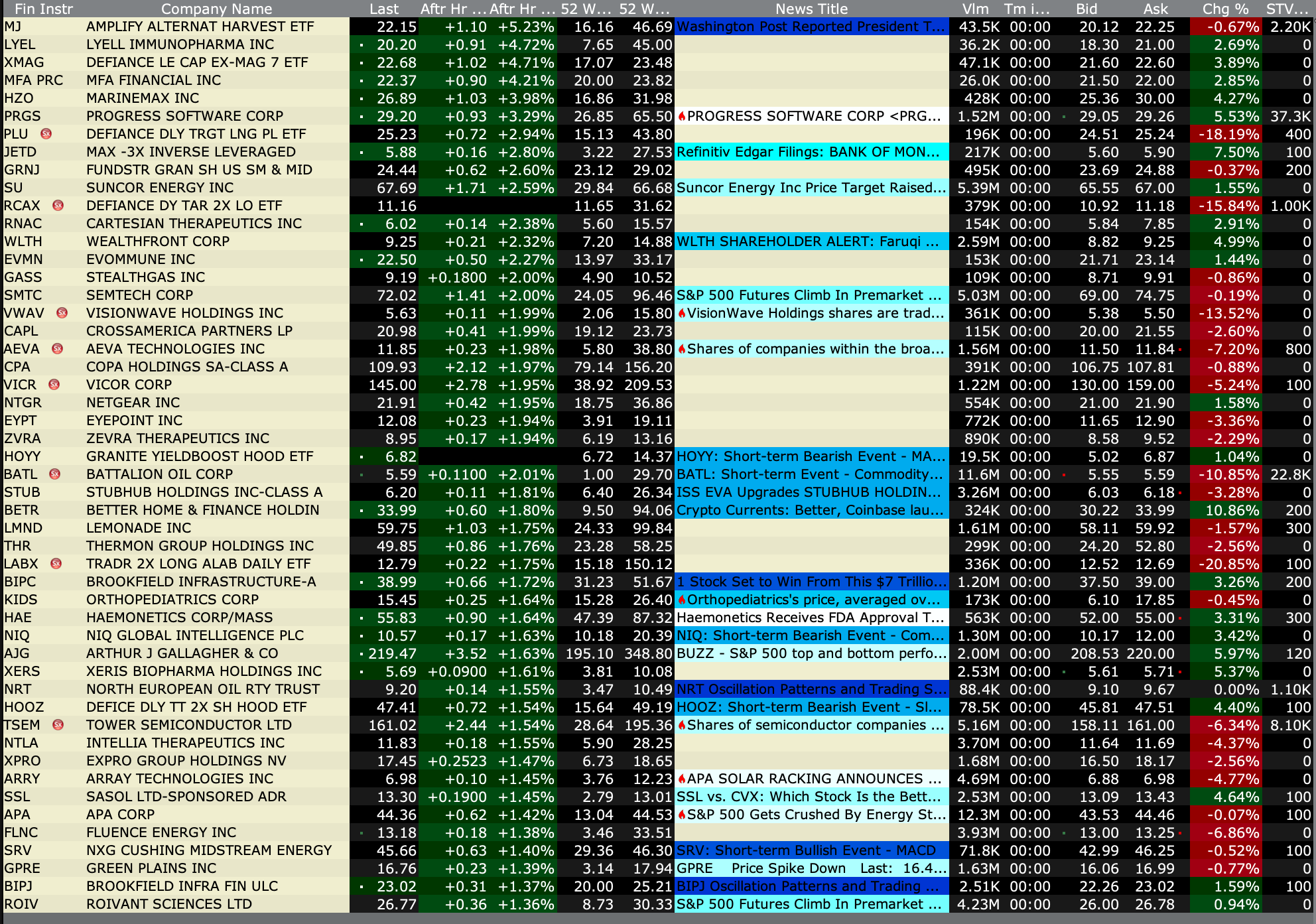

Monday's After-Hours Advancers and Decliners

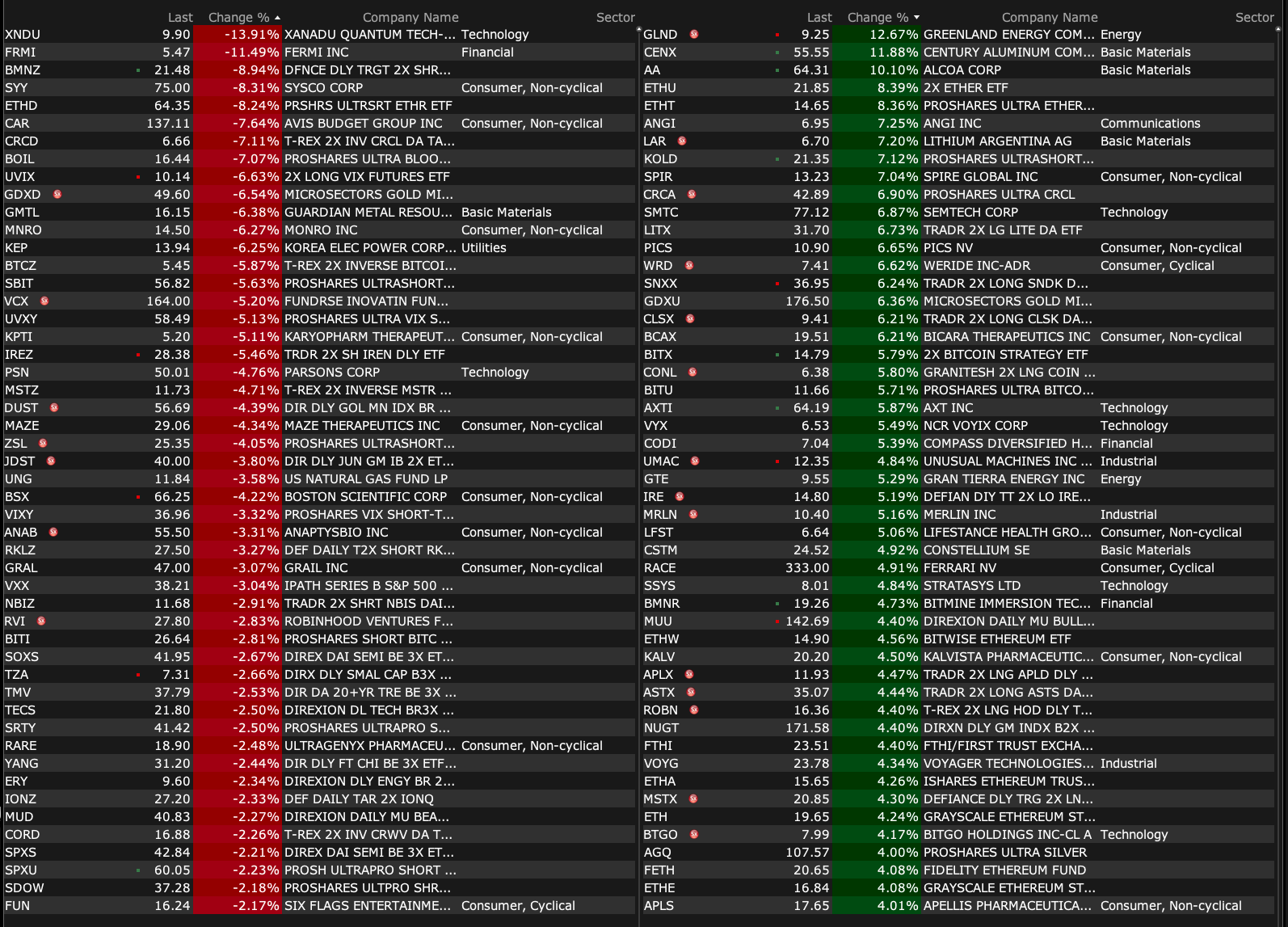

After-Hours % Advancers

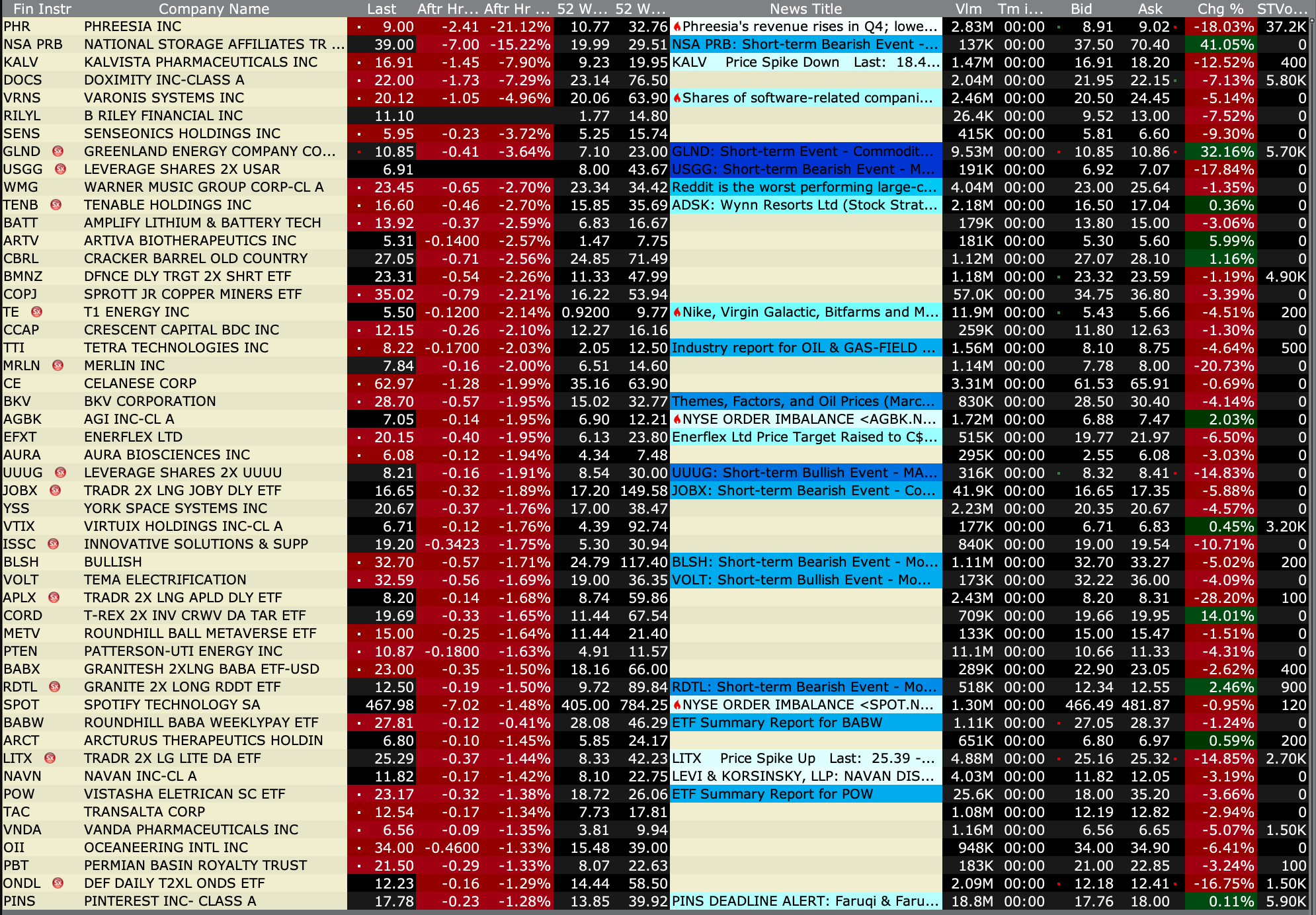

After-Hours % Decliners

BY Doug Kass · Mar 30, 2026, 4:40 PM EDT

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Mar 30, 2026, 4:40 PM EDT

Closing Volume

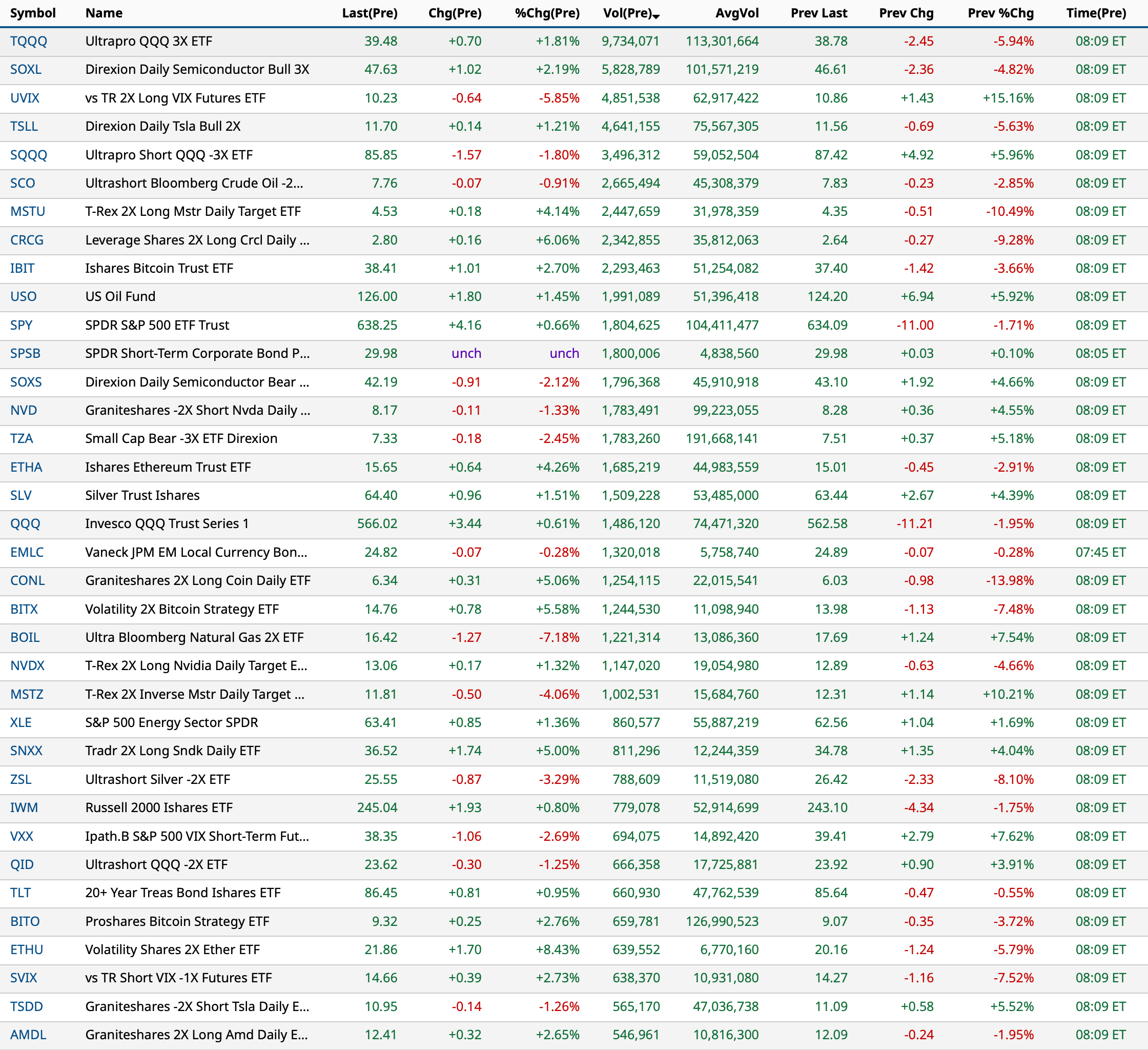

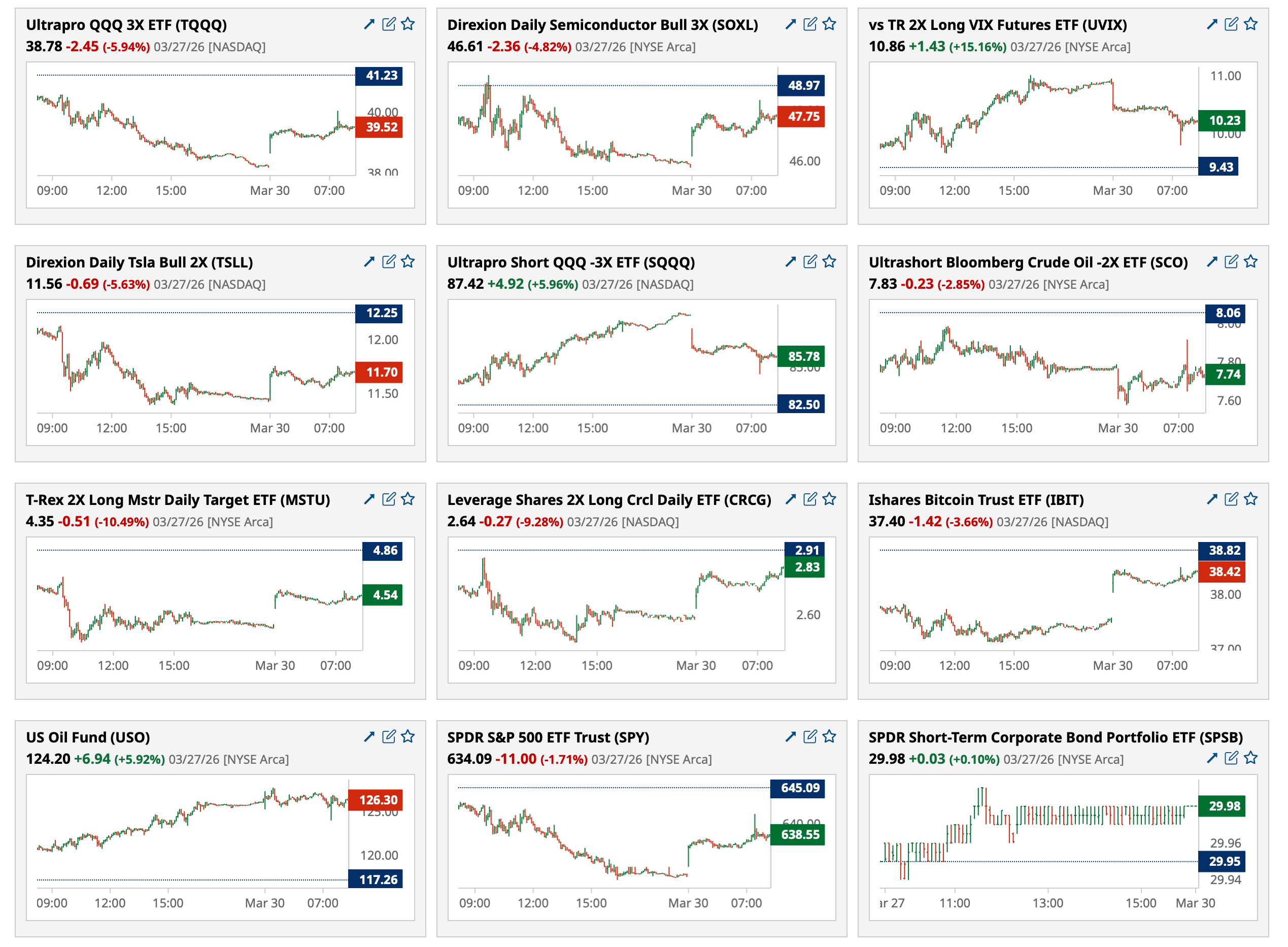

- NYSE volume 3% below its one-month average

- NASDAQ volume 4% above its one-month average

- VIX index: down 1.96% to 30.44

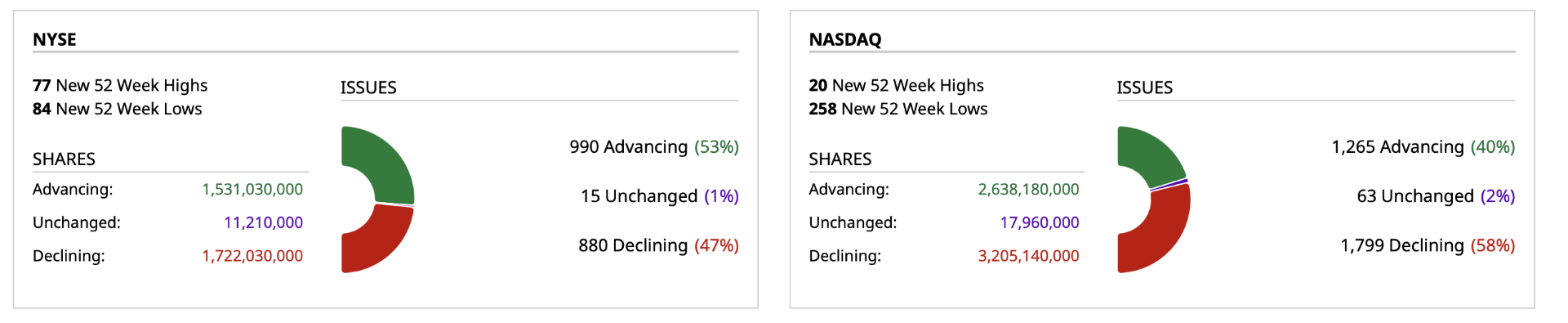

Breadth

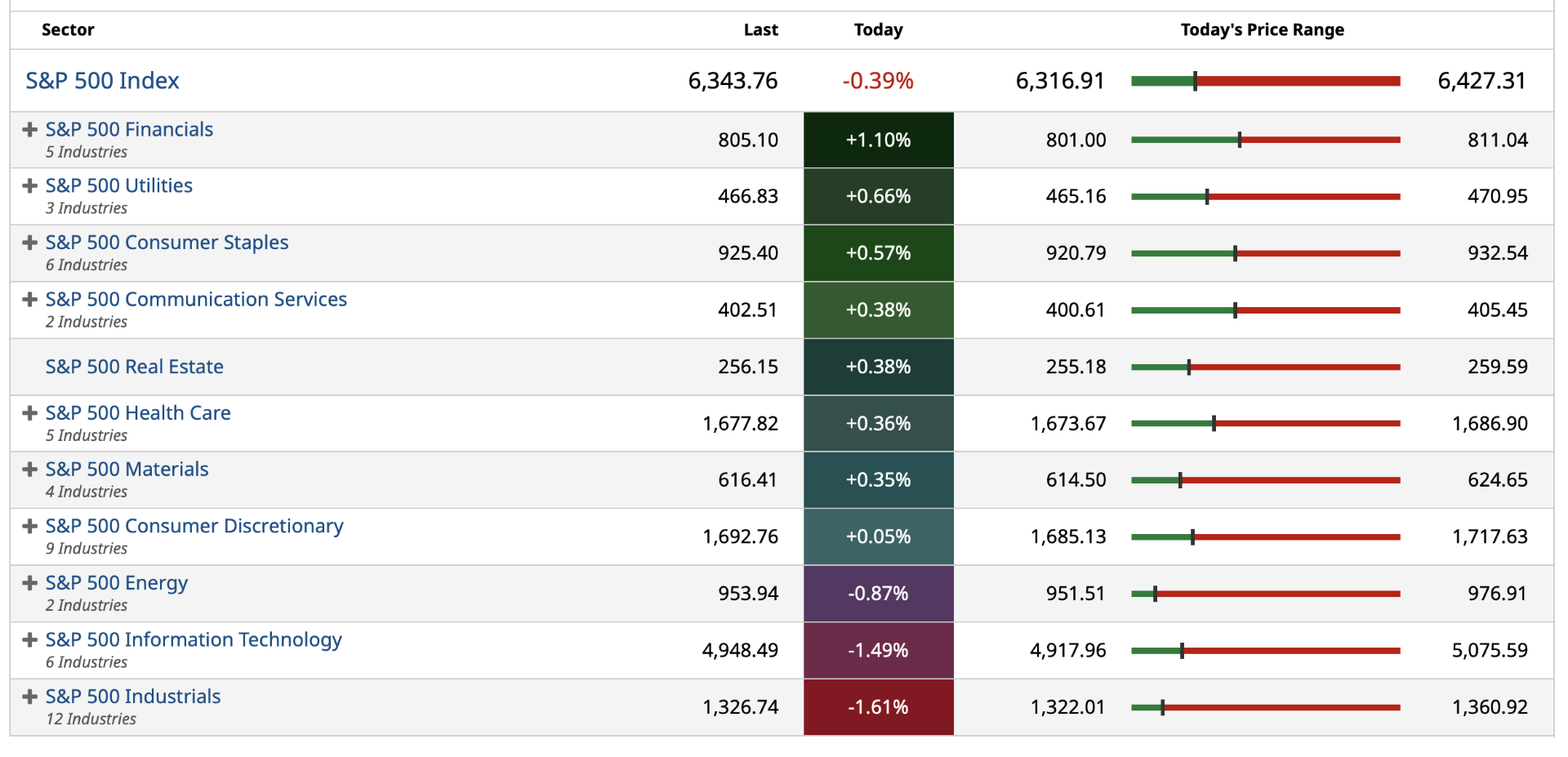

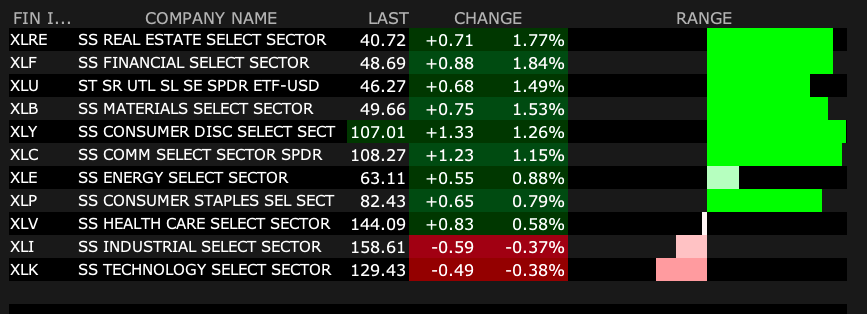

S&P 500 Sectors

% Movers

Nasdaq 100 Heat Map

Closing S&P 500 Heat Map

BY Doug Kass · Mar 30, 2026, 4:30 PM EDT

I added to Amazon (AMZN) at $200.35.

Position: Long AMZN (M)

BY Doug Kass · Mar 30, 2026, 4:02 PM EDT

The White House has scheduled four meetings for April 1 and 2 as officials review a new FDA CBD enforcement policy. https://t.co/fBslbmV8sF

— Anthony Martinelli (@AMartinelliWA)

BY Doug Kass · Mar 30, 2026, 4:00 PM EDT

Systematic selling of US equities may be running out of steam:

— The Kobeissi Letter (@KobeissiLetter)

Commodity Trading Advisors (CTAs), the algorithm-driven funds that buy and sell based on price trends, have sold -$85 billion in US equities over the last 30 trading sessions.

This marks the largest 30-day sale… pic.twitter.com/2MiiLMcFHk

BY Doug Kass · Mar 30, 2026, 2:00 PM EDT

I added to Microsoft (MSFT) at $359.23.

Position: Long MSFT (M)

BY Doug Kass · Mar 30, 2026, 1:52 PM EDT

I am taking my older doxie to the vet.

I will be out between 2:30 PM and the close.

BY Doug Kass · Mar 30, 2026, 1:45 PM EDT

I just added to my long index positions:

* (SPY) $635.08

* (QQQ) $561.91

Position: Long SPY common (M), QQQ common (M); Short SPY calls (S), QQQ calls (S)

BY Doug Kass · Mar 30, 2026, 1:37 PM EDT

Long adds this morning:

* (UNH) $258.14

* (MSOS) $3.37

* (UBER) $69.73

Position: Long UNH (S/M), MSOS (L), MSOX (S), UBER (S)

BY Doug Kass · Mar 30, 2026, 12:47 PM EDT

None.

BY Doug Kass · Mar 30, 2026, 11:20 AM EDT

Run, don't walk to watch Carter, Dan and Guy on MRKT CALL at 11 AM.

I watch them daily.

This is a very worthwhile 45 minute podcast - containing actionable ideas and candid economic/market/company commentary. (And they admit their mistakes!)

Let's go to the tape. MRKT Call - Monday, March 30th

none.

BY Doug Kass · Mar 30, 2026, 11:05 AM EDT

From Peter Boockvar:

We remain in this escalation spiral in terms of military strikes but with the unfortunate reality that the Iranian regime is not going to change, we are also seemingly days/weeks away from this being over. In part because instead of talking about price increases in a variety of key things, we’re now talking about Covid like shortages around the world that are hugely economically damaging.

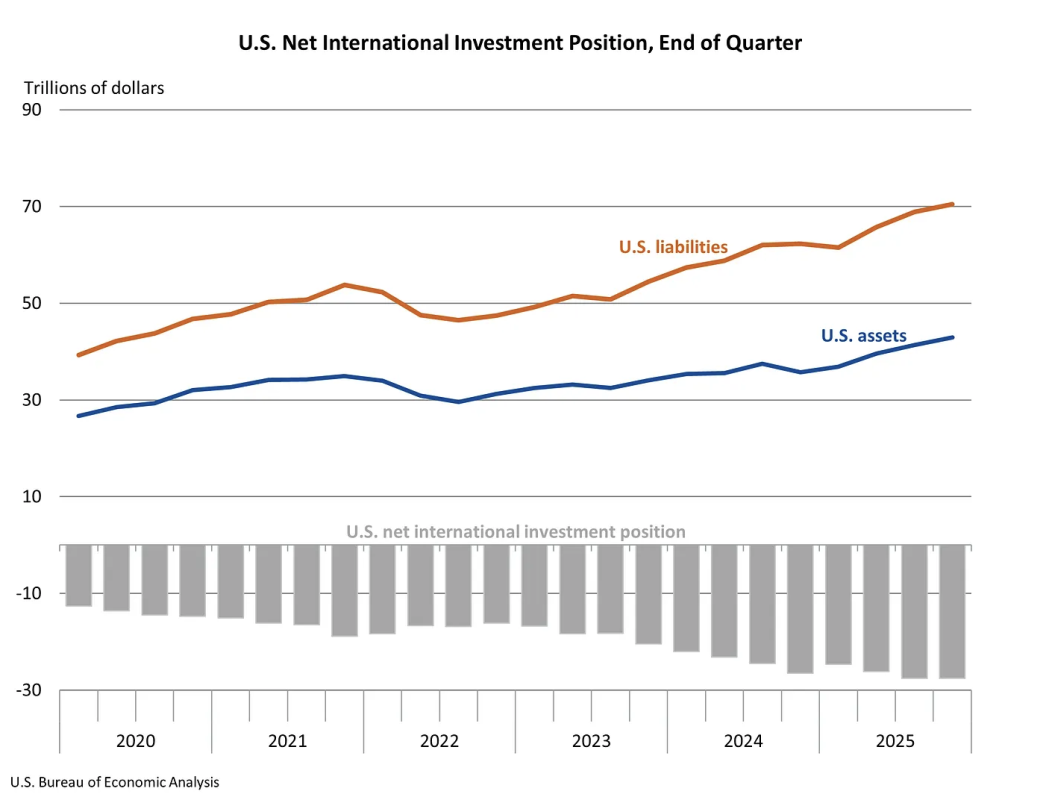

I do want to point out that part of the selloff in US stocks and Treasuries is not just due to worries about the growth and inflationary impact of what is going on but US markets are a source of funds for the rest of the world because of the huge amount of foreign ownership of US assets. According to the US government, the net international position of the US was -$27.55 trillion as of Q4 2025, meaning that foreign investors owned $27.55 trillion more of US assets than the US owned in foreign assets. These numbers came out last week. See the chart below. Specifically, foreigners own about 30% of US marketable Treasuries and we also know that the Mag 7 stocks became also a reserve asset for them. These are now a source of funds for countries needing the money. We’ve already seen Turkey liquify thru a swap some of its gold holdings in order to buy lira to stem its fall. www.bea.gov/

When it comes to sentiment, we are ripe for a big rally, upon the end of this, as seen with Friday’s close in the CNN Fear/Greed index which is down to 10. I believe it got as low as 3 in March/April 2020 in the teeth of you know what. www.cnn.com

Some more notable things I’m seeing in response to the war. Stupid is as stupid does is how it’s best described of Germany’s decision years ago to close its remaining nuclear facilities. Last Thursday I saw this Bloomberg News story, “Germany discusses firing up coal reserves to cut energy costs.”

On Friday I saw a Reuters story titled “From beer to cosmetics, Asia feels full force of war fueled energy crisis.” They quote Choi Gun-soo, “the manager of a 57 year old South Korean factory that makes plastic films used by farmers to cover crops as well as by television manufacturers, said his suppliers were raising prices of some raw materials as much as 50%, while other suppliers had simply run out of stock.” He went on to say, “Since we’re out of raw materials for some products, we’ll have to gradually shut down the machines, and the next one to two weeks is likely to very critical.”

More, and something I mentioned last week from a Nikkei News story, “The most acute shortages right now are in oil derivatives such as naphtha, sourced predominantly from the Gulf and used in refineries across Asia to make the plastics and other petrochemicals that go into almost every manufactured product.”

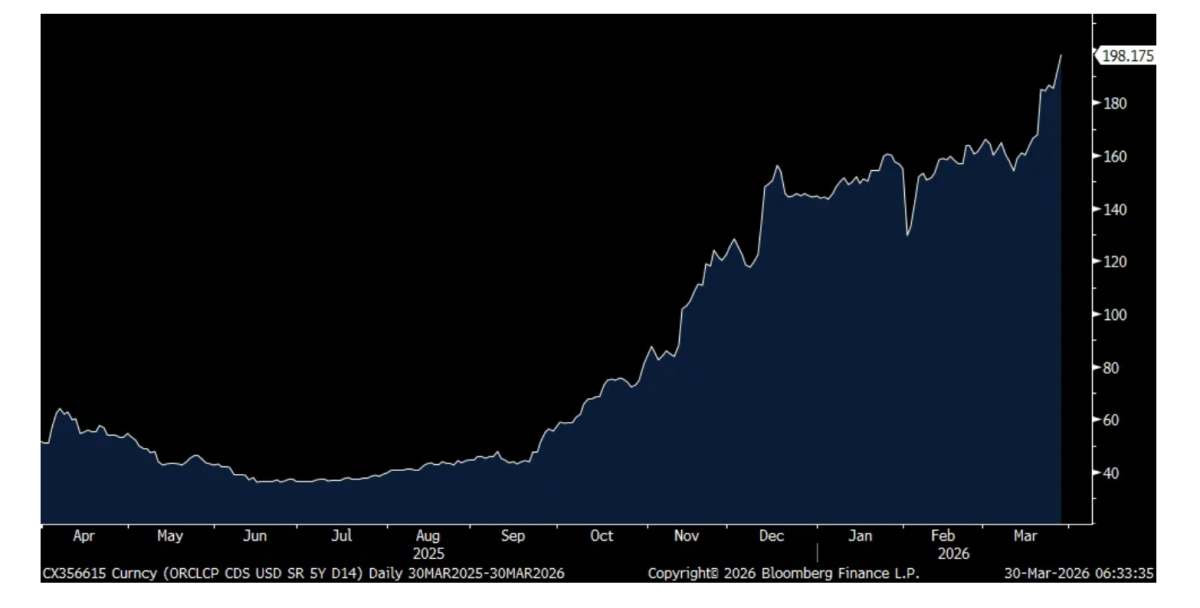

We also are hearing more stories about the growing helium shortage and what that means for semiconductor production. Directly impacting the AI buildout but a trend that was clearly in place before the war, the 5 yr CDS of Oracle further blew out Friday to 198 bps. Meaning that for $10 million of bond insurance, it now costs $198,000 to insure against it vs about $51,000 one year ago.

Oracle 5 yr CDS

This is what Hapag Lloyd said Friday on their earnings call about what they’re seeing:

“We have suspended all transit through the Strait of Hormuz, also through the Red Sea, where we were actually getting closer to returning to the Red Sea. We’ve stopped all bookings from and to the Upper Gulf region, simply because we cannot move the boxes. We are adjusting our network. We continue to offer the connection from Asia to the Middle East, even if in some cases it now goes with a different routing. Costs are increasingly sharply. I mean, if we look at the impact that this has on us, then we talk easily about $40 million to $50 million per week that we are facing at this point in time, mainly related to bunker (fuel), but also insurance costs are up significantly and so are costs related to storage and in some cases, also inland transportation.”

Carnival reported Friday and said this of note:

Business is great but fuel costs keep rising. “Turning to our business, we are off to an excellent start to the year. First quarter results came in ahead of guidance, thanks to higher yields and better cost performance, reflecting healthy fundamentals and solid execution across the business. Close-in demand remained robust, guests continued to spend more onboard and pricing strengthened...We’re seeing this momentum continue in onboard and pre-cruise sales.”

Also, “Guests are engaging earlier in the vacation journey, purchasing more inclusive packages, excursions and other experiences before they even step onboard...We’re also seeing it in our bookings. Bookings for current year sailings increased 10% y/o/y, adding to our record book position for the remainder of the year at historically high prices. With nearly 85% of 2026 already on the books and less inventory available than this time last year, we remain well positioned to keep improving yields as the year unfolds. Cumulative future year bookings also reached a first quarter record, adding to our continued confidence in the trajectory of the business.”

Higher fuel costs though are going to cost them an additional $500 million off an EBITDA base of $7 billion. The CFO said “A 10% change in our fuel cost per metric ton excluding emission allowances for the remainder of the year impacts our bottom line by $160 million or $.11 per share.”

Also last week was earnings from Winnebago, the RV maker and they said this:

“Retail activity across the second quarter remained aligned with a seasonally slower retail period of the year, but also reflected a challenged near term consumer sentiment environment, with comps lower than the same period a year ago. Additionally, retail both at the dealers but also at certain consumer retail shows through the January-February months were impacted by adverse weather events in key regions.”

“Dealers continue to manage inventory cautiously, keeping ordering and stocking closely aligned with retail conditions. Wholesale activity has remained disciplined, with shipments also moderating throughout the seasonally slower period. The RV Industry Association’s Spring Road Signs Outlook calls for modest industry shipment growth in calendar 2026, with total volumes forecast to increase by approximately 2% y/o/y. That outlook continues to assume a first half of calendar year 2026 weighted towards seasonal softness, with improvement expected in the back half of the year as retail demand stabilizes. It also assumes mixed performance across segments, including resilience in fifth wheels and a more gradual recovery in certain motorized categories.”

“Our own internal RV wholesale planning remains intentionally more cautious than this outlook, with a focus on retail driven ordering patterns and disciplined production pacing as conditions evolve.”

Last Friday we also saw the Apartment List National Rent Report for March and rents rose .4% m/o/m, getting a seasonal lift, up for a 2nd month though still down 1.7% y/o/y for new leases, not including renewals. The vacancy rate held at 7.3%, “a record high for our index going back to 2017.” Understand though that this is mostly due to the large amount of supply.

“The most important driver behind the soft market conditions that have persisted for three years is a historic surge of multifamily construction. Today, we’re past the peak of that supply wave, but not entirely through with it.”

Austin remains the weakest market with rents down 6% while Virginia Beach right now is the best, up 5.5% y/o/y. San Francisco is the second best market after badly lagging coming out of Covid.

The bottom line from them, “Eventually, the market will absorb the swell of new units, and occupancy and pricing trends should begin to gradually tighten. But for now, conditions remain soft, and if anything, the runway for these sluggish conditions is likely only lengthening.”

Lastly, understand too that most of the excess supply is in the sunbelt markets and mountain regions like Denver. “Meanwhile, many markets in the Northeast, Midwest, and parts of the West Coast continue to see prices trend up despite the winter slowdown.”

None.

BY Doug Kass · Mar 30, 2026, 10:30 AM EDT

Added to indexes;

* (SPY) $635.25

* (QQQ) $562.55

Long SPY common M QQQ common M

Short SPY calls S QQQ calls S

BY Doug Kass · Mar 30, 2026, 10:07 AM EDT

I added to my Index longs:

* (SPY) $636.15

* (QQQ) $563.93

Long SPY common M QQQ common M; Short SPY calls S QQQ calls S

BY Doug Kass · Mar 30, 2026, 9:57 AM EDT

* "Happy Dogwood Sunday"

Here's a funny childhood story that I produce annually to take us all into last weekend's Palm Sunday and next weekend's Easter holiday:

I'm reminded at this time every year (by my famous artist sister Debbie) of a true story that occurred in the late 1950s when I was about 10 years old.

When I was in fourth grade at my Rockville Centre, Long Island, N.Y., elementary school, the students were notified of a "special assembly" to be held that afternoon.

When we all arrived in the auditorium, there was a woman on the stage in a chair who explained that she was an NBC representative for a TV quiz show called Tic-Tac-Dough, which aired at that time in New York on Channel 4.

She went on to explain that Tic-Tac-Dough, the predecessor show to Hollywood Squares (which used the same concept), was looking for two students to represent Long Island on the show during Christmas vacation week. (Adults participated on the show the rest of the year.)

She began to ask the students questions, but I was shy and never raised my hand. But in response to a question, my buddy Jo Anne Zerillo raised her hand and said she didn't know the answer but "The Professor" (my nickname then!) might. She pointed at me.

I answered the question and then another, and was notified that I had been selected along with my friend and classmate Carrie Spivak to represent our area on Tic-Tac-Dough.

Jack Barry, a fellow Long Islander and a Wharton graduate (as I would later be), was the host and (along with Dan Enright) the show's producer.

If you remember Jack Barry, it's probably because his production company was responsible for the scandal-ridden game show Twenty One. It turns out that Charles Van Doren and champion Herb Stempel were provided with answers to Twenty One's questions in advance after principal advertiser Geritol complained that the unrigged production was dull and boring.

Barry's production company later created other game shows like Dough Re Mi, Winky Dink and You (reputedly the world's first-ever interactive TV program), the fabulously successful Concentration and the long-running Joker's Wild.

I went on Tic-Tac-Dough several weeks later and won my first six games, breaking a record for the show.

But in the seventh game, I selected the box "Holidays" and was asked by Jack Barry to name the Sunday before the Easter holiday. He went on to say that the holiday was the name of a tree.

The music played in the background and after waiting about 10 or 15 seconds, Mr. Barry asked if I knew the answer.

I thought long and hard, but had no idea of the answer. So I figured I should take a shot and guess the answer, as I already knew the holiday had the name of a tree in it.

Under pressure from Mr. Barry, I said: "Dogwood Sunday."

As the words came out of my mouth, I could hear my mother and Grandma Koufax (who were in the audience) gasp. My mom, clear as day, said, "Oh, no!" (I can still hear her words as if it were yesterday.)

I instantly knew it was the wrong answer and said — I swear I did! — "No, Mr. Barry. It's Redwood Sunday!"

Jack Barry, was in front of a pyramid of empty Crest toothpaste boxes that were stacked up in preparation for a commercial later on in the show. (The "Look Ma, No Cavities!" commercial was initially aired on Tic-Tac-Dough.)

Barry then said, "Doug, I am sorry. That is the wrong answer. The correct answer is Palm Sunday. Haven't you ever heard of Palm Sunday, the Sunday before Easter?"

I immediately said — remember, this was live television — "No, Mr. Barry. I never heard of Palm Sunday. I am Jewish."

Barry, who was also Jewish, fell over laughing right into the boxes of Crest toothpaste, which all fell down into a mess.

I hope you enjoyed the story about Dogwood — er, I mean, Redwood — Sunday.

I will never forget the experience, and I have the tape of the week's appearances to prove it. (My office has been listening to them all day).

In this holiday spirit, I want to be the first to wish a Happy Dogwood Sunday, Holy Week and Happy Easter to my family, all of my friends, subscribers, contributors, editors, and the entire TheStreet Pro management team!

Position: None

BY Doug Kass · Mar 30, 2026, 9:55 AM EDT

I am long FNMA and FMCC:

The math on Fannie and Freddie is so dislocated it looks like a pricing error.

— Aakash Gupta (@aakashgupta)

Fannie printed $14.4 billion in net income last year. Freddie printed $10.7 billion. Combined market cap on the pink sheets right now: ~$12 billion. The market is pricing $25 billion in annual… https://t.co/7u1xxlrDrz

Long FNMA S FMCC S

BY Doug Kass · Mar 30, 2026, 9:45 AM EDT

-ELAB +150% (wholly-owned subsidiary NorthStrive Biosciences signs Licensing Agreement Amendment with MOA Life Plus [KOSDAQ: 142760] for Dual Myostatin Assets Targeting Muscle Preservation in Combination with GLP-1 Treatments)

-EEIQ +56% (momentum)

-ASTC +40% (momentum)

-SGML +25% (earnings, guidance)

-UTHR +17% (Nebulized Tyvaso (treprostinil) Inhalation Solution meets primary endpoint for treatment of Idiopathic Pulmonary Fibrosis; Plans to seek priority review of Tyvaso sNDA by end of summer)

-AA +11% (two Middle East peers hit by Iranian strikes creating supply disruption concerns)

-INSM +5.9% (Morgan Stanley Raised INSM to Overweight from Equal Weight, price target: $212 from $166)

-CRWD +5.7% (Hearing Wolfe Research raised CRWD to Outperform from Peer Perform, price target: $450)

-TSSI +5.3% (Needham Initiates TSSI with Buy, price target: $16)

-SPIR +4.9% (momentum)

-RACE +4.8% (hearing of constructive commentary from JPM)

-FLEX +4.2% (to acquire Electrical Power Products for $1.1B in cash deal expected to close in Q1 2027)

-PTON +3.6% (strength attributed to positive comments from Erik Jackson on X)

-SNDK +3.6% (memory weakness)

-PANW +3.5% (CEO purchases $10M in shares)

-PCRX +2.7% (will present data on EXPAREL at Orthopaedic Research Society 2026 Annual Meeting)

-EXPE +2.6% (hearing Jefferies Raised EXPE to Buy from Hold, price target: $300)

-SOC +2.5% (starts oil sales through Santa Ynez Pipeline; Heritage restart today; Hondo expected by end of Q2 2026)

-MU +2.4% (memory weakness)

-VRDN -38% (Elegrobart REVEAL-1 Phase 3 trial data)

-CAR -7.2% (enters 5M share equity distribution agreement)

-SYY -6.2% (confirms to acquire Jetro Restaurant Depot for $29B; affirms FY26 guidance)

-BSX -4.5% (Raymond James Cuts BSX to Outperform from Strong Buy, price target: $88)

BY Doug Kass · Mar 30, 2026, 9:41 AM EDT

None.

BY Doug Kass · Mar 30, 2026, 9:14 AM EDT

None.

BY Doug Kass · Mar 30, 2026, 9:09 AM EDT

11:30 a.m.: Treasury hosts a $89B 3 and a $77B 6-Month Bill Auction

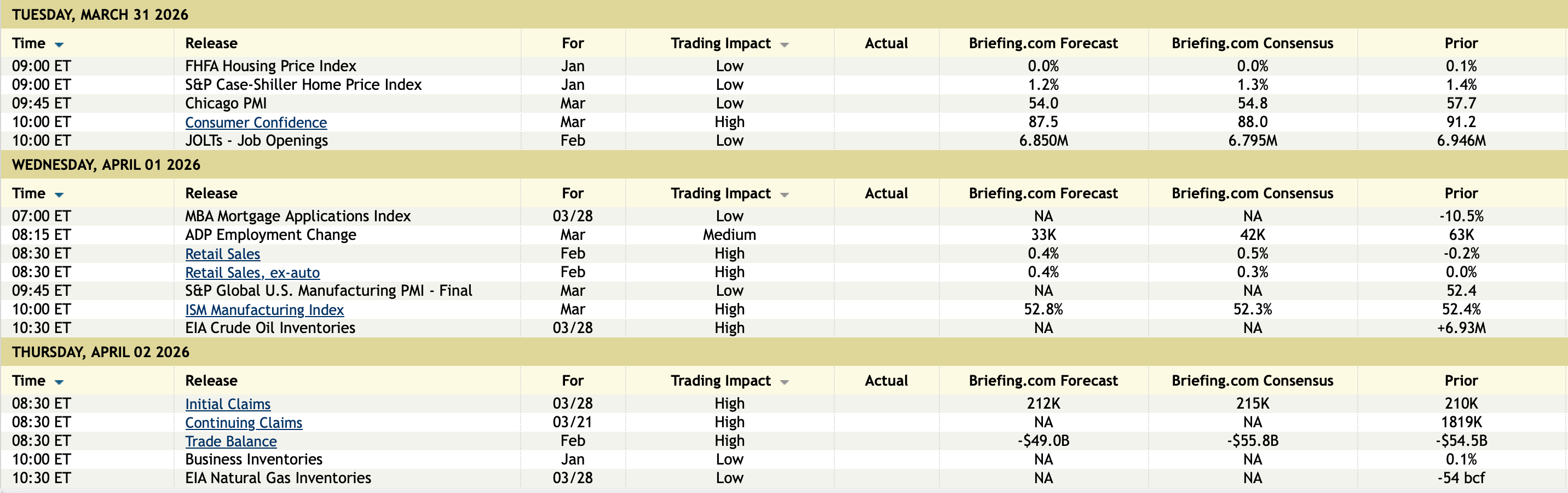

10:30 a.m.: Fed Chair Powell participates in a moderated discussion at Harvard University, Boston, MA (Audience questions expected);

4:00 p.m.: Fed Bank of New York President Williams (Voter) participates in conversation at event organized by the Staten Island Economic Development Corporation, Staten Island, NY (Text and moderated Q&A expected)

None.

BY Doug Kass · Mar 30, 2026, 8:59 AM EDT

I have long argued that changing market structure poses risk to equities, as with so many worshiping at the altar of price (and momentum), too many were on the same side of the "long" boat.

Now the movie is in reverse, as momentum-based funds dump equities:

Global CTAs dumped $190 Billion worth of stocks over the last month, the fastest pace of selling since Covid 📉🚨 pic.twitter.com/HSIKfXoP8B

— Barchart (@Barchart)

As to the "cash on the sidelines" argument it was always a convenient and non rigorous crutch for perma bulls in a maturing bull market (in which valuations went sky high).

Though promulgated by "talking heads" on the shows (and prominently by Fundstrat's Tom Lee)... the "cash on the sidelines" argument was B.S. from the get go.

None

BY Doug Kass · Mar 30, 2026, 8:45 AM EDT

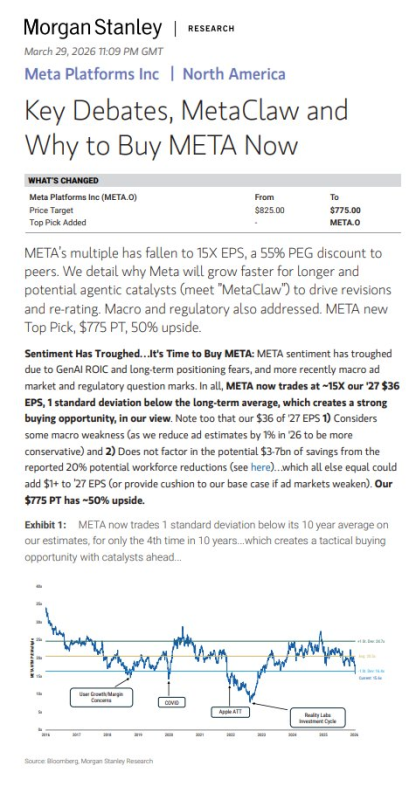

For only the fourth time in the last decade, META's valuation is one standard deviation below its average P/E ratio....

I am generally in agreement with Morgan Stanley's buy recommendation on (META) (over the weekend):

Mag-7 $MAGS -5% last week, worst week since April and fifth straight weekly loss (now down nearly -19% from the December closing high). $NVDA $META $MSFT $AMZN pic.twitter.com/UahCVmAE3c

— Special Situations 🌐 Research Newsletter (Jay) (@SpecialSitsNews)

Long META S/M

BY Doug Kass · Mar 30, 2026, 8:35 AM EDT

BY Doug Kass · Mar 30, 2026, 8:28 AM EDT

It's hard to overemphasize how important tech is to this market, so here's a statistic that helps to drive it home.

— Markets & Mayhem (@Mayhem4Markets)

Tech is expected to account for a whopping 87% of annual S&P 500 earnings growth in Q1.

As goes tech, so too goes the market. pic.twitter.com/FW5gWDABB2

BY Doug Kass · Mar 30, 2026, 8:15 AM EDT

#Iran War Update No. 30 (focus on Iranian strategic narrative):

— Hamidreza Azizi (@HamidRezaAz)

🔹Iranian strategic assessments increasingly point to a prolonged conflict, with expectations that the war could last at least eight more weeks and may escalate further, including the potential deployment of U.S.…

BY Doug Kass · Mar 30, 2026, 8:05 AM EDT

From Bramo:

Brent crude is up about 58% so far this month, the biggest monthly gain on record. pic.twitter.com/I3abtgACtw

— Lisa Abramowicz (@lisaabramowicz1)

BY Doug Kass · Mar 30, 2026, 7:55 AM EDT

Maybe there is some value in GenAI after all:

One way I’ve integrated AI into the classroom is that I begin each class by having students take out their laptops, open up Claude, and talk to it about whatever for 45 minutes while I go outside and vape.

— Paul Schofield (@pschofie79)

BY Doug Kass · Mar 30, 2026, 7:45 AM EDT

🇺🇸 Valuations

— ISABELNET (@ISABELNET_SA)

With the Russell 2000 and Nasdaq 100 trading at 24 times forward earnings and the S&P 500 at 20, the market's appetite for growth hasn't faded

👉 https://t.co/14i5SQVCfd@GoldmanSachs $spx #spx $ndx $qqq $rut #stocks #equity pic.twitter.com/S9ZKlJRVEh

BY Doug Kass · Mar 30, 2026, 7:35 AM EDT

Hard work beats talent when talent doesnt work hard.

— Dougie Kass (@DougKass)

Buffett outworked everyone. Most people know he read the Moody's Manual front to back. Twice. But did you know he brought Moody's Manuals on his honeymoon? He copied balance sheets by hand, because Standard and Poor's had… https://t.co/PzYglXaEv7

BY Doug Kass · Mar 30, 2026, 7:25 AM EDT

I have taken an initial LONG investment position in Uber (UBER) ($69.75)

More on my analysis later in the week.

Position: Long UBER (S)

BY Doug Kass · Mar 30, 2026, 7:15 AM EDT

* Bill Ackman is...

Some of the highest quality businesses in the world are trading at extremely cheap prices. Ignore the MSM. One of the most one-sided wars in history that will end well for the U.S. and the world. And we have the potential for a large peace dividend.

— Bill Ackman (@BillAckman)

One of the best times in a…

and...

I’m warning you…fade Ackman at your own peril. I checked, and the other times he tweeted that stocks are very cheap were March 2020 (bottom), October 2022 (bottom), and April 2025 (bottom) https://t.co/WTFmGqepUw

— DG (@gordocap18)

BY Doug Kass · Mar 30, 2026, 7:05 AM EDT

In the early going on Monday morning, President Trump buoys futures with some assurances:

*TRUMP SAYS INDIRECT TALKS VIA EMISSARIES PROGRESSING WELL: FT

— zerohedge (@zerohedge)

*TRUMP SAYS A DEAL COULD BE MADE 'FAIRLY QUICKLY': FT https://t.co/QDFkrJfH6U

BY Doug Kass · Mar 30, 2026, 6:55 AM EDT

I don't relish in others' disappointments but this is striking:

Bill Ackman manages $15.5 billion in AUM at Pershing Square. Estimated YTD loss is -19% of NAV vs. SP500 -7.14%. Here's his top 7 holdings by size:

— Stocks World (@anandchokshi19)

1. Brookfield: 18.15%

2. Uber: 15.90%

3. Amazon: 14.28%

4. Google: 12.46%

5. Meta: 11.37%

6. QSR: 9.47%

7. Canadian Pacific: 8.12%

Bill is thorough (in analysis) and I would use his holdings list as a menu of opportunities — particularly after the share-price declines.

BY Doug Kass · Mar 30, 2026, 6:45 AM EDT

With the risks apparent and as noted in my Diary I have been buying as the consensus has been selling:

The S&P 500 is down 7% in the first 59 trading days of 2026, the 14th worst start to a year in history. $SPX pic.twitter.com/giuunxMRVO

— Charlie Bilello (@charliebilello)

BY Doug Kass · Mar 30, 2026, 6:35 AM EDT

Q, $NVDA has been "overearning" for several years (2x, 3x even 4x over booking/ordering) - so it naturally seems inexpensive. (I have written 189 columns @thestreetpro @dougkass entitled "More Tales From Nvidia" over the last 15 months). @carlquintanilla

— Dougie Kass (@DougKass)

In those analyses I have… https://t.co/tcK4R5wmd9

BY Doug Kass · Mar 30, 2026, 6:25 AM EDT

Price increases since the start of the Iran war...

— Charlie Bilello (@charliebilello)

Heating Oil: +77%

European Natural Gas: +71%

Brent Crude Oil: +58%

WTI Crude Oil: +51%

Urea: +48%

Diesel: +44%

Sulfur: +43%

Gasoline: +42%

Fertilizer: +29%

Coal: +21%

Palm Oil: +14%

Iron Ore: +7%

Rice: +7%

US Natural Gas: +6%

BY Doug Kass · Mar 30, 2026, 6:15 AM EDT

BY Doug Kass · Mar 30, 2026, 6:05 AM EDT

Dougie Kass

Sunday night trading. Added to Indices:

* SPY $629.64

* QQQ $557.57

805PM

maircampbell

so, I need a tip on who I can trade with over night?

Dougie Kass

At 1219AM Monday morning...

Sold above Indices:

* SPY $634.30

* QQQ $562.82

Position: Long SPY common (M), QQQ common (M); Short SPY calls (S), QQQ calls (S)

BY Doug Kass · Mar 30, 2026, 5:55 AM EDT

The S&P Short Range Oscillator moved a bit more into oversold territory at -3.58% vs. -2.85%.

Position: Long SPY common (M), QQQ common (M); Short SPY calls (S), QQQ calls S

BY Doug Kass · Mar 30, 2026, 5:45 AM EDT

It's hard to overemphasize how important tech is to this market, so here's a statistic that helps to drive it home. Tech is expected to account for a whopping 87% of annual S&P 500 earnings growth in Q1. As goes tech, so too goes the market.

Systematic selling of US equities may be running out of steam: Commodity Trading Advisors (CTAs), the algorithm-driven funds that buy and sell based on price trends, have sold -$85 billion in US equities over the last 30 trading sessions. This marks the largest 30-day sale Show more

The math on Fannie and Freddie is so dislocated it looks like a pricing error. Fannie printed $14.4 billion in net income last year. Freddie printed $10.7 billion. Combined market cap on the pink sheets right now: ~$12 billion. The market is pricing $25 billion in annual Show more

And Fannie and Freddie are stupidly cheap. Asymmetry at its best. They could be a 10X and it could happen soon.

One way I’ve integrated AI into the classroom is that I begin each class by having students take out their laptops, open up Claude, and talk to it about whatever for 45 minutes while I go outside and vape.

Global CTAs dumped $190 Billion worth of stocks over the last month, the fastest pace of selling since Covid 📉🚨

The embedded tweet could not be found…

The White House has scheduled four meetings for April 1 and 2 as officials review a new FDA CBD enforcement policy. themarijuanaherald.com/2026/03/white-…

Some of the highest quality businesses in the world are trading at extremely cheap prices. Ignore the MSM. One of the most one-sided wars in history that will end well for the U.S. and the world. And we have the potential for a large peace dividend. One of the best times in a Show more

🇺🇸 Valuations With the Russell 2000 and Nasdaq 100 trading at 24 times forward earnings and the S&P 500 at 20, the market's appetite for growth hasn't faded 👉 isabelnet.com/?s=valuation @GoldmanSachs $spx #spx $ndx $qqq

Hard work beats talent when talent doesnt work hard. Buffett outworked everyone. Most people know he read the Moody's Manual front to back. Twice. But did you know he brought Moody's Manuals on his honeymoon? He copied balance sheets by hand, because Standard and Poor's had Show more

Top of the risk mgt morn

Brent crude is up about 58% so far this month, the biggest monthly gain on record.

Bill Ackman manages $15.5 billion in AUM at Pershing Square. Estimated YTD loss is -19% of NAV vs. SP500 -7.14%. Here's his top 7 holdings by size: 1. Brookfield: 18.15% 2. Uber: 15.90% 3. Amazon: 14.28% 4. Google: 12.46% 5. Meta: 11.37% 6. QSR: 9.47% 7. Canadian Pacific: 8.12%

*TRUMP SAYS INDIRECT TALKS VIA EMISSARIES PROGRESSING WELL: FT *TRUMP SAYS A DEAL COULD BE MADE 'FAIRLY QUICKLY': FT

*TRUMP SAYS COULD TAKE KHARG ISLAND 'VERY EASILY': FT *TRUMP THINKS IRANS HAVE NO DEFENSE ON KHARG ISLAND: FT

The S&P 500 is down 7% in the first 59 trading days of 2026, the 14th worst start to a year in history. $SPX

Price increases since the start of the Iran war... Heating Oil: +77% European Natural Gas: +71% Brent Crude Oil: +58% WTI Crude Oil: +51% Urea: +48% Diesel: +44% Sulfur: +43% Gasoline: +42% Fertilizer: +29% Coal: +21% Palm Oil: +14% Iron Ore: +7% Rice: +7% US Natural Gas: +6%

Q, $NVDA has been "overearning" for several years (2x, 3x even 4x over booking/ordering) - so it naturally seems inexpensive. (I have written 189 columns @thestreetpro @dougkass entitled "More Tales From Nvidia" over the last 15 months). @carlquintanilla In those analyses I have Show more