From Peter Boockvar:

"Out of clutter, find simplicity; from discord, find harmony; in the middle of difficulty lies opportunity"

The war trade is of course reversing again with stocks, bonds, commodities, the US dollar and gold. The CNN Fear/Greed index has risen to 14 from the 10 level I mentioned last week that was a great set up for the rally that only needed a nudge from any indication of an end to the war. I do want to reiterate my belief that even with a cessation in the war and the immediate drop in commodity prices, particularly crude and crops, that would follow, we’re in a commodity bull market and prices are not going back to where they were pre-war and we are positioned as such. With respect to the S&P 500, 6638 is the 200 day moving average and a spot we can trade to on this bounce which will then get tested again, particularly because of the faltering GenAI tech trade, especially with the hyperscalers because of their shrinking free cash flows which I’ve talked about.

The war trade is of course reversing again with stocks, bonds, commodities, the US dollar and gold. The CNN Fear/Greed index has risen to 14 from the 10 level I mentioned last week that was a great set up for the rally that only needed a nudge from any indication of an end to the war. I do want to reiterate my belief that even with a cessation in the war and the immediate drop in commodity prices, particularly crude and crops, that would follow, we’re in a commodity bull market and prices are not going back to where they were pre-war and we are positioned as such. With respect to the S&P 500, 6638 is the 200 day moving average and a spot we can trade to on this bounce which will then get tested again, particularly because of the faltering GenAI tech trade, especially with the hyperscalers because of their shrinking free cash flows which I’ve talked about.

I’ll go right to Nike, a stock we’ve recently bought, and what they said on their call of note that has the stock down 10% pre market:

The main angst is the revenue guide of down 2-4% rather than the expected increase of about 2% for the fresh quarter we’re now in “with modest growth in North America despite lapping of value liquidation in the prior year, largely offset by declines in Greater China and Converse.”

“Order books are growing and we are taking back shelf space. However, sell-through trends are not yet where we want them to be. Despite making progress versus a year ago, digital is still too promotional. Markdowns across the marketplace remain elevated. Our teams are pulling levers to manage inventory and protect brand health, but this continues to be a headwind to gross margin profitability.”

“North America is leading our comeback and is well positioned to sustain the momentum as we move forward...While sell-through has been below plan, sell-through improved in February, and we drove positive growth in all channels in the geography for the first time in two years.” North American sales rose 3%.

EMEA sales fell 7%. “Given the softness in sportswear, traffic patterns, and promotions across Europe, as well as recent disruption in the Middle East, we anticipate ending the fourth quarter with elevated inventory.”

“In Greater China, Q3 revenue declined 10%” but, “we made forward progress in Greater China.” The rest of Asia saw sales down 2% but “we saw bright spots with running up double digits and growth in training and football, while sportswear declined double digits.”

“While the tariff environment has been uncertain, assuming no significant changes, we expect the first quarter of fiscal ‘27 to be the final quarter where higher tariffs continue to be a material y/o/y headwind to gross margin.” And why again do we have tariffs on sneakers and apparel that we will never make here?

Finally of note from Nike, “We’re not seeing a consumer reaction to what’s going on in the Middle East at this point in time in North America.”

The other key earnings call was RH and from its CEO Gary Friedman and whose stock is down 18% this morning. Gary said this of note:

“Albert Einstein’s three rules of work - out of clutter, find simplicity; from discord, find harmony; in the middle of difficulty lies opportunity - seem especially relevant at this moment. We’re compounding clutter from tariffs, global discord as a result of war, and the most dire housing market in decades can make it difficult to separate the signal from the noise.”

In the coming years, he’s banking on rich people to spend on RH furniture. “There are two important factors that will meaningfully expand the size of our market over the next 10 years. One is the exponential spending of high and ultra high net worth consumers on the home. Ultra high net worth consumers, with a net worth above $20 million, own an average of 3.7 homes; billionaires own 10. Ultra high net worth consumers spend 6.4x more on home furnishings than a consumer with a single primary residence.”

“Two is the estimated $30 trillion to $38 trillion wealth transfer projected to take place over the next 10 years, which is more than double the past 10 years.”

In terms of the stock fall, a lot has to do with the drop in margins as “we’re in peak investment cycle and trough economic cycle, especially from a home point of view” and “you’ve had the whole kind of chaotic tariff cycle that’s caused kind of significant disruption on the business...So, it’s all of those things together...So, this is a good time to buy our stock. This is when people create generational wealth, right? This is no different than trough times in a real estate market, trough times in any kind of a transitional time for an industry or business.”

With the macro and the housing market, “do we have the housing market getting worse? I’d say we have embedded in this, the current environment right now, which I believe is worse, and mostly from a geopolitical point of view and a perception of view of more things can go wrong than maybe can go right. And I think that’s how the markets generally risk times likes these when you’ve got uncertainty and you’ve got global tensions and war and oil issues and the endless amount of things that oil impacts, right?”

“But did the housing market get better when interest rates came down somewhat? Not really. Is the housing market going to get worse if they go back, if we get 25, 50, 75 basis points, you get three hikes? I don’t think it gets much worse. I think you’ve got to think back at history and say in 1978, we there’s 4.06 million homes sold, and that was a low point. And in 2003, 2004, and 2005 you had 4.06 million homes sold...And that’s with 53% more people, right? So, it’s hard to believe it gets worse than this because you get worse than this for a small period.”

“I mean, none of us have seen a world war in our lifetimes, right? Is there risk of world war? I don’t think so. I mean, I think cooler heads will prevail, but this is uncertain times.”

Dave & Buster’s is rallying pre market and said this of note:

“As we discussed on our Q3 call, we saw improvement in same store sales throughout last quarter. I’m encouraged to share that excluding the three days of impact from Winter Storm Fern in January, we also saw improvement throughout the fourth quarter.”

“Our F&B same store sales have now been positive for the last six fiscal months through February 2026. In addition to our new menu, our improved execution around our Eat & Play combo offering has also been a powerful driver.”

On the macro, “obviously there’s a lot going on from a macro perspective, from gas prices, from consumer sentiment, and the like, it’s just hard for us to parse through what’s impacted the macro versus some of these holiday shifts with spring break and Easter. So, as typical for a business, we kind of like to get through this spring break period of time and try to get a better read on things, but we certainly know it’s out there, but it’s too early for us to really parse through what impact that’s having.”

“We have spoken to our customers, we have spoken to our teams to understand what our guests are saying. And one of the things that they’ve been craving for is more games, more experiences and more immersive experiences. So, we’re going to give it to them, not only through like the typical arcade game, but through culturally relevant IPs.”

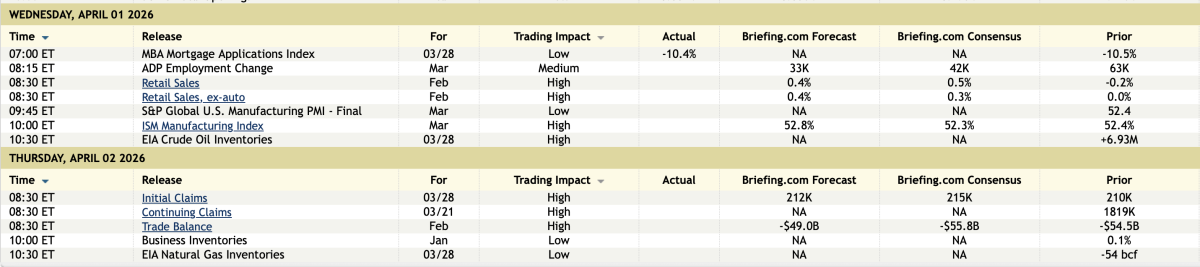

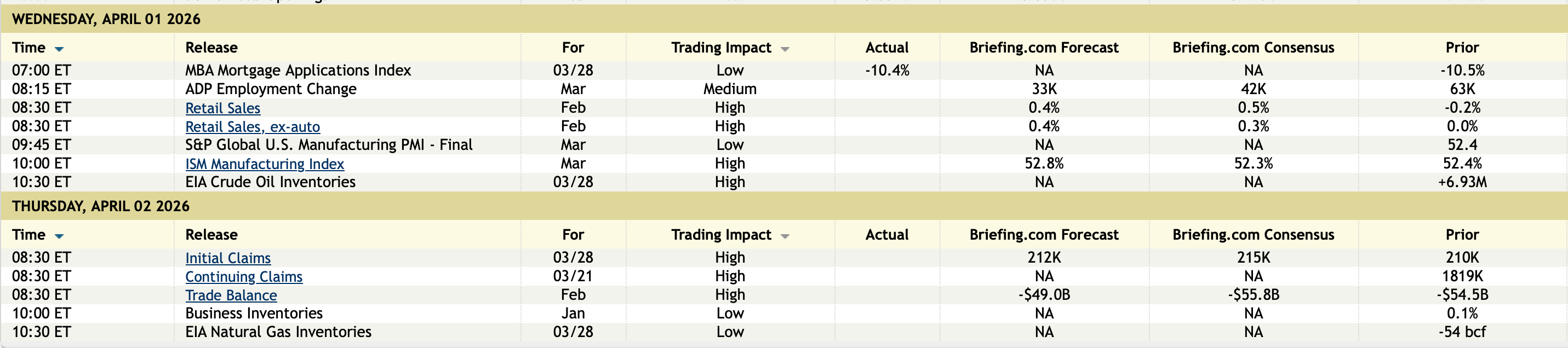

Shifting to some data. Mortgage applications fell 10.4% w/o/w with almost all of that due to a 17% drop in refi’s because of another rise in mortgage rates to 6.57% on average from 6.43% in the week before, 6.3% the week before that and 6.19% in the week before that. It was at 6.09% in the last week of February. Purchase applications fell for a 2nd week, by 2.6%.

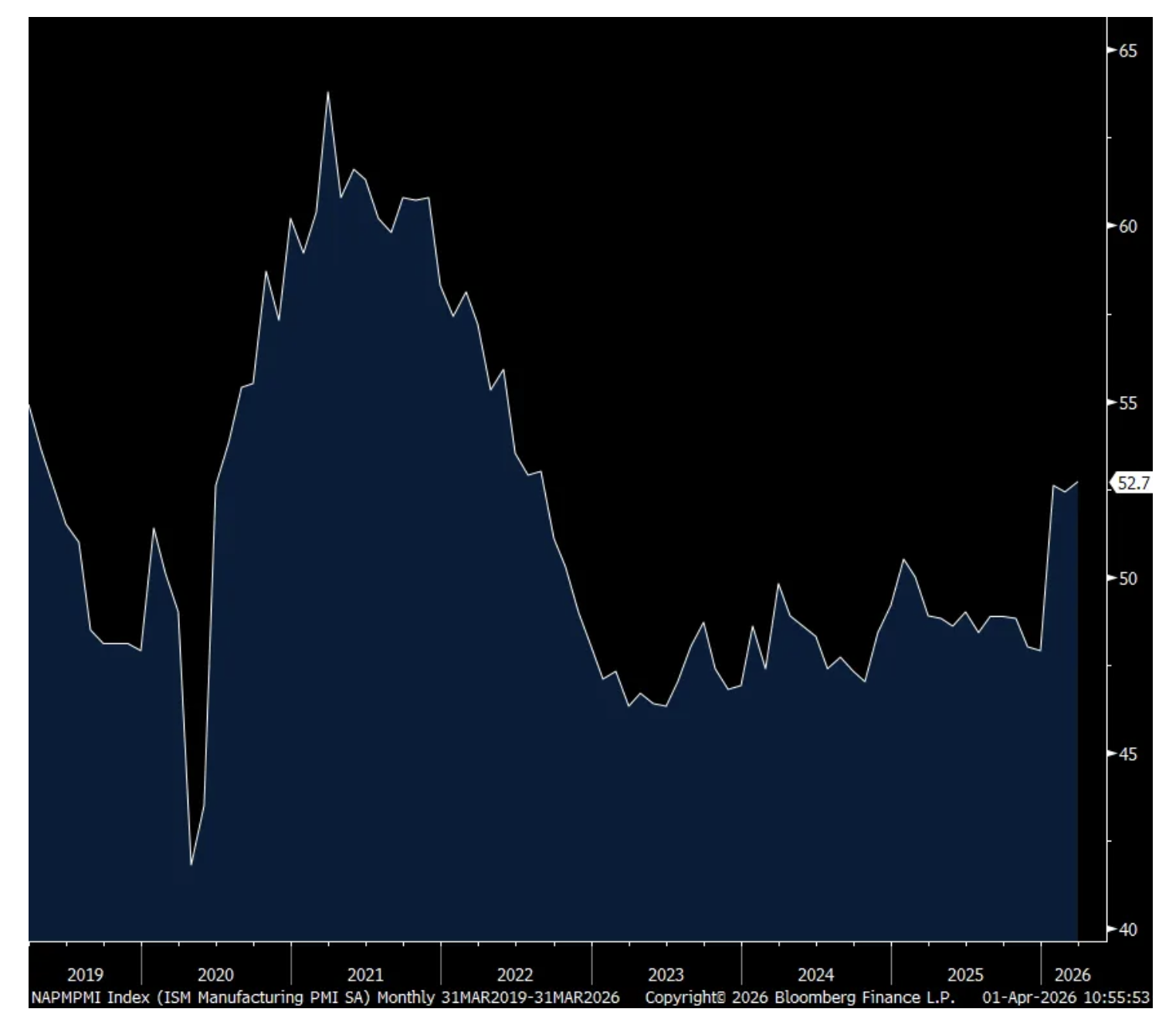

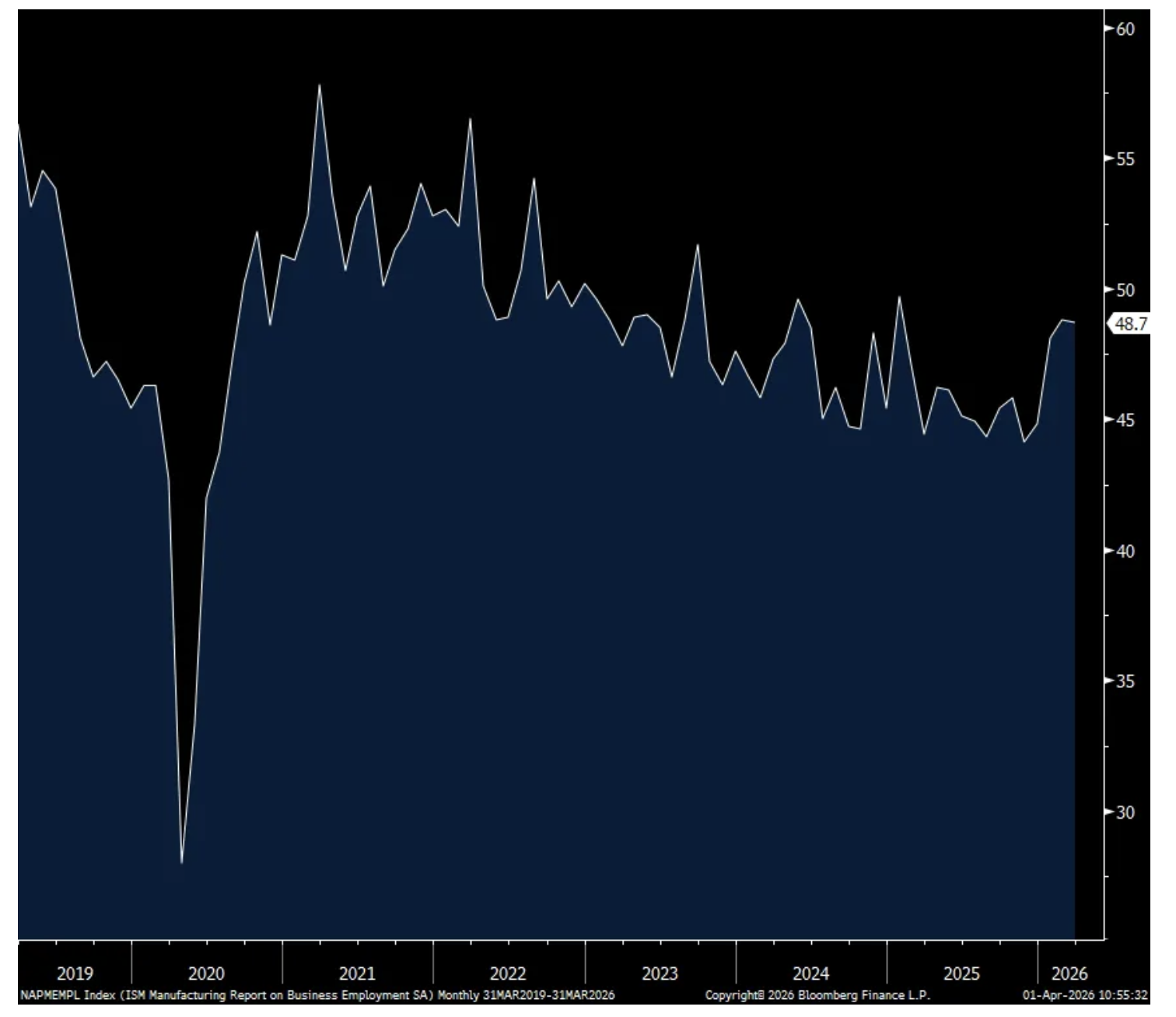

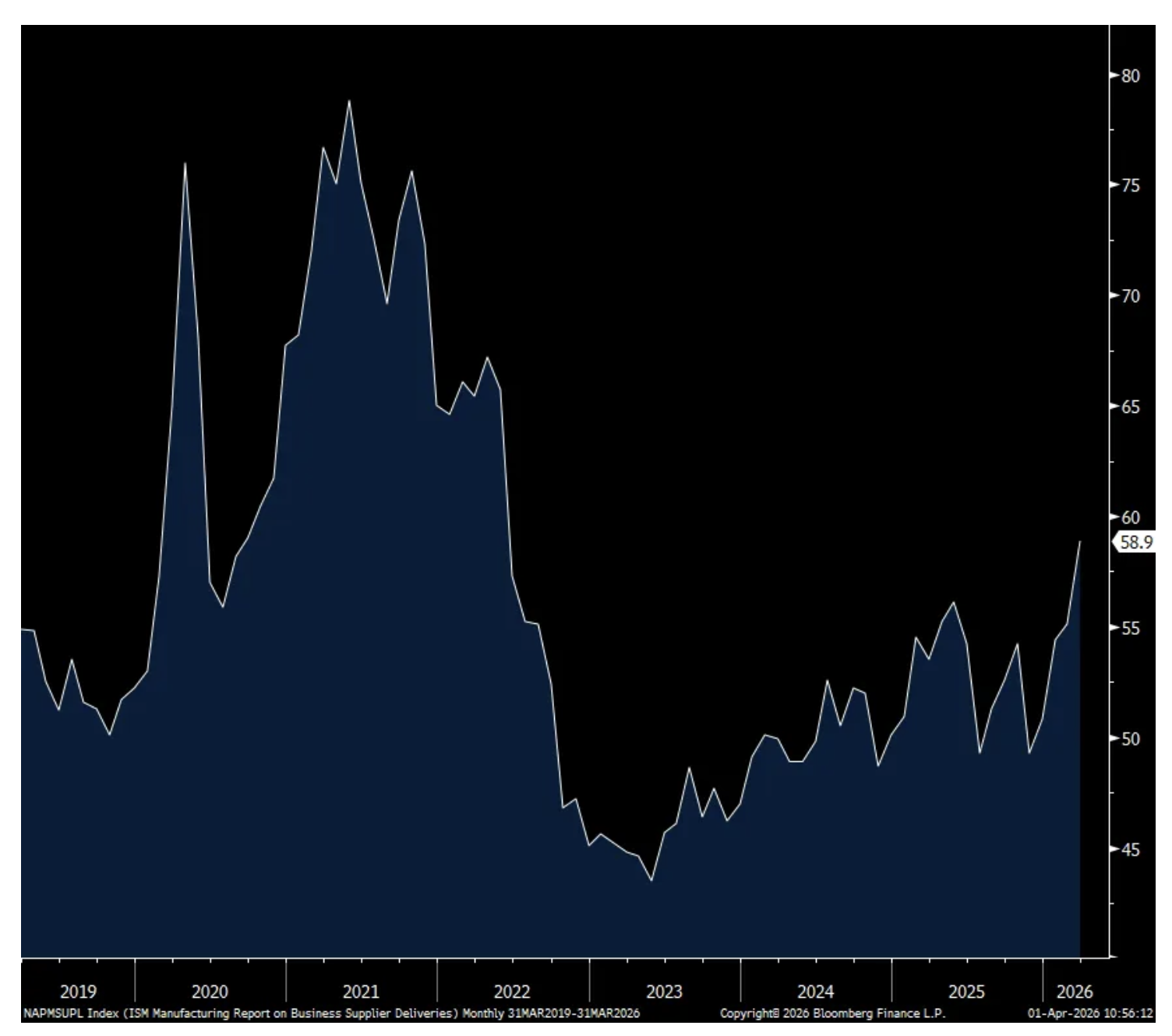

Here are some of the March manufacturing PMI’s released today ahead of the ISM at 10am est and most fell m/o/m not surprisingly:

China 50.8 vs 52.1

Japan 51.6 vs 53

Australia 49.8 vs 51

Taiwan 53.3 vs 55.2

Vietnam 51.2 vs 54.3

South Korea 52.6 vs 51.1

Indonesia 50.1 vs 53.8

Thailand 54.1 vs 53.5

Philippines 51.3 vs 54.6

Malaysia 50.7 vs 49.3

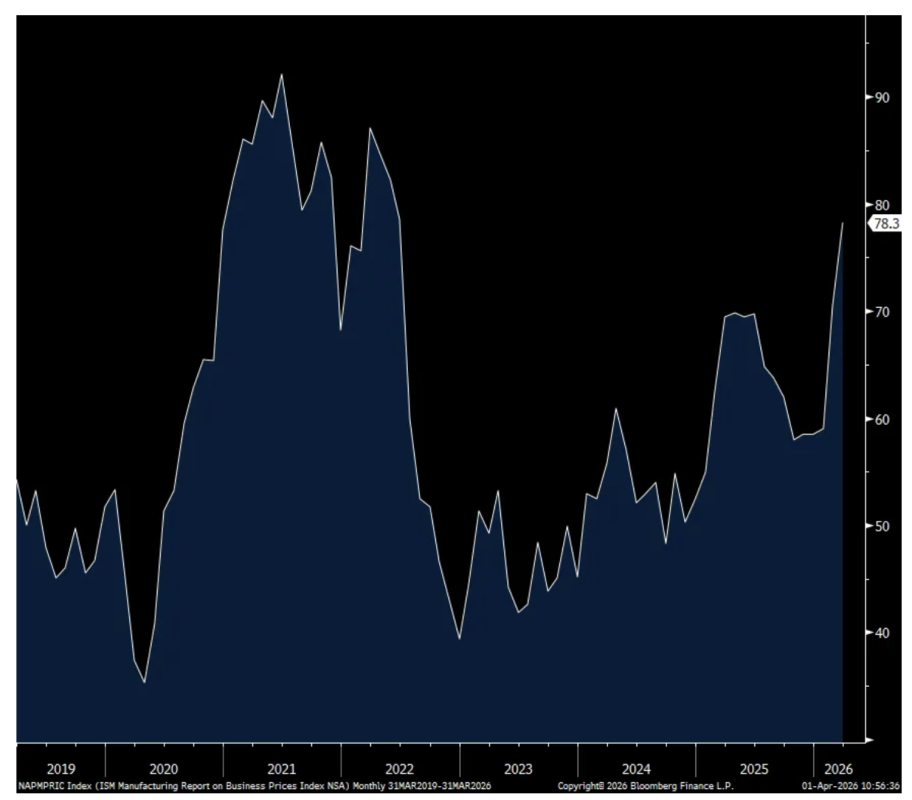

With China specifically, Rating Dog said “Notably, cost pressures intensified significantly. The rate of input price inflation accelerated to the highest since March 2022. Driven by this, output prices also increased at the sharpest in four years. Concurrently, supply chains faced notable disruptions, with suppliers delivery times lengthening to the greatest extent since December 2022, posting challenges to operational efficiency.”

The final Eurozone manufacturing PMI was 51.6 vs 51.4 initially and vs 50.8 in February. S&P Global said, “The war in the Middle East has already left its mark on euro area manufacturing. Suppliers’ delivery times have risen sharply as logistics markets re-adjust to maritime disruption, while surging oil and energy prices have pushed factory input cost inflation up to its highest level since late 2022...we saw some of the war driven inflation impulse being passed straight through to final prices in March.”

The UK final manufacturing PMI was 51 vs 51.7 in February.

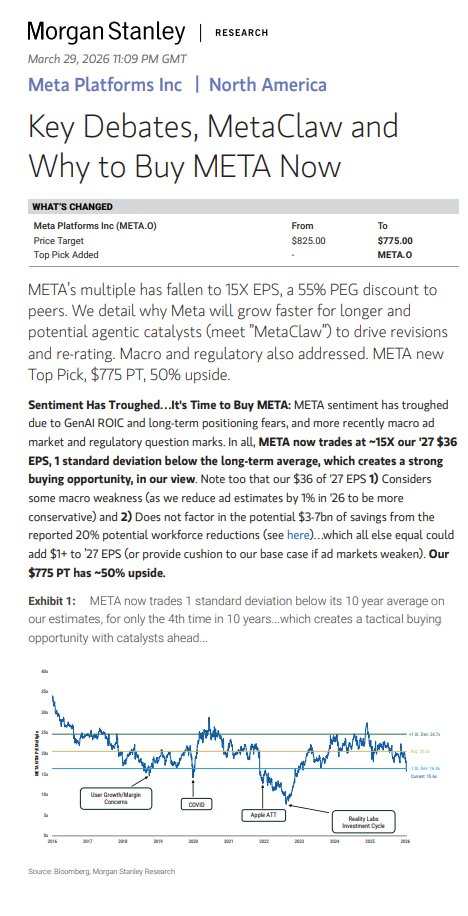

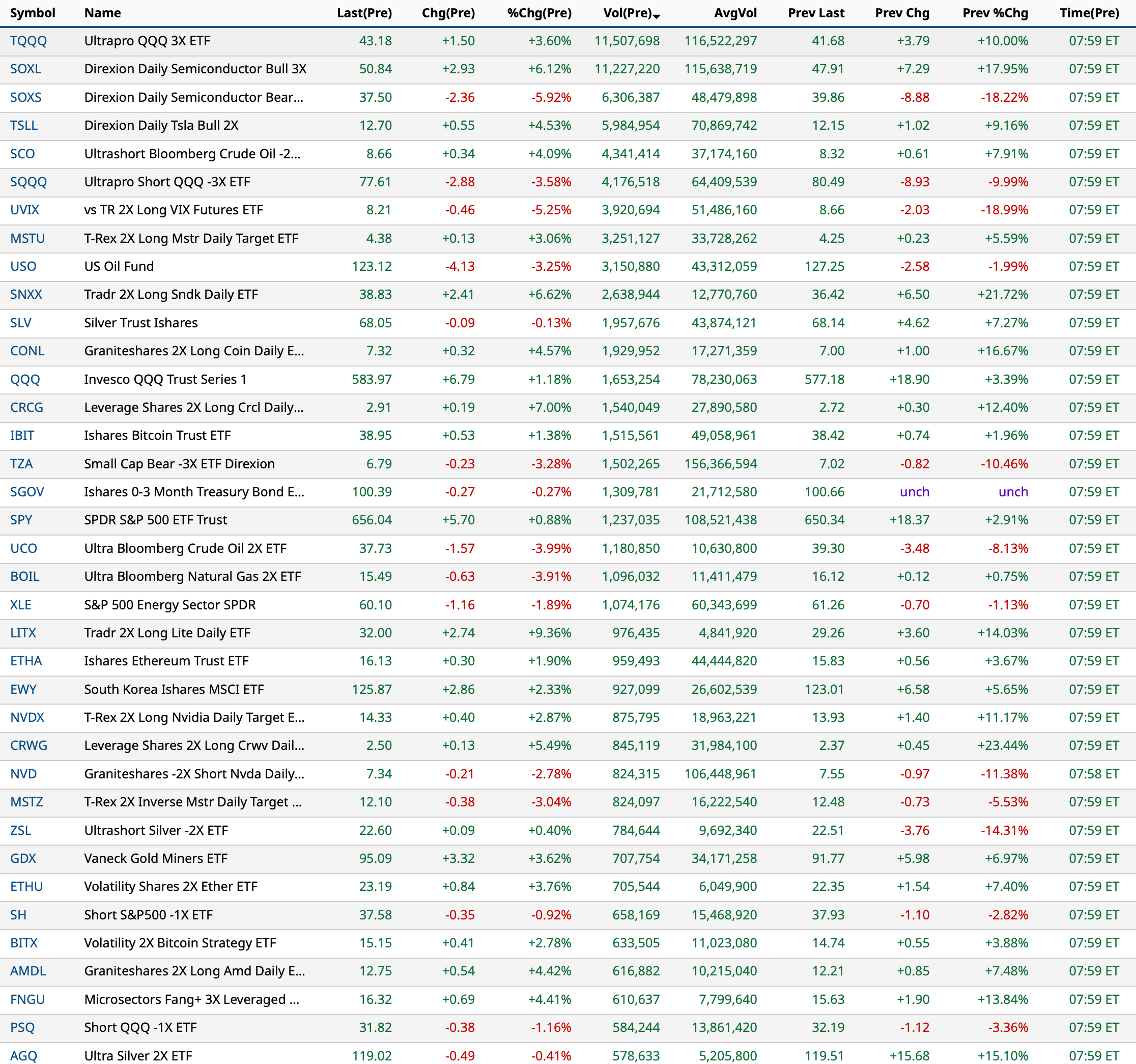

None.