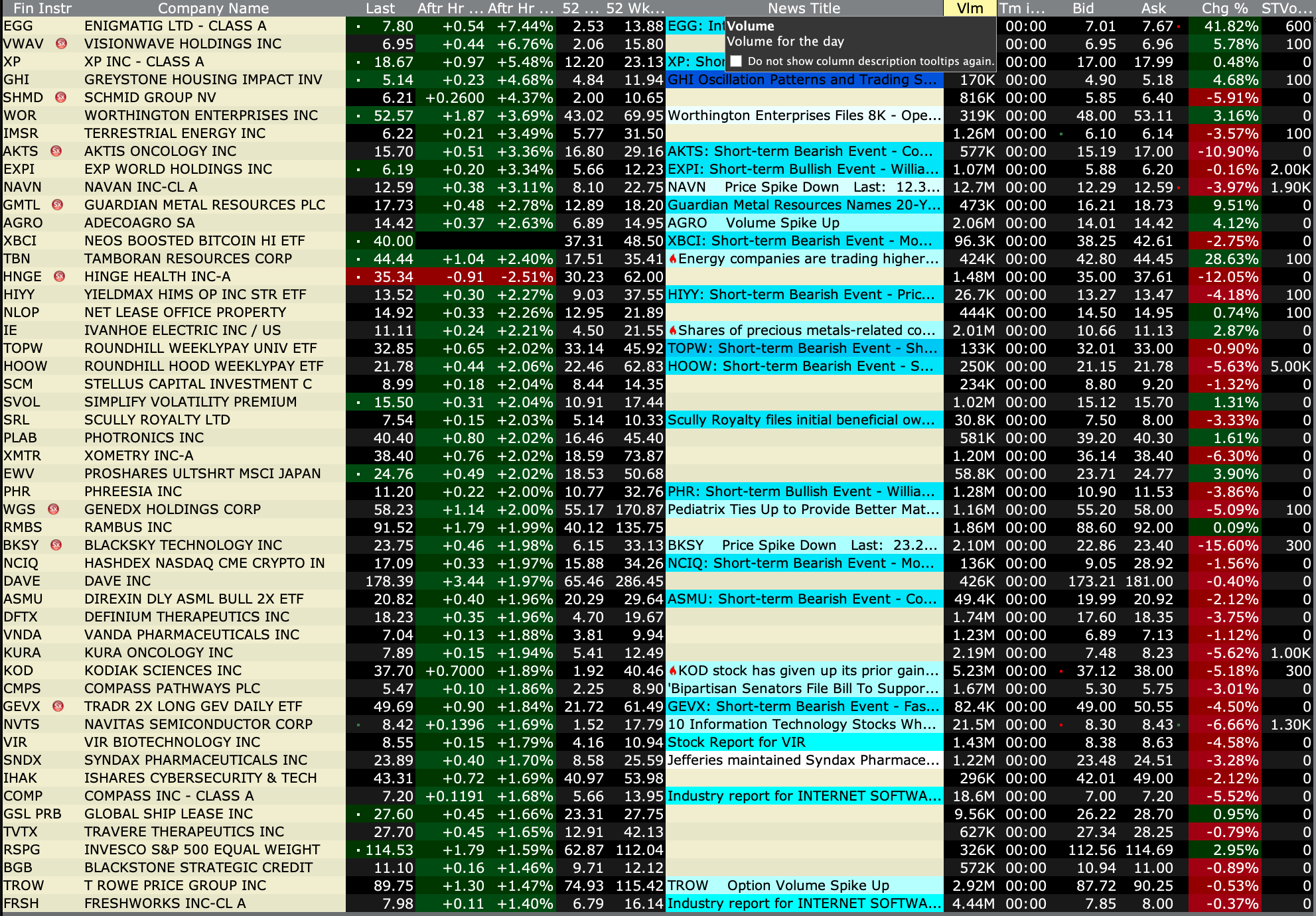

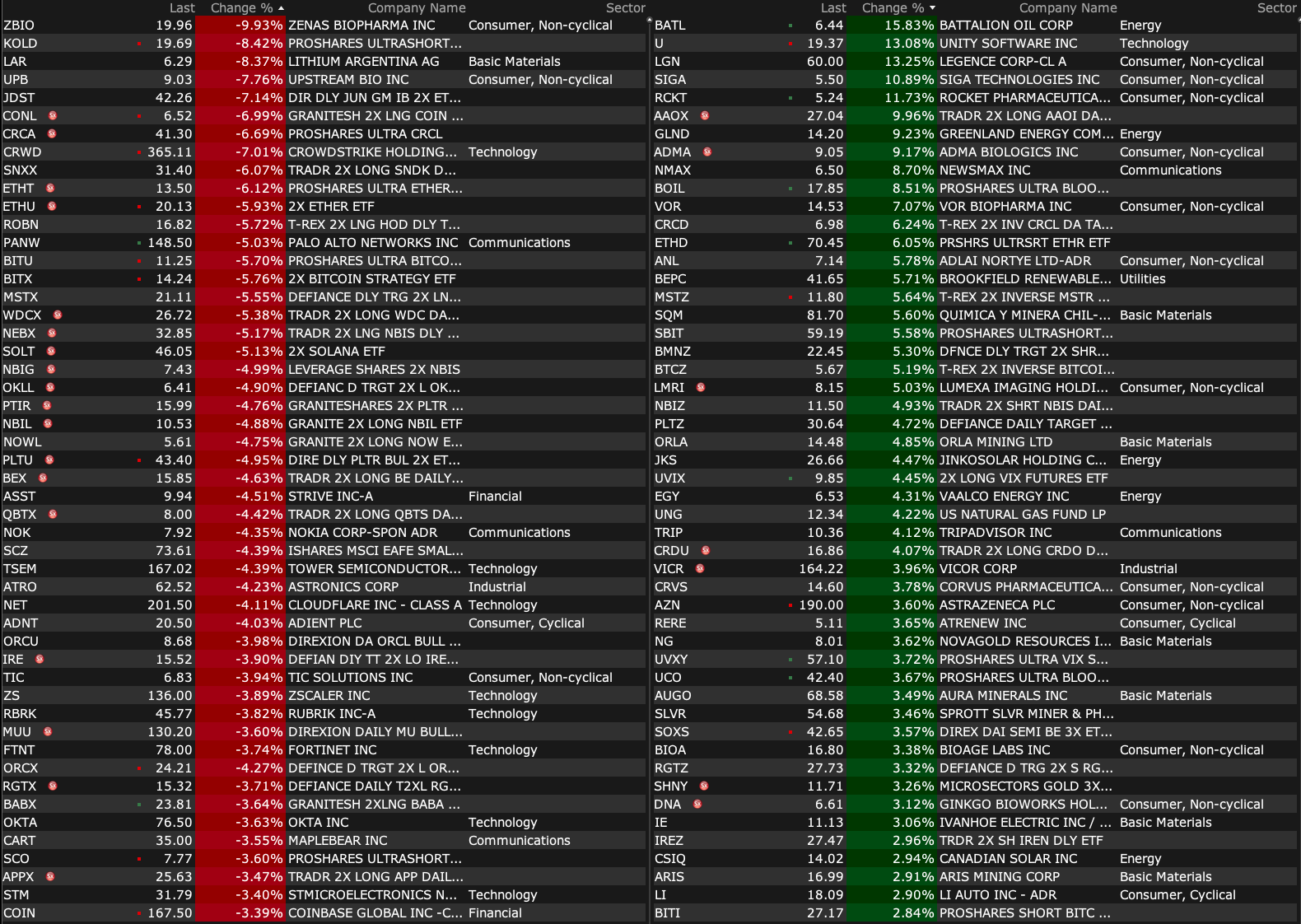

Friday's After-Hours Advancers and Decliners

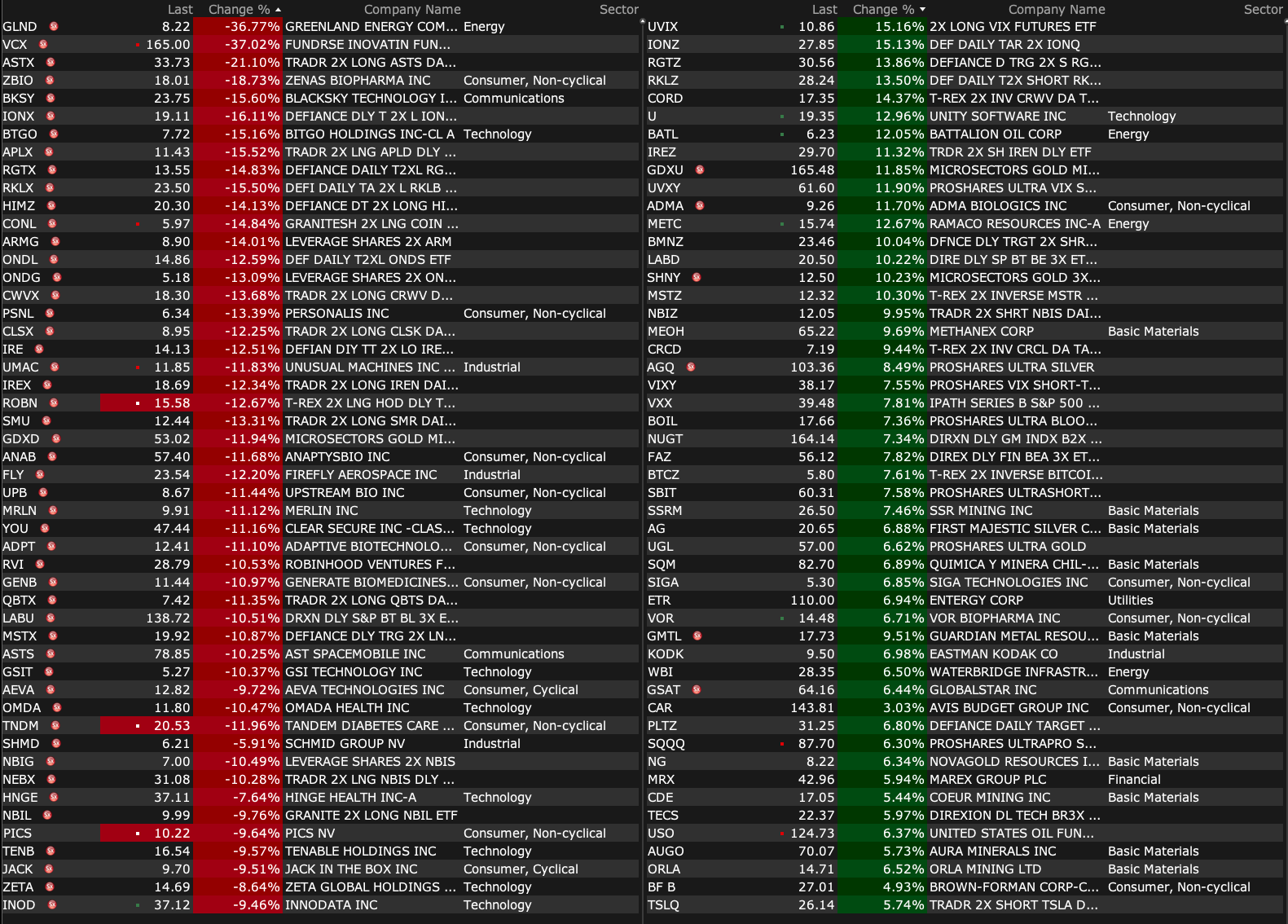

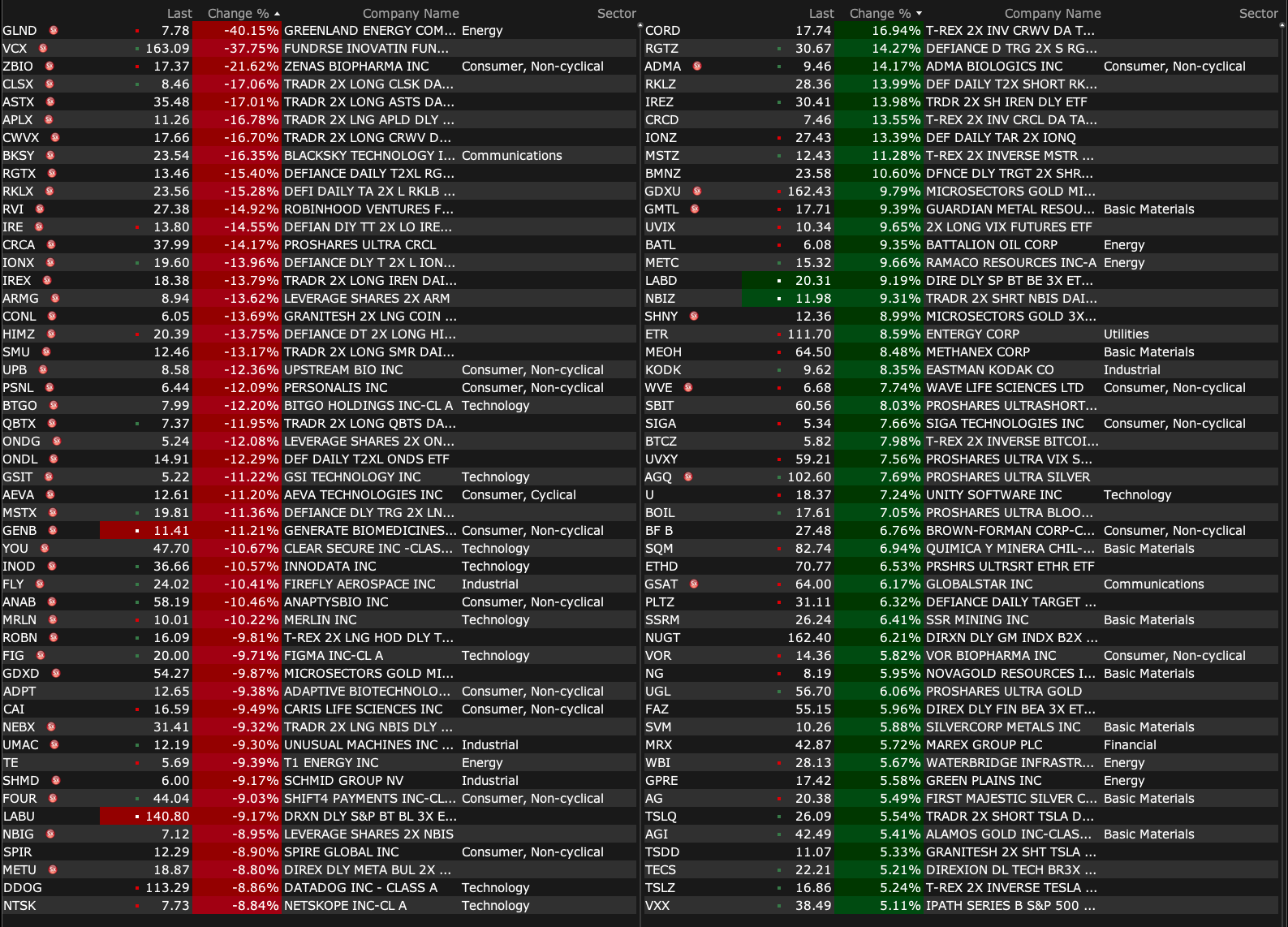

After-Hours % Advancers

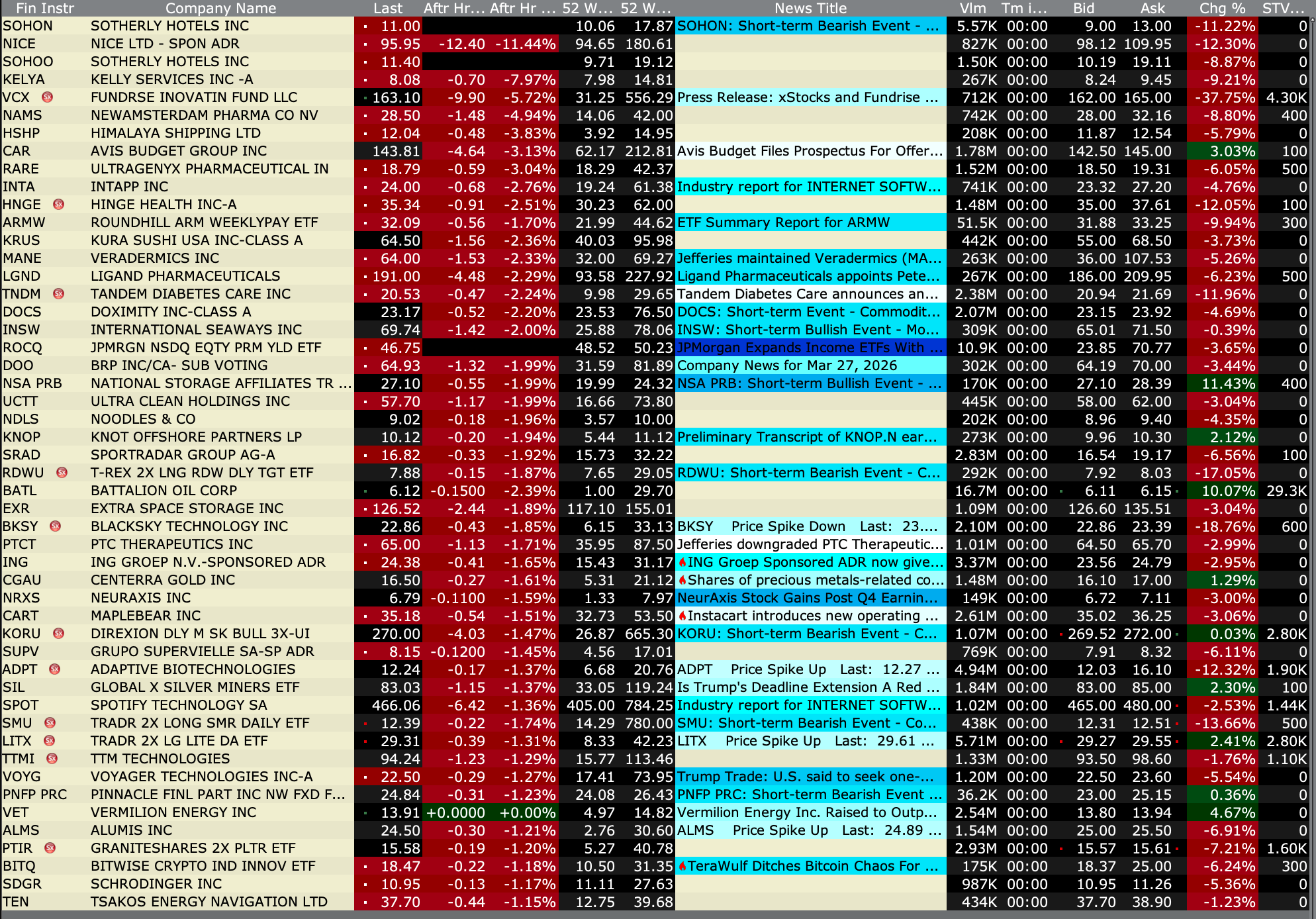

After-Hours % Decliners

BY Doug Kass · Mar 27, 2026, 4:40 PM EDT

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · Mar 27, 2026, 4:40 PM EDT

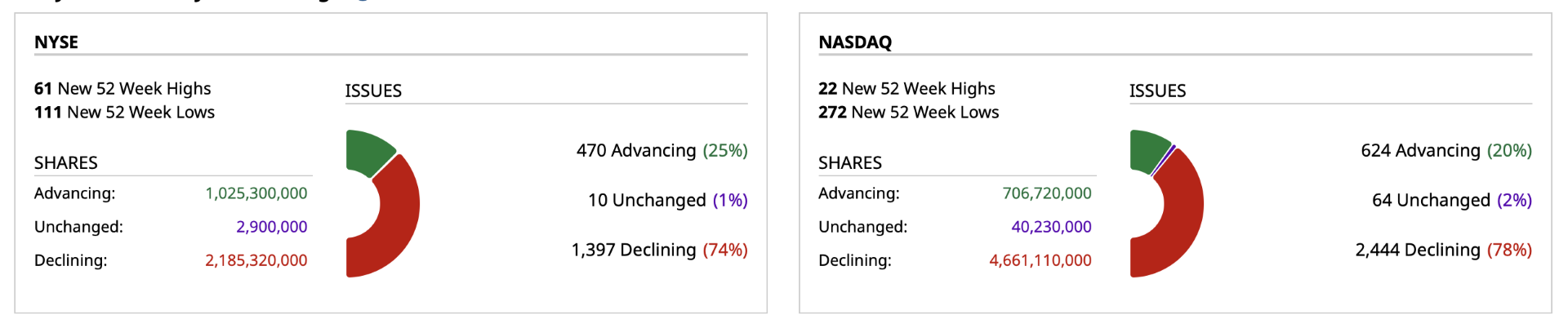

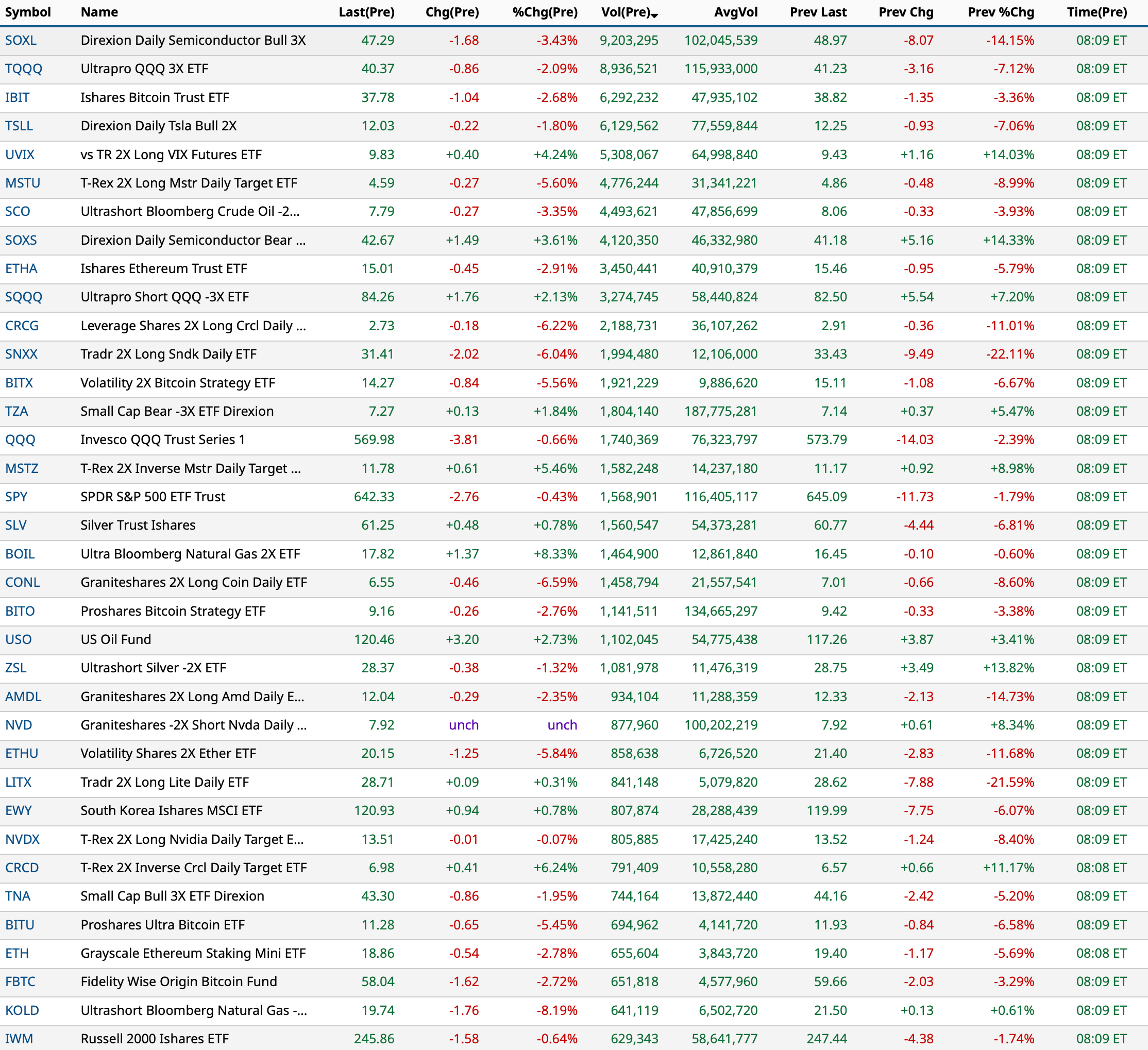

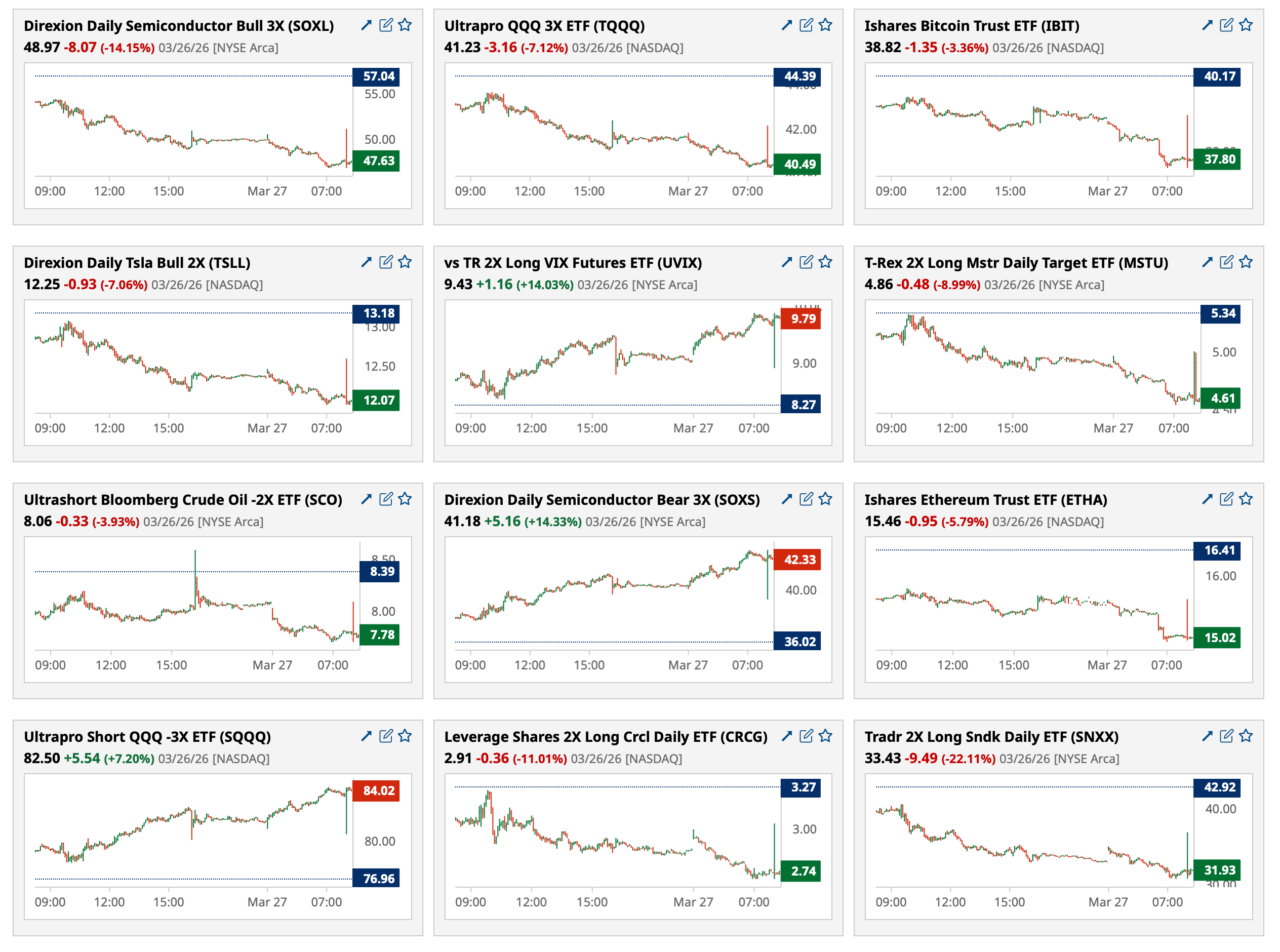

Closing Volume

- NYSE volume 11% below its one-month average

- NASDAQ volume 1.5% below its one-month average

- VIX index: up 13.34% to 31.10

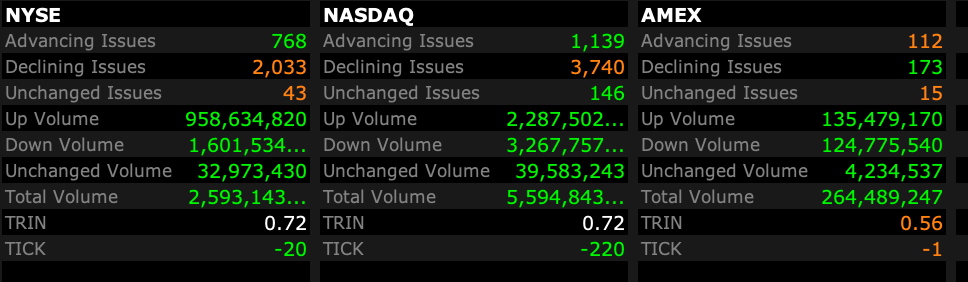

Breadth

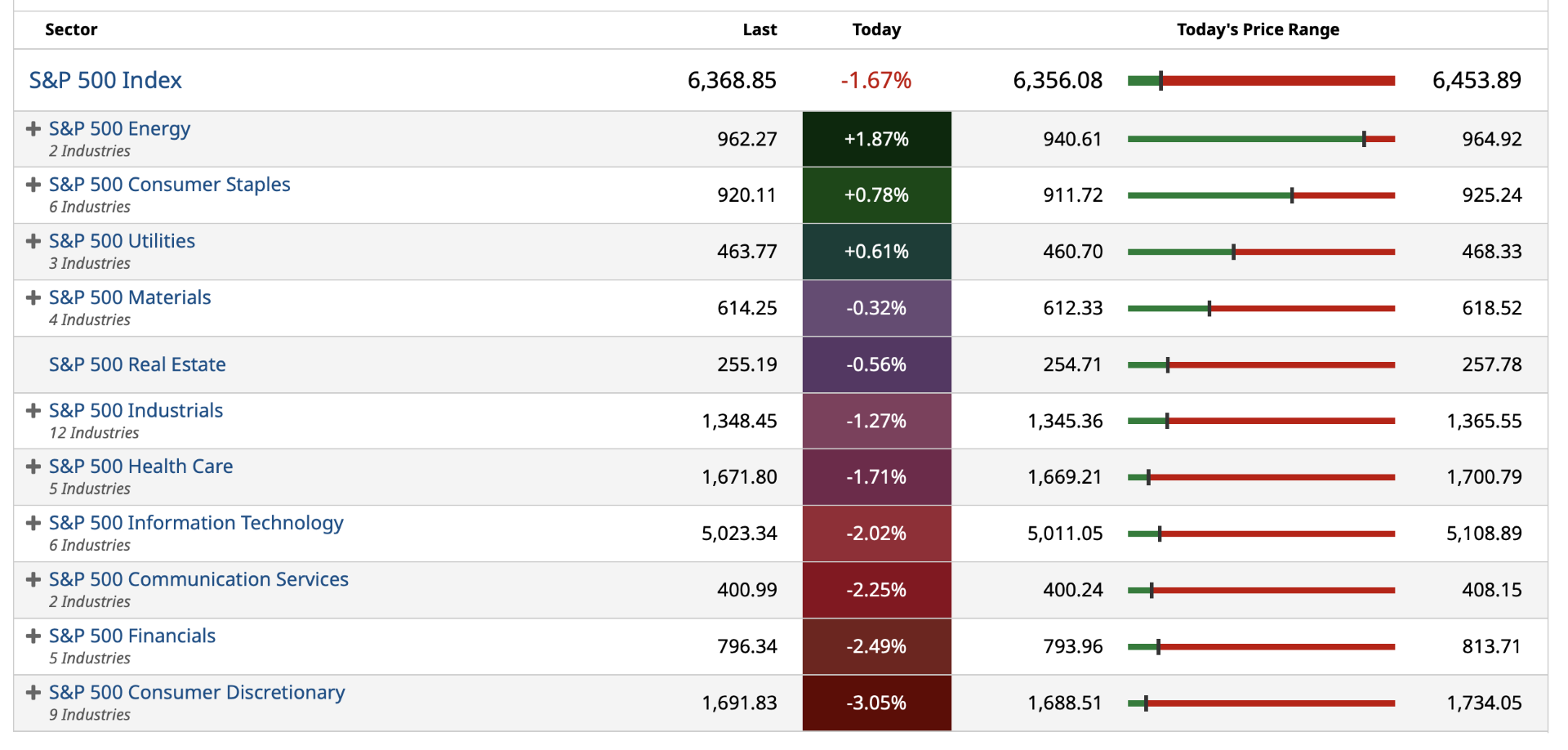

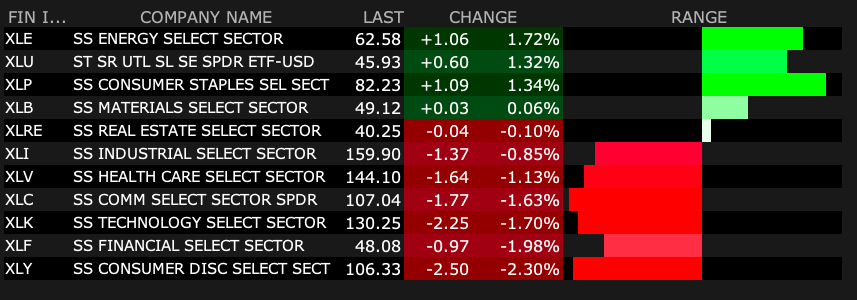

S&P 500 Sectors

% Movers

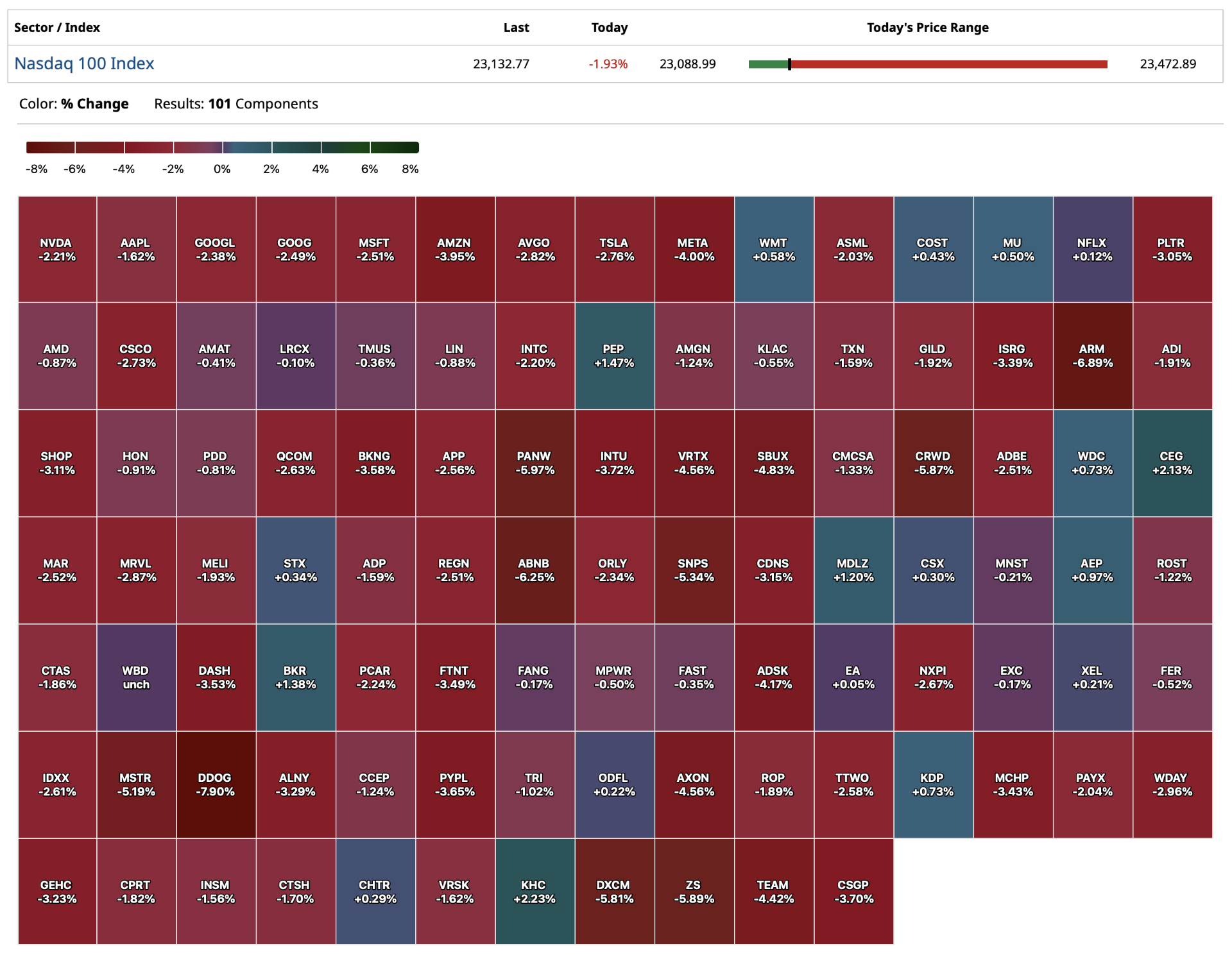

Nasdaq 100 Heat Map

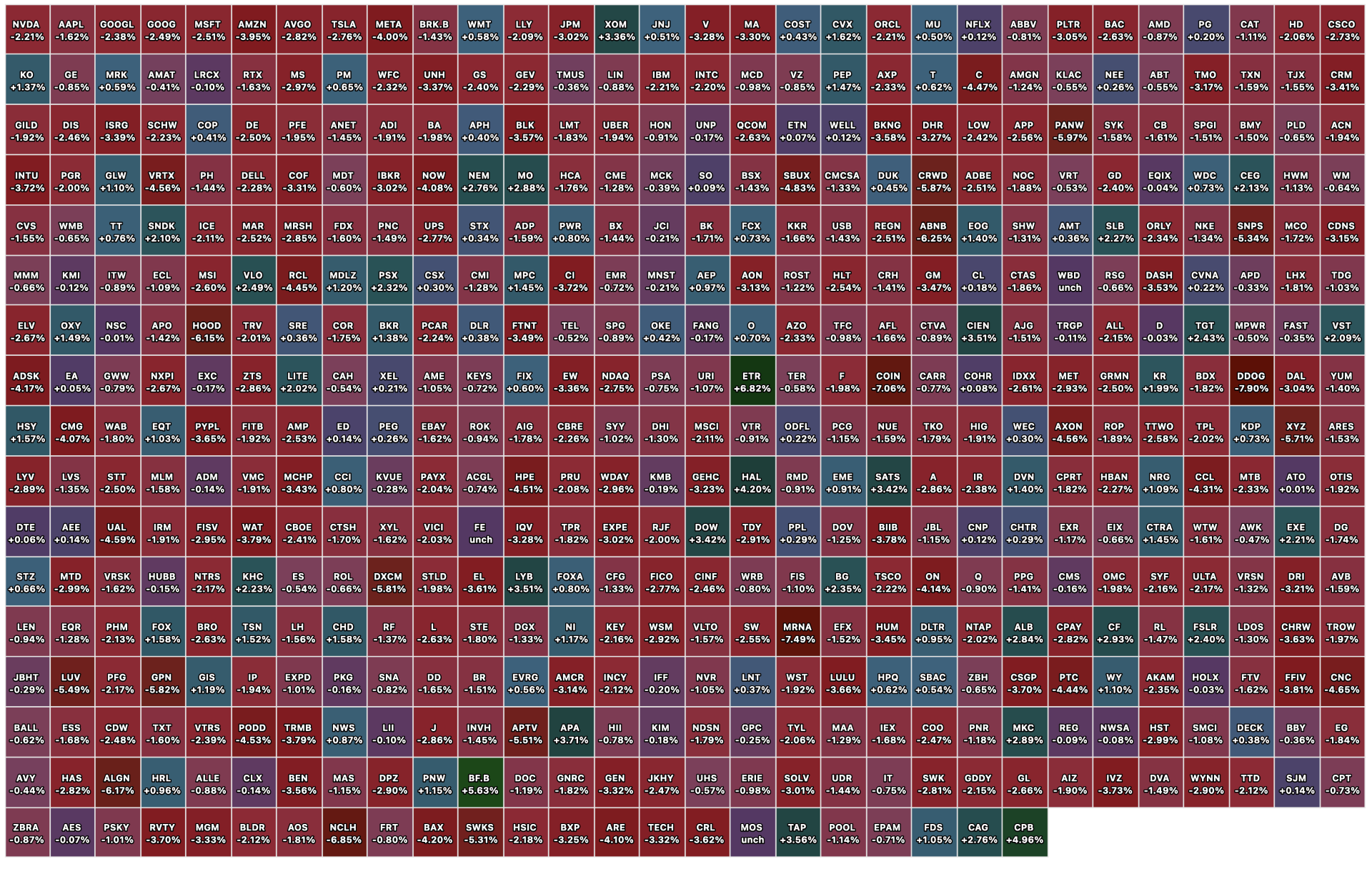

Closing S&P 500 Heat Map

BY Doug Kass · Mar 27, 2026, 4:31 PM EDT

I am calling it a day, a bit early.

Thanks for reading my Diary today and all week.

I hope my output was helpful.

Enjoy the weekend.

Be safe.

BY Doug Kass · Mar 27, 2026, 3:40 PM EDT

(PEP) is +$3.45 today. I am letting some go.

Position: Long PEP (VS)

BY Doug Kass · Mar 27, 2026, 3:05 PM EDT

Nasdaq’s forward PE valuation premium over the S&P 500 is just 4.4%, the smallest since January 2019. As recently as October, the premium stood at 35.7%: BBG pic.twitter.com/Jynj0oDSl0

— zerohedge (@zerohedge)

BY Doug Kass · Mar 27, 2026, 2:50 PM EDT

Barring a yuuuuge rally into the close, the S&P 500 will have risen only 3 of the first 12 weeks of the year.

— Jason Goepfert (@jasongoepfert)

That's tied for the worst ever. pic.twitter.com/015dH0ndV9

BY Doug Kass · Mar 27, 2026, 2:35 PM EDT

From Peter Boockvar:

Positives,

1) It seems from all the signaling that we are trying hard to negotiate an end to the war.

2) For the week ended 3/21, initial claims rose by 5k to 210k as expected but still remaining very low. The 4 week average was unchanged at 211k. Continuing claims, for the week ended 3/14, fell to 1.819mm from 1.851mm which interestingly is the lowest since May 2024.

3) At least from the perspective of the US oil/gas patch, in the first release since the war and oil price spike, the Dallas Fed released its Q1 Energy Survey and not surprisingly the index went from -6.2 in Q4 to 21 and the outlook rose from -15.2 to +32.2. However, “Oil and gas production was little changed in the first quarter, according to executives at exploration and production firms. The oil production index increased slightly from -3.4 to 0. Similarly, the natural gas production index edged higher from 0 to 2.3.”

4) From Chewy: “Pet is a uniquely attractive industry fueled by increasing pet humanization, premium product adoption and expanding lifetime value per household. Spending in this category is driven by an emotional attachment and recurring non-discretionary needs, which translates into resilient demand across economic cycles. We expect 2026 pet industry dynamics to largely mirror 2025, steady and resilient to macro trends, but without cyclical acceleration. Pet household formation appears stable with no evidence of deterioration.” And, “When we look across the business, across customer engagement, retention, overall spend behavior, the trends we see remain stable and consistent with what we’ve seen over the past several quarters.”

5) From Smithfield Foods: “Protein demand is strong and growing across consumer demographics, valued for its nutrition and health benefits.”

6) The March French business confidence index held at 97, one point above the estimate. A drop in manufacturing confidence was offset by a lift in retail, employment and construction confidence. Services were unchanged.

7) Spanish inflation in March rose 3.3% y/o/y up from 2.5% in February because of higher fuel prices but that wasn’t as bad as the estimate of up 3.8%.

8) I got home at 1am last night from my baseball fantasy draft and why there was no morning comment today but Spring has officially begun with Opening Day!

Negatives,

1) It seems that from all the signaling, the Iranian regime is not going anywhere.

2) We saw a weak set of US Treasury auctions of 2s, 5s and 7s and the US 10 yr approaches 4.50%. The rise in global bond yields is global too.

3) February import prices rose 1.3% m/o/m, about double the estimate of up .6% and also comes off an upward revision to January which saw an .8% rise vs the initial print of up .4%. Prices ex food and fuels saw prices rise by 1.2% in the month and are now up 3% y/o/y. They are up 2.8% y/o/y ex fuels. This of course before the events in March.

4) The CRB Food Stuff index moves up to the highest since November 2025.

5) A gallon of gasoline at the pump rises to just shy of $4 on average nationally according to AAA.

6) Container shipping prices continue to rise but as the Houthi’s haven’t yet disrupted the Red Sea, they still remain relatively muted. The Shanghai to LA trip rose by $95 to $2,686 to the highest since mid January. The route to NY rose by a similar amount to $3,393 and to Rotterdam, Netherlands from Shanghai too to $2,552.

7) The jump in mortgage rates and maybe some of the change in consumer psyche KB Home talked about was reflected in weekly mortgage applications where purchases fell 5.4% w/o/w. With refi’s, solely driven by rates, dropped by 14.6% after falling by 18.5% in the week before. The average 30 yr mortgage rate has moved up to 6.43% from 6.09% just before the war.

8) These were some of the comments from S&P Global in their March US PMI on manufacturing and services (that miss key sectors like retail/wholesale trade and construction) where the former was 52.4 vs 51.6 in February and the latter was 51.1 vs 51.7 in the month before: “The service sector was harder hit as manufacturers reported an upturn in output and new order book growth. A similar divergence was also seen regarding output expectations, with a weaker outlook among service providers contrasting with a more upbeat perspective among manufacturers, the latter buoyed in part by fewer tariff related worries. However, overall private sector confidence declined and contributed to the first fall in employment for over a year.” Also of note, “Average input costs meanwhile rose at a sharp rate again, posting the largest monthly increase for ten months and feeding through to the largest increase in average selling prices since August 2022. Higher prices were widely linked to the war related spike in energy costs and tightening supply conditions. Supplier delivery times in manufacturing lengthened to the greatest extent since October 2022.”

9) The final March UoM consumer confidence index fell to 53.3 from 56.6 and slightly below the estimate of 54 with both components lower. Not surprisingly, one year inflation expectations rose to 3.8% from 3.4% but the 5-10 yr guess slipped to 3.2% from 3.3%. As expected, those that think gas prices rise in the coming year jumped to 61 from 34. The employment index fell 4 pts m/o/m but the income side was less negative. Buying intentions were little changed which in light of what is going on, is a victory for now. The bottom line from the UoM, “The persistence of high prices continues to be the dominant factor for consumer views of the economy, with 47% of consumers spontaneously noting that prices are currently eroding their personal finances…Consumers with middle and higher incomes and stock wealth, buffeted both by escalating gas prices and volatile financial markets in the wake of the Iran conflict, exhibited particularly large drops in sentiment.”

10) March manufacturing index from Richmond Fed rose 10 pts from -10 to 0.

11) From Paychex: “on the macro side, I think what we said is and what we see is that it has been relatively stable. It’s really a low fire and a low hire type of environment right now. We’ve not seen a significant change in this fiscal year in terms of the small business index that we report. And again, I think we are in a dynamic environment right now where, again, what we hear from clients, particularly in the small end of the market, less than 50, is a continued inability to find qualified people for the jobs that they have open, and we are doing a lot of things to try to support them there. And then I think you have got a degree of potential hesitancy to add in this uncertain environment as you move up market.”

12) From KB Home: “Consumers have been faced with a variety of challenges over the past two years. And the conflict in the Middle East that began at the end of February has added another layer of uncertainty. Against this backdrop, and taking into consideration that our net orders in the first quarter were below the level we needed to hold our prior full year delivery guidance, we are lowering our range for the year…Near term, buyers continue to demonstrate the desire for homeownership and the ability to qualify, although tepid consumer confidence, elevated mortgage interest rates, and affordability pressures have stifled underlying demand.”

13) More stories like this I’m hearing/reading: From Nikkei News, “Japan relies on the Middle East for more than 40% of its supply of naphtha, which has become tougher to procure...Although around 40% of demand is met through domestic supply, this is produced from crude oil, more than 90% of which is imported from the Middle East. At least six of Japan’s 12 ethylene production facilities have cut production to conserve naphtha.”

14) From a Bloomberg News article, “Sulfur is trading at an 18 year high as key Persian Gulf supplies are kept off the market.” Not only is sulfur used to make sulfuric acid which is a key input to making the fertilizer phosphate, but it’s also used for the leaching process in mining copper and other metals to strip the metal from the ore. “In normal times, more than 90% of sulfur supply to the African copper belt, which uses about 1.2 million tons a year to extract metal from ores, is shipped via Hormuz...Inventories at the Tanzanian port of Dar es Salaam, a key sulfur storage hub for African miners, should last two months, but concerns are growing over the risk of a protracted supply shock,” said Argus in the article.

15) And another, “Signs are growing that Asian countries are hoarding jet fuel after the Iran war sent oil prices surging, reflecting growing strain on the aviation industry. South Korean carriers got notified about refueling restrictions from some countries and the government is discussing whether to redirect export bound jet fuel to the local market, the nation’s transport ministry said in a statement to Bloomberg on Wednesday. Philippine Airlines president said in an interview that the Southeast Asian nation may soon resort to fuel rationing. In Vietnam, the aviation agency warned of potential jeet fuel shortages from early April and is cutting flights as a result.”

16) From gCaptain: “Over 80% of the world’s 454 ports mapped are deemed in critical status, 60-70% are severely congested, and 45-59% are considered highly congested.” According to a market analyst at Xeneta, “This shows the impact of the three waves of disrupted cargo. The first wave was vessels already in or near the Persian Gulf when the conflict started, the second wave was vessels that departed from Asia before suspensions were announced, and the third wave is of cargo bookings currently being made.” As a result, “All of this has led to the deterioration of vessel schedules.”

17) The March German IFO business confidence index fell 2 pts m/o/m to 86.4, the lowest since February 2025, with all of the weakness in the Expectations component as the Current Assessment was unchanged. IFO stated the obvious, “Uncertainty among companies has increased noticeably. The war in Iran has put any hope of a recovery on ice for the time being.”

18) On the heels of the RBA rate increase last week, the pre war, February Australian trimmed mean CPI rose 3.3% y/o/y, the same pace seen in January while the headline figure rose 3.7%.

19) In the UK, February CPI was up 3% y/o/y as expected with a core rate increase of 3.2% because of continued high inflation in services which rose 4.3% y/o/y. PPI jumped .8% m/o/m, above the estimate of .5% but all of this is old news as we know.

20) The March UK PMI dropped to 51 from 53.7 with most of the decline led by services which went to 51.2 from 53.9. Manufacturing was down by just .3 pts m/o/m to 51.4. S&P Global said succinctly, “The war in the Middle East has hit the UK economy in March, stalling growth while driving inflation sharply higher.” Further, “Output growth across manufacturing and services has slowed to a crawl as companies blamed lost business directly on the events in the Middle East, whether through heightened risk aversion among customers, surging price pressures, higher interest rates, or via travel and supply chain disruptions.” And, “Inflationary pressures have surged higher on the back of rising energy prices and fractured supply chains. The acceleration in cost growth in the manufacturing sector was especially severe, being the sharpest since the depreciation of sterling following Black Wednesday in 1992.” I bolded to highlight.

21) The March Eurozone PMI fell to 50.5 from 51.9 but interestingly the manufacturing component lifted to 51.4 from 50.8 (but maybe due to the jump in supplier deliveries because of slowing supply chains) with the services side seeing the weakness, down to 50.1 from 51.9. S&P Global said “The flash Eurozone PMI is ringing stagflation alarm bells as the war in the Middle East drives prices sharply higher while stifling growth. Firms’ costs are rising at the fastest rate for over three years amid the surge in energy prices and choking of supply chains resulting from the war. Supplier delays have jumped to their highest since mid-2022, largely linked to shipping issues.” To quantify, “The survey data are indicative of Eurozone GDP growth slowing to a quarterly rate of just below .1% in March with the forward looking indicators pointing to a heightened risk of a downturn in the coming months. The survey’s price gauge is meanwhile indicative of consumer price inflation accelerating close to 3%, with cost pressure likely to add still further to selling price inflation in the coming months.”

22) Japan’s composite March PMI held above 50 at 52.5 vs 53.9 in February with both components lower. S&P Global said, “The slowdown coincides with the recent outbreak of the war in the Middle East, which contributed to a sharp rise in input costs amid reports of supply chain difficulties and higher prices for fuel. A weak yen exchange rate and rising labor costs also contributed to the upturn in expenses, further adding to the squeeze on company margins.”

23) Australia’s March PMI fell to 47 from 52.4, mostly driven by the drop in services to 46.6 from 52.8. Manufacturing stayed above 50, barely, at 50.1 vs 51 last month. S&P Global said, “Businesses faced steep cost pressures, with the rate of inflation at a more than 3 year high. At least some of this increased cost burden was passed through to customers, however, with selling prices rising at the sharpest rate since August 2023…Qualitative evidence linked lower output to a deterioration in demand conditions, in part a reflection of global uncertainty and economic disruption due to the Middle East war.”

24) India remains an economic standout but certainly not immune to what is going on as they import much of their energy needs and the rupee continues to weaken. Its PMI fell to 56.5 from 58.9 with most of the decline in manufacturing which went to 53.8 from 56.9. Services slipped by .9 pts to 57.2. S&P Global said, “The largest slowdown was seen at goods producers, who reported that the war in the Middle East weighed on production growth by exacerbating market instability, driving inflationary pressures higher and restricting demand through heightened future uncertainty among clients and end consumers. March’s increase in factory output was the softest since August 2021.”

BY Doug Kass · Mar 27, 2026, 2:15 PM EDT

The only green is seen in staples and energy.

Position: Long PEP (S), PG (S), KMB (S)

BY Doug Kass · Mar 27, 2026, 1:58 PM EDT

Breadth

S&P 500 Sector ETFs

% Movers

BY Doug Kass · Mar 27, 2026, 1:50 PM EDT

I have another research call at 1:45 PM. Back by 2:30 PM.

BY Doug Kass · Mar 27, 2026, 1:46 PM EDT

The view from Apollo chief economist Torsten Slok:

— Luke Kawa (@LJKawa)

“Markets are overreacting to what will likely be a 4- to 6-week period of volatility, which will ultimately result in 50 years of stability in oil markets, supply chains and geopolitics.”

BY Doug Kass · Mar 27, 2026, 1:10 PM EDT

BY Doug Kass · Mar 27, 2026, 12:55 PM EDT

It is remarkable to me that Fin TV panelists @HalftimeReport @ScottWapnerCNBC actually believe that the prospects for S&P EPS growth in 2026 is stronger today than it was a month ago.

— Dougie Kass (@DougKass)

To think that higher interest rates and substantially higher inflationary influences (energy,… https://t.co/Y4IUT026N1

BY Doug Kass · Mar 27, 2026, 12:50 PM EDT

Remember, nearly EVERY opinion that was confidentally delivered on @cnbc over the last two months were totally wrong:

— Dougie Kass (@DougKass)

1. There is economic risk. (The threat to global economic growth is obvious)

2 There is geopolitical risk (Duh!)

3. There is interest rate and inflation risk.… https://t.co/Y4IUT026N1

BY Doug Kass · Mar 27, 2026, 12:35 PM EDT

I have covered my CoreWeave (CRWV) short at $74.97. It's -$6/share on the day and considerably lower than my cost basis of the short.

This is my third trade in the name.

BY Doug Kass · Mar 27, 2026, 12:03 PM EDT

Two of my favorite investment people, Dan Greenhaus and Dan Nathan, participate in this podcast "How To Invest in Volatile Markets."

Run don't walk to watch the two Dans!

How To Invest In Volatile Markets with Dan Greenhaus - YouTube

BY Doug Kass · Mar 27, 2026, 11:50 AM EDT

BY Doug Kass · Mar 27, 2026, 11:30 AM EDT

With S&P cash -65 handles I am seeing some "stability" in the tech sector for the first time in several days.

None.

BY Doug Kass · Mar 27, 2026, 10:58 AM EDT

I have two research calls from 10:45 a.m. to noon.

None

BY Doug Kass · Mar 27, 2026, 10:49 AM EDT

Bidding for more (MSOS) and (MSOX) now.

Long MSOS L MSOX S

BY Doug Kass · Mar 27, 2026, 10:39 AM EDT

BY Doug Kass · Mar 27, 2026, 9:52 AM EDT

*OAKTREE WILL MEET 8.5% PRIVATE CREDIT FUND REDEMPTIONS IN FULL

— Negligible Capital (@negligible_cap)

Oaktree Strategic Credit Fund is honoring all redemptions, with $BN providing $80B

“The Oaktree fund will repurchase 6.8% of its own shares, while Brookfield agreed to buy an additional 1.7% from a single investor… pic.twitter.com/jSWnLvuEMu

None.

BY Doug Kass · Mar 27, 2026, 9:45 AM EDT

-ARTL +176% (withdraws registration for stock offering)

-ONCO +51% (momentum)

-RBNE +23% (momentum)

-U +16% (earnings, guidance)

-LTRN +12% (US FDA clears subsidiary Starlight Therapeutics' IND for Planned STAR-001 (LP-184) Phase 1 Pediatric CNS Cancer Trial with 18 to 42 patients planned across about 15 centers)

-AGX +10% (earnings)

-RCKT +8.5% (US FDA Approves Kresladi (marnetegragene autotemcel), first Gene Therapy for Severe Leukocyte Adhesion Deficiency Type I)

-VOR +6.6% (to sell 5.34M shares at $14.05/shr in private placement)

-ETR +5.9% (signs agreement with Meta that will deliver an additional $2B in customer savings)

-AZN +3.8% (Tozorakimab met main endpoint in two Phase III COPD trials)

-CJMB +2.8% (supports U.S. Scale-Up of Multi-Indication Immune Platform, including JKB-122, with Phase 2b/3 Advancement)

-TFX +2.7% (Irenic Capital Management, LP (2% stakeholder) urges Teleflex board to engage with buyers; Raymond James Raised TFX to Outperform from Market Perform, price target: $128)

-PRMB +2.0% (Jefferies Raised PRMB to Buy from Hold, price target: $25)

-DTCX -29% (prices common stock offering)

-RPD -4.4% (acquires Kenzo Security)

-COIN -3.3% (crypto weakness)

None.

BY Doug Kass · Mar 27, 2026, 9:27 AM EDT

I moved to medium-sized long indexes:

* (SPY) $641.28

* (QQQ) $569.10

Long SPY Common M QQQ Common M; Short SPY Calls S QQQ Calls S

BY Doug Kass · Mar 27, 2026, 9:23 AM EDT

11:00 a.m.: Fed Bank of Richmond President Barkin (Non-Voter) speaks before the Appalachian Highlands Economic Forum, Johnson City, TN (No livestream. Text available at richmondfed.org at speech time. Moderated Q&A expected);

11:30 a.m.: Fed Bank of San Francisco President Daly (Non-Voter) gives introductory remarks before the Macroeconomics and Monetary Policy Conference hosted by the Federal Reserve Bank of San Francisco, San Francisco, CA (Other details TBA)’

11:35 a.m.: Fed Bank of Philadelphia President Paulson (Voter) speaks before the Macroeconomics and Monetary Policy Conference hosted by the Federal Reserve Bank of San Francisco, San Francisco, CA (Other details TBA)

None.

BY Doug Kass · Mar 27, 2026, 9:15 AM EDT

None.

BY Doug Kass · Mar 27, 2026, 9:10 AM EDT

In today's Early Look: "#Quad3 Imploding The Mother Of All Bubbles"

— Keith McCullough (@KeithMcCullough)

60/40 portfolios. 50 and 200-day Simple Moving Monkeys. Gaussian distributions. All relics of an age that decided the market was a machine with predictable gears — not a living system that breathes, adapts, and… pic.twitter.com/YFSoNufKMY

BY Doug Kass · Mar 27, 2026, 9:05 AM EDT

To everything - turn, turn, turn

There is a season - turn, turn, turn

And a time to every purpose under heaven

A time to be born, a time to die

A time to plant, a time to reap

A time to kill, a time to heal

A time to laugh, a time to weep

To everything - turn, turn, turn

There is a season - turn, turn, turn

And a time to every purpose under heaven

A time to build up, a time to break down

A time to dance, a time to mourn

A time to cast away stones

A time to gather stones together

- The Byrds "Turn! Turn! Turn!" on The Ed Sullivan Show

To everything there is a season - even to the "generational compounders":

Mag 7 now down ~15% from the highs ... approaching the Summer 2024 in terms of magnitude of drawdown. - GS pic.twitter.com/JssKABGFGf

— Ayesha Tariq, CFA (@AyeshaTariq)

None.

BY Doug Kass · Mar 27, 2026, 8:40 AM EDT

None.

BY Doug Kass · Mar 27, 2026, 8:30 AM EDT

Citi with a recession shout out:

— Brian Sozzi (@BrianSozzi)

"The Middle East turmoil presents significant downside risks for the global economy. While our baseline growth forecast for 2026 is only slightly lower from February, more severe scenarios could drag global growth below 2%, push headline…

BY Doug Kass · Mar 27, 2026, 8:15 AM EDT

* I remain of the view that the Iranian conflict is "at the beginning of the end" ... and I am expanding my small net long exposure

It is my core belief that both the U.S. and Iran are aggressively looking for an off ramp to their conflict.

That said, there remains a lot of skepticism, as illustrated by the partial Administration's "TACO" after the close of trading Thursday in which President Trump instituted a lengthier 10-day pause for negotiations — yet stocks only briefly rallied (and, based on stock futures are now modestly lower than Thursday's close).

Despite the market's skepticism, the news yesterday continues to underscore my more constructive comments made earlier this week (excerpted from below):

Both parties, for different reasons, need to come to an agreement.

"Iran has been devastated and is likely defenseless going forward. They will continue to use aggressive rhetoric because that is what regimes that are about to be defeated do.

The Trump Administration doesn't want the conflict to linger. There is an upcoming election in November, oil prices are a regressive tax (hurting those least able to tolerate the increase) and the stock market will likely be imperiled by any further escalation in the conflict. Meanwhile, interest rates and inflationary expectations are rising."

My complete column from Wednesday:

* We are now likely "at the beginning of the end" of the conflict in Iran...

… One can have a broken heart

living in misery.

Two can really ease the pain

like a perfect remedy.

One can be alone in a bar,

like an island he's all alone.

Two can make just any place

seem just like bein' at home.

- Marvin Gaye and Kim Weston, It Takes Two Baby Frankie Gaye And Kim Weston - It Takes Two

Both parties, for different reasons, need to come to an agreement.

Iran has been devastated and is likely defenseless going forward. They will continue to use aggressive rhetoric because that is what regimes that are about to be defeated do.

The Trump Administration doesn't want the conflict to linger. There is an upcoming election in November, oil prices are a regressive tax (hurting those least able to tolerate the increase) and the stock market will likely be imperiled by any further escalation in the conflict. Meanwhile, interest rates and inflationary expectations are rising.

I remain short-term bullish and intermediate-term bearish.

Note: The use of lyrics and the double entendre ("It takes two baby") is not to meant to minimize the horrors of the Iran/U.S. conflict.

BY Doug Kass Mar 25, 2026, 2:25 PM EDT

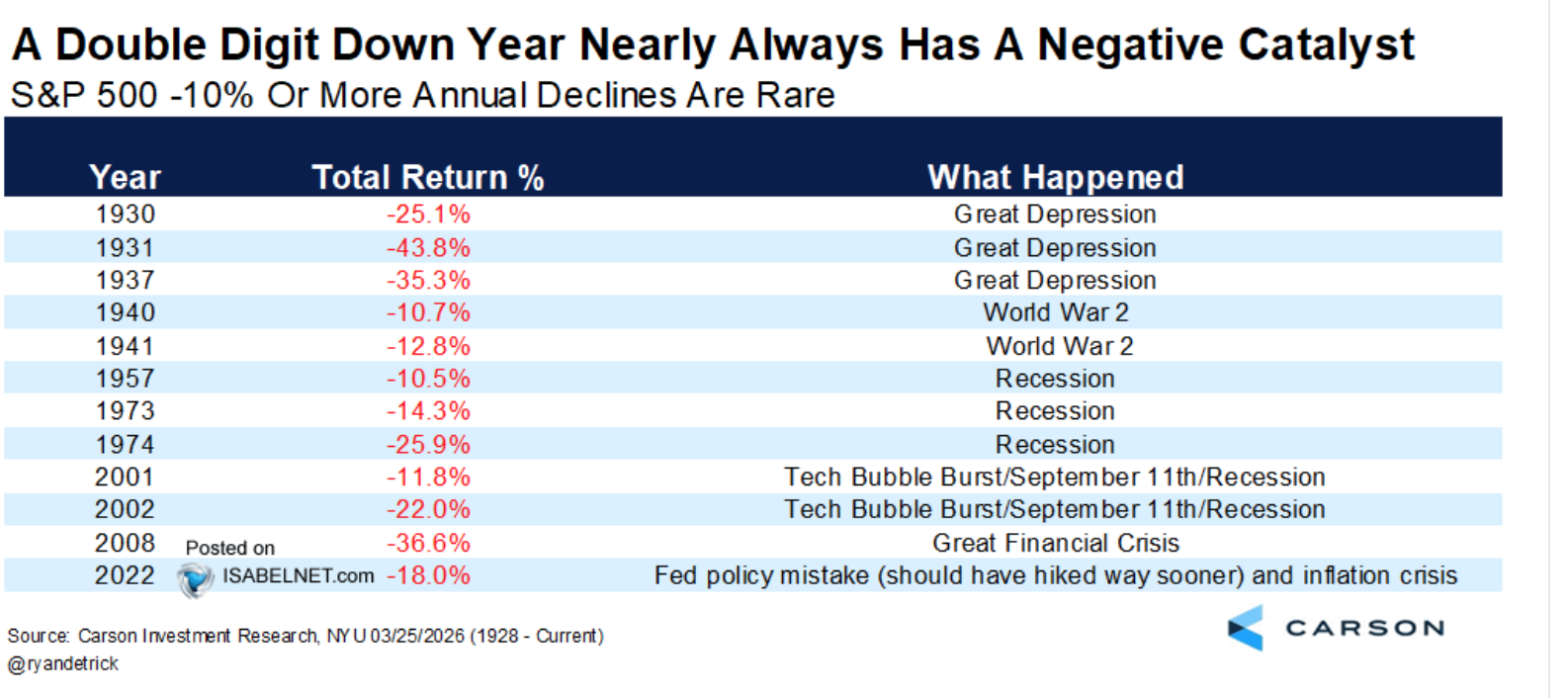

In support of my buying from my column from yesterday "Disasters Have a Way of Not Happening":

Disasters have a way of not happening. (h/t Byron Wien)

There have been only 12 data points in which the S&P Index fell by 10% or more:

For the reasons mentioned in "Growing Less Bearish" I have begun to accumulate equities — after being net short for some time.

Here are some more reasons I have begun to buy:

* The compression in valuations has been multiple driven and the swiftness of the drop in price earnings multiples was last seen five years ago during Covid:

* The price earnings ratio of the S&P Index is now one turn under the five-year average:

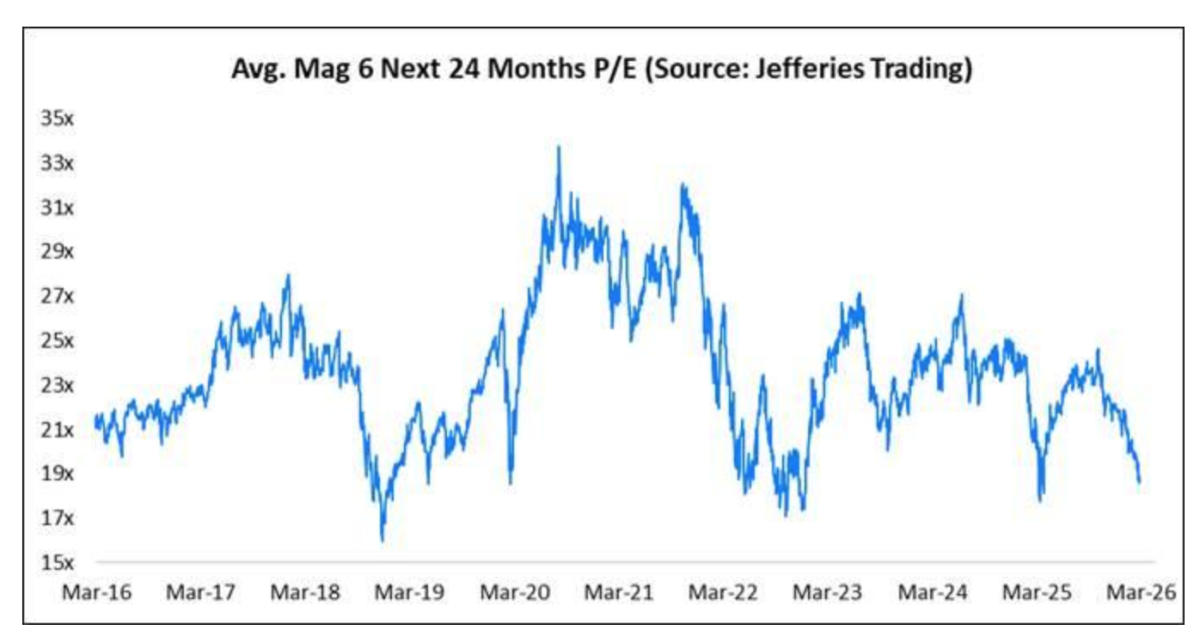

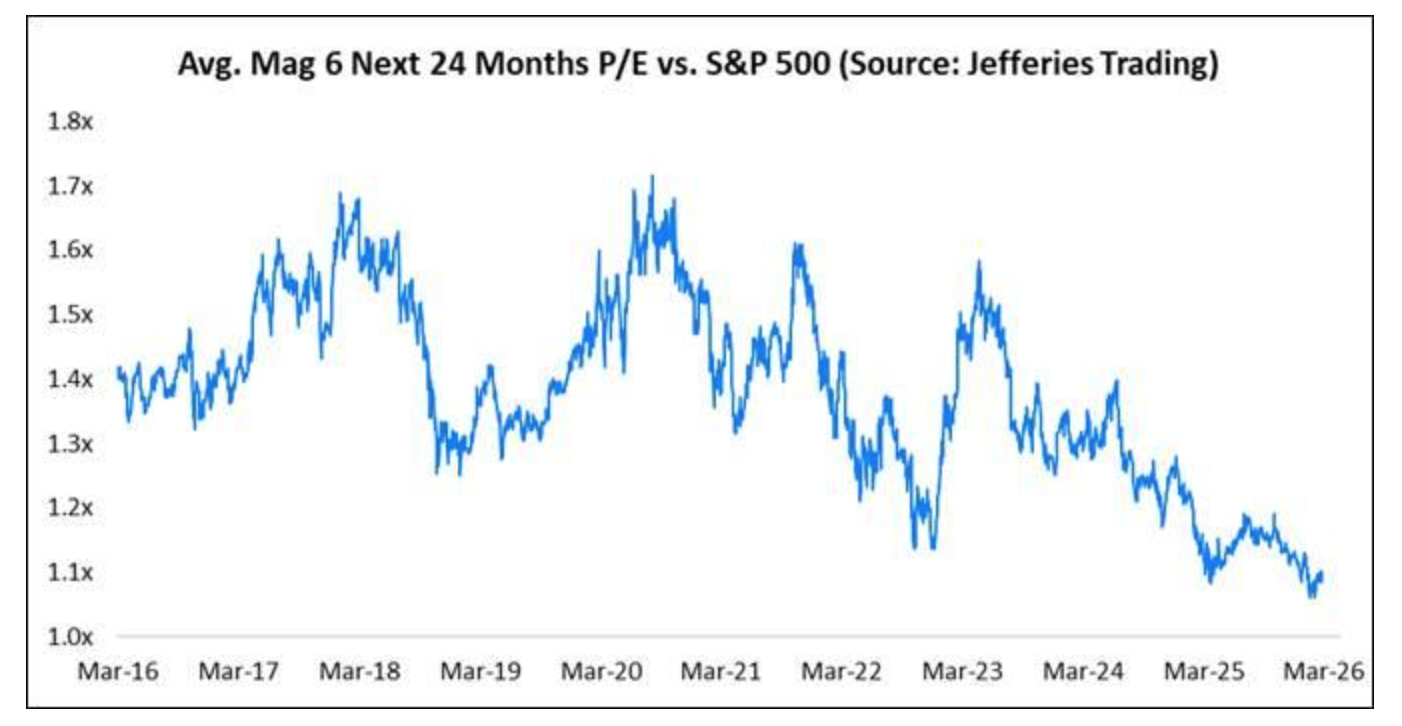

* MAG 7 valuations (excluding Tesla) are down to 19-times vs. 17-times low over the last decade:

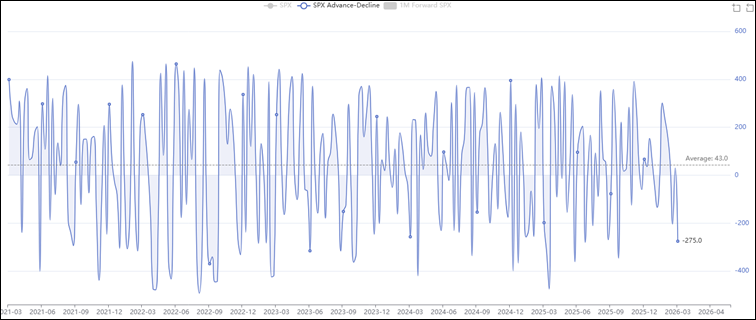

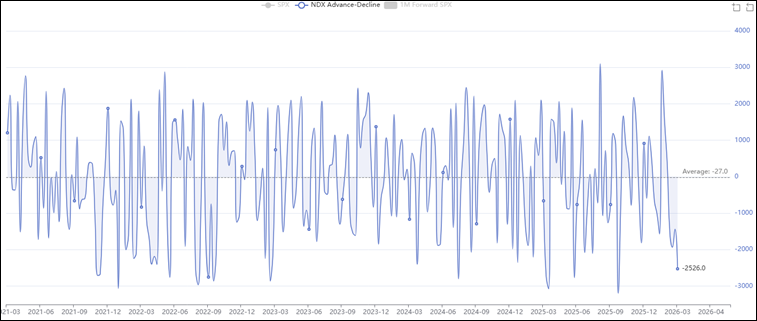

* Sentiment has deteriorated. S&P and Nasdaq advance/decline lines are near five-year lows:

BY Doug Kass · Mar 26, 2026, 9:45 AM EDT

Position: Long SPY common (S/M), QQQ (S/M); Short SPY calls (S), QQQ calls (S)

BY Doug Kass · Mar 27, 2026, 7:15 AM EDT

Tech stock valuations are back to the lows seen around the April 2025 tariff shock: pic.twitter.com/ryNMHyk0AO

— Brian Sozzi (@BrianSozzi)

BY Doug Kass · Mar 27, 2026, 7:00 AM EDT

Chart of the Day: XLE

Following its massive breakout, short interest in the Energy sector (XLE) has climbed to its highest levels since 2008.

When short interest has reached prior extremes, its often preceded multi-year advances and a sustained short squeeze.

This only adds fuel to the fire as XLE is already up roughly +38% this year, and is extremely close to having its best quarter in history.

The Takeaway: A record quarter and elevated short interest suggest this move in Energy may be far from over.

- (6) Subu Trade (@SubuTrade) / X

The Nasdaq is now in correction mode. Down 10.5% from its peak late January.

— jeroen blokland (@jsblokland)

Because no one knows how the "Iran war" will end or can end. pic.twitter.com/kfnrzU7YWk

The list of technical damage across the broader market continues to grow. Only 43% of S&P 500 stocks are holding above support from their November lows. The big question now is whether the index follows suit. pic.twitter.com/hati91LRiY

— Adam Turnquist, CMT (@adam_turnquist)

Technically, both the cap-weighted and equal-weighted indices remain in their cyclical bull markets, which started some 41 months ago in October 2022. We still have higher highs and higher lows, which are the very definition of an uptrend. Both indices are now at or below their… pic.twitter.com/PdiwyNibi6

— Jurrien Timmer (@TimmerFidelity)

Record Tech Flows

— Macro Charts (@MacroCharts)

From BofA via BBG:

- Tech had the biggest weekly inflow in client data history (2008)

- Energy, Discretionary, Financials, Staples, Utilities, and Materials all had record or near-record outflows pic.twitter.com/jVSbheqh9T

Rising Oil prices have historically been positive for the performance of Transportation stocks. https://t.co/t0Eqoo4oCC $IYT $XLI $USO #Stocks pic.twitter.com/t7WLFrV5iE

— Equity Clock (@EquityClock)

This is my simplistic view of the price of oil as a gauge of war sentiment and how its price is likely to impact equities.$CL_F $USO $SPY $QQQ pic.twitter.com/uPTzZMIVPG

— Brian Shannon, CMT (@alphatrends)

As stock indexes threaten a break of 6-month lows gold is also breaking down, contrary to the expectation that it's a safe haven. The key is understanding 'real rates', which are moving higher taking the 'shine' off gold. Will discuss on @CNBC at ~ 2:30 @jillpschneider pic.twitter.com/GSchEA4gLL

— Todd Gordon (@ToddFGordon)

Bonus — Here is a great link:

BY Doug Kass · Mar 27, 2026, 6:45 AM EDT

I sold some indices at about midnight:

* (SPY) $649.12

* (QQQ) $577.60

I just (530 AM) repurchased some of the indices I sold:

* SPY $645.54

* QQQ $573.89

Position: Long SPY common (S/M), QQQ common (S/M); Short SPY calls (S), QQQ calls (S)

BY Doug Kass · Mar 27, 2026, 5:55 AM EDT

The S&P Short Range Oscillator again moved to be less oversold at -2.85% vs. -3.13%

Position: Long SPY common (S/M), QQQ common (S/M); Short SPY calls (S), QQQ calls (S)

BY Doug Kass · Mar 27, 2026, 5:46 AM EDT

The embedded tweet could not be found…

As stock indexes threaten a break of 6-month lows gold is also breaking down, contrary to the expectation that it's a safe haven. The key is understanding 'real rates', which are moving higher taking the 'shine' off gold. Will discuss on @CNBC at ~ 2:30 @jillpschneider

Technically, both the cap-weighted and equal-weighted indices remain in their cyclical bull markets, which started some 41 months ago in October 2022. We still have higher highs and higher lows, which are the very definition of an uptrend. Both indices are now at or below their Show more

Rising Oil prices have historically been positive for the performance of Transportation stocks. equityclock.com/2026/03/25/sto… $IYT

*OAKTREE WILL MEET 8.5% PRIVATE CREDIT FUND REDEMPTIONS IN FULL Oaktree Strategic Credit Fund is honoring all redemptions, with $BN providing $80B “The Oaktree fund will repurchase 6.8% of its own shares, while Brookfield agreed to buy an additional 1.7% from a single investor

Citi with a recession shout out: "The Middle East turmoil presents significant downside risks for the global economy. While our baseline growth forecast for 2026 is only slightly lower from February, more severe scenarios could drag global growth below 2%, push headlineShow more

The view from Apollo chief economist Torsten Slok: “Markets are overreacting to what will likely be a 4- to 6-week period of volatility, which will ultimately result in 50 years of stability in oil markets, supply chains and geopolitics.”

The Nasdaq is now in correction mode. Down 10.5% from its peak late January. Because no one knows how the "Iran war" will end or can end.

Remember, nearly EVERY opinion that was confidentally delivered on @cnbc over the last two months were totally wrong: 1. There is economic risk. (The threat to global economic growth is obvious) 2 There is geopolitical risk (Duh!) 3. There is interest rate and inflation risk. Show more

@TheStreet @TheStreetPro The Business Media Has Failed You * Not providing two way discourse/debate (and relying on formulaic programming) has prepared investors poorly for when the halcyon days are over and the tides starts going out... "So much for objective journalism.

It is remarkable to me that Fin TV panelists @HalftimeReport @ScottWapnerCNBC actually believe that the prospects for S&P EPS growth in 2026 is stronger today than it was a month ago. To think that higher interest rates and substantially higher inflationary influences (energy,Show more

@TheStreet @TheStreetPro The Business Media Has Failed You * Not providing two way discourse/debate (and relying on formulaic programming) has prepared investors poorly for when the halcyon days are over and the tides starts going out... "So much for objective journalism.

Tech stock valuations are back to the lows seen around the April 2025 tariff shock:

Nasdaq’s forward PE valuation premium over the S&P 500 is just 4.4%, the smallest since January 2019. As recently as October, the premium stood at 35.7%: BBG