Monday's After-Hours Advancers and Decliners

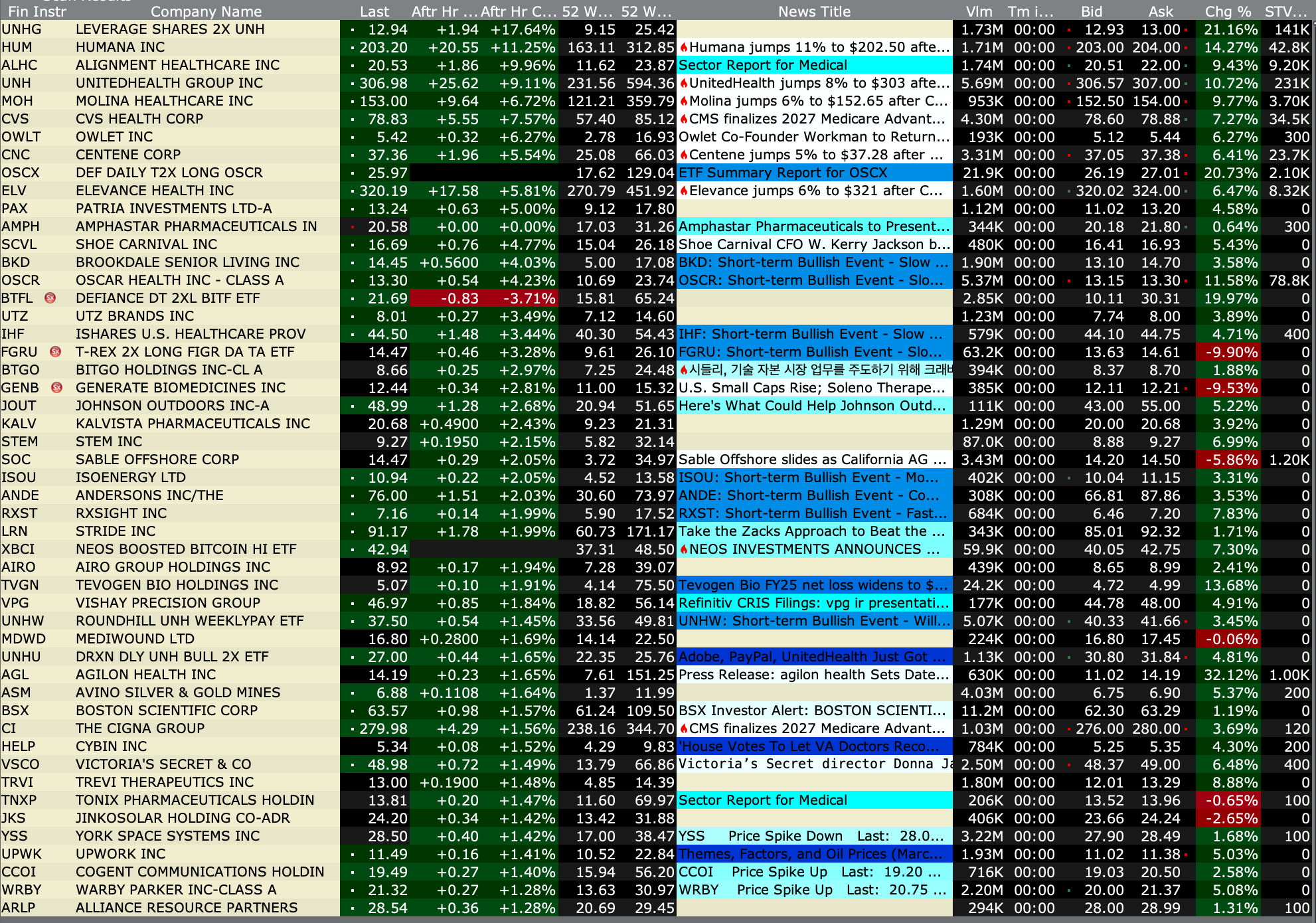

After-Hours % Advancers

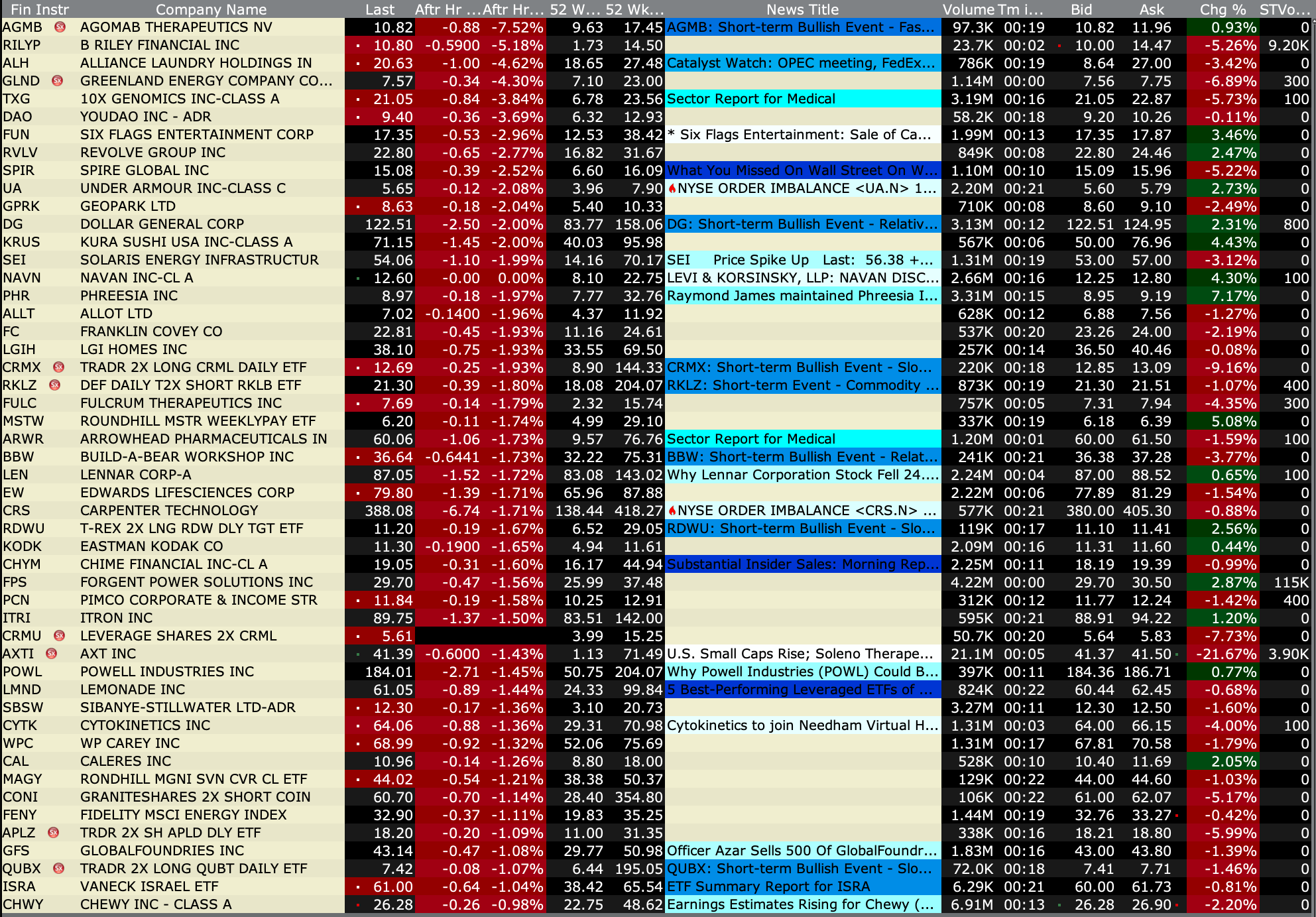

After-Hours % Decliners

BY Doug Kass · Apr 6, 2026, 4:55 PM EDT

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Apr 6, 2026, 4:55 PM EDT

Closing Volume

- NYSE volume 34% below its one-month average

- NASDAQ volume 10% below its one-month average

- VIX index: up 1.21% to 24.16

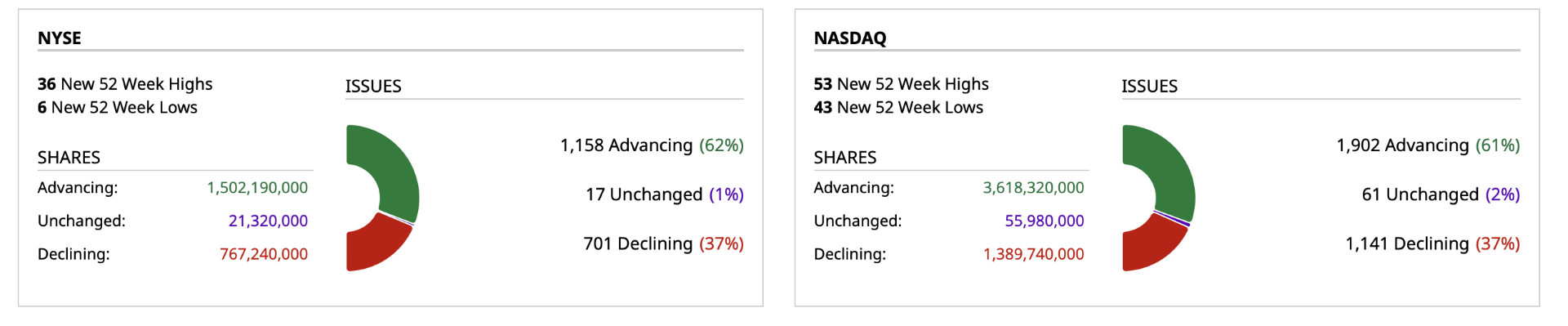

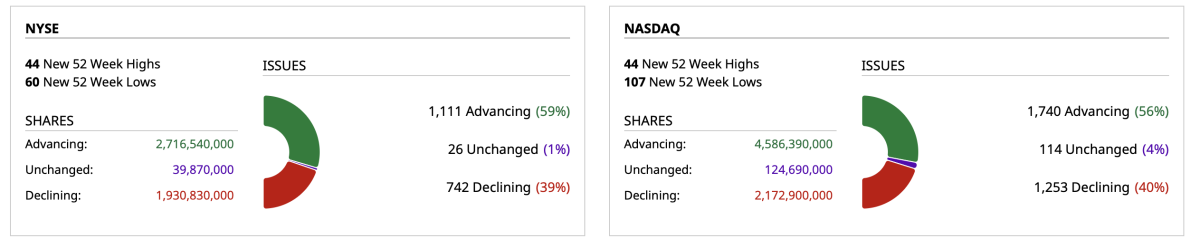

Breadth

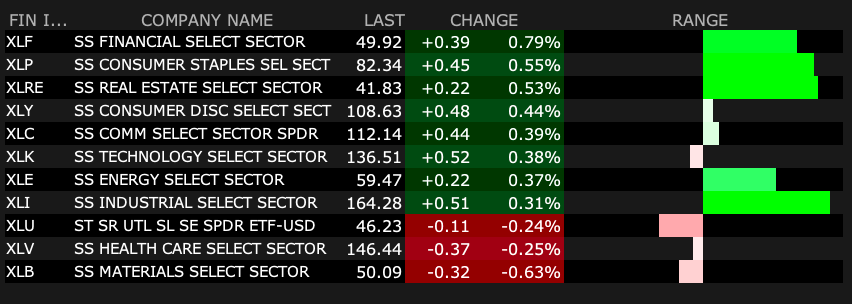

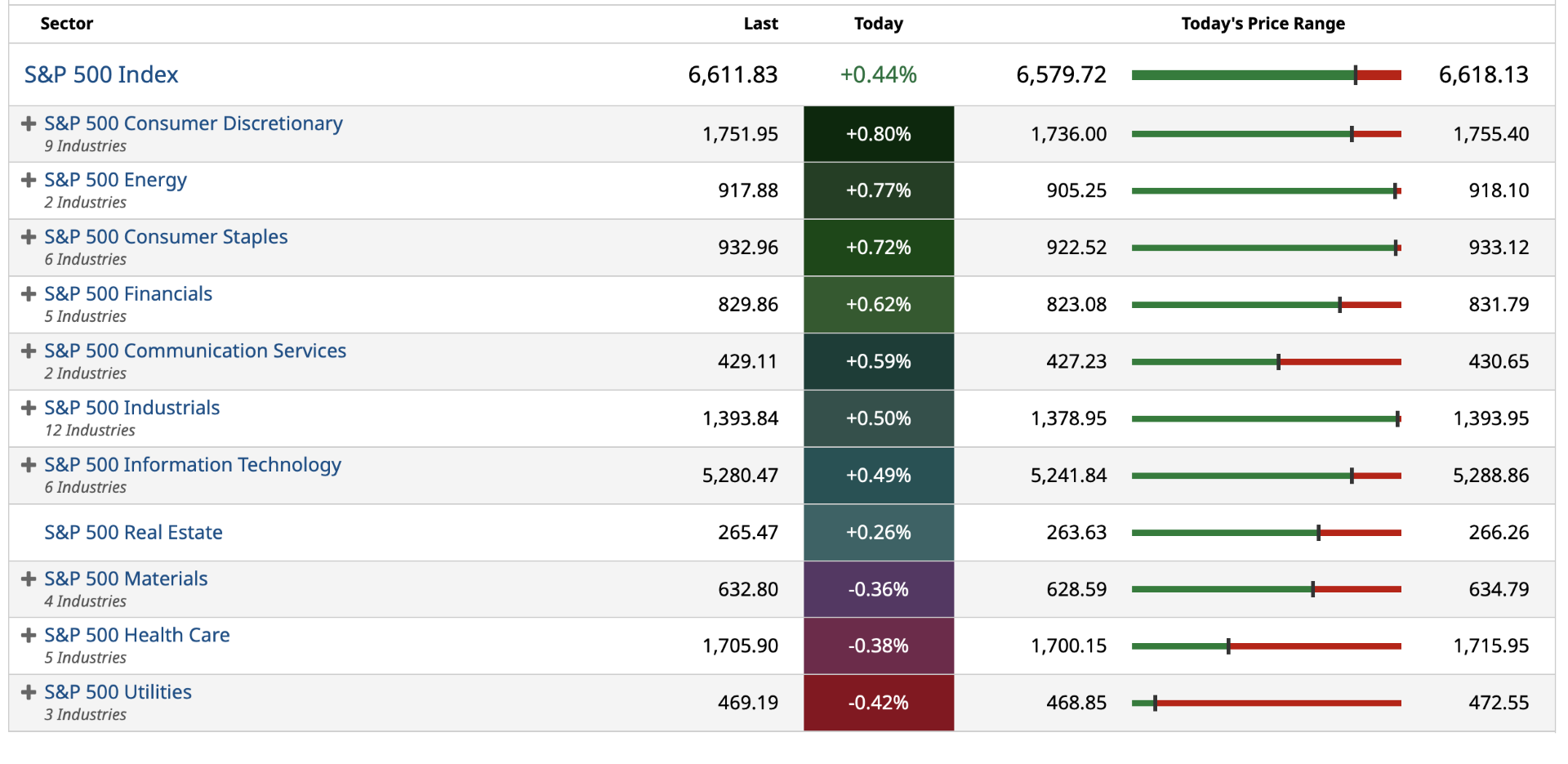

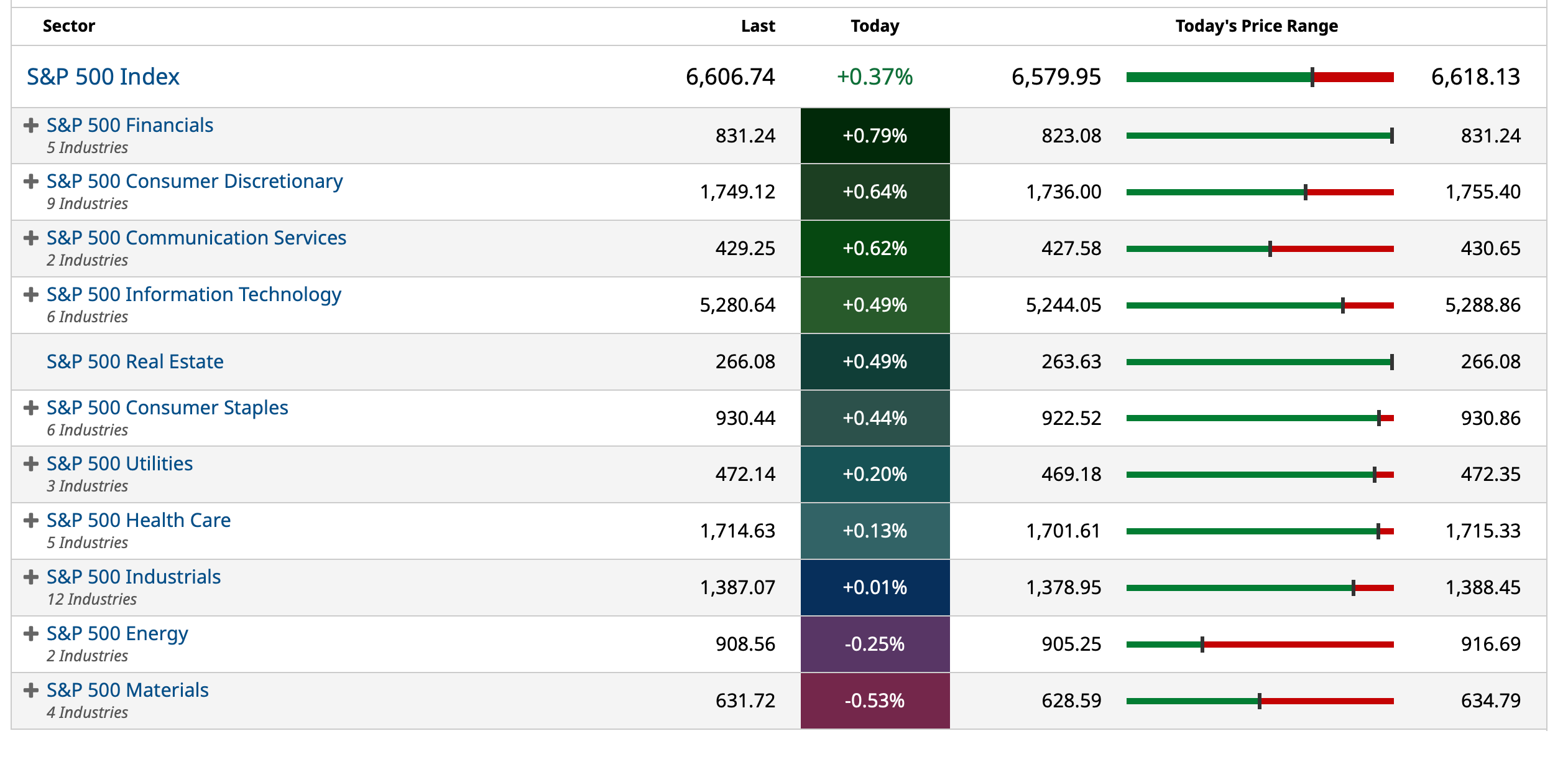

S&P 500 Sectors

% Movers

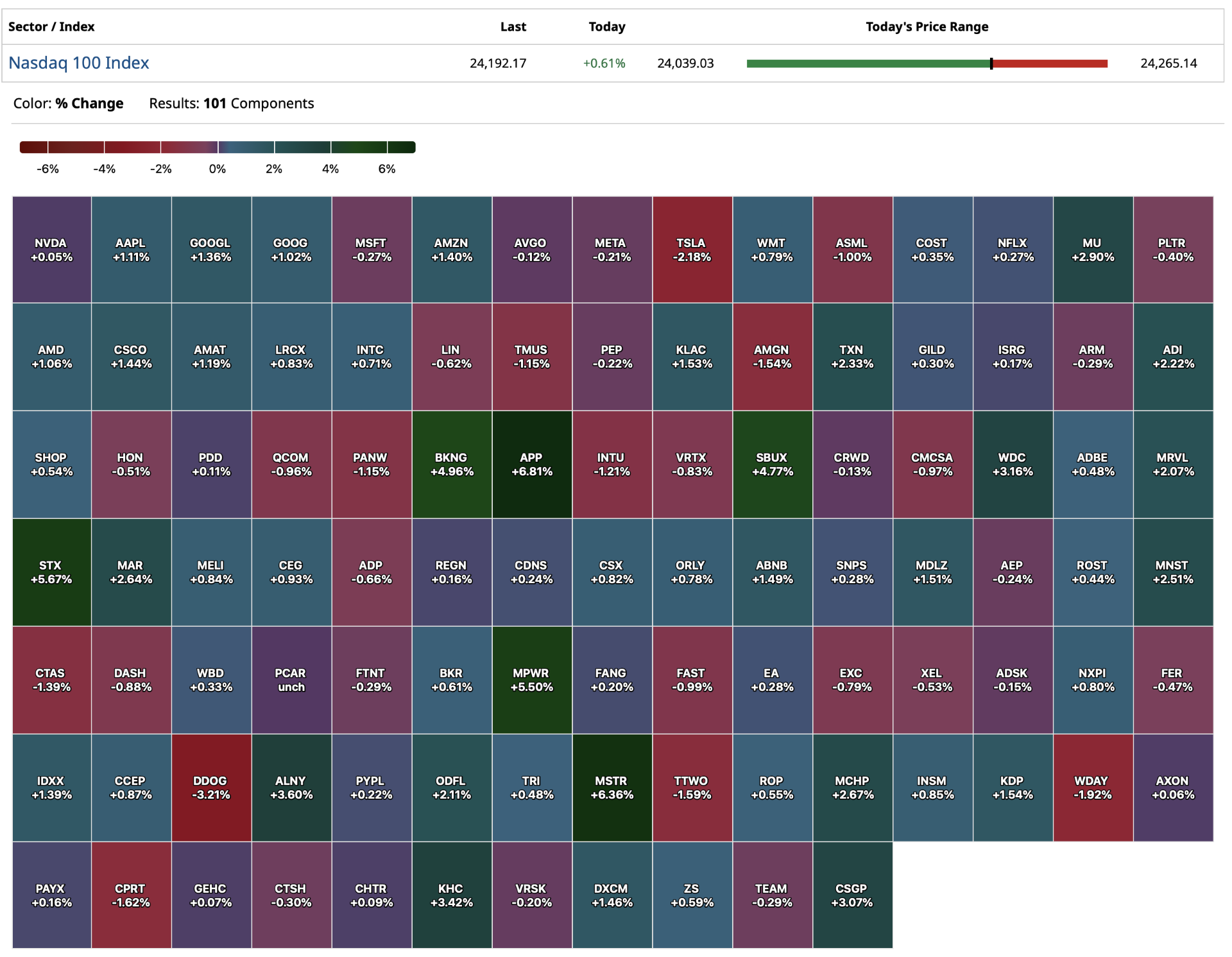

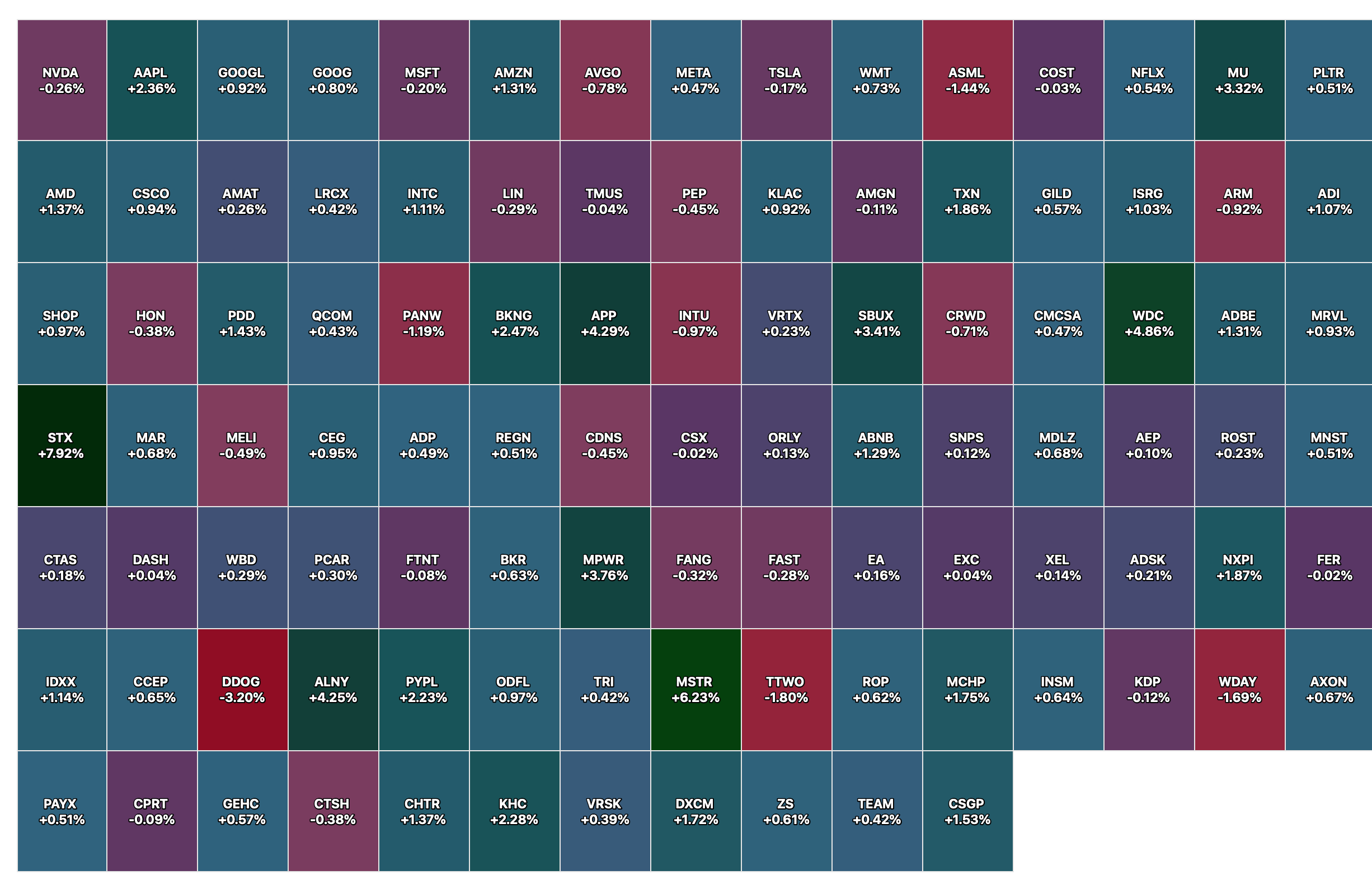

Nasdaq 100 Heat Map

BY Doug Kass · Apr 6, 2026, 4:45 PM EDT

I have sold out my (UNH) at $307.33 (+$30) on the favorable pricing news after the close.

BY Doug Kass · Apr 6, 2026, 4:40 PM EDT

The S&P Short Range Oscillator has now moved back into overbought territory (at 2.29%). @jimcramer @tomkeene @pisani @business @carlquintanilla @ScottWapnerCNBC @SquawkCNBC @cnbcfastmoney @HalftimeReport @KeithMcCullough @SamofAmerica @HedgeyeDJ

— Dougie Kass (@DougKass)

BY Doug Kass · Apr 6, 2026, 4:35 PM EDT

Break in.

Healthcare stocks gapping higher after the close led by Humana (HUM) and UnitedHealth (UNH) (both +$23) after Centers for Medicare & Medicaid Services finalizes Medicare payment policy.

Position: Long UNH (S)

BY Doug Kass · Apr 6, 2026, 4:27 PM EDT

Wolf Street howls about a multi-decade high in JGB yields.

BY Doug Kass · Apr 6, 2026, 3:55 PM EDT

I made a mistake in including (LVS) in my casino basket.

Obviously, LVS has no Las Vegas exposure (I believe they sold their properties almost four years ago!).

BY Doug Kass · Apr 6, 2026, 3:15 PM EDT

I just sold off the indices I bought less than two hours for a small profit — moving me slightly net short (from slightly net long) indices:

Sale prices:

* (SPY) $658.18

* (QQQ) $588.06

I want to sell more of my long indices and move to a net short exposure in the indices.

From earlier:

I sold index calls (as I suggested into strength this morning).

I added to index longs at 1:15 PM:

* (SPY) $656.08

* (QQQ) $585.21

I am slightly net long on a delta-adjusted basis.

Position: Long SPY common (M), QQQ common (M); Short SPY calls (M) and QQQ calls (M)

BY Doug Kass · Apr 6, 2026, 2:06 PM EDT

Position: Long SPY common (M), QQQ common (M); Short SPY calls (M), QQQ calls (M)

BY Doug Kass · Apr 6, 2026, 3:08 PM EDT

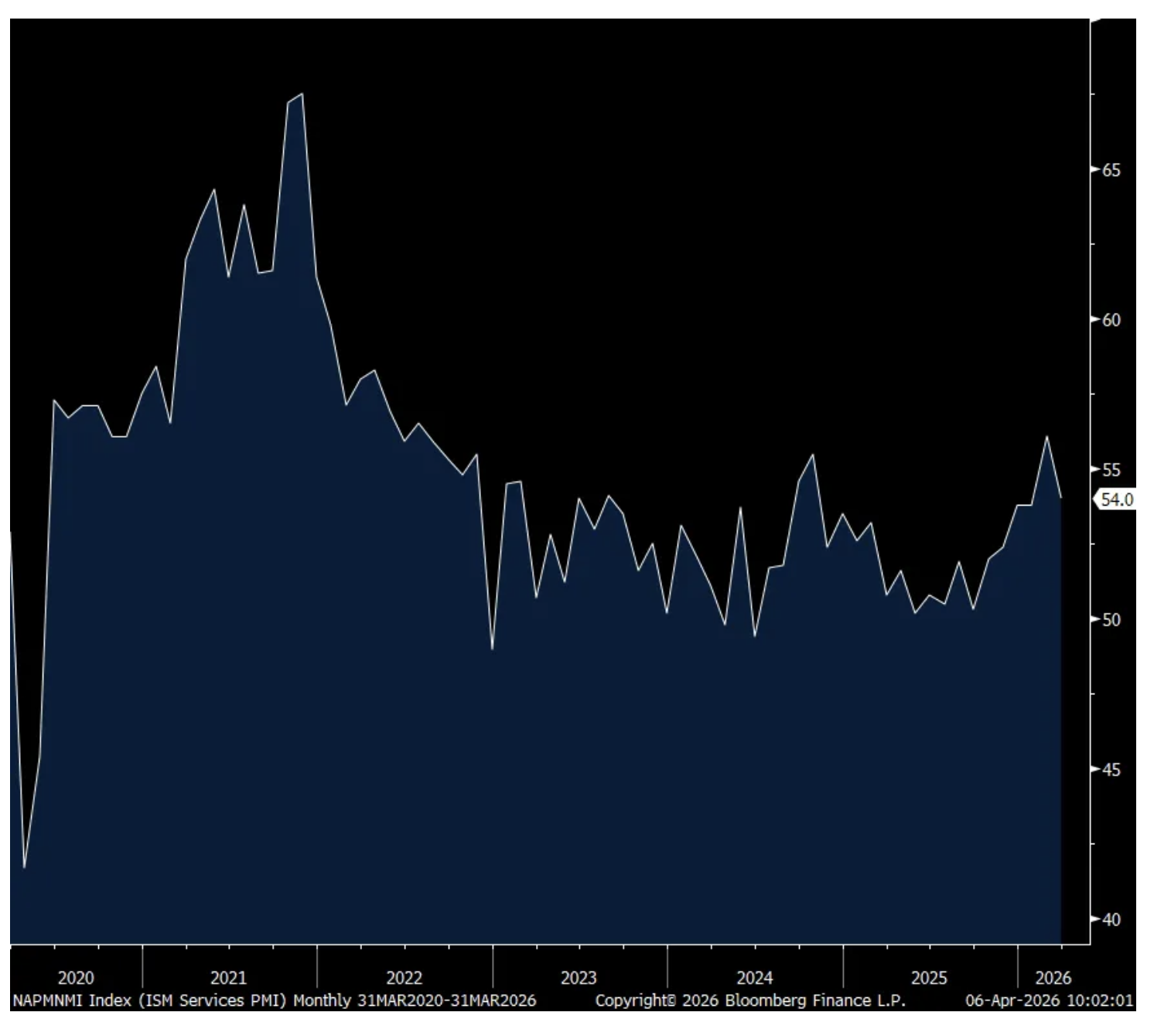

From Peter Boockvar:

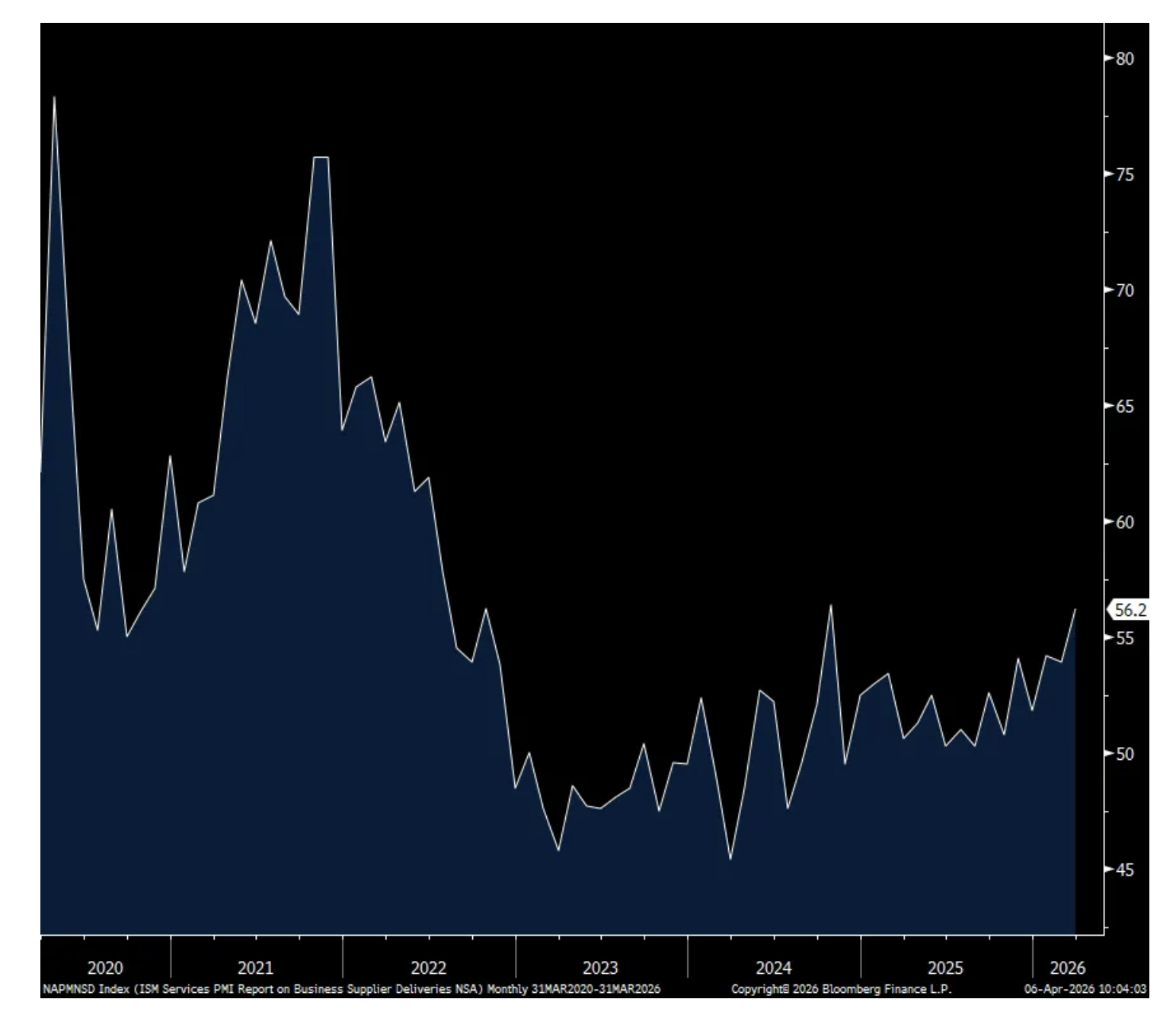

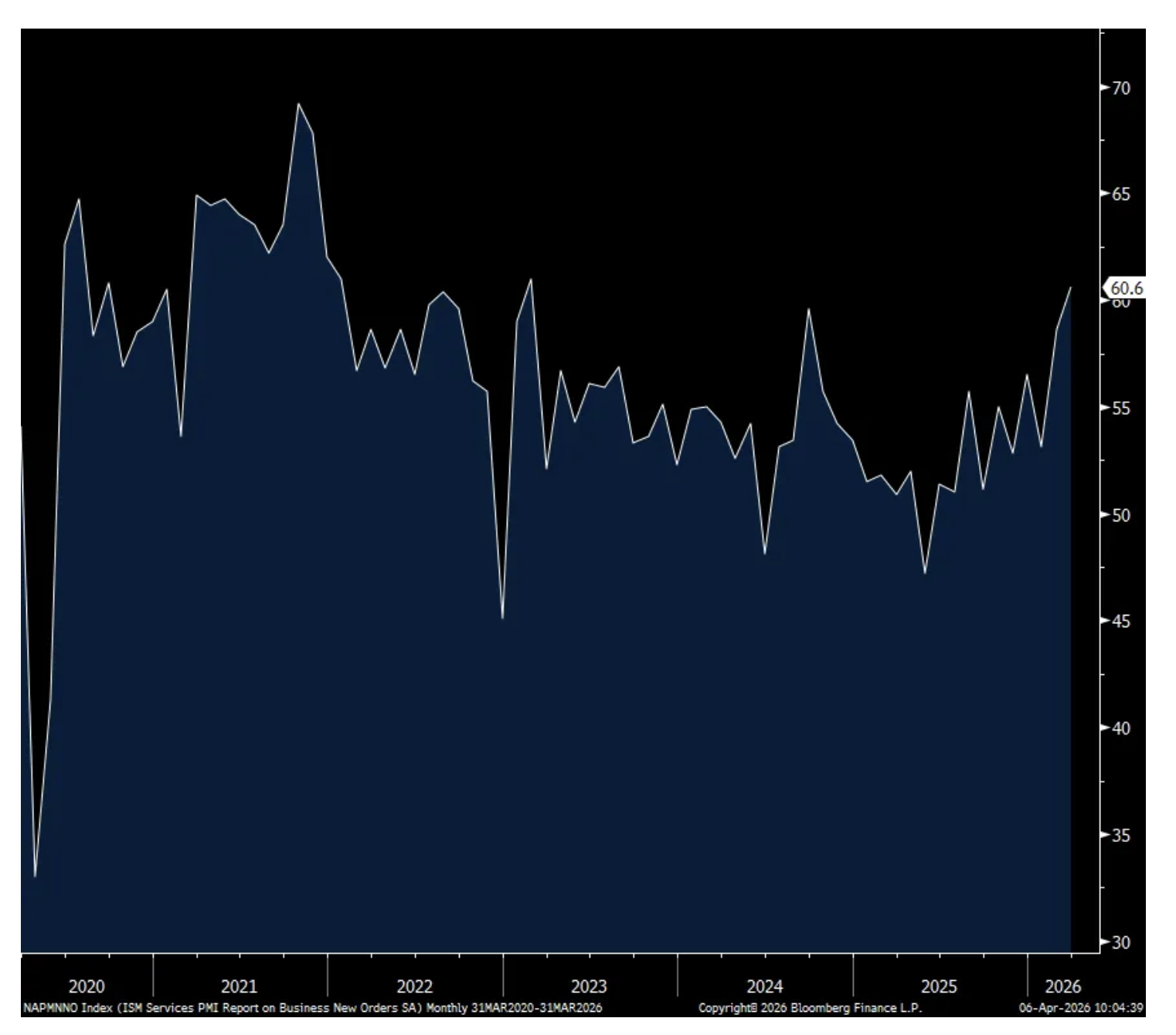

The March ISM services index fell to 54 from 56.1 and below the estimate of 54.9. The Business Activity component dropped by 6 pts to 53.9, the lowest since September. New orders though did rise by 2 pts to 60.6 which is the highest since February 2023 and I have to believe this is a result of companies wanting to front load ordering in light of what’s going on. To this, ISM quoted these company comments, “We are purchasing additional inventory to account for geopolitical issues” and “Stockpiling oil-derivative products in case the extended conflict in Iran or closure of the Strait of Hormuz cause supply issues.” Backlogs slipped by 2.3 pts to 53.6 but above 50 for a 2nd month for the first time since Spring 2024.

Higher energy prices, along with others, took the Prices Paid line item to 70.7 from 63 and that matches the highest since August 2022. Of the 18 industries asked, 17 are paying higher prices with one seeing no change. This comes as the Supplier Deliveries index rose by 2.3 pts to 56.2, the highest since October 2024 and reflects longer lead times and rising supply disruptions. On those deliveries, the ISM said “Comments from respondents include: ‘Back orders from suppliers and manufacturers are creating delays’ and ‘A shortage of trucks is slowing down deliveries.’ “ We know trucking capacity has been leaving the market and spot rates have been firming, as heard from a variety of trucking companies in the industry.

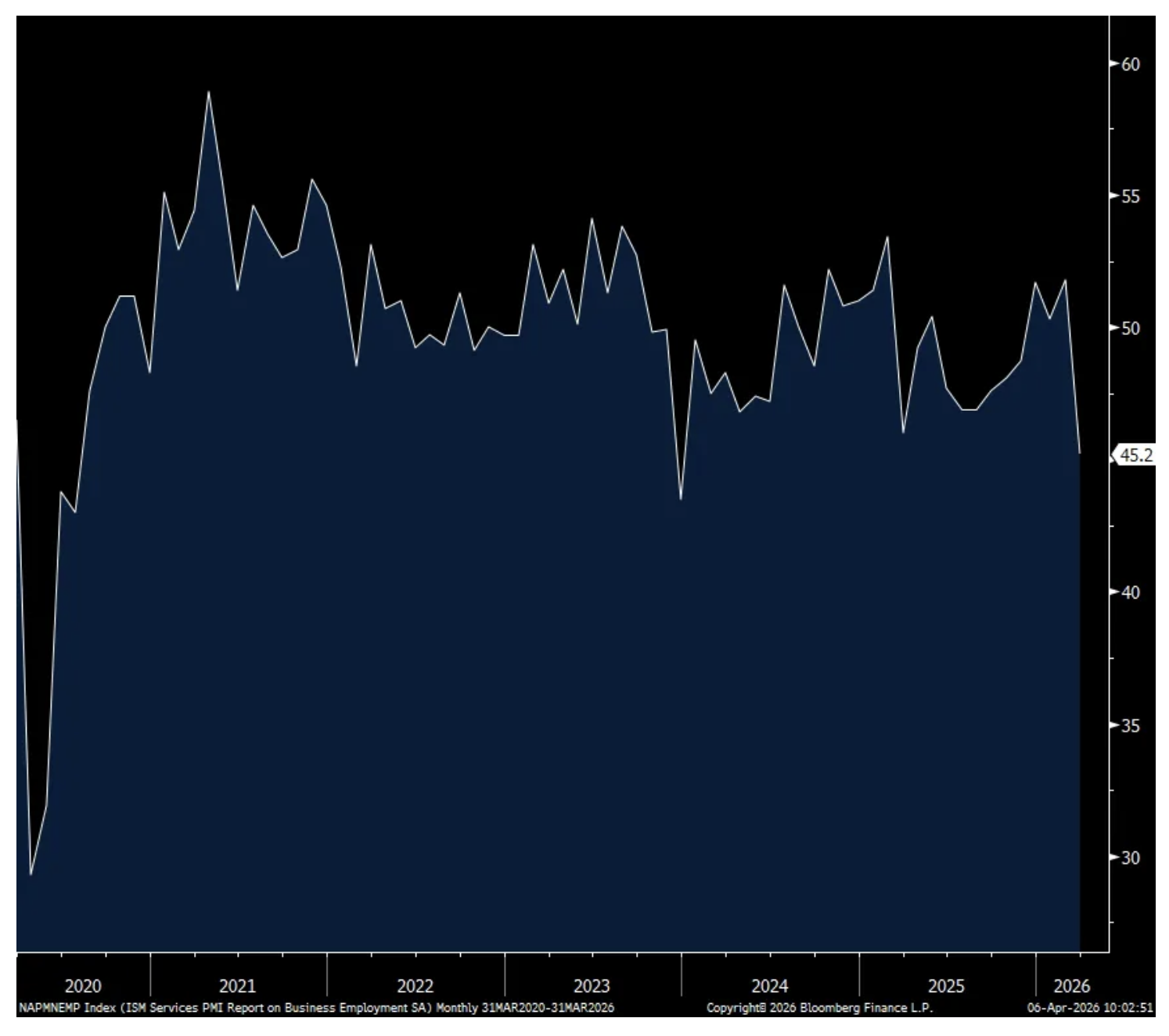

Put yourself in the shoes of a business owner. Your costs are going up all around you and what do you do in response? You likely hire less. The employment component declined by 6.6 pts m/o/m to 45.2, the weakest print since December 2023.

With regards to industry breadth, 13 saw growth vs 14 in February while 3 said their business contracted, the same number seen last month with the balance seeing no change.

Not surprisingly the ISM said this, “The predominant commentary this month was about impacts and adjustments due to the conflict with Iran and the expected flow through of higher oil prices at some point. Companies across many industries reported seeing higher gas and diesel pricing, and inventories of multiple goods increased to withstand supply chain disruptions or short-term oil price impacts. Such construction products as lumber, copper and steel were noted as up in price. Although tariff impacts were still noted by panelists, Iran-related impacts dominated the comments in March.”

Bottom line, life throws curve balls and everyone has a business plan until they get punched in the mouth to paraphrase Mike Tyson. This again is one of those times.

Here were some of the respondent comments and sounds mixed:

“Tariff rollbacks are resulting in favorable price adjustments, but the news of new implementation is driving continued uncertainty. Snowstorms last month disrupted demand and supplier operations, mostly around the availability of labor. Forecasted seasonal growth is starting to materialize due to daylight savings time and higher temperatures.” [Accommodation & Food Services]

“Transportation disruptions in the Middle East are inhibiting both incoming and outgoing cargoes from the region. While force majeure has been received from several Middle Eastern suppliers, business operations are generally at normal levels and no interruptions, except shipping.” [Construction]

“We are still in cost cutting and operational streamlining mode as technology continues to advance. We have seen more concessions regarding passing through tariff surcharges. We continue to closely monitor the political situation in the Middle East and how ramifications could impact our supply chain and overall costs.” [Finance & Insurance]

“As we close out the first quarter, demand for AI computer infrastructure remains incredibly resilient. Customers have opened their 2026 capital budgets, leading to a strong refresh in new order intake. Operationally, our focus has shifted toward efficiency and margin protection.” [Information]

“Political uncertainty with Iran conflict has resulted in less international business. Domestic business remains consistent with January and February levels.” [Mining]

“We’re seeing some expansion across the services economy with stronger business activity and new orders. Clients remain active on regulatory, tax planning, and risk management initiatives, though persistent pricing pressures and evolving economic conditions continue to shape project prioritization and budgeting.” [Professional, Scientific & Technical Services]

“The war in Iran has added an additional layer of uncertainty on top of an already shaky macroeconomic climate. A spike in inflation due to higher oil prices will reduce purchasing power, affecting every industry.” [Real Estate, Rental & Leasing]

“Recent increases in fuel prices are having a substantial impact on the airline industry, resulting in significantly higher operational costs compared to pricing from just one month ago.” [Transportation & Warehousing]

“Continued volatility in copper, aluminum and steel markets — driven by supply chain constraints and strong infrastructure demand — has increased costs and lead times for electric utility projects. These conditions are influencing purchasing strategies and capital planning across the industry.” [Utilities]

“The U.S.-Israel military operations against Iran have created significant uncertainty for our Omani frankincense imports. Threats to close the Strait of Hormuz and rising war-risk surcharges are pressuring regional logistics costs, even for air freight. Combined with the Supreme Court’s emergency tariffs ruling — which replaced our 10-percent tariff with a 15-percent Section 122 tariff — landed costs have increased materially. We are monitoring regional stability closely and maintaining communication with Omani suppliers.” [Wholesale Trade]

ISM Services

Prices Paid

Employment

Supplier Deliveries (higher it goes, more stretched out supply chains)

New Orders

BY Doug Kass · Apr 6, 2026, 2:40 PM EDT

I sold index calls (as I suggested into strength this morning).

I added to index longs at 1:15 PM:

* (SPY) $656.08

* (QQQ) $585.21

I am slightly net long on a delta-adjusted basis.

Position: Long SPY common (M), QQQ common (M); Short SPY calls (M) and QQQ calls (M)

BY Doug Kass · Apr 6, 2026, 2:06 PM EDT

BY Doug Kass · Apr 6, 2026, 12:59 PM EDT

- NYSE volume 31% below its one-month average;

- Nasdaq volume 6% below its one-month average;

- VIX index: up 0.17% to 23.91

None.

BY Doug Kass · Apr 6, 2026, 11:20 AM EDT

Chart from 9:43 a.m. ET

None.

BY Doug Kass · Apr 6, 2026, 9:54 AM EDT

From Peter Boockvar:

We of course wait to see what comes of the fresh ultimatum to the Iranians to reopen the Strait by Tuesday 8pm est (talk now also of a 45 day ceasefire that would include immediately open the Strait) but the weekend did see a pickup in the number of transits with an Iraqi ship going through, more from India and today I saw that some Japanese ships went through. Where Iran made a big mistake with effectively closing the Strait was the anger it engendered around the economic world (as we hear about more and more rationing going on of key things like jet fuel, fertilizer, aluminum, helium, naphtha, etc…). And if it thinks that taking a toll on every passing ship is a good idea for them, you can be sure that over the next 3-5 year years, every country in the region is going to be building bypass options, like pipelines, rail, whatever, to other passage ways, to never have to rely solely on traversing the Strait again as the only option. Thus, if this regime will unfortunately remain in place, their desire for toll taking now will be the undoing of this in the years ahead and Iran will then have little to no economic leverage left with the only lever they can now pull.

Not having anything to do with the Strait closure in terms of shortages, I read this Bloomberg News article over the weekend from April 1st (h/t LG) that said “Almost half of the US data centers planned for this year are expected to be delayed or canceled. One big reason is the shortage of electrical equipment, such as transformers, switchgear and batteries. They are needed not just for powering AI, but also for building out the grid that is seeing increased consumption from electric cars and heat pumps. US manufacturing capacity for these devices cannot keep up with demand, and the scarcity has caused data center builders to rely on imports.”

And interestingly, “Electrical equipment adds up to less than 10% of the total cost of the data center, but it’s impossible to build the operation without it.” And yes, we get a lot of our electrical equipment from China. So, while tariffs were meant to encourage the production of more of it in the US or elsewhere, in the meantime it costs more to procure from China. Finally of note in the article, “The spike in demand from data centers and grid expansion have pushed up prices and extended delivery times to as much as five years. That is why some, like Crusoe (a data center builder), have even resorted to refurbishing old transformers from shuttered power plants as a stopgap measure.” I bring this up because almost half of the GDP growth of about 2% in 2025 was driven by data center construction.

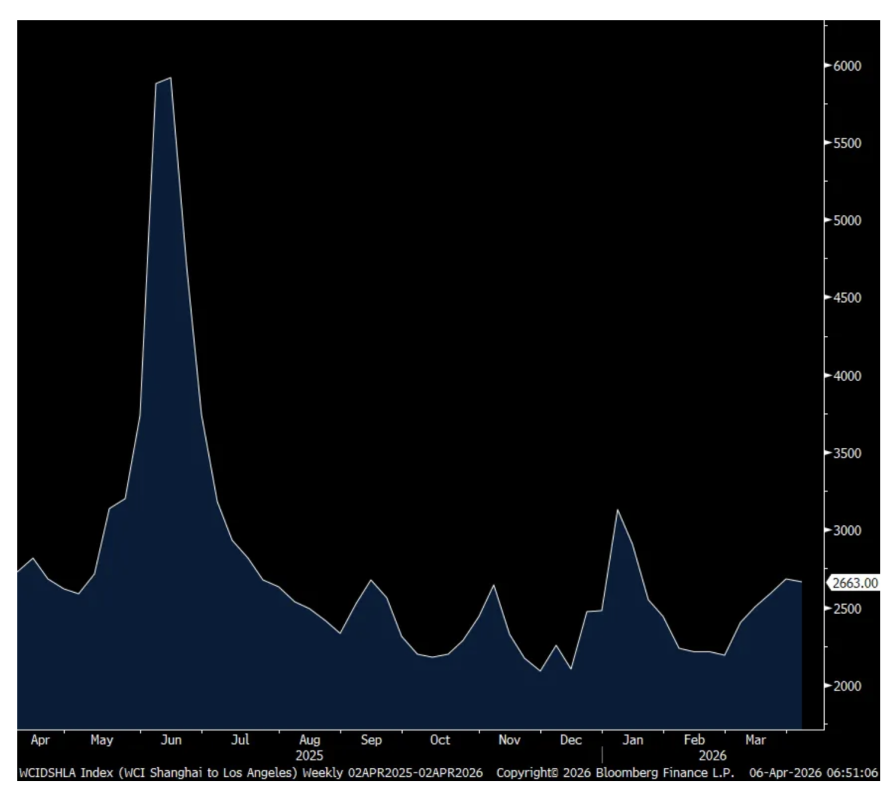

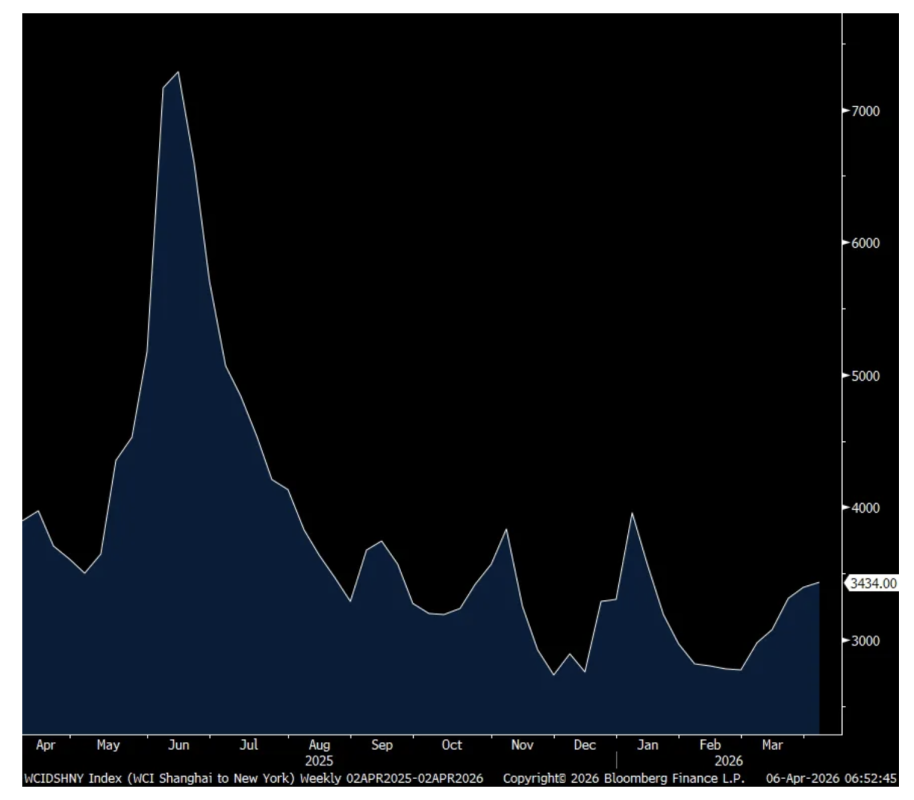

The new threat from the Houthi’s to target the Red Sea again had a mixed impact on container shipping prices. After rising for four straight weeks and by 23%, the Shanghai to LA price fell about 1% to $2,663 per 40 foot container. The Shanghai to NY route though did see a rise of 1.2% and up by 24% over the past five weeks. The Shanghai to Rotterdam trip was little changed after rising by 24% over the prior three weeks.

Shanghai to LA World Container Index

Shanghai to NY

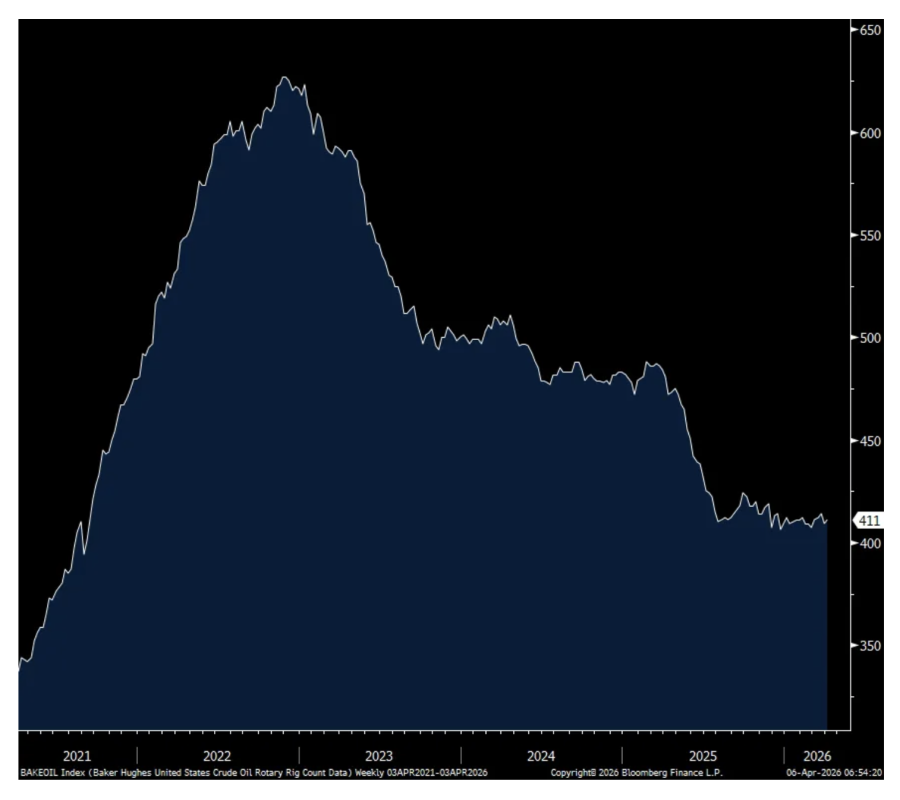

There still is almost no reaction in the US oil patch to the jump in prices as seen with the crude oil rig count. It rose 2 rigs w/o/w to 411 but that is up only 4 since late February and still bouncing around the lowest level since September 2021. It’s clear that drillers aren’t going to react until they see where prices settle out at. While the futures curve in any commodity predicts nothing other than what the market things today, the December WTI contract is trading at just $72 as of this writing vs the front month of around $110.

WTI Crude Oil Futures Curve

Crude Oil Rig Count

There is of course a lot of focus now on private credit but private equity is having difficulty in raising money too. They are clogged up with unsold companies and if private credit has a lessened ability to finance private equity transactions going forward, private equity returns will slip as the cost of capital goes up. According to the WSJ over the weekend, “Private equity firms globally raised $86 billion for buyout, growth and turnaround funds in the first three months of the year, putting the industry on pace to fall short even of last year’s disappointing total of $423.4 billion, data tracking firm PitchBook said Friday.” https://www.wsj.com/

None.

BY Doug Kass · Apr 6, 2026, 9:45 AM EDT

-PFSA +118% (expands into molecular diagnostics; LOI values PanOmics deal at $30M in equity)

-SLNO +33% (Neurocrine confirms to acquire Soleno Therapeutics for $53.00/shr in cash or $2.9B)

-NVNI +32% (to acquire 51% controlling stake in the American business of Beyondsoft Corporation)

-AKTX +25% (announces strategic partnership with WuXi XDC to advance development of its novel ADC Payload Targeting RNA Splicing)

-AAOI +6.6% (receives new 800G transceivers order)

-PLTK +4.7% (announces strategic review of portfolio)

-BOOT +4.1% (Jefferies Raised BOOT to Buy from Hold, price target: $195)

-KTOS +3.7% (Jefferies Raised KTOS to Buy from Hold, price target: $85)

-MU +3.6% (KeyBanc Capital Markets Reiterates MU with Overweight, price target: $600)

-TWLO +3.6% (Jefferies Raised TWLO to Buy from Hold, price target: $160 from $125)

-HOLO +3.5% (plans to invest $400M to upgrade the Bitcoin protocol to resist quantum attacks)

-COIN +3.3% (momentum following conditional approval from the OCC for a US trust charter)

-AMKR +3.1% (Melius Research Raised AMKR to Buy from Hold, price target: $60)

-JBS +2.5% (Colorado plant workers to end strike amid resumption of discussions)

-NFLX +1.8% (Goldman raised to Buy from Neutral, price target $120 from $100)

-VELO -13% (files $500M mixed shelf)

-AESI -9.4% (files to sell convertible note offering)

-LGN -2.9% (hearing to market $620M share sale for two days)

-DOW -2.6% (Tier1 firm Cuts DOW to Underperform from Neutral, price target: $35 from $31)

-CAR -2.3% (Deutsche Bank Cuts CAR to Hold from Buy, price target: $128)

-NBIX -2.0% (Neurocrine confirms to Acquire Soleno Therapeutics for $53.00/shr in cash or $2.9B)

None.

BY Doug Kass · Apr 6, 2026, 9:25 AM EDT

* Casinos will continue to be disintermediated by betting online and by the prediction markets

* I am short the major Las Vegas casinos...

I have recently accumulated a short position in four gaming stocks - (CZR) , (WYNN) , (LVS) and (MGM) .

The core reason for the industry short is that traditional gaming is being disintermediated by the proliferation of on line sports betting and by the growing acceptance of prediction markets:

* Visitations in Las Vegas in 2025 declined by almost 8% -- the largest drop in over 55 years.

* The Administration's attitude (and trade war) toward Canada is (particularly) hurting visitations from the north.

* High gas prices and congestion at airports won't help 2026 Las Vegas casino industry visits.

* Las Vegas' unemployment rate is rising - and is now well above the national average.

* Real estate prices are dropping. In real (inflation adjusted terms) Las Vegas casino industry revenues, after being flat for the last 25 years are now beginning to decline.

What is making matters worse is that a Las Vegas visit is no longer cheap. Daily room rates are +$50 room (to over $183/night) over the last six years and that doesn't include a daily resort fee surcharge. Perks like parking and drinks are no longer complimentary — adding to the per diem costs. Entertainment costs are literally (The Sphere) thru the roof.

This is hurting the K-shaped economy where it hurts the most- in the middle class (that dominates Las Vegas visits).

At the gaming tables, casinos are making it more difficult for gamblers to win - with many roulette tables featuring three zero spaces (vs two historically) and blackjack tables are reducing their payouts.

Casinos are fighting demographic trends: Young gamblers, in particular, are showing less interest in Las Vegas casinos. The 20- something traffic is half today of pre-Covid Las Vegas traffic.

More on this short investment theme later this week...

Position: Short CZR (VS), WYNN (VS), LVS (VS), MGM (VS)

BY Doug Kass · Apr 6, 2026, 9:00 AM EDT

None.

BY Doug Kass · Apr 6, 2026, 8:50 AM EDT

None.

BY Doug Kass · Apr 6, 2026, 8:29 AM EDT

11:30 a.m.: Treasury hosts an $89B 3 & a $77B 6 month bill auction.

Early Morning: Fed Bank of Chicago President Goolsbee (Non-Voter) PodcastAppearance -- The Indicator

None.

BY Doug Kass · Apr 6, 2026, 8:15 AM EDT

I suppose ignorance is bliss and laziness and the absence of homework/factor analysis (Japanese yields exploding/credit spreads, who cares?), the same guests day in and day out and the lack of penetrating questions are simply passe. @cnbc

— Dougie Kass (@DougKass)

So, the predictable, dull and…

BY Doug Kass · Apr 6, 2026, 7:35 AM EDT

Unfortunately, this morning the business media is preoccupied with fruitless, nondifferentiated and non-value added discussions about the conflict in Iran.

They don't seem capable of multi-tasking, which is worrisome as there are so many other issues facing market participants.

Here is one variable and influence — mentioned by Keith at Hedgeye — that the business media will not mention today:

It's "off topic" for Macro Tourists this morning, but its still happening

— Keith McCullough (@KeithMcCullough)

Japanese Bond Yields ramping to new #Quad3 Cycle Highs as markets price in higher inflation pic.twitter.com/tz4Pb6zTgP

BY Doug Kass · Apr 6, 2026, 7:20 AM EDT

COMMODITIES: New #Quad3 Cycle Highs last week should keep Bond Yields in breakout mode pic.twitter.com/m2QLuLPYDZ

— Keith McCullough (@KeithMcCullough)

BY Doug Kass · Apr 6, 2026, 7:00 AM EDT

This morning I will be participating in a charity event and will be out from 9 a.m. to noon.

My posts will be less frequent and much briefer during that time.

BY Doug Kass · Apr 6, 2026, 7:00 AM EDT

Bank of America downgrades Carvana (CVNA) .

Position: Long BAC (S); Short CVNA (VS)

BY Doug Kass · Apr 6, 2026, 6:52 AM EDT

🇺🇸 Valuations

— ISABELNET (@ISABELNET_SA)

Valuations have cooled: the S&P 500 has compressed to 20 times forward earnings, and the Mag-7 has come down to 24 times after January's lofty 31 times. Still not exactly cheap, but definitely a move in the right direction

👉 https://t.co/14i5SQVCfd@GoldmanSachs pic.twitter.com/TDXYBpotYO

BY Doug Kass · Apr 6, 2026, 6:35 AM EDT

Americas Banks: 1Q26 Preview: A healthier valuation backdrop, but macro uncertainty may create 2H earnings risk

6 April 2026 | 1:04AM EDT | Research | Equity

As we head into 1Q26 earnings, we see four key themes which we expect investors to focus on: 1) the outlook (and potential upside) for NII; 2) risks to the capital markets revenue from the spike in market volatility; 3) impacts to credit quality and provisions from higher energy prices (and hence weaker GDP); and 4) how banks will utilize the increased balance sheet flexibility from lower capital requirements. Valuation for the group appears more attractive after the 7% sell-off YTD, which was entirely multiple-driven, with valuation more in-line with historical levels, despite banks generating attractive ROTCEs even when factoring in some of the recent macro risks. In our view, the best positioned and most topical stocks remain BAC, C and WFC.

BY Doug Kass · Apr 6, 2026, 6:25 AM EDT

SENIOR IRANIAN OFFICIAL: TEHRAN WILL NOT ACCEPT DEADLINES OR PRESSURE TO MAKE A DECISION

— *Walter Bloomberg (@DeItaone)

SENIOR IRANIAN OFFICIAL: TEHRAN WILL NOT REOPEN STRAIT OF HORMUZ IN EXCHANGE FOR A 'TEMPORARY CEASEFIRE'

SENIOR IRANIAN OFFICIAL: TEHRAN BELIEVES THAT THE UNITED STATES LACKS READINESS FOR…

BY Doug Kass · Apr 6, 2026, 6:15 AM EDT

#Iran War Update No. 37 (focus on Iranian strategic narrative):

— Hamidreza Azizi (@HamidRezaAz)

🔹The central development of Day 37 was the U.S. rescue operation inside Iran following the downing of an F-15E. In Iranian framing, the point is not to deny that the United States can still conduct complex…

BY Doug Kass · Apr 6, 2026, 6:05 AM EDT

The S&P Short Range Oscillator is approaching neutral after being oversold for several days -0.52% vs. -1.53%.

All things being equal when the market opens I will be selling index calls against the common I purchased in Friday's after hours.

Position: Long SPY common (VS), QQQ common (VS)

BY Doug Kass · Apr 6, 2026, 5:57 AM EDT

* Purchased (SPY) at $654.55 and (QQQ) at $584.90.

* Added to (META) at $573.19 long.

Position: Long SPY common (VS), QQQ common (VS)

BY Doug Kass · Apr 6, 2026, 5:49 AM EDT

COMMODITIES: New #Quad3 Cycle Highs last week should keep Bond Yields in breakout mode

🇺🇸 Valuations Valuations have cooled: the S&P 500 has compressed to 20 times forward earnings, and the Mag-7 has come down to 24 times after January's lofty 31 times. Still not exactly cheap, but definitely a move in the right direction 👉 isabelnet.com/?s=valuation @GoldmanSachs

It's "off topic" for Macro Tourists this morning, but its still happening Japanese Bond Yields ramping to new #Quad3 Cycle Highs as markets price in higher inflation

SENIOR IRANIAN OFFICIAL: TEHRAN WILL NOT ACCEPT DEADLINES OR PRESSURE TO MAKE A DECISION SENIOR IRANIAN OFFICIAL: TEHRAN WILL NOT REOPEN STRAIT OF HORMUZ IN EXCHANGE FOR A 'TEMPORARY CEASEFIRE' SENIOR IRANIAN OFFICIAL: TEHRAN BELIEVES THAT THE UNITED STATES LACKS READINESS FOR Show more

The S&P Short Range Oscillator has now moved back into overbought territory (at 2.29%). @jimcramer @tomkeene @pisani