Wednesday's After-Hours Advancers and Decliners

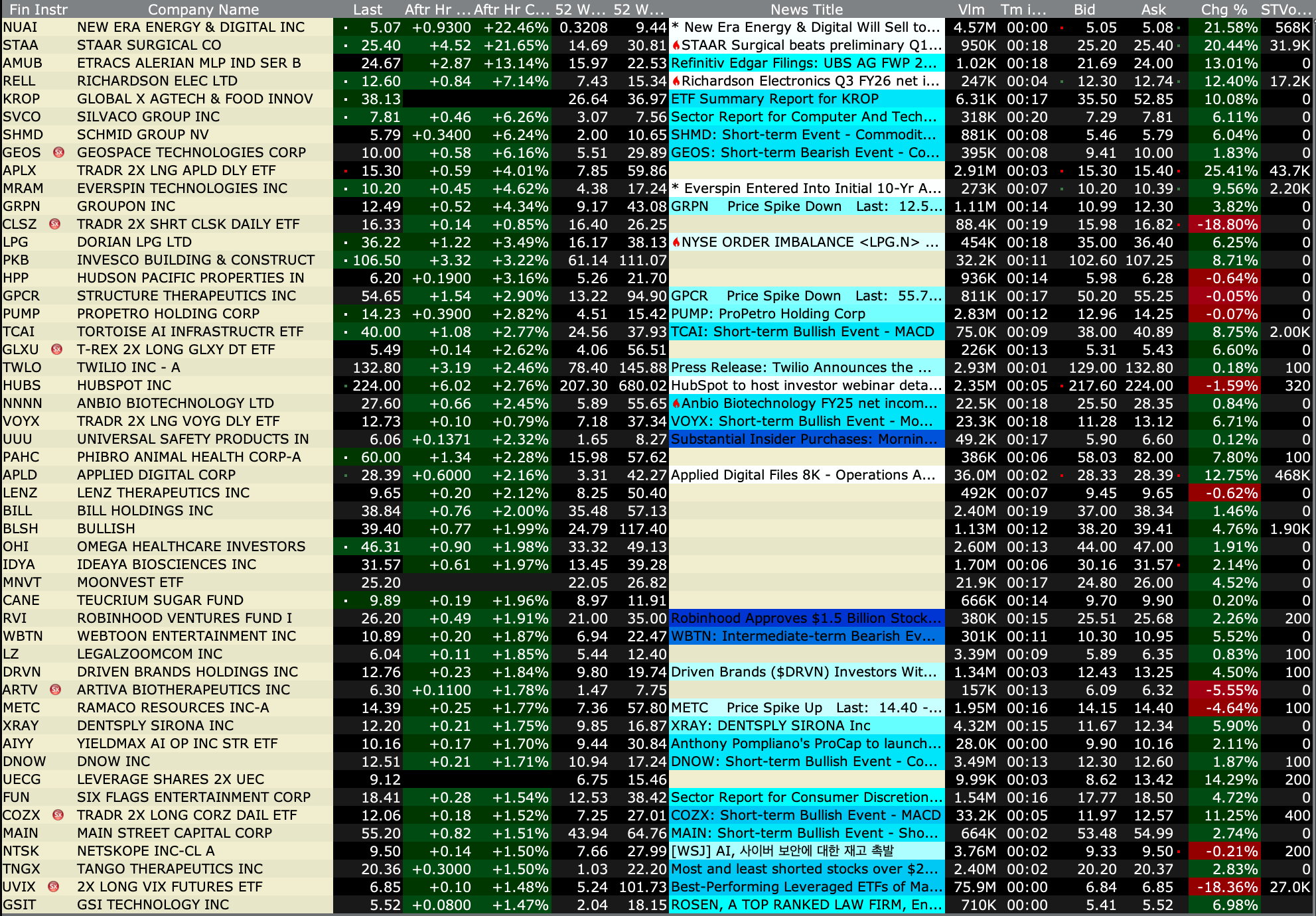

After-Hours % Advancers

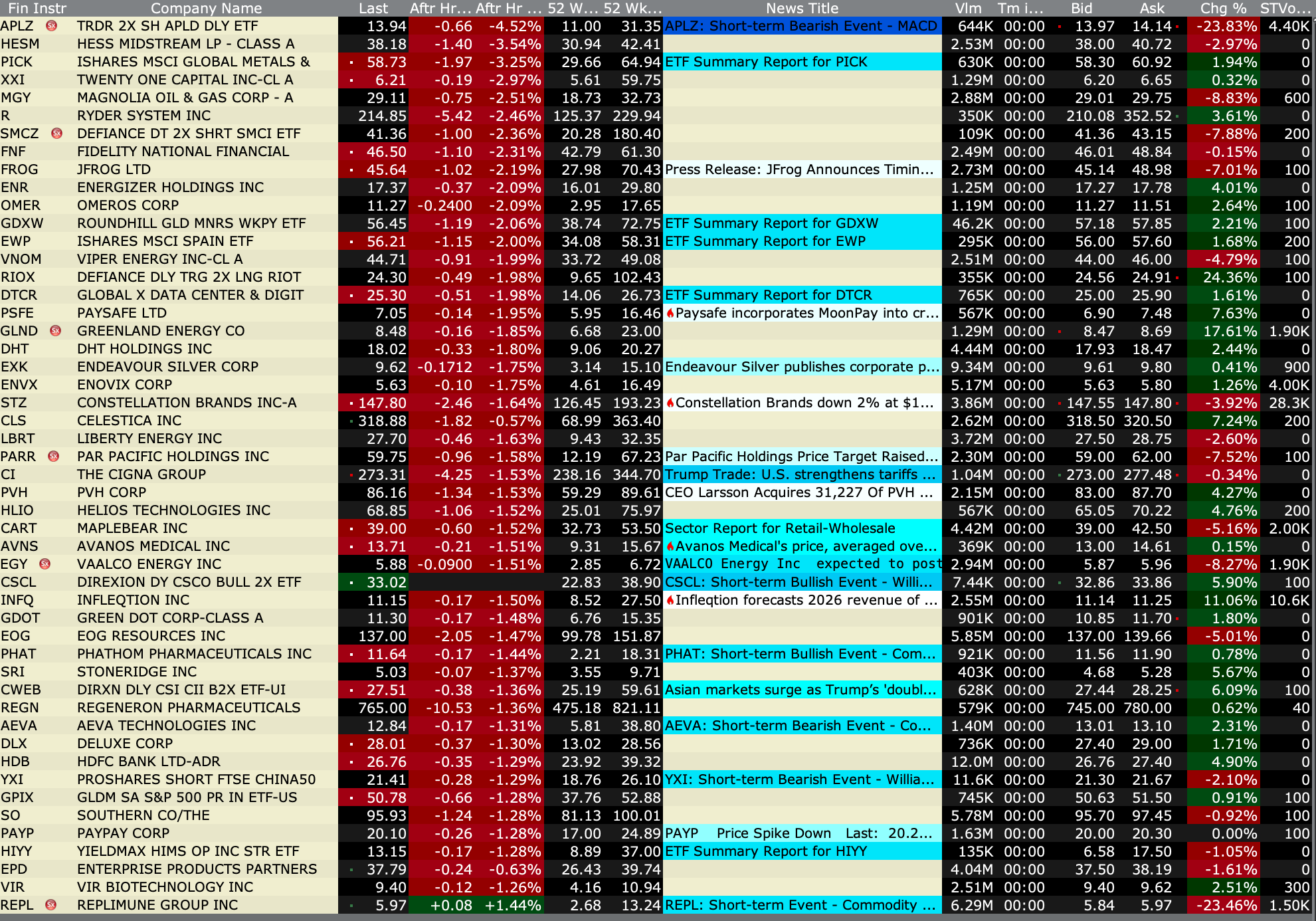

After-Hours % Decliners

BY Doug Kass · Apr 8, 2026, 4:40 PM EDT

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Apr 8, 2026, 4:40 PM EDT

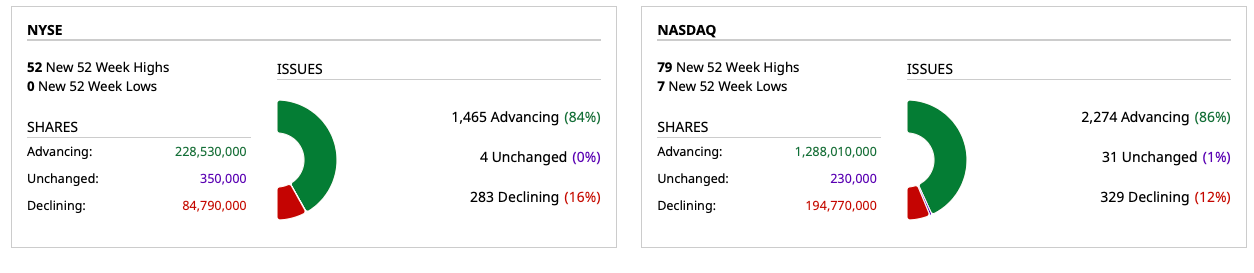

Closing Volume

- NYSE volume 6% above its one-month average

- NASDAQ volume 21% above its one-month average

- VIX index: DOWN 18% to 21.14

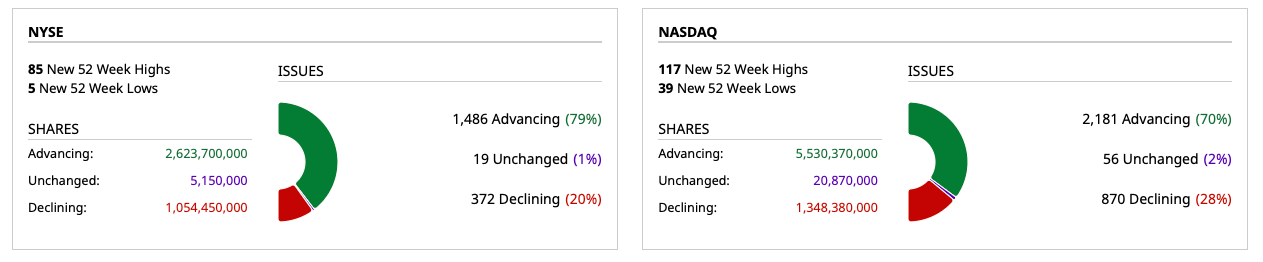

Breadth

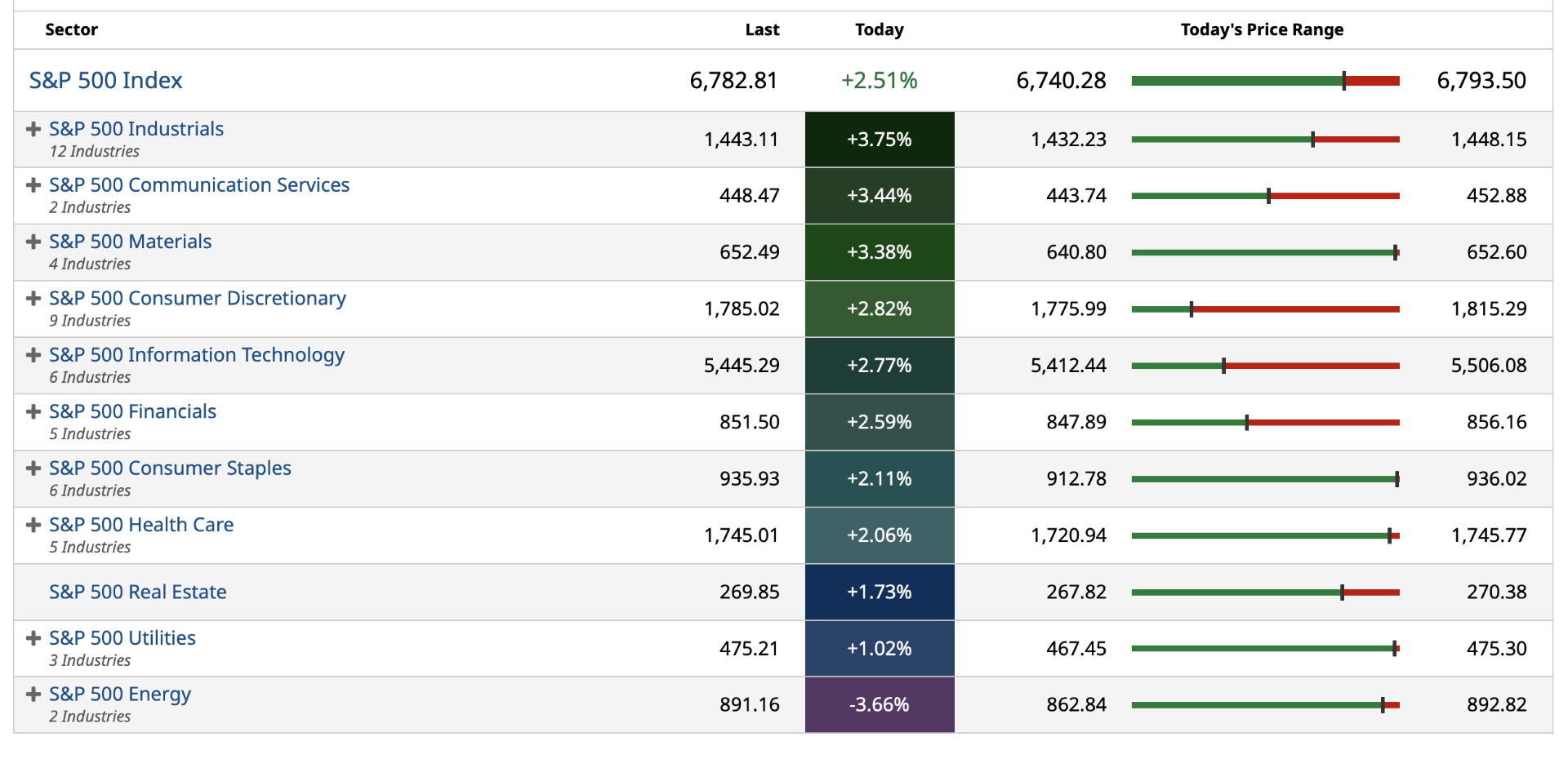

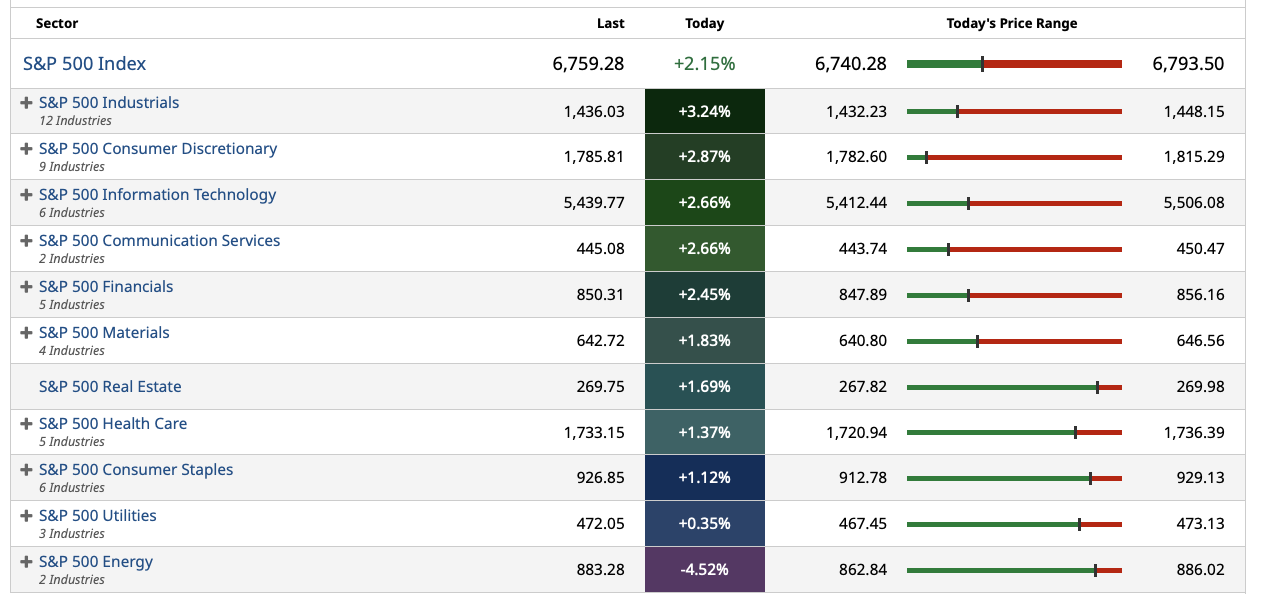

S&P 500 Sectors

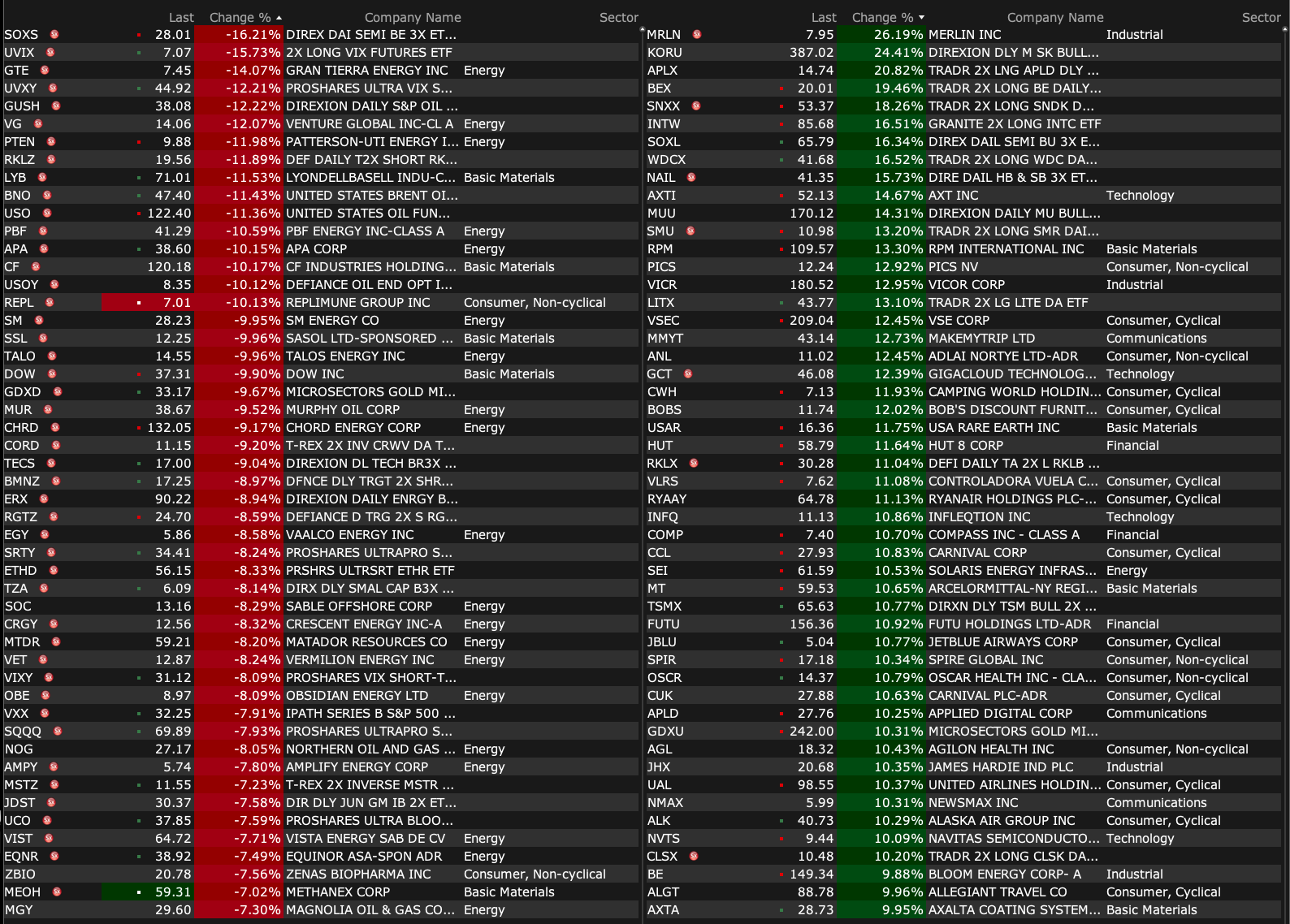

% Movers

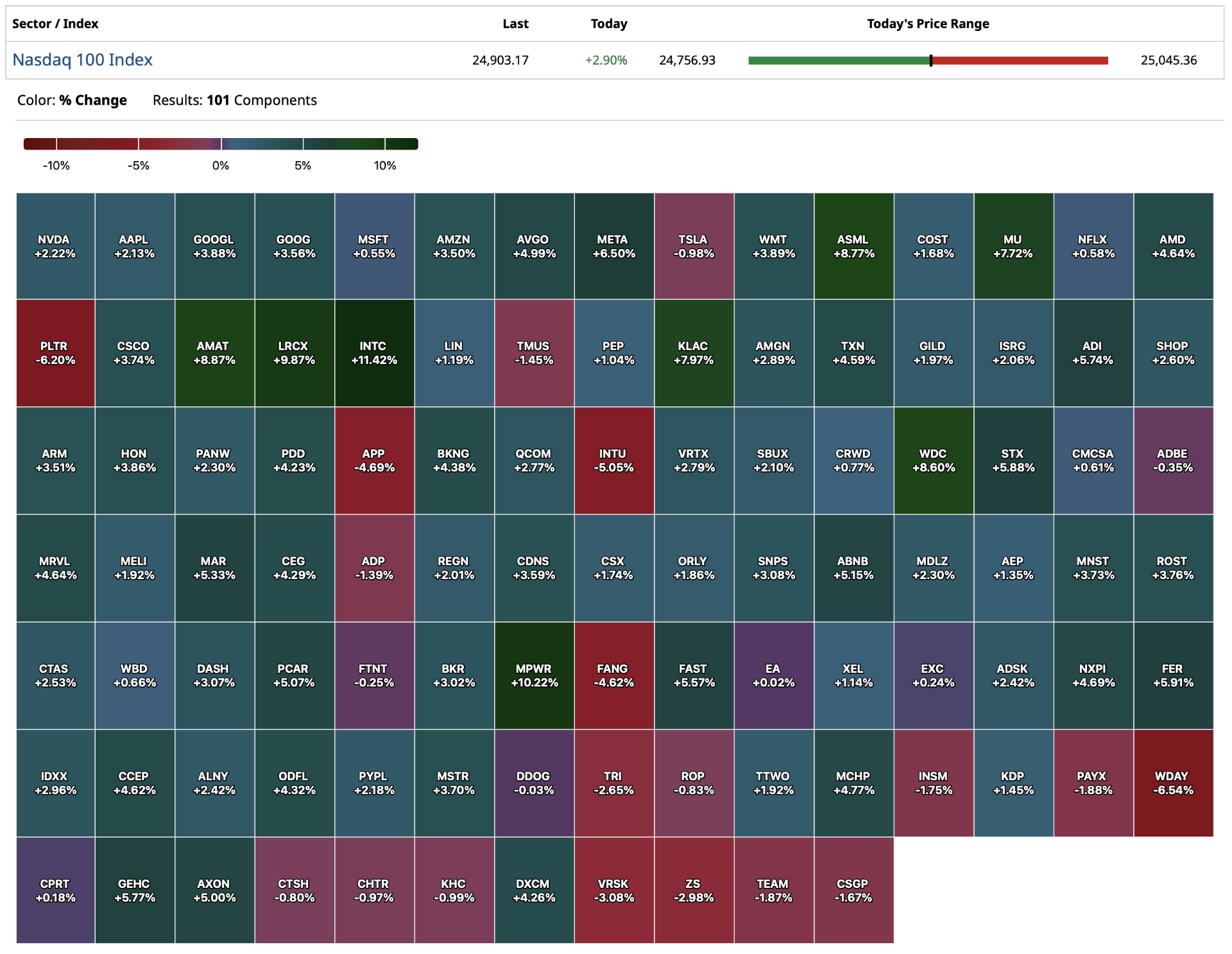

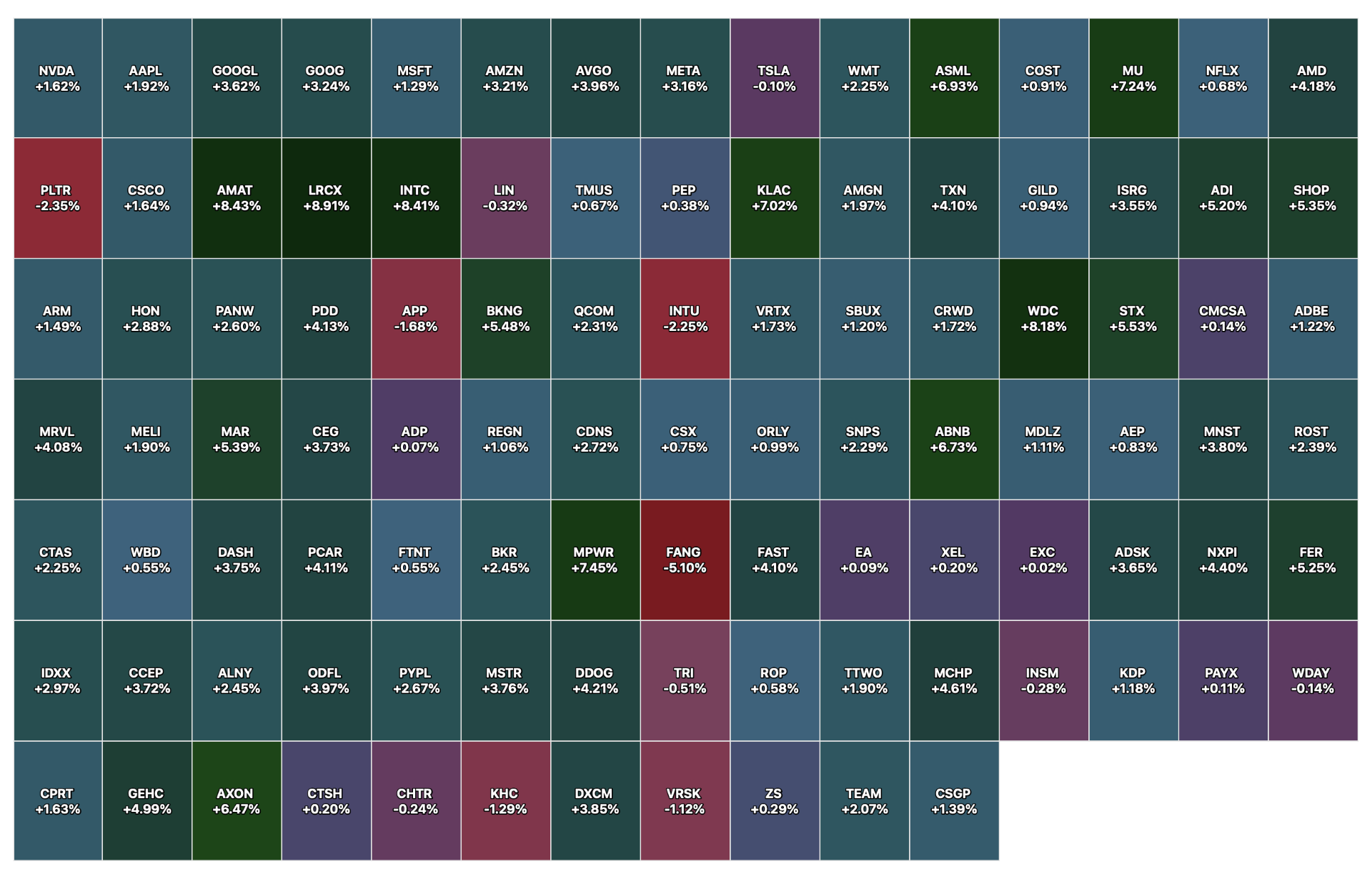

Nasdaq 100 Heat Map

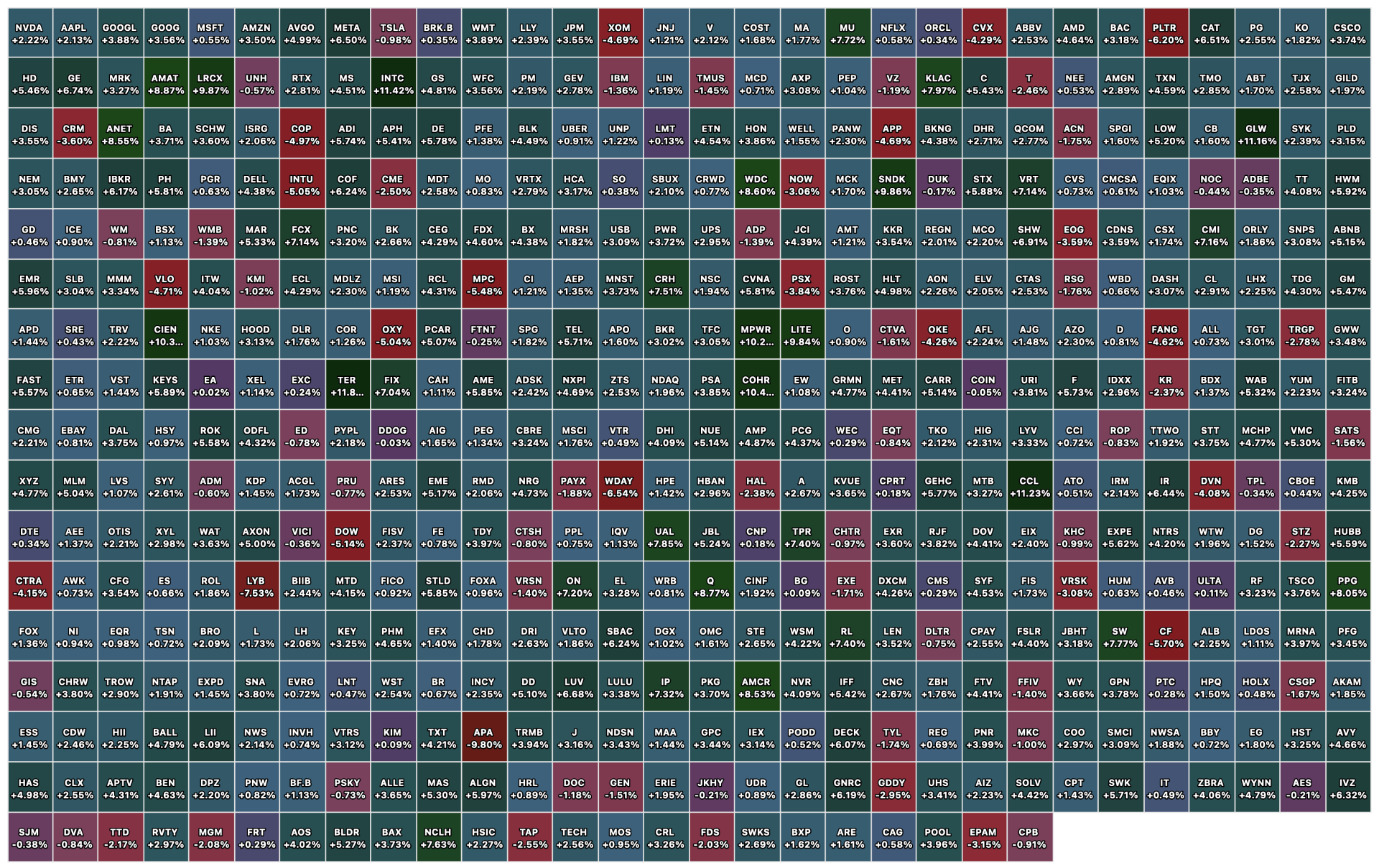

Closing S&P 500 Heat Map

BY Doug Kass · Apr 8, 2026, 4:30 PM EDT

"Just one last thing."

- Lt. Columbo

Near the close I went back short SPY at $675.91

Position: Short SPY common (S)

BY Doug Kass · Apr 8, 2026, 4:10 PM EDT

BREAKING: Iran's Speaker of the Parliament Ghalibaf releases a statement claiming that 3 clauses of their "10 point proposal" have been violated by the US and Israel.

— The Kobeissi Letter (@KobeissiLetter)

Parliament Speaker Ghalibaf says:

1. The first clause of the 10-point proposal has been violated regarding a…

BY Doug Kass · Apr 8, 2026, 3:27 PM EDT

I covered my trading short rental in the indices just now for a small profit:

* (SPY) $673.27

* (QQQ) $603.16

From earlier:

I added to index shorts:

* (SPY) $676.06

* (QQQ) $607.33

I am keying my short entry points on the action of the VIX, which is now at 20.97 +1 from the day's low of 19.99 (and not close to a trend breakdown (which would be bullish) at about 19.15.

Position: Short SPY common (VS), QQQ common (VS)

BY Doug Kass · Apr 8, 2026, 1:28 PM EDT

Position: None

BY Doug Kass · Apr 8, 2026, 3:13 PM EDT

Most always point out the good-performing stocks.

Here are the bad ones:

Salesforce (CRM)

Microsoft (MSFT)

Oracle (ORCL)

Palantir (PLTR)

Snowflake (SNOW)

CrowdStrike (CRWD)

Uber (UBER)

Nike (NKE)

DraftKings (DKNG)

Strategy (MSTR)

Robinhood (HOOD)

Chewy (CHWY)

Howard Hughes (HHH)

Position: Long MSFT (VS)

BY Doug Kass · Apr 8, 2026, 3:03 PM EDT

From Peter Boockvar:

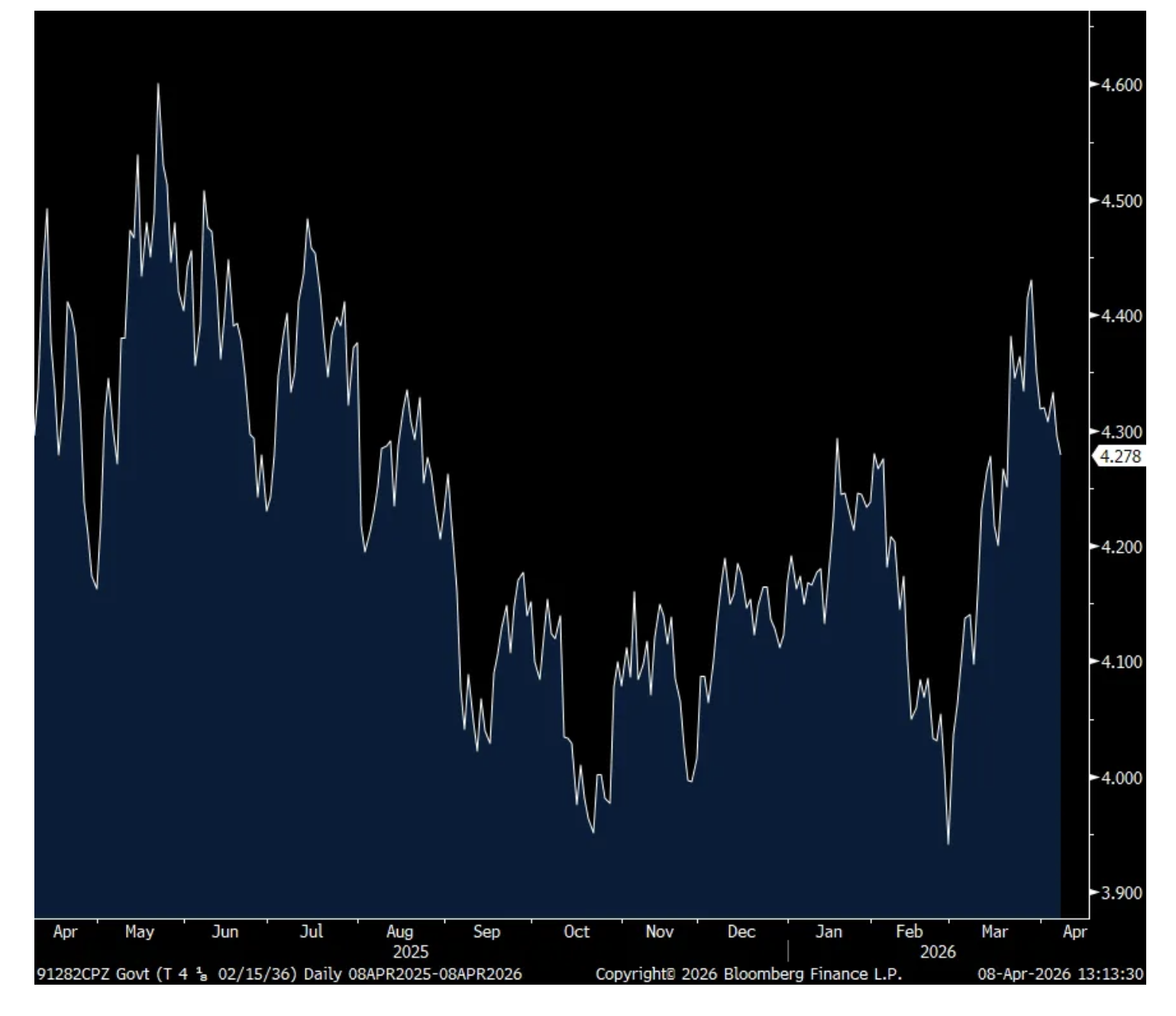

The 10 yr yield is almost back to unchanged on the day at 4.28%, down less than 2 bps on the day after a mediocre 10 yr auction. It was as low at 4.23% earlier today. The yield of 4.282% was about in line with the when issued pricing of 4.28%. The bid to cover of 2.43 was below the one year average of 2.52, and matches the 2nd lowest since last August. And, dealers were left with about 90% of the auction which is exactly the average over the prior 12 months.

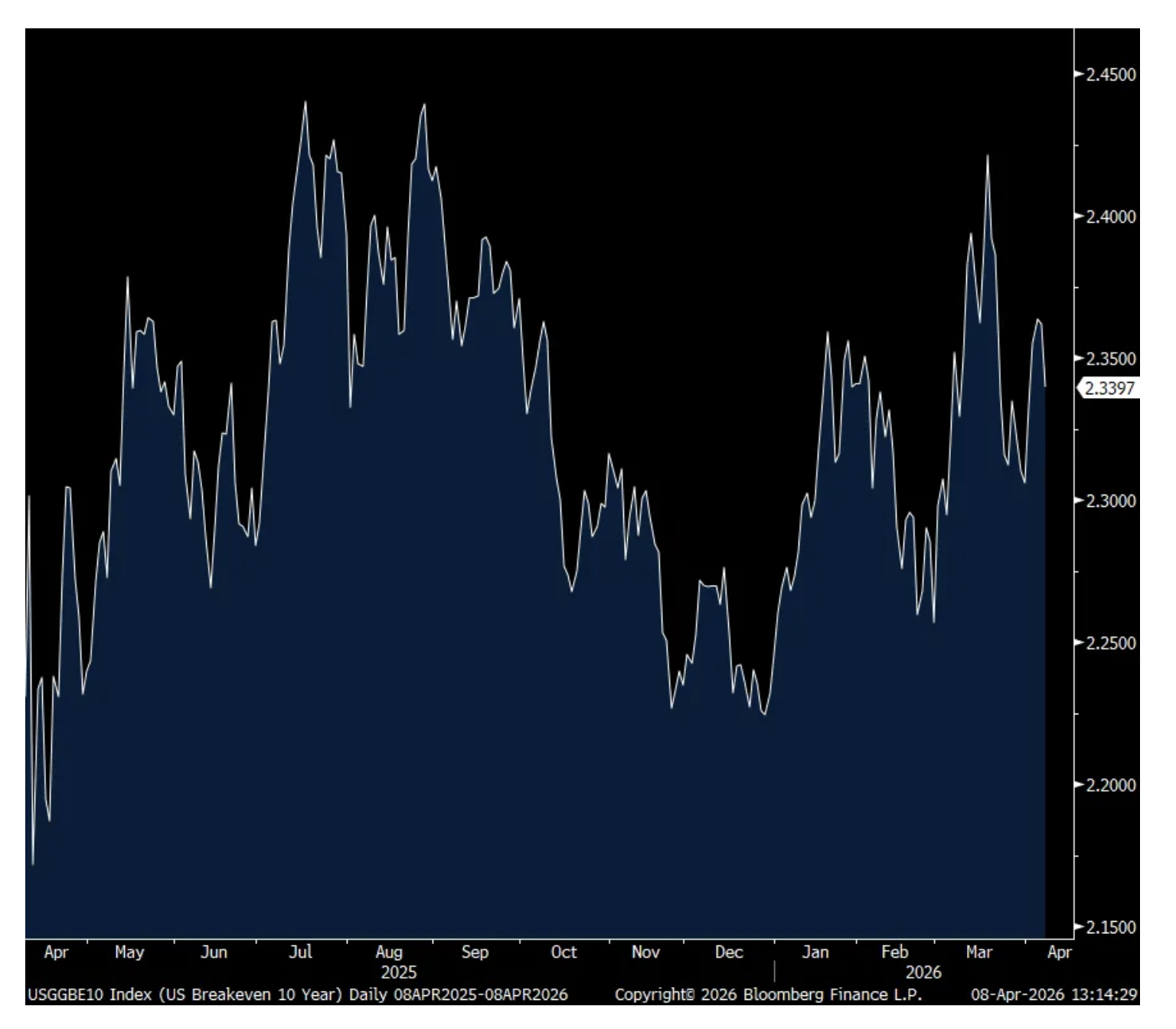

For perspective, the average 10 yr yield over the past year is about 4.22%. Today, the 10 yr inflation breakeven is at 2.34%, down 2 bps and has been much more tame than the shorter term 2 yr breakeven over the past 5 weeks. The 5 yr 5 yr forward inflation breakeven rate has been extremely tame at just 2.16%, pricing in what the market thinks today the average inflation rate will be in year 6 thru 10. This all said, I still think debts and deficits now matter, not just for the US, but for all the overindebted developed countries, and that is flowing through in the demand for long duration bonds.

10 yr Yield

10 yr Inflation Breakeven

BY Doug Kass · Apr 8, 2026, 1:55 PM EDT

I added to index shorts:

* (SPY) $676.06

* (QQQ) $607.33

I am keying my short entry points on the action of the VIX, which is now at 20.97 +1 from the day's low of 19.99 (and not close to a trend breakdown (which would be bullish) at about 19.15.

Position: Short SPY common (VS), QQQ common (VS)

BY Doug Kass · Apr 8, 2026, 1:28 PM EDT

I'm back short the indices/ETFs:

* (SPY) $675.31

* (QQQ) $606.32

* (JOET) $41.72

* (GRNY) $24,87

Peeling off some of the cheap (PG) and (KMB) that I bought in the hole yesterday.

Selling more (META) at $613.28 (+$38) on the "Muse Spark" AI model.

Offering some financials slightly above the market.

Position: Long PEP (VS), KMB (S), BAC (VS), WFC (VS), MS (VS); Short SPY common (VS), QQQ common (VS), GRNY (VS), JOET (VS)

BY Doug Kass · Apr 8, 2026, 12:25 PM EDT

Breadth

Sectors

% Movers

Nasdaq 100 Heat Map

BY Doug Kass · Apr 8, 2026, 12:05 PM EDT

There's battle lines being drawn

Nobody's right if everybody's wrong

Young people speaking their minds

Getting so much resistance from behind

It's time we stop

Hey, what's that sound?

Everybody look, what's going down?

- Buffalo Springfield, For What It's Worth 1967

From Wally:

One of the strongest openings ever and it's only a 78% upside day at 10:30. "There's something happening here; what it is ain't exactly clear..." UVOL/(UVOL+DVOL); Lowry’s definition. Data per https://t.co/iX5L1DJIjD. See https://t.co/7TpOm9eA5A for explanation.

— Walter Deemer (@WalterDeemer)

Children, what's that sound?

Everybody look, what's going down?

BY Doug Kass · Apr 8, 2026, 11:42 AM EDT

I have taken in my index short rentals very early this morning (for a small profit):

* (SPY) $673.60

* (QQQ) $604.85

From earlier:

At around 4:15 AM I am taking a small trading short rental in the indices:

* (SPY) $676.05

* (QQQ) $608.02

Position: Short SPY common (S), QQQ common (S)

BY Doug Kass · Apr 8, 2026, 5:45 AM EDT

None.

BY Doug Kass · Apr 8, 2026, 10:45 AM EDT

From Peter Boockvar:

War trade off, hopefully this time for good and hopefully we see a flood of ships safely traversing thru the Strait in the coming weeks and thereafter upon a complete cessation of kinetic activity. I mentioned on Monday my belief that Iran was basically sowing the seeds of the end of their economic leverage over the Strait and its use as a weapon of mass disruption because every country in the region post war was going to build transportation and logistics infrastructure away from the Strait, just as Saudi Arabia did years ago with its East-West pipeline. Agreeing with me is Badr Jafar, the UAE’s special envoy for business and philanthropy who wrote an Op-Ed in the Financial Times yesterday titled “Future trade won’t depend on the Strait of Hormuz.”

He said while we’re of course all currently focused on the Strait and its effective closure, “inside the region a different story is unfolding – one that will outlast whatever ceasefire or escalation comes next. A 50 year old trade and infrastructure model is being redrawn in weeks.” Realizing how over reliant the region was on the free passage of vital goods, “Those investing in post-Hormuz resilience are constructing the trade infrastructure of the future. Saudi Arabia’s Red Sea ports and expanded pipeline capacity offer an alternative energy corridor. The UAE’s east coast provides deep water ports and pipeline routes connecting Gulf producers to the Indian Ocean. Oman’s developments at Duqm and Sohar sit well outside the chokepoint. Goods and energy are already moving along these routes – in some cases through cross-boarder land bridge arrangements that would have seemed improbable just months ago.”

Some more on this, “The Middle East also holds a largely untapped inheritance: pipeline infrastructure built in previous crises and mothballed for decades, road and rail corridors, cross border electricity grids and water systems that stretch beyond established networks. With renewed cooperation, these assets could deepen regional connectivity to global markets. The crisis is doing what years of summitry could not – creating the conditions for genuine intraregional economic integration. States whose ties were strained only weeks ago are now finding common cause.”

His bottom line, “However the current crisis is resolved, no government will return to a posture of strategic dependence on a narrow strait controlled by an unpredictable neighbor. The pipelines will be expanded. The port capacity will be built. The power grids, water systems and trade corridors connecting the region’s economies will be formalized. The world is watching what is being destroyed. It should pay equal attention to what is being built.” www.ft.com/

I’ll add this again, Iran’s only leg of economic leverage over this region has seen the beginning of the end of it. This will of course take time but the world is not going back to where it was before the war started, in so many other ways too.

Just to highlight how dangerously close the world was on an economic breakdown that was headed big time to the US, Lori Ann Larocco wrote a piece yesterday talking about the shrinking supplies of jet fuel in Europe that was the on cusp of creating a major supply problem for the US. “Europe is a major US air freight exporter to the US grappling with lower jet fuel inventories. US companies are facing a triple whammy of higher air freight costs, diminished belly capacity, and the risk of not receiving critical equipment on time. Airborne components manufactured in Europe are critical to the US economy. Pharmaceuticals, aerospace parts, automotive parts, electronics, high end fashion, advanced machinery, specialized AI/cryptocurrency hardware, and specialized data center and artificial intelligence equipment all move by air.”

“Major airports in Italy have announced fuel restrictions, and airlines in Europe are warning of flight cancellations. All have a direct impact on air freight capacity…Aerospace components, pharmaceuticals, and ‘Made in Italy’ perishables all leave via air freight. Aircraft and helicopter components represent over 60% of Italian aerospace exports to the US.”

So, we’re going to get some well needed commodity inflation relief but I’ll argue again that we’re not going back to $65 oil. We are in a commodity bull market (not withstanding today’s pullback in energy prices) and countries and companies around the world are going to shift to stockpiling mode of all key things. I read today from Nikkei News referring to one anecdote pointing to this, “The Taiwan Semiconductor Industry Association is calling on the government to stockpile strategic raw materials such as helium and liquified natural gas and voicing support for the reopening of nuclear plants amid concerns that conflict in the Middle East could disrupt long term supplies of critical materials and energy.” We’re also long uranium producing stocks.

With respect to other goods price inflation, Manheim yesterday said that its March wholesale used vehicle index rose 6.2% y/o/y and 1.4% m/o/m. They said “As soon as this year began, prices at Manheim started moving higher as dealers anticipated strong demand from higher tax refunds to consumers. Sales conversion rates, a clear sign of demand, were higher against 2025 for every week but one in Q1, and vehicle value trends at auction show we are well ahead of last year and where we would normally be during a spring bounce in the wholesale markets.”

And this, “We thought we’d see some impact from the Middle East conflict, and that may still happen. But right now, the data is clear: used vehicle demand is healthy and inventory levels are relatively tight.”

Delta is jumping, both for the obvious reason of the big drop in jet fuel but also because earnings were pretty good. They said this of note in their earnings release:

“Demand remains strong, and we are taking actions to protect our margins and cash flow. This includes meaningfully reducing capacity growth, with a downward bias until the fuel environment improves, and moving quickly to recapture higher fuel costs.” That likely means higher airline fares

They said they saw “broad demand strength across corporate and leisure” but it still is tilted to the upper end. “Premium revenue grew 14%” y/o/y. Main cabin was up 1%.

Kura Sushi reported better than expected numbers last night. They said:

Comps grew 8.6%, “with 4.3% of positive traffic, and 4.3% of price on the mix.” Out of home food price inflation is still real.

Economic data wise, purchase applications bounced a touch, by 1.1% w/o/w after falling in the two prior weeks with the rise in mortgage rates. Refi’s declined for a 4th straight week.

The Reserve Bank of New Zealand kept its overnight rate unchanged at 2.25% and seem on hold for now.

None.

BY Doug Kass · Apr 8, 2026, 9:30 AM EDT

-BBGI +65% (earnings)

-MTEX +41% (momentum)

-SKIL +26% (earnings, guidance)

-DAL +13% (earnings, guidance; strength following Iran cease fire)

-LAES +11% (reports Q1 revenue, guidance)

-LEVI +11% (earnings, guidance)

-CCL +10% (leisure stock strength following Iran cease fire)

-RPM +10% (earnings, guidance)

-AXTA +9.1% (higher in sympathy with RPM)

-BBBY +8.7% (acquires F9 Brands assets in nearly $150M deal)

-MU +8.5% (invests in SiMa.ai)

-RGTI +7.8% (Cepheus-1-108Q now available)

-U +7.2% (extends multi-year partnership with Meta for VR platform)

-VIK +7.1% (leisure stock strength following Iran cease fire)

-VSAT +7.1% (Barclays Raised VSAT to Equal Weight from Underweight, price target: $49)

-BABA +7.0% (China Commerce Ministry (MOFCOM) issues guide to promoting the development of e-commerce)

-PLUG +6.4% (momentum following Courant deal)

-MPLT +6.2% (Needham Initiates MPLT with Buy, price target: $37)

-WAL +6.0% (bank strength following Iran cease fire)

-FRPT +5.3% (TD Cowen Raised FRPT to Buy from Hold, price target: $80)

-META +5.1% (reaches collaboration agreement with Unity Software)

-COIN +4.7% (wins Australian derivatives license)

-GM +3.8% (strength following report of two-week pause on Iran strikes per President Trump)

-ANIP +3.6% (FDA approved and launched Isosorbide Mononitrate Tablet USP, 10 mg and 20 mg)

-GEHC +3.3% (reiterated as a Buy at Stifel)

-DOW -10% (chemical, materials weakness following Iran cease fire)

-MUR -8.0% (energy equity weakness following Iran cease fire)

-XOM -5.6% (guidance; energy equity weakness following Iran cease fire)

-OKE -5.5% (energy equity weakness following Iran cease fire)

-ADM -5.1% (downside momentum)

-CVX -5.0% (energy equity weakness following Iran cease fire)

None.

BY Doug Kass · Apr 8, 2026, 9:18 AM EDT

On this morning's premarket surge higher (+175 S&P handles) I am taking down (AMZN) (+$9), (GOOGL) (+$12.50), (MSFT) (+$11.65) and (META) (+$29.45) to very small-sized.

Long AMZN VS GOOGL VS MSFT VS META VS

BY Doug Kass · Apr 8, 2026, 9:05 AM EDT

From JPMorgan:

US: Futs are higher on the ceasefire agreement which has triggered a global risk-on rally. Look for a re-risking in the very near-term albeit it with higher energy prices. Pre-mkt, bond yields are down 3-7bp as the yield curve bull steepens, USD depreciates, and cmdtys decline as energy sees double-digit declines. In Eqys, Mag7 and Semis seeing significant bids as part of an ‘Everything Rally’ ex-Energy. The macro data focus today is on the Fed Minutes ahead of PCE and CPI releases later this week.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

We are moving back to Tactically Bullish. This ceasefire should trigger a re-risking potentially similar to the post-Liberation Day pivot. How far could this go? SPX futures are trading ~6810, so breaching 7k feels likely as euphoria returns to markets. A positive earnings season (previewed below) is likely to help boost Equities further especially given the decline in Tech valuation over the course of the conflict. We reposted the most recent Positioning Intel note. The keys are that Iran is opening SoH and that both sides can extend the ceasefire after two-weeks. Assuming that this is not a feint from any of the parties, the market is likely to treat this as a de facto end of the conflict despite the economic damage that is still coming across all regions. Normalization of SoH throughput will matter to Energy markets and ultimately inflation; further, there may be a residual geopolitical / re-escalation risk premium that keeps oil prices elevated over the near-term. Longer-term, energy shocks tend to boost inflation, negatively impacting consumer; but, this will take time to play out in the data so keep an eye on jobs and spending data as well as incremental fundamental improvements that support a sustainable move above 7k in the SPX.

None.

BY Doug Kass · Apr 8, 2026, 9:00 AM EDT

None.

BY Doug Kass · Apr 8, 2026, 8:50 AM EDT

None.

BY Doug Kass · Apr 8, 2026, 8:35 AM EDT

11:00 a.m.: Treasury buyback announcement (liq support);

11:30 a.m.: Treasury hosts a $69B17-Week Bill Auction;

1:00 p.m.: Treasury hosts a $39B10-Year Note Auction

1:05 p.m.: Fed Bank of San Francisco President Daly (Non-Voter) gives keynote speech and participates in moderated conversation on the economy and monetary policy before event hosted by the St. George Area Chamber of Commerce, St. George, UT (Embargoed text available. No group media interview. Livestream at frbsf.org);

2:35 p.m.: Fed Board Governor Waller (Voter) speaks on "Reflecting on Time at Bemidji State University and Early Career" before the Bemidji State University 27th AnnualStudent Achievement Conference (Bemidji, MN (No text. No Q&A. No webcast)

None.

BY Doug Kass · Apr 8, 2026, 8:25 AM EDT

BREAKING: President Trump says Iran will have “no enrichment of Uranium” and the US will be working with Iran to “dip up and remove” all of Iran’s “nuclear dust.”

— The Kobeissi Letter (@KobeissiLetter)

Trump also says the US is discussing tariff and sanction relief with Iran. pic.twitter.com/kuHMNoAciC

BY Doug Kass · Apr 8, 2026, 8:05 AM EDT

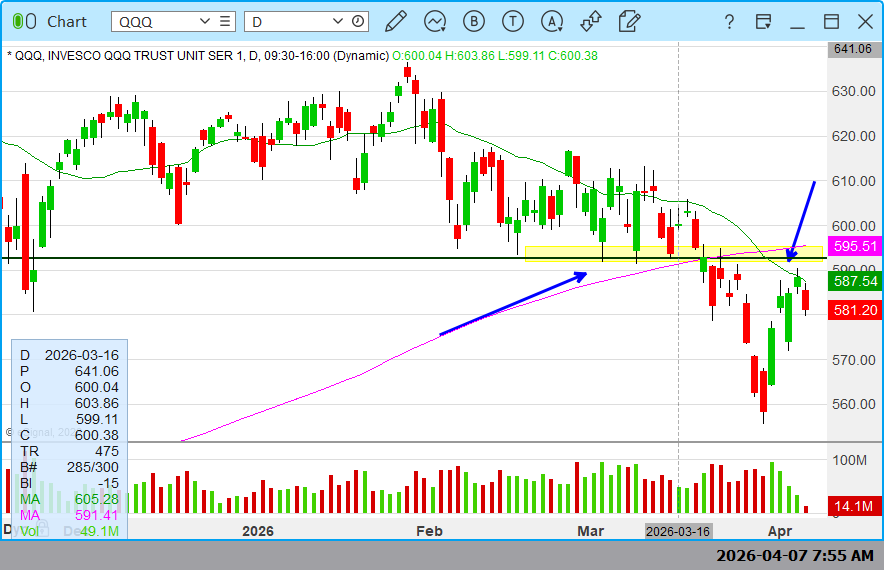

Chart of the Day: QQQ

The Nasdaq 100 finished relatively flat on the day (+0.02) after being down over -1% during intra-day trading, and posted its fifth consecutive up day on declining volume.

Price found resistance around 590, a level of former support now reinforced by a downward sloping 20-day moving average.

From here, bulls need to absorb near-term selling and carve out a reversal pattern, while bears are looking for a decisive flush with expanding volume.

The Takeaway: The Nasdaq staged a significant intra-day reversal and closed higher for a fifth consecutive session as bears couldn’t maintain selling pressure.

This is interesting…

— YCharts (@ycharts)

The S&P 500 is down -4.33% to start 2026, but strip out the Mag 7 and the rest of the index is only down -1.02% 👀

Meanwhile, the Magnificent Seven stocks have dropped -10.62% 📉

In other words, most stocks aren’t doing nearly as bad as the headline index… https://t.co/ICDG7Izf5A pic.twitter.com/gppdB5mLf4

Just bought some $AAPL. Nice risk-reward here. pic.twitter.com/YRQLh08ysF

— Amanda Zmolek (@AmandaZmolek)

$MOO Agribusiness ETF is looking perky pic.twitter.com/Y75PdI7WdU

— Jack (@alphacharts365)

This week brings the first inflation report reflecting surge in oil prices since the start of the U.S. – Iran conflict.

— Bluekurtic Market Insights (@Bluekurtic)

Forecasts point to a 1% MoM increase, which would be the highest since June 2022.

Major oil supply shocks have always pushed the inflation higher. pic.twitter.com/de5VIndJMu

It’s not getting much press but #gasoline prices yesterday surpassed 2004’s peak to become the highest non-pandemic related gas price in AAA’s history. pic.twitter.com/vAc8YU9Ufa

— Richard Bernstein Advisors (@RBAdvisors)

I remain unimpressed with #Bitcoin

— Brian Shannon, CMT (@alphatrends)

It is a choppy consolidation in an overall downtrend

Comments open, tell me how its going to a million 🤣

block button ready! pic.twitter.com/5O7DKd3Rgi

2) Daily structure is tight:

— ₿IRB (@crypto_birb)

- Below 200D MA (~$95,200) and 50D MA (~$88,900)

- Higher lows forming from the ~$60K base

- Resistance: $74K-$76K

- Support: $65K-$67K

- RSI mid-range (45-50)

- PPO improving toward neutral

No visible confirmed reversal signs but big move ahead. pic.twitter.com/UwleTGIm64

Bonus — Here is a great link:

BY Doug Kass · Apr 8, 2026, 7:45 AM EDT

The S&P Short Range Oscillator slid towards neutral, standing at 1.06% vs. 2.29%.

Position: Short SPY common (S), QQQ common (S)

BY Doug Kass · Apr 8, 2026, 6:05 AM EDT

#Iran War Update No. 39 (focus on Iranian strategic narrative):

— Hamidreza Azizi (@HamidRezaAz)

🔹As Trump’s 8 p.m. EDT deadline approaches, Day 39 of the war is marked by a combination of maximal coercion and active mediation. Pakistan is publicly seeking a two-week extension, a temporary ceasefire, and the…

BY Doug Kass · Apr 8, 2026, 5:55 AM EDT

At around 4:15 AM I am taking a small trading short rental in the indices:

* (SPY) $676.05

* (QQQ) $608.02

Position: Short SPY common (S), QQQ common (S)

BY Doug Kass · Apr 8, 2026, 5:45 AM EDT

I remain unimpressed with #Bitcoin It is a choppy consolidation in an overall downtrend Comments open, tell me how its going to a million 🤣 block button ready!

It’s not getting much press but #gasoline prices yesterday surpassed 2004’s peak to become the highest non-pandemic related gas price in AAA’s history.

One of the strongest openings ever and it's only a 78% upside day at 10:30. "There's something happening here; what it is ain't exactly clear..." UVOL/(UVOL+DVOL); Lowry’s definition. Data per wsj.com. See cmtassociation.org/wp-content/upl…

2) Daily structure is tight: - Below 200D MA (~$95,200) and 50D MA (~$88,900) - Higher lows forming from the ~$60K base - Resistance: $74K-$76K - Support: $65K-$67K - RSI mid-range (45-50) - PPO improving toward neutral No visible confirmed reversal signs but big move ahead.

BREAKING: Iran's Speaker of the Parliament Ghalibaf releases a statement claiming that 3 clauses of their "10 point proposal" have been violated by the US and Israel. Parliament Speaker Ghalibaf says: 1. The first clause of the 10-point proposal has been violated regarding a Show more

BREAKING: President Trump says Iran will have “no enrichment of Uranium” and the US will be working with Iran to “dip up and remove” all of Iran’s “nuclear dust.” Trump also says the US is discussing tariff and sanction relief with Iran.

$MOO Agribusiness ETF is looking perky

Just bought some $AAPL. Nice risk-reward here.

This week brings the first inflation report reflecting surge in oil prices since the start of the U.S. – Iran conflict. Forecasts point to a 1% MoM increase, which would be the highest since June 2022. Major oil supply shocks have always pushed the inflation higher.

This is interesting… The S&P 500 is down -4.33% to start 2026, but strip out the Mag 7 and the rest of the index is only down -1.02% 👀 Meanwhile, the Magnificent Seven stocks have dropped -10.62% 📉 In other words, most stocks aren’t doing nearly as bad as the headline index Show more

The S&P 500 has gained over $2 trillion in market cap over the last 5 days 📈 🟢 Nasdaq +4.77% 🟢 S&P 500 +3.59% 🟢 Dow Jones +3.08%