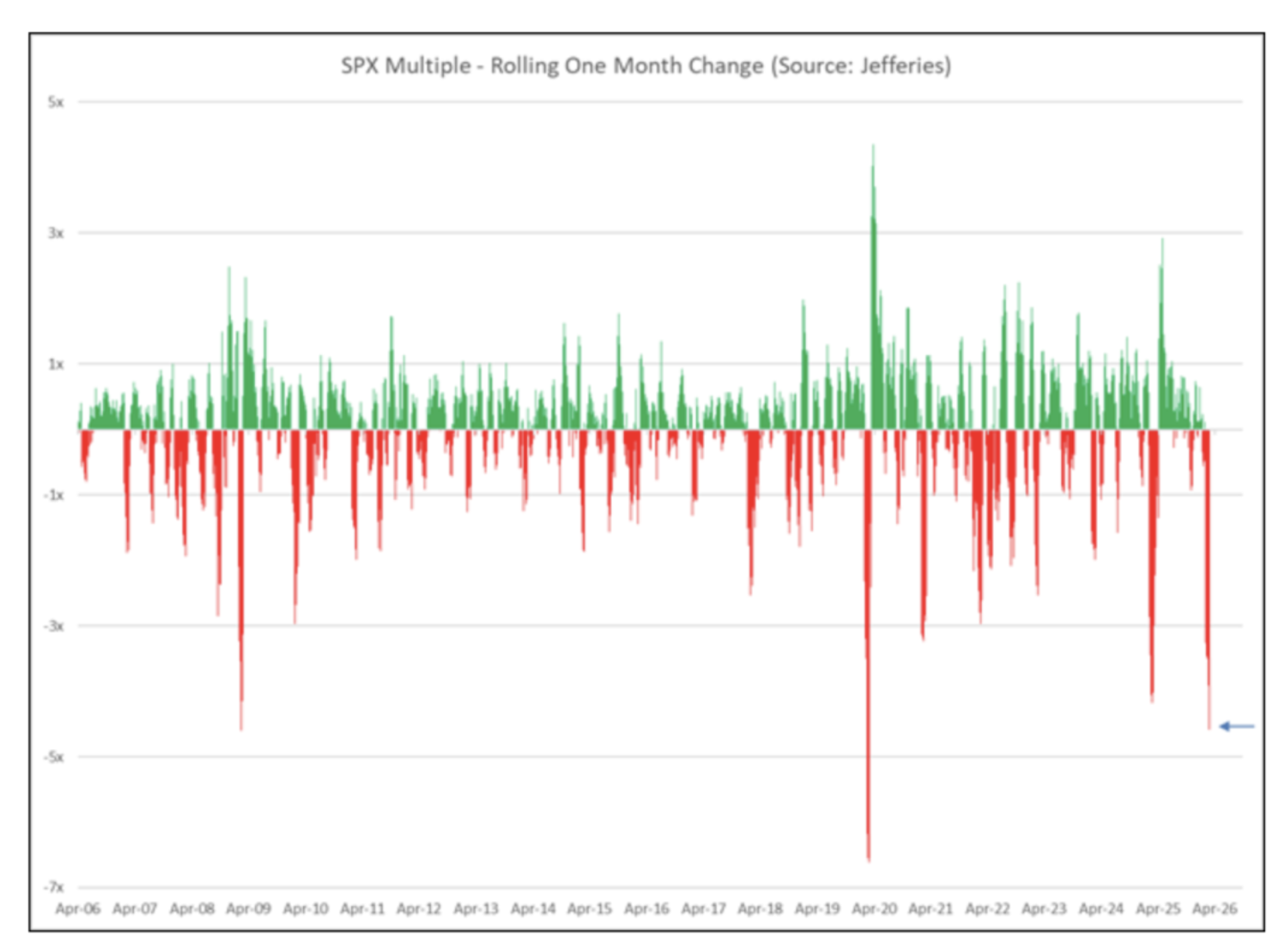

* The compression in valuations has been multiple driven and the swiftness of the drop in price earnings multiples was last seen five years ago during Covid:

* The price earnings ratio of the S&P Index is now one turn under the five-year average:

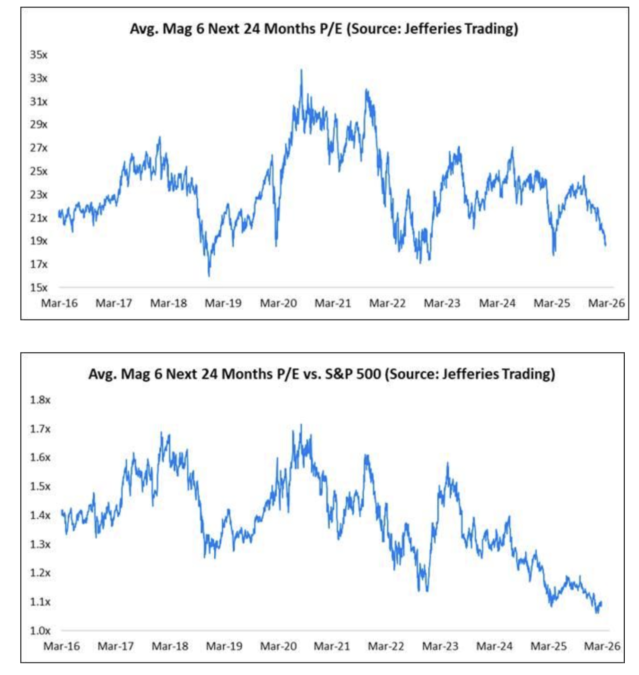

* MAG 7 valuations (excluding Tesla) are down to 19-times vs. 17-times low over the last decade:

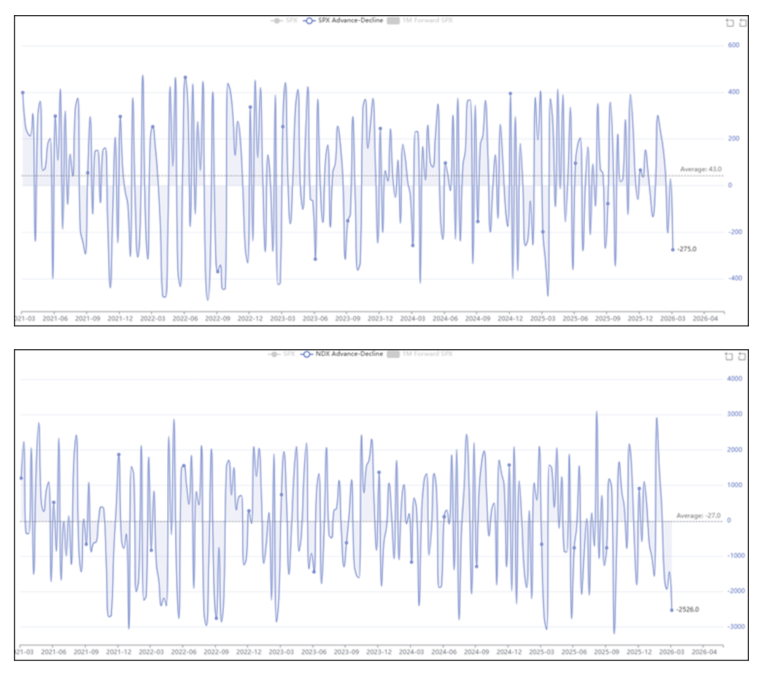

* Sentiment has deteriorated. S&P and Nasdaq advance/decline lines are near five-year lows:

And I sold (dispassionately) Wednesday at the sound of trumpets (the announcement of a temporary ceasefire agreement) — just as I promised in Tuesday's 2026 Looks To Be A Down S&P Year:

BY DOUG KASS · Apr 7, 2026, 9:30 AM EDT

* Though the negatives are accumulating, a few stocks are approaching buyable levels

* "Slugflation" is more likely than ever — with economic growth prospects moderating the pressured part of the K-shaped economy might move into the upper middle class (if equities fall and the negative wealth effect takes hold) just as inflationary pressures are mounting (and the knock-on effect of higher oil prices is felt)

* The equity risk premium has turned into an equity risk discount — portending weak equities ahead

* Improvisational U.S. foreign policy will have a destabilizing impact on our alliances (trade and political)

* For the next few months we see a broadening trading range with a negative bias lower

* But opportunities could emerge in this year's second half, setting up the stage for a good market in 2027

What follows is a compilation of commentary from my Daily Diary on TheStreet Pro and from communications to my hedge fund investors at Seabreeze Partners...

As noted in my commentary of the last few months we have been prepared for the market downdraft by building up our cash reserves.

Many stocks are already down in excess of 25%. As reported in March, we are ready (as individual equities justify purchase) to return to the land of the living and we are open to building up our long exposure.

We expect a very volatile "two-way" market going forward — something we relish as it provides numerous trading and investing opportunities for the opportunistic and dispassionate who have a sense of (intrinsic) value in the averages, in sectors and in individual stocks. This likely market backdrop will be far different than the runaway bull market experienced since late 2022. To quote my Grandma Koufax, a great philosopher, businesswoman and money manager... "the coming market conditions will likely demonstrate the difference (in performance) between 'the men and the boys.'"

Though we still think there is more to go on the downside, selected equities have grown attractive and (as suggested last month) we have moved from a net short exposure to a modest net long exposure in the last two weeks.

Our current gross exposure stands at 80%. Our net exposure (gross longs (45%) less gross shorts (35%)) is about 10% net long. We envision taking our net long exposure higher over the balance of the year.

We remain broadly and conservatively diversified with no individual stock position accounting for more than five percent of our portfolio. Both our longs and shorts generally consist of actively traded (liquid) stocks with large market capitalizations.

Recent new portfolio additions (made in the move lower in the averages) include Fannie Mae (FNMA) , Freddie Mac (FMCC), Meta (META) , Alphabet (GOOGL) , Amazon (AMZN) , Microsoft (MSFT) and Disney (DIS).

While we are of the view that some stocks have reached buyable levels, we are skeptical about the violence of the initial upside move (which was likely exacerbated by short-covering). The breakneck speed in which stocks rose reduced the reward vs. risk opportunities and took away some "margin of safety."

There is still downside risk to economic and corporate profit growth and valuations — and to equity prices.

We will stay patient in building up our long book — waiting for the right pitches.

President Trump's speech last Thursday evening underscored a likely lengthier and drawn-out conflict in Iran (and, with it, heightened and adverse economic ramifications). Indeed, in some ways it bolstered my medium-term economic and investment concerns.

While the war in Iran will eventually will be "resolved," the impact will be to have knock-on consequences to economic growth (weaker), inflation (stronger and more persistent), tighter-than-expected (Fed) monetary policy (so interest rates will be "higher for longer") and produce something of a supply shock (for a vast array of critical materials and products).

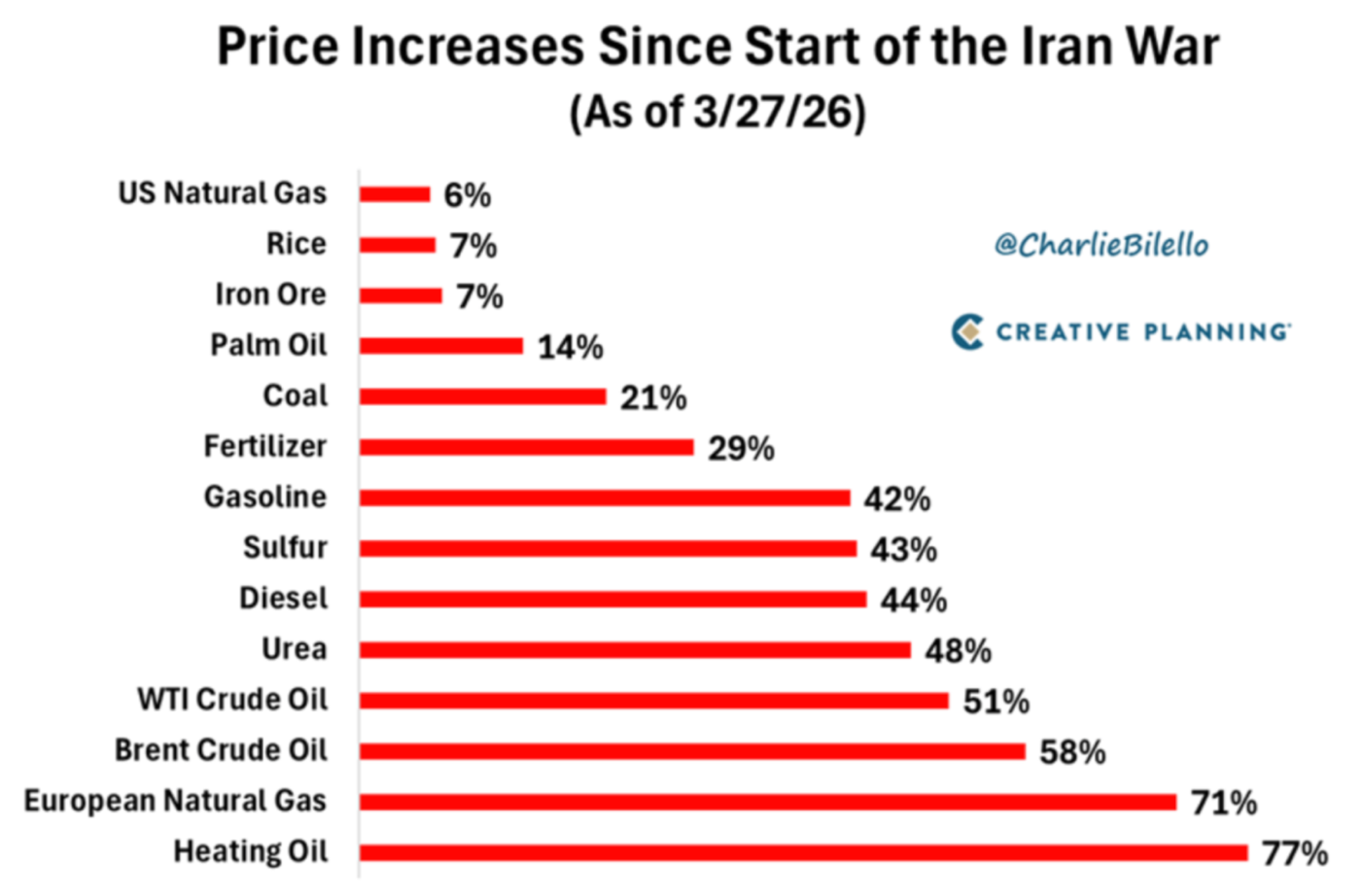

Oil is the spark, but inflation is the fire. And once it spreads, it's much harder to contain:

With inflation already elevated before the Iran conflict, "slugflation" (sluggish economic growth and persistent inflation) is now almost guaranteed to be a semi-permanent condition.

Oil is a tax on consumption and the problem is that we now have to get comfortable with the notion of higher oil prices for longer.

From my pal, the estimable John Mauldin (Thoughts From the Frontline Mauldin Economics - Publisher of Free and Premium Investment Research):

"I have written for years that oil prices act like a tax on the economy, both on the US and globally. It is actually simply the price paid, but the effect on the economy is similar to a tax. If the price goes up, it takes more money from individual consumers that would otherwise be saved or spent somewhere else. Just like taxes.

The growth of the global economy is really the growth in energy and how we use it. When energy become scarce or high-priced it is necessarily going to reduce global GDP. It will reduce GDP much more in some countries than others, depending on their need for both energy and its related products like fertilizers, plastics, and all the things that energy produces.

The Strait of Hormuz is a big deal. About 20% of the world's oil consumption, 20% of LNG and 25% of seaborne oil trade passes through the Strait of Hormuz."

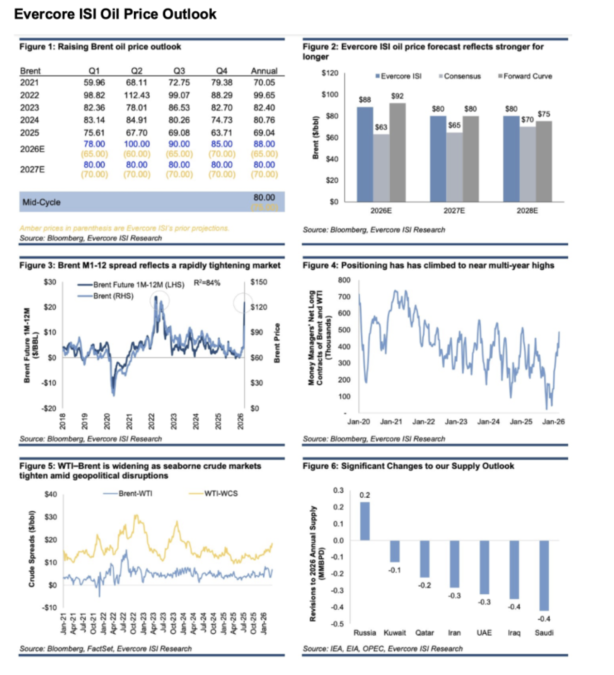

Here is Evercore ISI's oil price forecast:

Since the beginning of the conflict with Iran on February, 28 2026, American drivers have paid an additional $8.4 billion in fuel costs — representing an additional $240 million per day. The average cost of a gallon of gas in the U.S. is now up to $4.10/gallon, the highest since June 2022. This puts the cost of gas up +$1.30/gallon since January 2026.

The bottom and the middle of the K-shaped U.S. economy are bound to be even more pressured in the months ahead as general affordability is materially threatened by a weakening jobs market and stubbornly higher costs (and inflation). Should stocks continue to fall, the negative wealth effect will begin to impact the upper middle class and the rich.

Importantly, consensus corporate profit growth expectations (of about +15% year over year) will likely have to be ratcheted down despite protestations from the cabal of (ostrich-like) perma-bulls.

With interest rates staying above previous expectations and S&P profits below elevated and unrealistic consensus forecasts — the equity risk discount has grown ever deeper — providing a possible backdrop for a future greater-than-expected contraction in valuations.

We continue to remain concerned about the systemic risks associated with the private equity and credit industries. For three years I was a member of the Board of Directors of a business development company listed on the New York Stock exchange where I saw what everyone knows is going on now — that private equity/credit are remarkably proficient at kicking the can down the road (as assets are marked to model and myth but not to reality and market). However, it looks (to me and to others) that the likely the end of the road is near.

I also remain concerned about the destabilizing impact of improvisational U.S. foreign policy and what it means for our alliances (trade and political).

While some stocks have become attractive, the factors listed above are not valuation friendly and, at the very least, will likely constrain the enthusiasm and upside that was demonstrated in the middle of the past week.

As noted earlier, Seabreeze is modestly net long in exposure.

Given the rapidly changing reward vs. risk prospects, which are an outgrowth of a near +4% advance in the broader averages (from recent lows), our investment strategy will be to stay vigilant, flexible and opportunistic.

If forced to make a forecast for the next six months, I would suggest that we are likely in a broadening trading range with a slightly negative bias. This anticipated backdrop will be fertile with both trading and investing opportunities.

Despite the emergence of individual equity opportunities, I continue to see 2026 as a negative year for the broad averages — with most rally attempts failing or being constrained by persistent inflation, moderating corporate profit expectations, relatively tight Fed policy (and higher for longer interest rates), a ballooning U.S. debt load, inconsistent leadership and poorly framed and impromptu policy (without previous thought and analysis) and declining valuations.

Depending on the nature of the emerging economic fundamentals and the direction of stock prices, we might be setting up for an excellent buying opportunity during the second half of this year — setting the stage for a much better stock market in 2027.

***

Position: Short SPY common (S)

BY Doug Kass · Apr 9, 2026, 9:30 AM EDT

-STAA +20% (reports prelim Q1 revenue, color)

-RELL +13% (earnings)

-RGP +9.4% (earnings)

-BB +8.1% (earnings, guidance)

-FBRX +6.6% (prices ~5.7M common shares at $26.27/share)

-GDRX +4.2% (expands access to Eli Lilly's Foundayo and Zepbound)

-PSMT +3.9% (earnings)

-NIO +3.3% (releases photo of new SUV ES9 model)

-INFQ +2.7% (guidance)

-CRWV +2.3% (Meta reportedly commits additional $21B to CoreWeave; files to sell $1.25B of senior unsecured 2031 notes and files to sell $3.0B in convertible senior notes due 2032 with option for additional $450M)

-DDOG +2.2% (Guggenheim Securities Raised DDOG to Buy from Neutral, price target: $175)

-SMPL -23% (earnings, guidance)

-ANVS -17% (prices 5.26M shares at $1.90/shr in ~$10M underwritten offering)

-BYRN -12% (earnings)

-NEOG -9.2% (earnings, guidance)

-ZS -3.3% (BTIG Cuts ZS to Neutral from Buy)

-APLD -2.5% (earnings, color)

-BLSH -2.4% (hearing Rosenblatt Securities Inc. Cuts BLSH to Neutral from Buy, price target: $39)

None.

BY Doug Kass · Apr 9, 2026, 9:11 AM EDT

None.

BY Doug Kass · Apr 9, 2026, 9:02 AM EDT

11:00 a.m.: Treasury Announces a 6 and 13 Week Bill Auction and a 3 and 6 Month Bill Auction;

11:30 a.m.: Treasury hosts an $80 billion 4 and a $75 billion 8 Week Bill Auction;

1:00 p.m.: Treasury hosts a $22 billion 30-Year Bond Auction;

2:00 p.m.: Treasury buyback (liq support)

None.

BY Doug Kass · Apr 9, 2026, 8:35 AM EDT

None.

BY Doug Kass · Apr 9, 2026, 8:26 AM EDT

* As alcohol sales fall, cannabis sales rise...

BY Doug Kass · Apr 9, 2026, 7:03 AM EDT

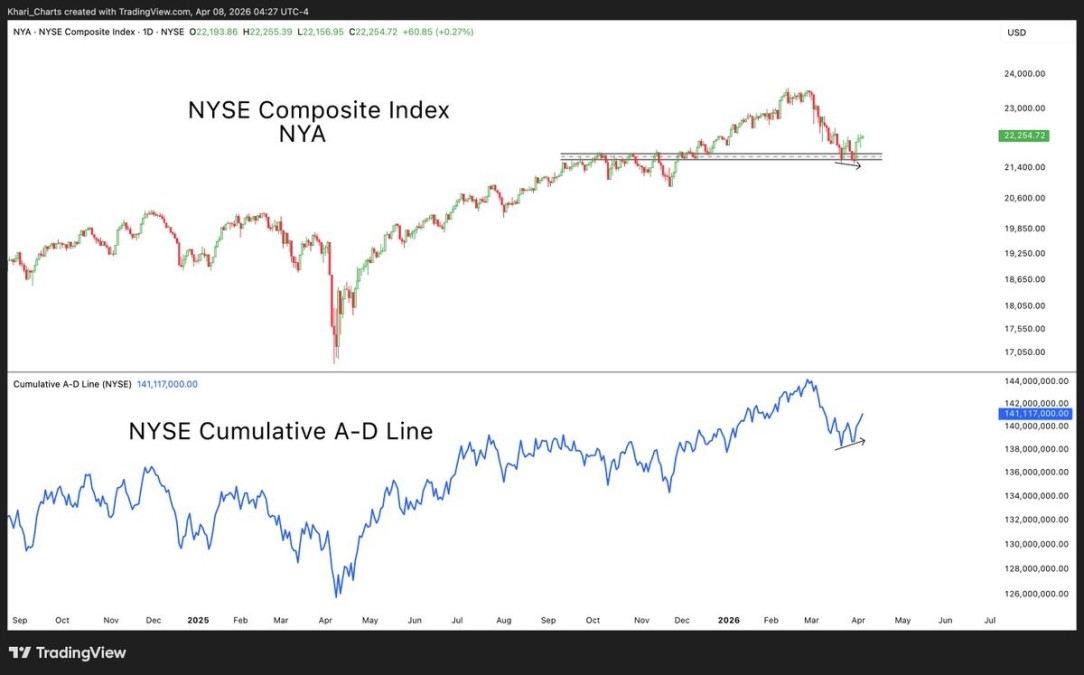

Chart of the Day

The NYSE Composite Index (NYA) registered a strong bullish engulfing candle today, and posted its biggest single-day gain since April 9, 2025.

Importantly, while price made a lower low on Monday, the NYSE Cumulative A-D Line held a higher low, signaling a bullish breadth divergence.

This divergence developed at a key polarity level from the October ’25 highs, which was notably when the Nasdaq topped.

The Takeaway: A textbook breadth divergence and successful polarity flip suggest the NYSE Composite Index may have formed a bottom.

- (4) A.J. Gregor (@KhariCharts) / X

The S&P500 ETF $SPY has gapped up above the 200 day moving average.

— quantdata21 (@bitcoindata21)

The last 2 times this happened, led to multi month rallies, without the gap closing. pic.twitter.com/j4EHswapqO

Today has the *potential* to rank amongst the top 10 largest gap ups we have ever seen in $QQQ. For context, the index would need to open at or above $608.70 to dethrone the #10 spot, which just so happens to be exactly one year ago (4/8/25). pic.twitter.com/upWQIpdN1H

— Gino (@MarginoCall)

$XTL more new highs. Optical remains a leadership group. https://t.co/OXi33SQnN4 pic.twitter.com/XEl6I8a7kS

— Larry Tentarelli, Blue Chip Daily (@bluechipdaily)

Base Metals and Precious Metals are improving while energy is weakening. $CPER $XME $GLD $PPLT $PALL $SLV pic.twitter.com/o43iVQ0fUk

— Jim Knarr (@ChartMonitor)

Got Copper? pic.twitter.com/jbeSFVuWYK

— Patrick Karim (@badcharts1)

Every major relative breakout for Gold is done — except one.

— Jordan Roy-Byrne CMT, MFTA ⛏⛏ (@TheDailyGold)

The last one is setting up: Gold vs. Nasdaq, a 9-year base ready to resolve before 2027. pic.twitter.com/Mpvt2SKpq4

Bonus — Here are some great links:

BY Doug Kass · Apr 9, 2026, 6:35 AM EDT

From Charlie!

BY Doug Kass · Apr 9, 2026, 6:25 AM EDT

* OIH traded higher yesterday despite a -$12 drop in the price of oil — something that was not exactly on investors' bingo cards...

Continuing geopolitical risks, lower crude oil inventories, the peaking of U.S shale production, gas oversupply pushed back by more than one year and continuing rising oil demand (among other factors) suggest that oil prices (as well as inflation) will be higher for longer.

This means we are likely entering an exciting setup for a revival of oil exploration and growth in oil services (after 15 years of pain).

This helps to explain why, despite a -$12/barrel drop in the price of oil yesterday, (OIH) was UP ON THE DAY with a daily gain of +$2.60.share.

This is friendly to oil exploration and services equities, but not necessarily friendly to the general stock market and its valuations.

Position: None

BY Doug Kass · Apr 9, 2026, 6:15 AM EDT

BREAKING: President Trump says "all US ships, aircraft, and military personnel and anything else that is appropriate and necessary for the lethal prosecution and destruction of Iran, will remain in place in, and around, Iran, until such time as the real agreement is reached is… pic.twitter.com/Be3GOVCw5k

— The Kobeissi Letter (@KobeissiLetter)

BY Doug Kass · Apr 9, 2026, 6:05 AM EDT

Reflecting several concerns (discussed shortly) I re-shorted (SPY) after the close.

I wanted to be sure you saw the post in case you left early:

"Just one last thing."

- Lt. Columbo

Near the close I went back short SPY at $675.91.

Position: Short SPY common (S)

BY Doug Kass · Apr 8, 2026, 4:10 PM EDT

Position: Short SPY (S)

BY Doug Kass · Apr 9, 2026, 5:55 AM EDT

The S&P Short Range Oscillator moved deeper into overbought territory at 3.19% vs. 1.05%.

Remember this, I will be going back to the overbought in my discussion of yesterday's massive market gain.

Position: Short SPY common (S)

BY Doug Kass · Apr 9, 2026, 5:46 AM EDT

The embedded tweet could not be found…

The S&P500 ETF $SPY has gapped up above the 200 day moving average. The last 2 times this happened, led to multi month rallies, without the gap closing.

Got Copper?

Fin TV is remarkably simplistic as they (day in and day out) solely, simply and confidentally look at the markets in a linear way. Nearly every discussion in projecting stock prices is the observation of S and P (and sector) estimated EPS change (year over year). I used to Show more

Every major relative breakout for Gold is done — except one. The last one is setting up: Gold vs. Nasdaq, a 9-year base ready to resolve before 2027.

$XTL more new highs. Optical remains a leadership group.

BREAKING: President Trump says "all US ships, aircraft, and military personnel and anything else that is appropriate and necessary for the lethal prosecution and destruction of Iran, will remain in place in, and around, Iran, until such time as the real agreement is reached is Show more